grandriver

Thesis

The First Belief Pure Gasoline ETF (NYSEARCA:FCG) is an equities trade traded fund. Regardless of its nomenclature which could give the misunderstanding the fund invests in pure fuel futures, the car in actual fact holds a portfolio of Oil & Gasoline equities. FCG seeks funding outcomes that correspond typically to the value and yield of an fairness index referred to as the ISE-Revere Pure Gasoline™ Index. The index incorporates a mixture of transportation entities and exploration and manufacturing firms. By way of its composition the fund is a mirrored image of each the earnings made out of promoting pure fuel in addition to transporting it.

Historically each the transporter and E&P firms had two foremost dangers related to their enterprise fashions, specifically the value of pure fuel and secondly the structuring of the steadiness sheet. The primary danger is pretty straight ahead, with increased pure fuel costs make it extra worthwhile to extract it and to move it to a sure extent. The second danger issue skilled a fantastic reset in the course of the Covid disaster, with lots of the entities current within the portfolio struggling ‘close to loss of life’ experiences:

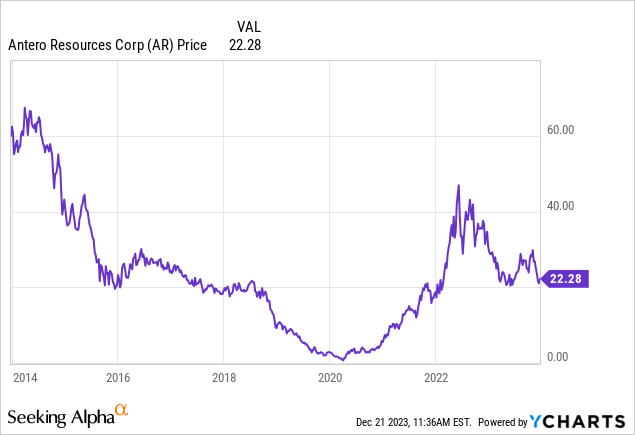

Antero Assets (AR) is a pure fuel E&P firm, and as we will see from the above graph courtesy of YCharts, the entity nearly went bankrupt throughout Covid. On one hand we had decrease pure fuel costs which drove profitability decrease, however the dire scenario for AR was largely pushed by its steadiness sheet throughout that interval. The corporate had many close to time period debt maturities and a poor liquidity place by way of its revolver. Nonetheless, Covid offered a really robust lesson for a lot of of those entities, who understood the significance of managing a steadiness sheet in a conservative style and the need to be prepared for one more down cycle. In at the moment’s world, many of the firms within the FCG portfolio have very wholesome steadiness sheet, with debt termed out in the course of the 2020/2021 zero charges surroundings and with massive revolving services with three to 5 years remaining maturities. Furthermore, most of them considerably diminished their leverage in the direction of 1x EBITDA, making certain not solely survival throughout at the moment’s down cycle, however truly strong fairness costs.

Pure fuel costs are again to sq. one

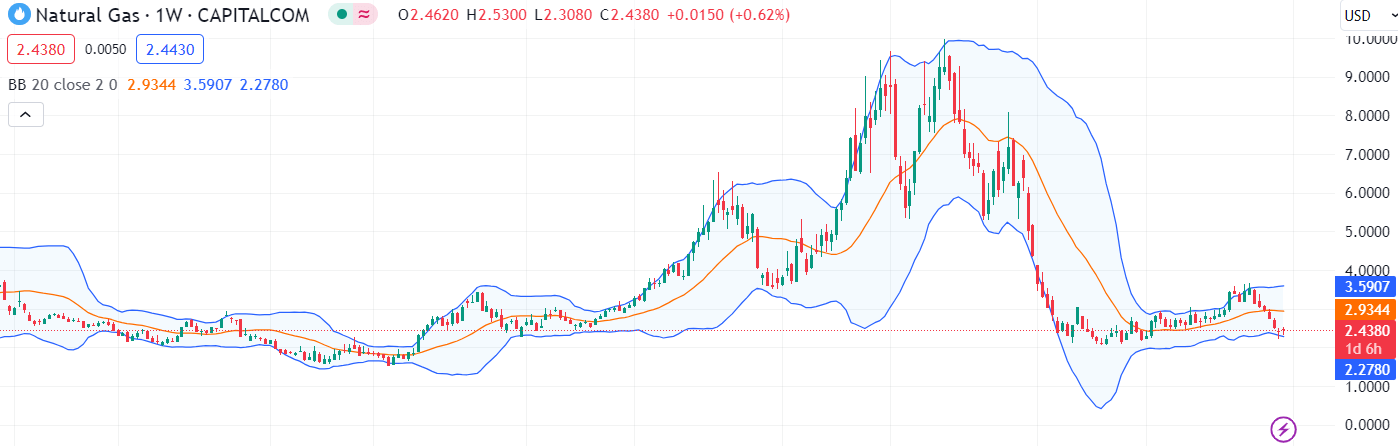

It has been a wild roller-coaster trip for pure fuel costs up to now few years:

Pure Gasoline Px (Tradingview)

After being as excessive as $9/MMBtu throughout 2022, pure fuel costs have come all the way down to $2.43/MMBtu now, however extra importantly they’re down over -30% since October. Seasonality performs an necessary function, with a hotter than anticipated winder each within the US and Europe contributing to a decrease than anticipated demand sample:

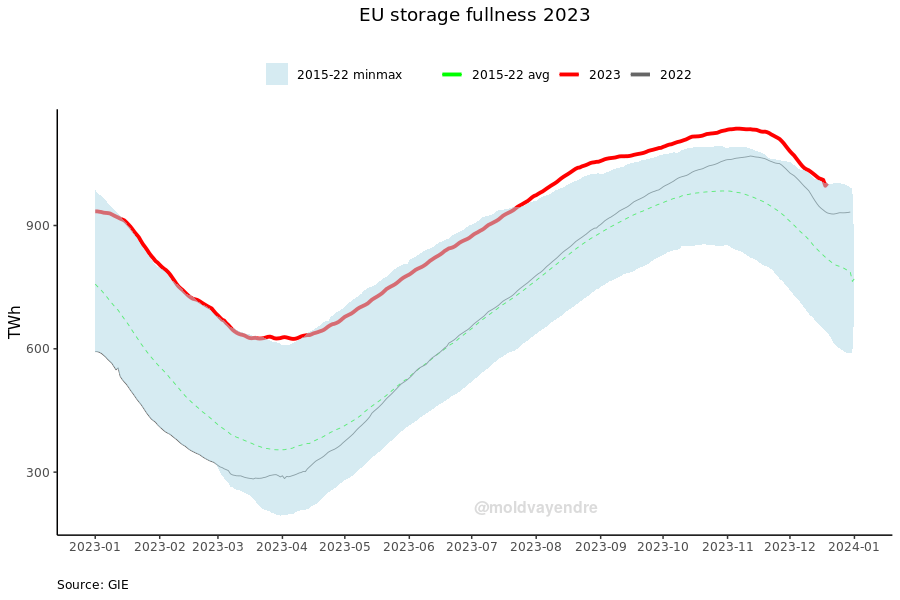

EU Storage (Twitter – moldvayendre)

Pushed by the Russian/Ukrainian battle, Europe has been very proactive about consumption in addition to the sourcing of fuel for its injection season. A really chilly winder may have theoretically pushed the continent in the direction of lack of assets for heating and its business. Fortuitously for Europeans, it has been the exact opposite. As we will see from the above graph, the EU storage is at a historic excessive, with most international locations now one of the simplest ways to cope with increased value purchases.

Within the US, when Henry Hub, we will see the spot value being again near its very long time assist line of $2/MMBtu, which outdoors of Covid is a really properly established technical and basic assist. Why? As a result of essentially most producers break even from a profitability perspective when pure fuel is within the mid-2s, so extended intervals of pure fuel at $2/MMBtu leads to much less stock drilling and extraction. Cycles take a very long time to play out, however traditionally that’s the reason this stage represents each a technical and basic assist stage.

FCG has achieved very properly in 2023

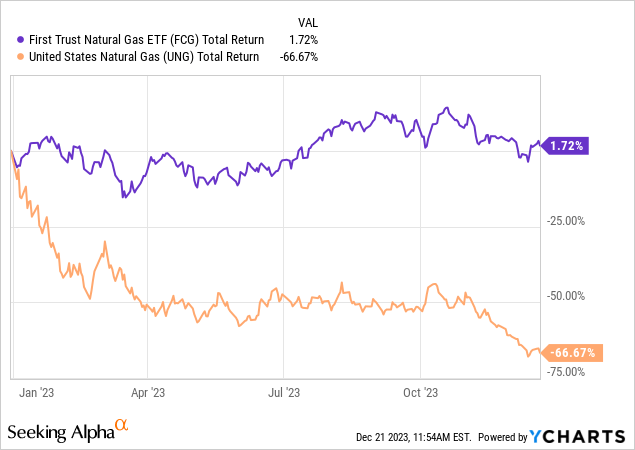

Sporting a 3.4% yield, the fund has achieved very properly in 2023 from a complete return perspective, contemplating absolutely the destruction in spot costs for pure fuel:

The USA Pure Gasoline (UNG) ETF is an trade traded fund utilizing futures to offer the return of spot pure fuel costs (readers can look on the Searching for Alpha platform for UNG particular articles), and the fund has been wrecked in 2023, down -66%. FCG however has been in a position to maintain a optimistic efficiency, regardless of the collapse in costs for its foremost commodity. The rationale? As defined within the ‘Thesis’ part, the parts in FCG have achieved tremendously properly in cleaning-up their steadiness sheets, thus the market is now pricing them on their ahead, quite than an imminent demise. So long as the futures curve is upwards sloping, the market can see bigger earnings sooner or later that get discounted to the current, thus the value affect to the fairness value just isn’t as abrupt as investing within the outright commodity.

Purchase low, promote excessive

In our opinion FCG just isn’t a real purchase and maintain, however as many commodities funds, a cyclical play. A retail investor ought to comply with the ‘purchase low, promote excessive’ mantra by following the pricing in the primary danger issue right here, specifically pure fuel. Ought to you could have purchased FCG when pure fuel costs have been always excessive? No. Must you think about buying FCG now, once we are very near historic assist ranges in pure fuel costs? We expect so. We’re of the opinion that the power transition will take a few years to happen, and till then oil and fuel will comply with their cyclical patterns, with the additional benefit to pure fuel of LNG terminals. The event of LNG terminals will principally ‘pull-up’ pure fuel spot costs within the US to match the upper ranges in Europe and Asia:

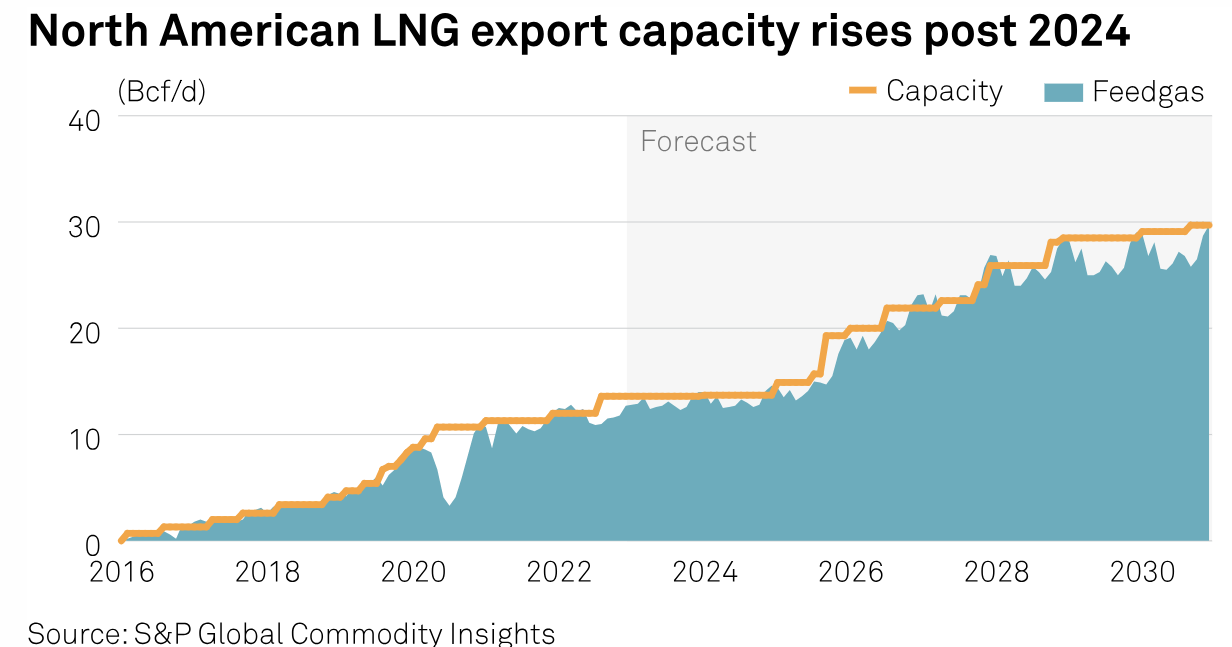

LNG capability (S&P)

If we glance into the long run, we will see capability ramping up considerably after 2024, which can translate into increased earnings for the parts making up the FCG collateral. Stated developments take time, and their progress is definitely intently monitored by the spot market, which typically data outsized strikes when delays are introduced. Nonetheless, increased export capability will translate into increased costs on a extra everlasting foundation.

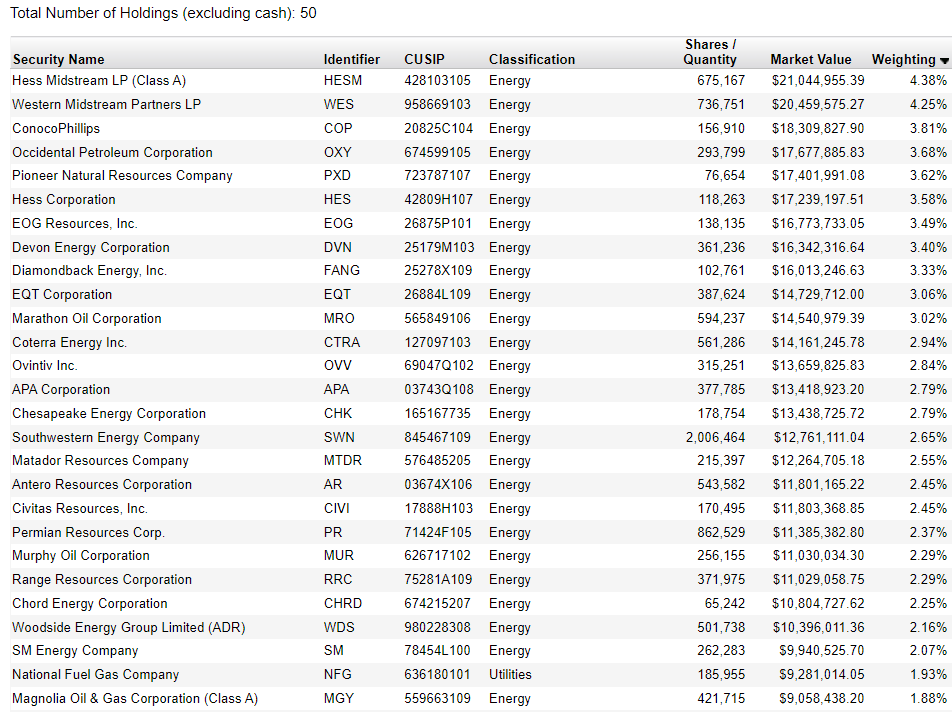

The fund parts are massive Oil & Gasoline firms or transportation MLPs, that are set to profit:

Holdings (Fund Web site)

Conclusion

FCG is an trade traded fund. The car holds a portfolio of pure fuel producers and transportation firms. The underlying entities have achieved a 180 by way of restructuring their steadiness sheets post-Covid by way of debt reductions, refinancings and extensions. Basically, all of the portfolio firms are in significantly better form than three years in the past, which explains the strong fund efficiency in 2023 regardless of the -66% drop in pure fuel costs as mirrored within the UNG ETF.

With pure fuel near its historic assist stage of $2/MMBtu, retail buyers ought to start thinking about investing in FCG. Pure fuel costs are extremely cyclical and unstable, however the improvement of LNG export services will present structurally increased costs going ahead. We really feel at the moment’s low value surroundings for pure fuel offers for a pleasant entry level into E&P producers and transportation firms as mirrored by FCG.