ssstep

There may be lots of hype about U.S. shale oil manufacturing going into year-end, and let me inform you like it’s, it is nearly all fluff.

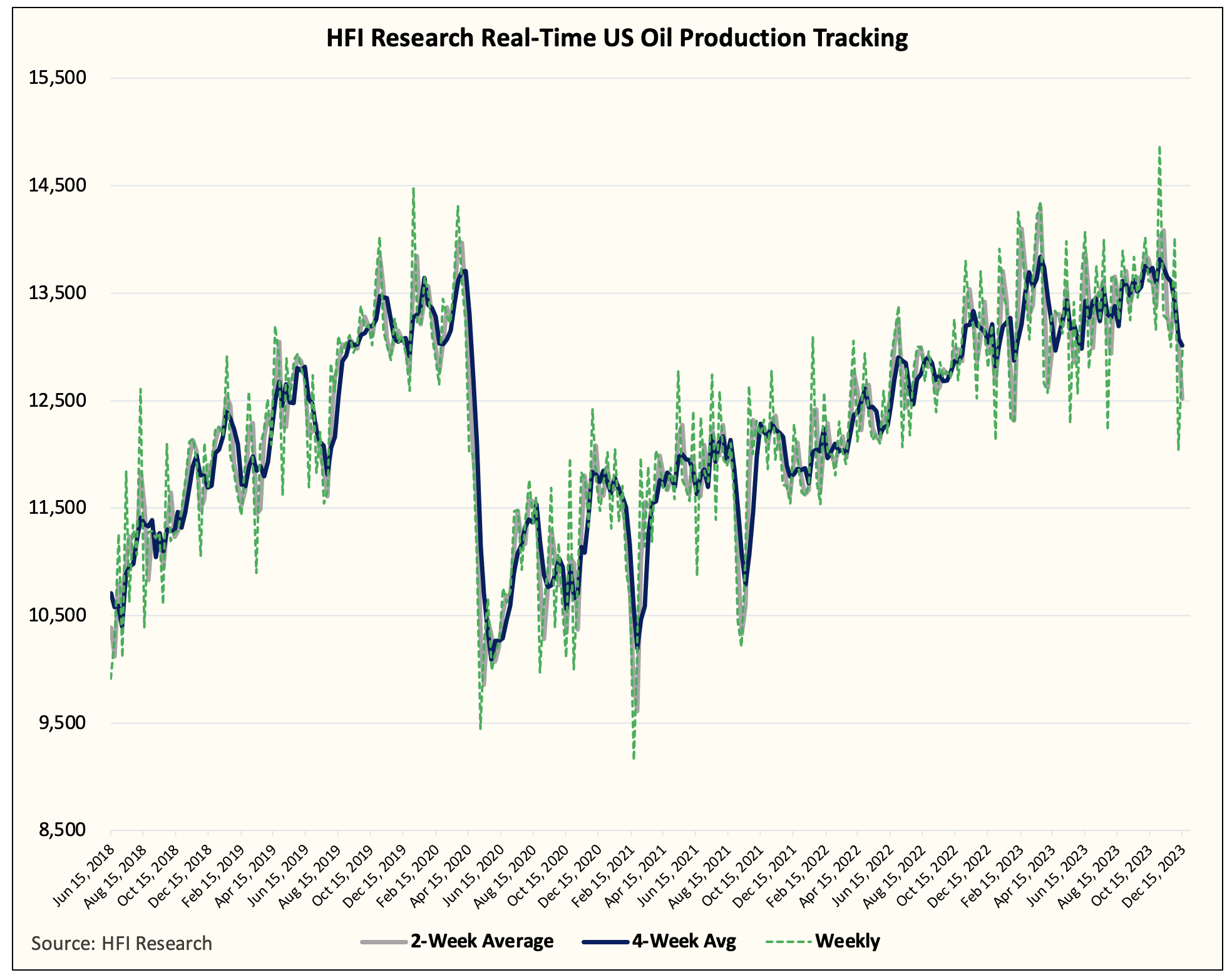

HFIR

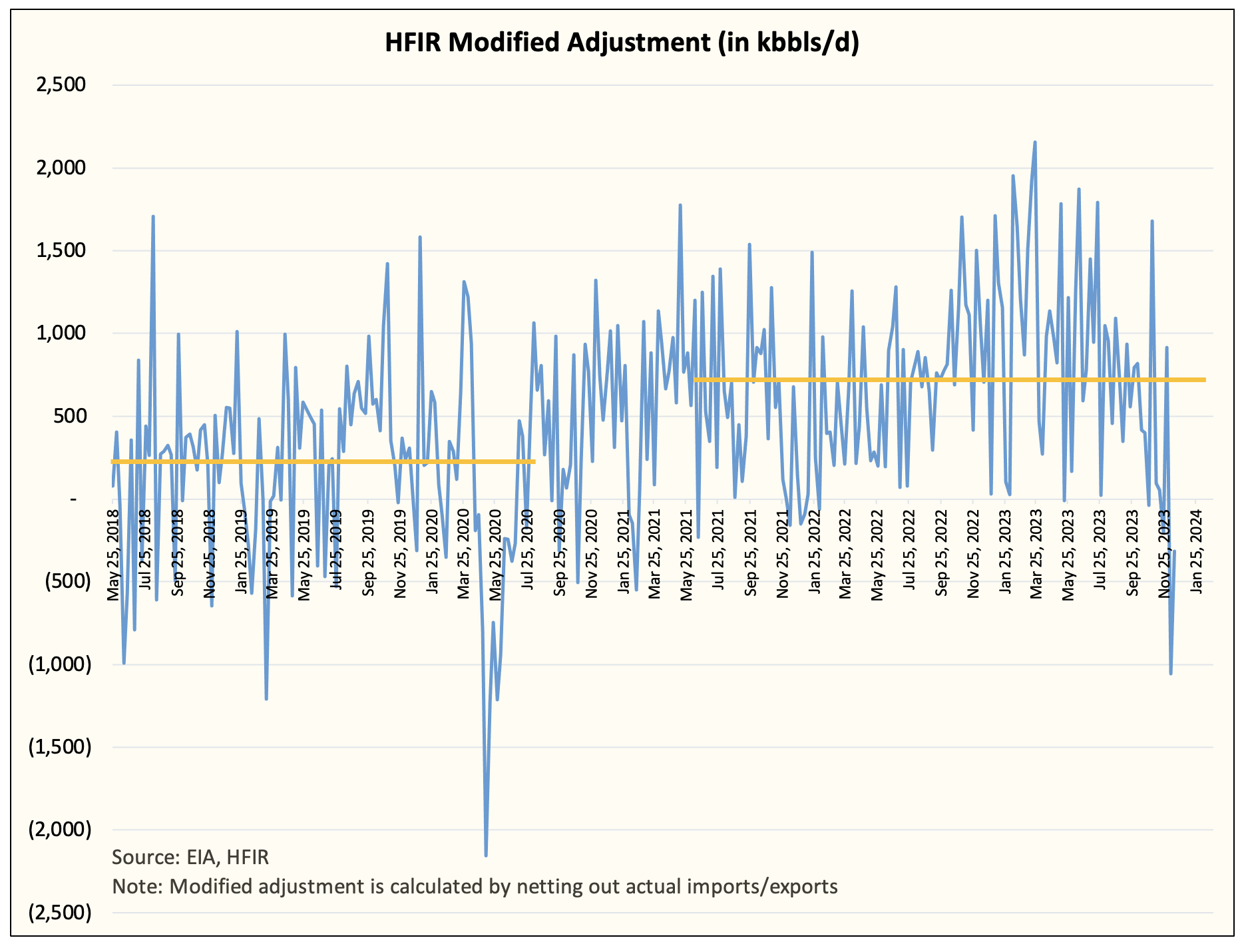

Observe: Figures following November don’t embody “transfers to crude oil supply.” As a substitute, it is a extra real looking reflection of U.S. oil manufacturing.

Taking a look at our real-time tracker, you possibly can see that U.S. oil manufacturing is nearer to ~13 million b/d right this moment. Over the previous 4-weeks, EIA has reported a median manufacturing of 13.011 million b/d. In November, U.S. oil manufacturing confirmed a median of ~13.392 million b/d.

Now there are some caveats with these figures. For starters, the primary week of November was when the “transfers to crude oil supply” was first launched. On the time, our modified adjustment confirmed a cloth leap to ~1.6 million b/d. On the time, we wrote that such giant jumps have at all times reverted. Since then, we have now seen a serious downward revision.

EIA, HFIR

If we needed to guess, November’s U.S. oil manufacturing was doubtless nearer to ~13.2 million b/d. Now for these of you watching U.S. oil manufacturing carefully, you’d observe that we estimated U.S. oil manufacturing to be ~13.08 million b/d in September. Headline figures out of the EIA confirmed U.S. oil manufacturing hitting ~13.2 million b/d, however the adjustment determine was solidly adverse. The implication of that’s EIA doubtless overstated U.S. oil manufacturing.

One of many massive fears going into year-end is that U.S. oil manufacturing would additional shock to the upside leaving these anticipating U.S. shale to peak to fold their arms. As a substitute, we predict the most recent information is validation that U.S. oil manufacturing wasn’t wherever close to as robust as folks suspected.

Following the November PSM launch, we wrote to readers that the upside shock of ~250k b/d was largely due to personal producers seeking to juice up manufacturing forward of the M&A growth we’re seeing in vitality. With out a profitable exit, many of those personal names must resort again to a gradual state, which ought to see manufacturing meaningfully fall into year-end and at the beginning of 2024.

Seasonally talking, U.S. oil manufacturing is at all times at its lowest in Q1, so with out a ramp into December, manufacturing normally falls extra meaningfully. We’re already beginning to see that.

My guess is that U.S. oil manufacturing will end December proper round ~13.05 million b/d. This may convey the upside shock to +100k b/d versus our authentic estimate of 12.95 million b/d. By Q1 2024, we count on U.S. oil manufacturing to have fallen to ~12.8 million b/d earlier than recovering to ~13.1 million b/d by Q2 2024.

Taking a look at 2024 balances, we count on U.S. oil manufacturing to succeed in ~13.5 to ~13.6 million b/d by Q3/This fall 2024. We can be taking a look at an exit of +500k b/d y-o-y.

Following this progress, 2025 ought to see U.S. oil manufacturing remaining flat proper across the ~13.5 to ~13.6 million b/d with a risk of ~13.7 million b/d. However that is about all the expansion there’s, U.S. oil manufacturing will peak following 2025.

Extra fluff than substance…

You may make all of the technical enhancements you need. You may enhance drilling velocity and completion turnaround, however on the finish of the day, you possibly can’t change the geology. U.S. shale progress is akin to working on a treadmill. The sooner you develop, the sooner it’s important to run simply to remain in place. For many producers, staying flat is probably the most optimum option to go, going ahead. By rising manufacturing steadily, you run the danger of: 1) working out of stock and a couple of) reducing your fee of return.

Self-discipline in U.S. shale isn’t as a result of shareholders are asking for it. Self-discipline in U.S. shale is occurring as a result of the geology, the stock, and the execution do not help speedy progress. At ~13.5 to ~13.6 million b/d whole U.S. oil manufacturing, U.S. shale oil manufacturing would see declines of over ~3 million b/d a yr. In essence, you must produce half a Permian a yr simply to remain flat. That is a tall activity and one thing that will not jive with the stock that is left on the market.

How do we all know we’re proper?

Easy. First issues first, U.S. oil manufacturing will decline to ~12.8 to ~12.9 million b/d in Q1 2024. If this occurs, this validates our thesis that personal producers have been the one motive U.S. oil manufacturing stunned to the upside.

Second, if U.S. oil manufacturing follows the roadmap we laid out, then we all know progress goes to cease quickly. By H2 2024, U.S. shale oil producers will sign extra capital returns again to shareholders by way of dividends versus share buybacks (you do not wish to purchase again in corporations with shrinking inventories).

Third, capex progress projections for 2025 will present minimal progress. This can as soon as once more sign that we’re on the fitting trajectory.

As soon as we validate that we’re on the fitting path, then readers will know that our evaluation of U.S. oil manufacturing peaking in 2025 can be appropriate.