Editor’s notice: Looking for Alpha is proud to welcome Florian Muller as a brand new contributor. It is simple to turn out to be a Looking for Alpha contributor and earn cash on your finest funding concepts. Lively contributors additionally get free entry to SA Premium. Click here to find out more »

Armando Oliveira/iStock Editorial through Getty Photographs

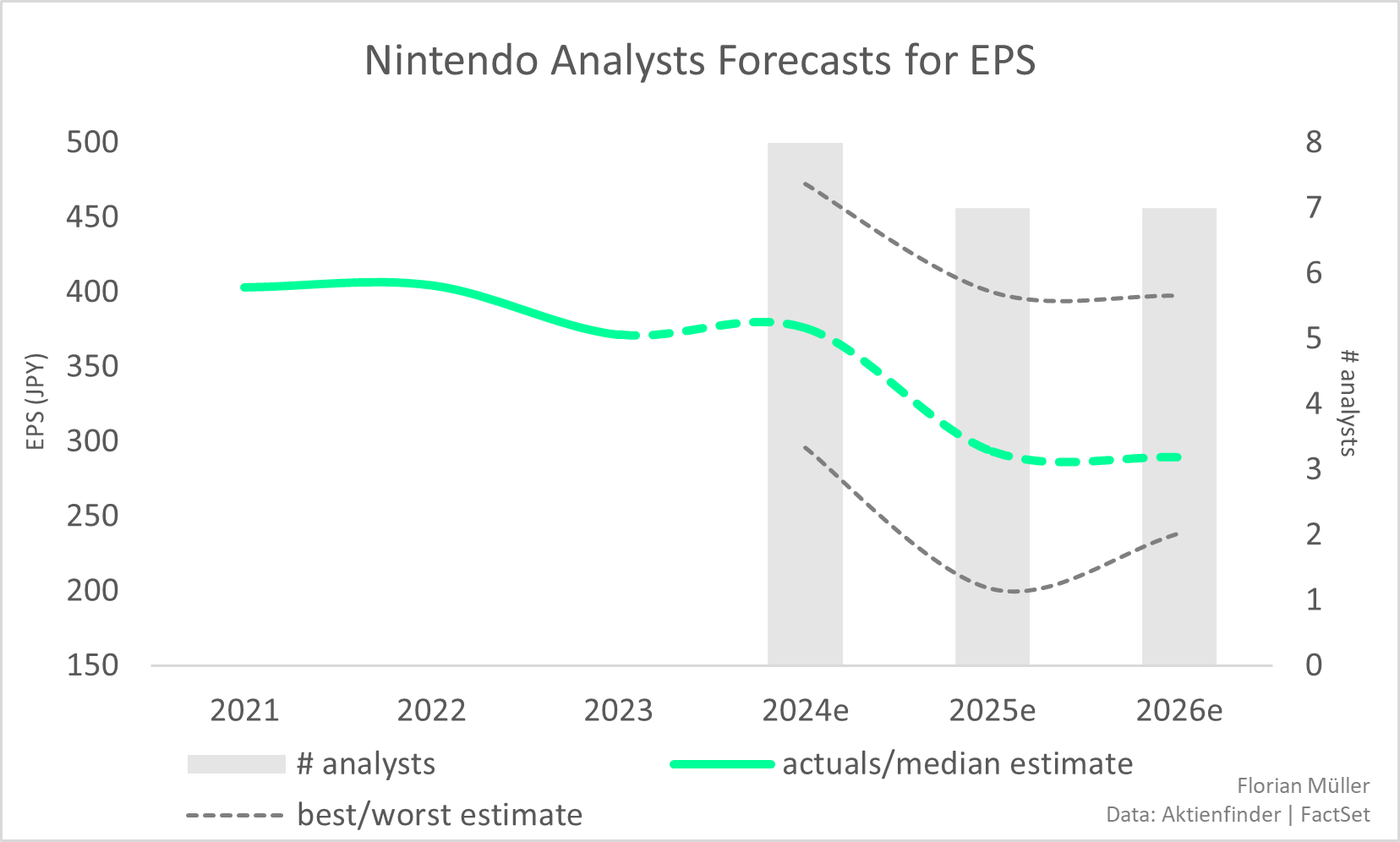

One would possibly suppose that, a minimum of within the brief time period, Nintendo (OTCPK:NTDOF) (OTCPK:NTDOY) just isn’t a high choose purely based mostly on earnings, given its anticipated enterprise contraction in line with the median analysts’ forecasts proven under. Some may declare that at finest the corporate presents an interesting narrative for die-hard followers. As for myself, I’ve recognized compelling causes to stay loyal to my present place within the inventory. I’ll clarify these within the sections that comply with.

Florian Müller | Knowledge: Aktienfinder.internet, FactSet

About half of Nintendo’s software sales are digital, which may probably maintain additional margin alternatives in the long run, offsetting declining revenues. Arguments like these, amongst others, have been exhaustively harassed in different analyses and maintain true for Nintendo. I, nonetheless, will base my evaluation on 4 key pillars:

- How Nintendo leverages forex dangers

- How Nintendo generates worth from its money surplus

- Nintendo’s product excellence and Mental Property technique

- A reduced money movement valuation

Navigating and Leveraging Foreign money Dangers

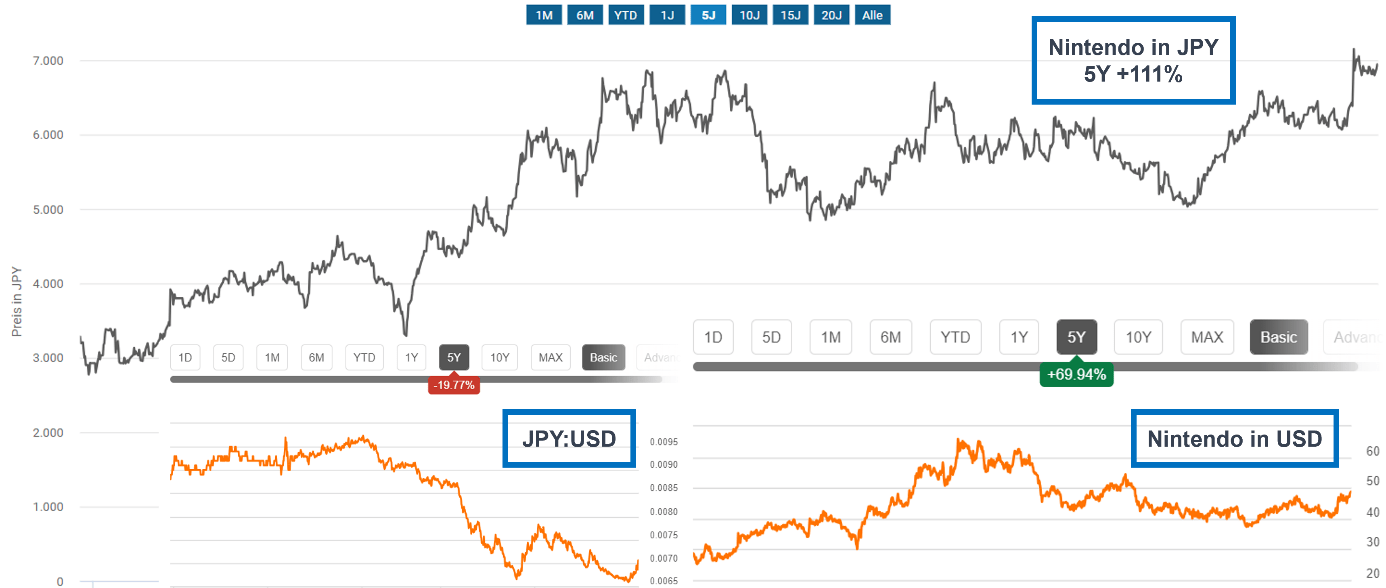

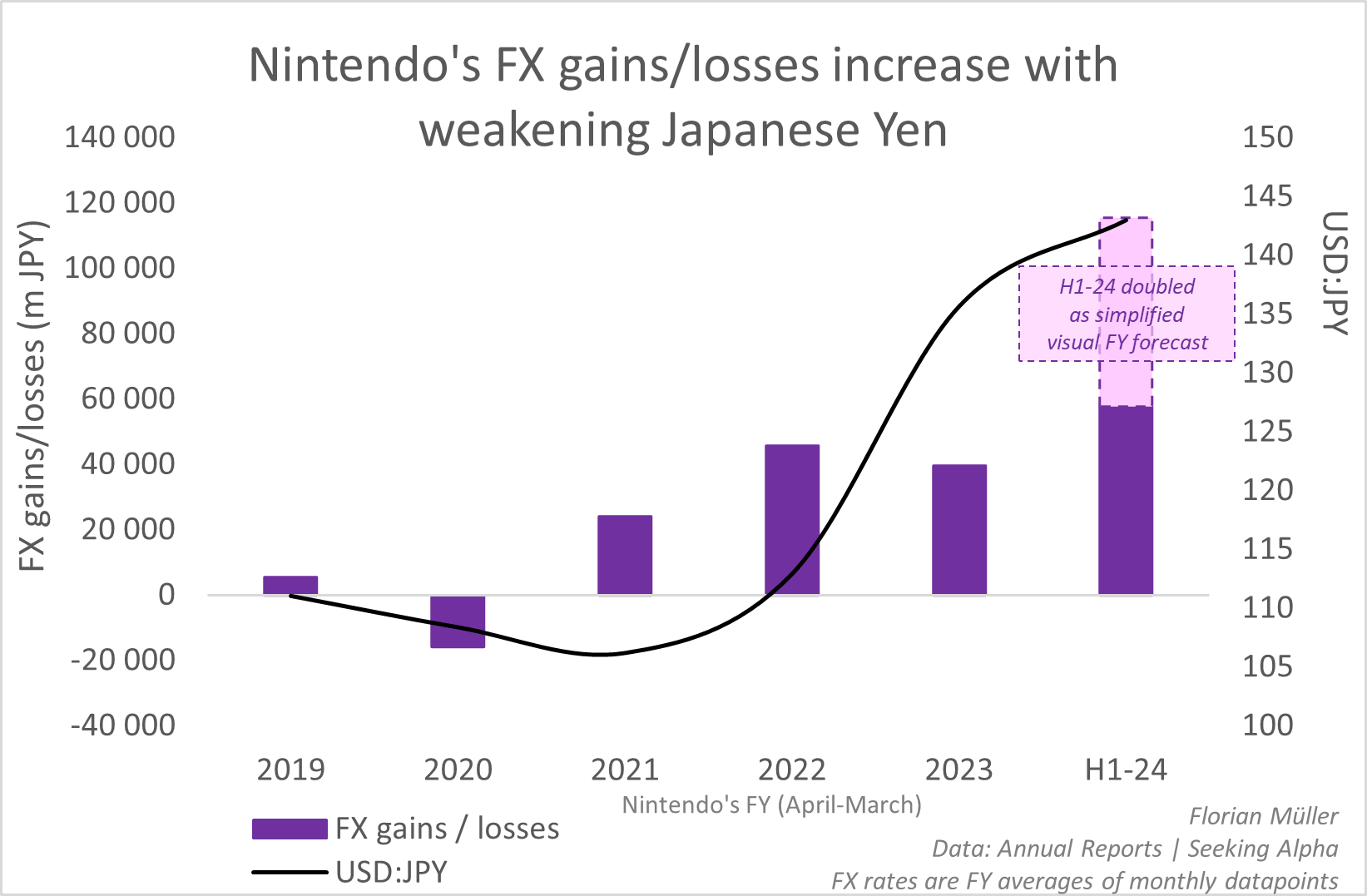

Previously 5 years, Nintendo’s inventory, listed in Japanese Yen on the Tokyo Inventory Change, has surged by more than 110%. Throughout the identical interval, the Japanese Yen has depreciated by almost 20% in opposition to the US Greenback – or conversely, the US Greenback has appreciated by 25 % in opposition to the Japanese Yen. Consequently, US buyers, when evaluated in US {Dollars}, have gained approximately 70% in Nintendo’s inventory over the past 5 years, versus the perceived 110%. A good portion of the features has been mitigated by the weakening Yen. Whereas this evaluation would not purpose to extensively deal with macro points reminiscent of forex fluctuations, this instance vividly illustrates the forex danger related to the Japanese Yen and thus, related to Nintendo from the angle of an investor exterior Japan.

Aktienfinder.internet, Looking for Alpha

Nonetheless, the corporate strategically leveraged this vulnerability in each their operations and non-operating extra money administration. With solely about 22% of its revenues not too long ago generated in Japan, 23% in Europe, and 44% in “The Americas”, the appreciating USD performed into the arms of the Japanese company when transformed into yen. In comparison with the earlier first half-year, Nintendo’s net sales have increased by 21.2%, or 139.3 million yen, with 36.8 million yen, or 5.6%, attributed solely to the weak yen. Conversely, a re-strengthening yen may exert stress on the gross sales aspect.

Moreover, cash-like property held by Nintendo in foreign currency resulted in non-operational foreign exchange gains. I’ve visually proven how Nintendo’s non-operating earnings from investments in foreign currency exterior of JPY have markedly elevated not too long ago. For instance, I’ve displayed the energy of the US Dollar exchange rate alongside, which correlates with Nintendo’s features from foreign currency. This illustrates that the weak yen has performed into Nintendo’s hand not simply operationally, but additionally as a consequence of its excessive money surpluses and their short-term investments overseas.

Florian Müller | Knowledge: Annual Studies, Looking for Alpha

Excessive Curiosity Charges? Sure, Please!

An funding in Nintendo appears to be a snug place in each excessive and low-interest charge environments. Whereas many indebted firms are battling rising curiosity bills, Nintendo sits on a considerable money (& equivalents) pile of more than 2 trillion yen or $14 billion. This, in flip, is being lucratively invested as I’ll illustrate in a second. Whereas financial circumstances in lots of locations could also be slowing because of the rising rate of interest surroundings, Nintendo is ready to generate returns on its excessive liquidity reserves, bolstering its monetary energy. Thus, Nintendo is armed to the tooth, able to strategically allocate its money reserves when the time is correct, particularly throughout the subsequent section of a brand new console launch or a possible shift in international financial insurance policies. Its sturdy liquidity place empowers Nintendo to finance future progress initiatives independently and react swiftly to market modifications and intense competitors.

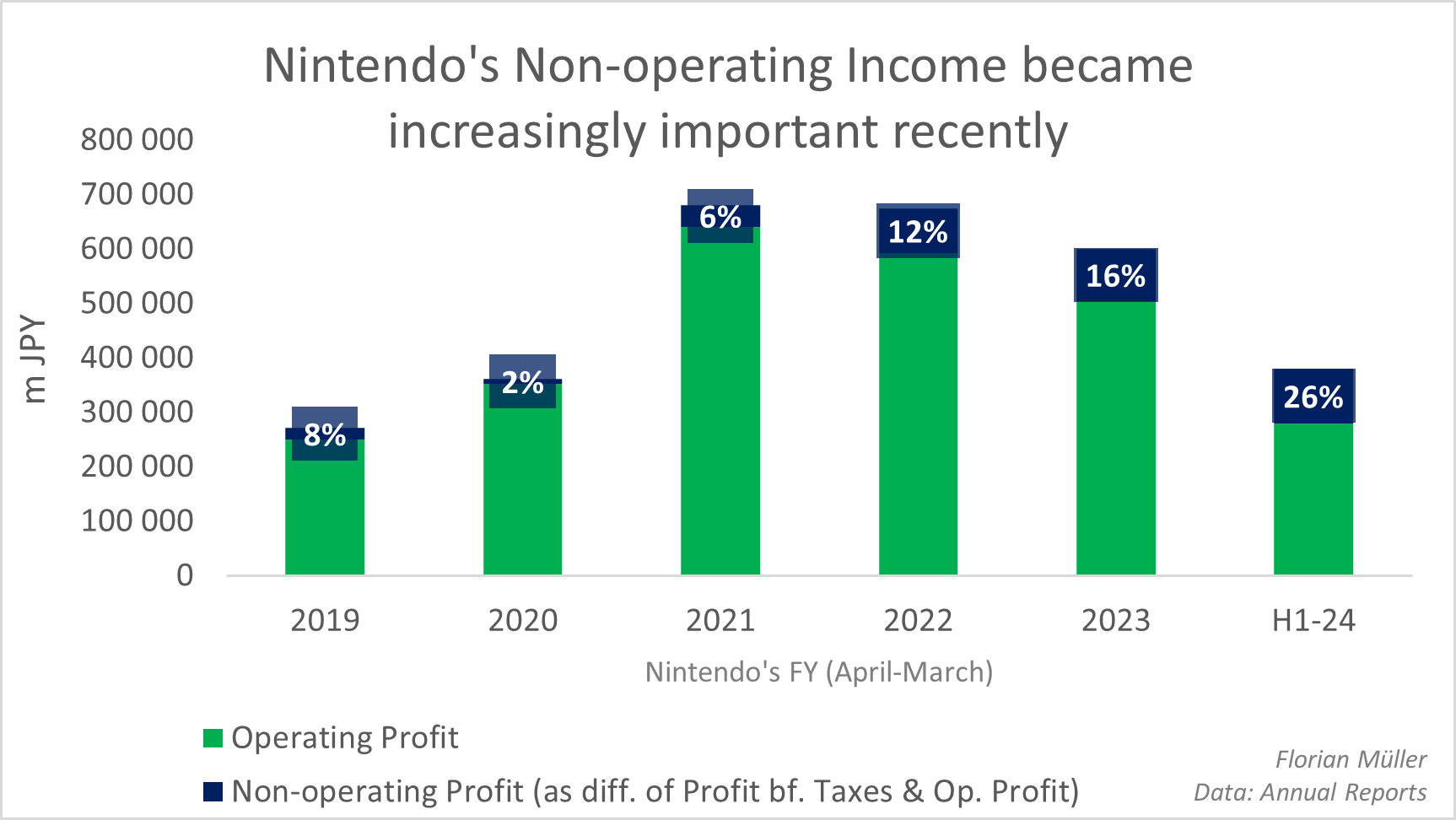

However already now, it’s evident how Nintendo’s administration strategically leverages its money surpluses to generate worth, recognizable by the rising non-operating earnings primarily fueled by international alternate features, as beforehand showcased, coupled with curiosity earnings.

Florian Müller | Knowledge: Annual Studies

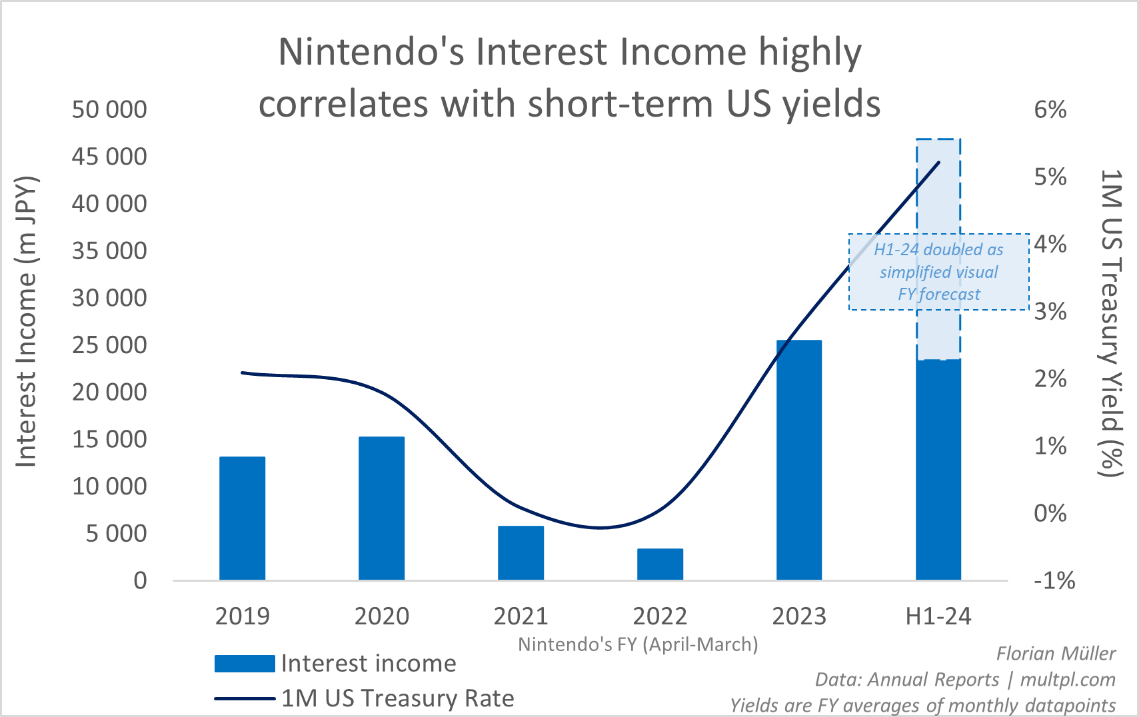

Nintendo’s current notable enhance in curiosity earnings from its substantial money reserves strongly correlates, as an example, with short-term US capital market yields. Thus, Nintendo has been capable of considerably profit non-operationally from the elevated rate of interest surroundings overseas, leveraging its excessive money holdings.

Florian Müller | Knowledge: Annual Studies, multpl.com

Understating its Product Excellence

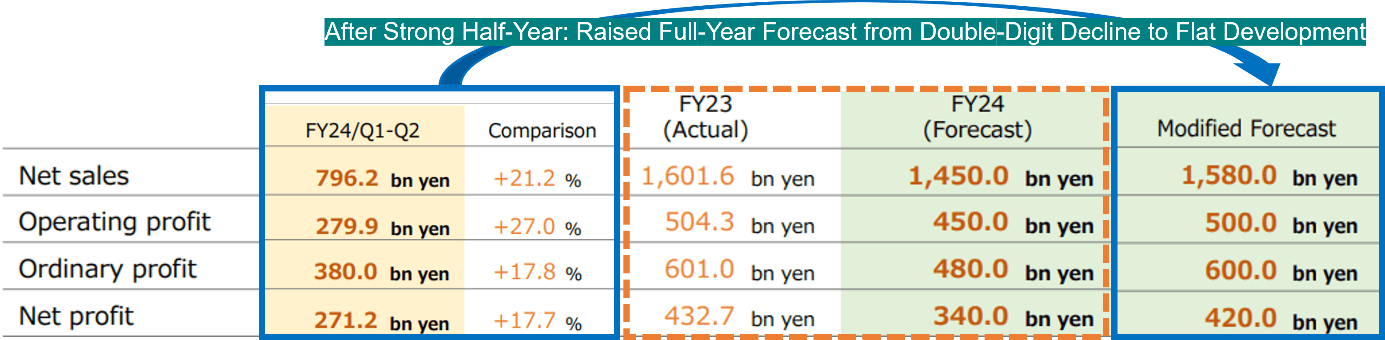

On the finish of the primary quarter of 2024, which concluded in June, Nintendo reported extremely sturdy progress figures, with income and revenue surging by 50 to over 80 % in comparison with the earlier 12 months’s quarter. Nonetheless, the administration was at first sustaining its annual forecasts, which anticipated a decline of almost 10 % in income and over 20 % in earnings. These forecasts may solely be an expression of understatement, particularly because the first quarter alone has already achieved 30 to 50 % of those targets. Supported by the current launch of Tremendous Mario Bros. Marvel, whose critiques are overwhelming in numerous gamer and informal gaming boards, I’d not have anticipated a major decline, substantial sufficient to not surpass the modest annual targets. Unsurprisingly, the administration has now finally revised the forecasts upwards with the most recent quarterly outcomes.

Tailored from Nintendo Q2/2024 Earnings Presentation

Nonetheless, this new forecast nonetheless implies a weaker second half of the 12 months. Given its numerically and qualitatively sturdy pipeline and the vacation season forward, it is laborious to actually imagine within the slowdown projected by the administration for the rest of the 12 months. As a substitute, this forecast appears as soon as once more conservative. The dividend, nonetheless, initially estimated to drop by 20 % to 147 Yen, will as an alternative stay virtually flat at 181 JPY for the total 12 months. The interim dividend has already been paid.

Nintendo Q2/2024 Earnings Presentation

Analyst estimates had constantly remained barely increased within the median when in comparison with the administration’s estimates and nonetheless exceed the modified forecast immediately. This may very well be as a result of analysts could be contemplating the ripple results of the Tremendous Mario Bros. Film, opposite to Nintendo’s indication earlier this 12 months, that they themselves do not issue these results into their monetary forecasts.

However even the flat growth over the present fiscal 12 months can be significantly pleasing, provided that its blockbuster console Nintendo Swap is already in its seventh 12 months since launch, with many eagerly anticipating its successor. Up till the fiscal 12 months 2021, console gross sales had seen important progress, additionally fueled by the COVID-induced gaming surge. Nintendo’s product excellence is confirmed by the steadily increasing number of dedicated gamers far past 100 million folks up till immediately, whilst console gross sales noticeably declined not too long ago on a fiscal 12 months foundation. Management remains reserved about saying a Subsequent-Gen console. Their main focus stays on nurturing and increasing the Swap universe. Nonetheless, ongoing efforts for future {hardware} are underway. Linked to that could be a hopeful enhance in annual analysis and growth spending from 102 billion yen in FY 2022 to a forecasted 130 billion yen in FY 2024.

Worth Creation By way of Mental Property

Nintendo could be steadily lowering its reliance on {hardware} gross sales, whereas the energy of its mental property and the recognition of its franchises come to the forefront. Segments involving mental property, which embrace income from the movie, taking part in playing cards, and merchandise, contribute lower than 7.5% to the corporate’s whole income. Nonetheless, in comparison with the earlier 12 months’s half, these segments have more than doubled, indicating their important potential as long-term progress drivers. Trying ahead, Nintendo has introduced to be engaged on a live-action film of The Legend of Zelda, one other one in all Nintendo’s extremely in style franchises in addition to Tremendous Mario.

“We do not intend to simply set a numerical sales target for our mobile and IP related business and then aim for that. The use of Nintendo IP requires extremely careful supervision so we don’t negatively affect the image people have of our IP or harm the emotional attachment they’ve formed with it from playing our games. While we always strive to achieve the maximum results possible in each initiative, we do not believe that setting numerical targets such as revenue for the IP related business is appropriate.”

“The Super Mario Bros. Movie,” launched since April, has shattered information with almost $1.4 billion in box office earnings, making it essentially the most profitable online game movie ever. Surpassing hits like “Minions,” it is monitoring to rival main animations like Disney’s “Frozen” and has even outperformed blockbuster franchises like Jurassic Park. Regardless of combined crucial critiques, the movie’s huge reputation displays the enduring attract of the Nintendo franchise. By strategically showcasing Nintendo in cinemas, the administration goals to interact new followers and rekindle curiosity amongst former fanatics. The movie’s optimistic impression on the “Mobile and Intellectual Property (IP)” phase is boosting this fiscal 12 months’s efficiency.

Nintendo’s growth into the analog world contains two Tremendous Nintendo Worlds, harking back to Disneyland. The primary debuted in Common Studios Japan, Osaka, in early 2021, adopted by one other in Universal Studios Hollywood in February 2023. These ventures, impressed by Disney’s theme park success, trace at promising non-gaming avenues for Nintendo’s long-term enterprise. Nintendo doesn’t operate these theme parks themselves as a result of they lack the experience for it. As a substitute, they acquire licensing charges for them.

Nintendo’s Valuation & Money Strongly Validate its Share Worth

After having mentioned the qualitative facets that make Nintendo an interesting funding regardless of anticipated contraction, I purpose to quantify this by a traditional firm valuation, calculating Nintendo’s honest worth.

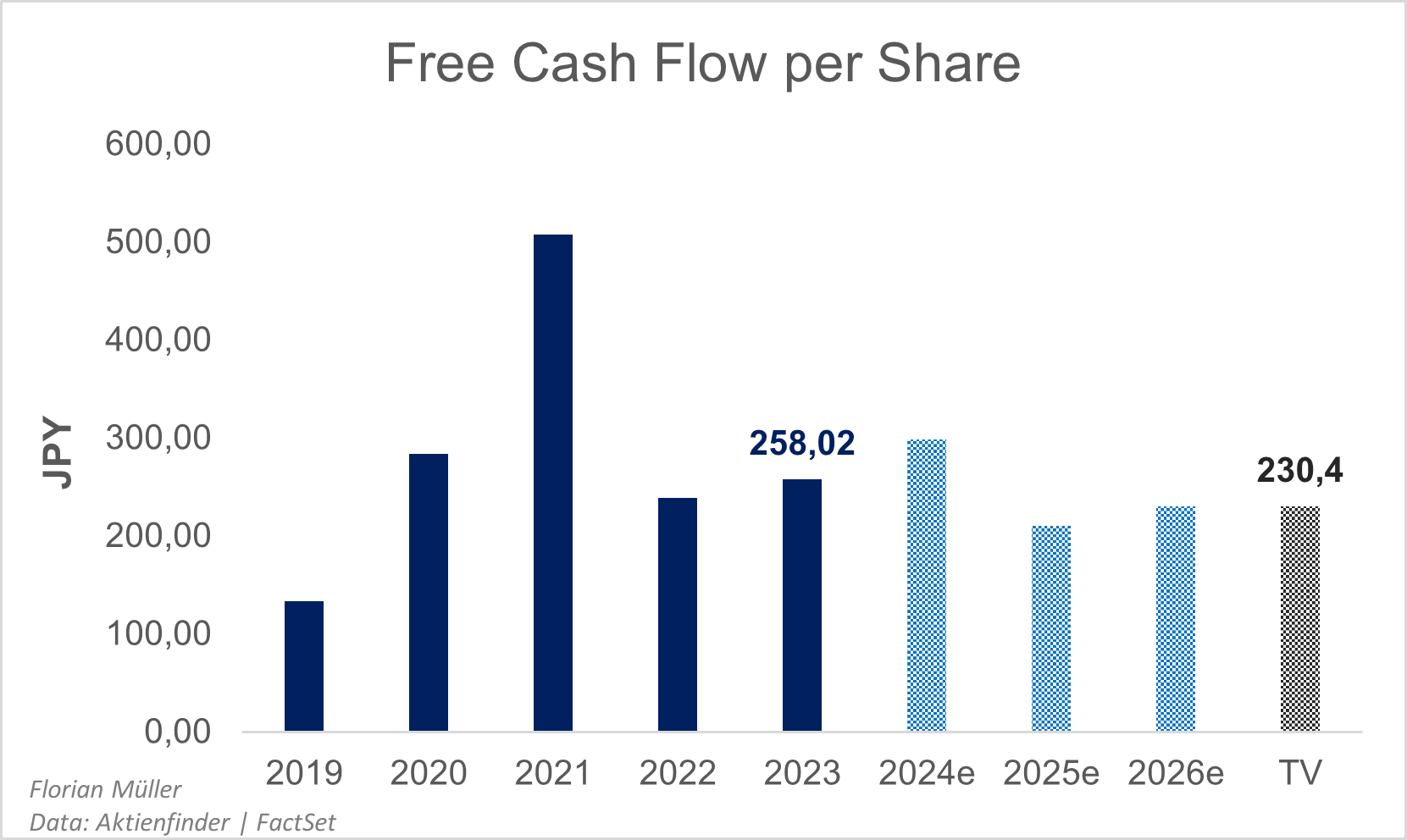

To derive Nintendo’s honest worth by a simplified Discounted Money Stream mannequin, I make the most of Free Money Stream projections sourced from Aktienfinder.internet, drawing on median analyst estimates till the fiscal 12 months’s finish in 2026, based mostly on FactSet’s database. I efficiently cross-verified the precise figures from the final 5 years for this metric (Free Money Stream) with these from Looking for Alpha. The Free Money Stream has stabilized at a conservative stage in comparison with the current Nintendo Swap increase however stays comfortably excessive when considered from a historic perspective. Due to this fact, I am utilizing the Free Money Stream of 2026 because the Free Money Stream for the Terminal Worth.

Florian Müller | Knowledge: Aktienfinder.internet, FactSet

My analysis on Nintendo’s WACC (Weighted Common Price of Capital) settles at a worth of seven.7%. This determine displays the elevated various funding alternatives within the risk-free area as a consequence of globally rising bond yields and is supported by Fairness Threat Premia per nation as revealed by the famend Prof. Damodaran. Contemplating Nintendo’s income distribution primarily in mature markets, there are not any important nation dangers on high of the Fairness Threat Premium. Statistically, Nintendo’s barely lower-than-market-average volatility – expressed in its Beta issue – contributes to conserving Nintendo’s WACC from being excessively excessive. I derived Nintendo’s Beta issue from a 10-year month-to-month regression in opposition to the Nikkei 225, adjusted utilizing the Blume technique. This calculation yielded a Beta issue of round 0.8 to 0.9. Debt financing prices are negligible as a consequence of Nintendo’s low stage of debt.

I’m making use of a terminal progress charge of three.9% into perpetuity, based mostly on the convergence assumption. Inside this assumption, I presume that newly invested capital yields neither extra nor lower than its required price of capital of seven.7%. Moreover, I assume that fifty% of Nintendo’s Free Money Stream is reinvested, aligning with Nintendo’s current 50% dividend payouts and the absence of great debt obligations.

Florian Müller | Knowledge: Aktienfinder.internet, FactSet

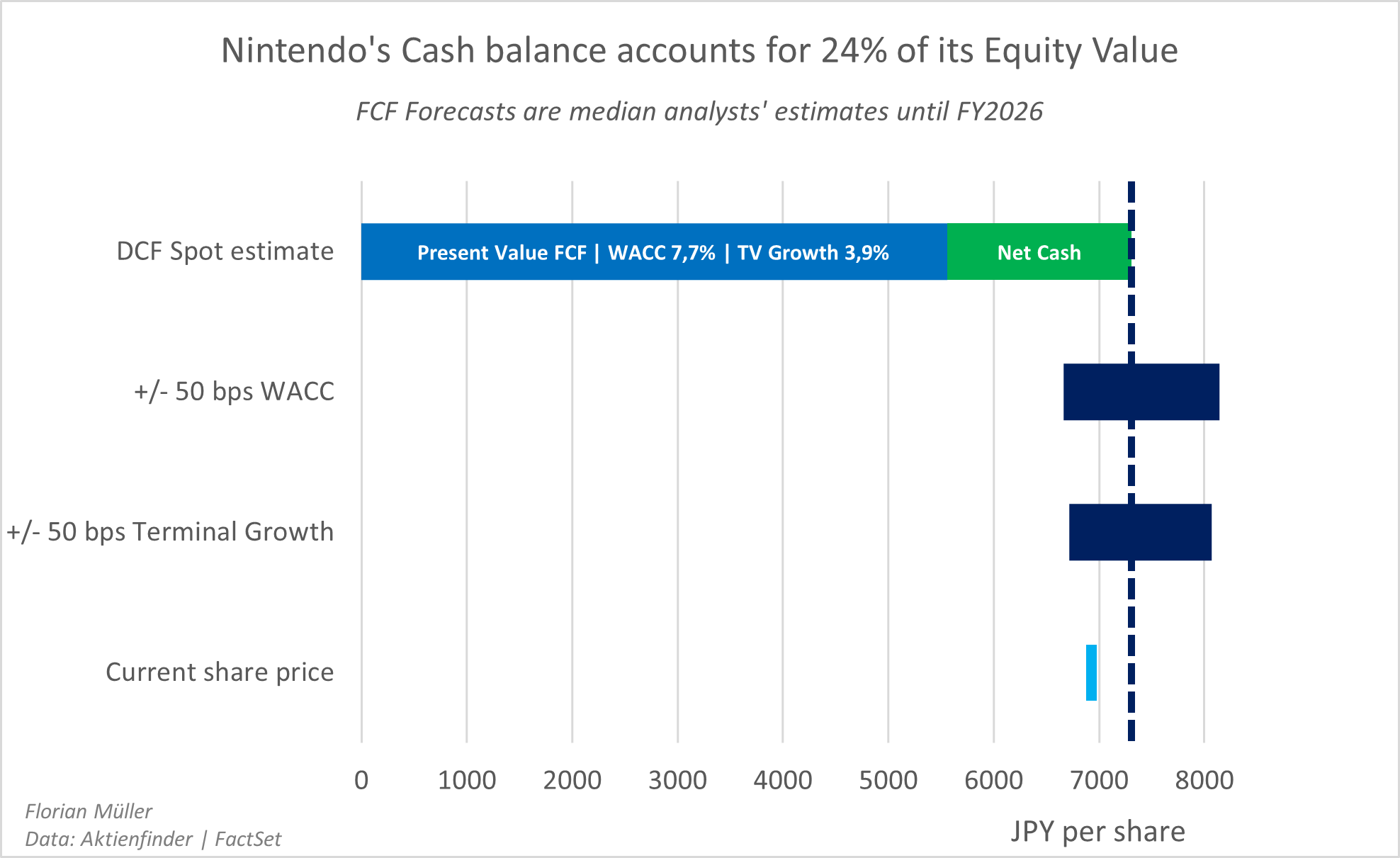

Utilizing these parameters, I’ve calculated the current worth of Free Money Flows for Nintendo at roughly 5,560 JPY per share (equal to 38 USD at present charges). Nonetheless, what’s essential right here is Nintendo’s substantial money reserves, totaling an extra virtually 1,745 JPY per share, internet of a negligible quantity of debt. When factoring in internet money, the whole fairness worth reaches 7,305 JPY per share (equal to 50 USD at present charges), barely surpassing the present share value of roughly 6,900 JPY. Whereas this valuation hinges on my assumptions, it is evident that Nintendo’s surplus money considerably bolsters its enterprise worth, contributing over 30% on high of it and thus representing 1 / 4 of its fairness worth.

Weak Spots of This Thesis

Nintendo’s present strengths in benefiting from a weak yen and excessive rates of interest would possibly face dangers if these circumstances reverse, affecting their non-operating earnings and the worth of their money reserves. Moreover, the corporate’s reliance on the recognition of its franchises is a cornerstone of its success. Nonetheless, overexploiting these IPs may danger diluting their worth over time. The absence of a transparent roadmap for a brand new console, and its potential success, poses a basic danger given the continuing dominance of the prevailing platform as the first income driver. Any uncertainty surrounding the long run console technique might impression market confidence and Nintendo’s progress trajectory. Traders ought to contemplate this alongside the corporate’s dependence on established IPs when assessing its long-term prospects.

Concluding Insights: Nintendo’s Enduring Worth

In essence, Nintendo’s adept dealing with of forex dangers, leveraging of money reserves, and efficient use of mental property trace at its resilience and progress potential. Regardless of near-term projections, the corporate’s adaptability, innovation, and robust monetary basis recommend promising prospects. The Discounted Money Stream valuation signifies Nintendo’s surplus money considerably bolsters its worth, providing stability amidst market fluctuations. Whereas short-term considerations exist, encompassing the superior life cycle of the Swap console with out an introduced successor mannequin, a probably devaluing money foundation in declining rate of interest eventualities, and forex fluctuations, Nintendo’s administration of the latter and its strategic initiatives make it a compelling long-term funding.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.