PM Photos

Whereas different REITs had been declining all through the summer time and fall months, Omega Healthcare Buyers, Inc. (NYSE:OHI) bounced off its 52-week low of $25.61 and rebounded to $34.77. Issues took a flip, and whereas the markets rallied into the Fed assembly and after Jerome Powell’s speech, shares of OHI retraced from their 52-week highs. Shares of OHI have fallen -11.65% since October 17, and just lately information broke that their Q4 funds available for distribution (FAD) will not match the dividend. I’ve skilled the ebbs and flows of being an OHI shareholder, from shares returning to all-time highs with a rising dividend to the dividend development being halted and ramifications from the pandemic lingering. Finally, I’ve remained bullish on OHI as a result of the healthcare house’s long-term care and expert nursing segments will see elevated demand because the child boomer inhabitants ages. I’ve documented the progress I’ve made on my authentic funding, and whereas shares have solely appreciated by 2.71% since my authentic purchases, my general funding is up 70.76%. Regardless of the information, I’m nonetheless lengthy OHI and can proceed to reinvest the dividend every quarter and compound my method right into a lower cost per share (PPS), bigger future dividend revenue, and a bigger share base. I feel OHI continues to be fascinating for long-term shareholders in search of REITs that supply giant single-digit yields because the Fed appears to be like to pivot someday in 2024.

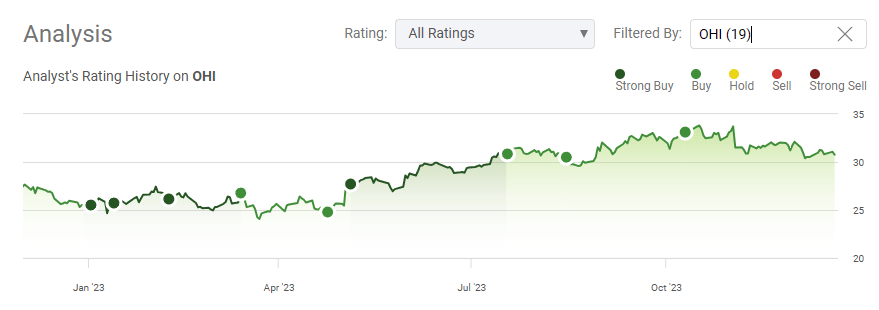

Looking for Alpha

Following up on my earlier article about OHI

On October 10, I wrote an article on OHI (can be read here) and mentioned why it appeared like OHI was getting a move when the market was fearful about debt on the stability sheets of many REITs, OHI’s enterprise, and the way my funding was doing. Since then, now we have had some vital macroeconomic information, OHI delivered their Q3 earnings, and OHI supplied what I’d take into account adverse information about their FAD. I wished to comply with up on my earlier article and talk about the FAD information, why I like OHI going into 2024, how my funding is doing, and why I wrote new lined calls on my place.

OHI delivered a Q3 beat, however then adverse information about their FAD emerged

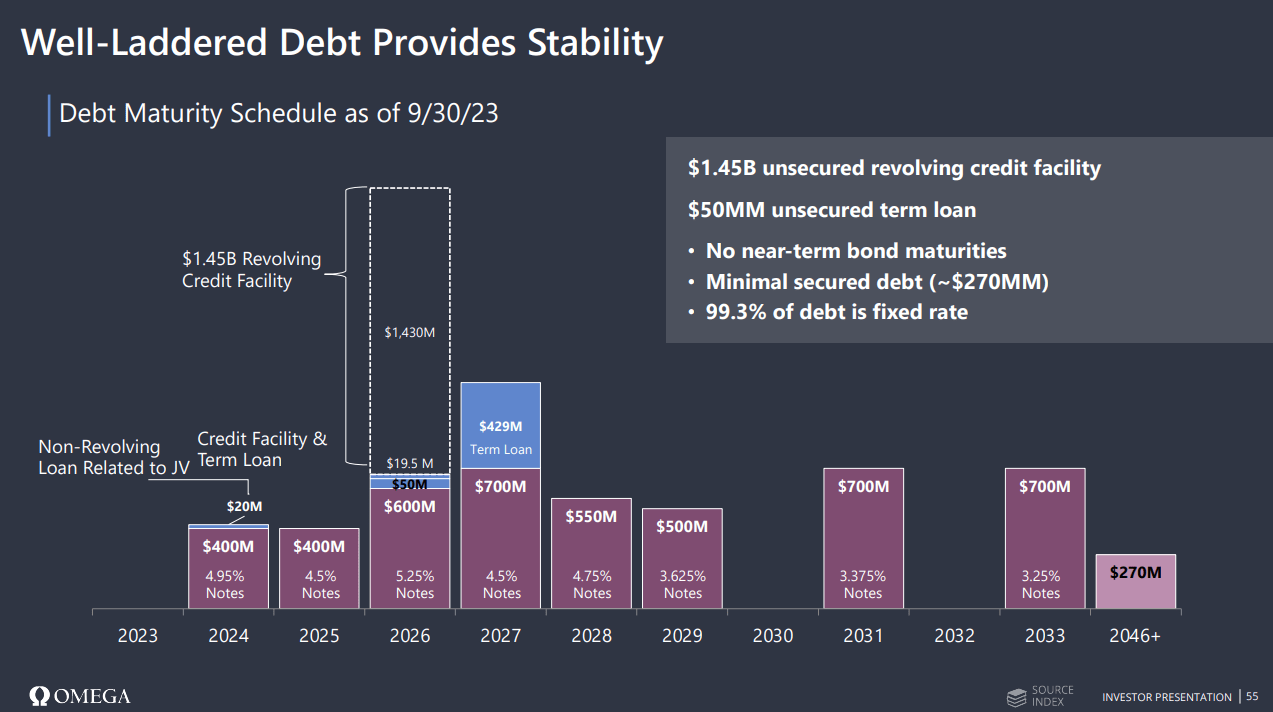

In Q3, OHI got here in larger than the road anticipated regardless of declining QoQ. The road was in search of $210.3 million on the highest line, and OHI delivered $242 million, which was sufficient to beat estimates however not sufficient to prime the $250.2 million of income generated in Q2. OHI generated $0.71 of adjusted funds from operations (FFO) which got here in forward of the $0.70 consensus estimate however was nonetheless a -$0.04 decline from $0.74 in Q2. On an operational degree, Q3 was considerably robust as OHI acquired sudden hire funds from some operators on a money foundation whereas incomes extra curiosity revenue than that they had accounted for. OHI’s FAD amounted to $0.68, which exceeded the quarterly dividend fee of $0.67, however was additionally a decline QoQ. OHI’s NAREIT FFO in Q3 was $161 million or $0.63 per share as in comparison with $159 million or $0.65 per share YoY. OHI paid off a $350 million bond that matured in August and ended Q3 with $554.7 million in cash on hand. OHI did dilute shareholders a bit as they issued 4 million shares or $126 million of fairness, which shall be used to additional de-lever the stability sheet.

Whereas there have been facets of Q3 that had been promising, OHI was upfront about the truth that FAD might be impacted in This autumn and probably into the start of 2024 as a consequence of ongoing restructurings, some tenants nonetheless being on a money foundation, and drawdowns from safety deposits. News broke roughly a month after Q3 earnings firstly of December that OHI’s This autumn FAD will not exceed the dividend. This is because of two of its operators paying lower than the contractual hire owed in November. Maplewood paid $3.3 million lower than its contracted hire in November and expects to be quick roughly $3 million in December, whereas Lavie paid $1.4M in hire in November, which is considerably lower than its earlier run-rate of $2.5M per 30 days. Whereas it’s unclear if Lavie can pay their obligated hire in December, OHI believes within the long-term worth and money circulate of those portfolios. Because the Lavie limiting concludes, OHI sees its contractual hire materially exceeding the This autumn run-rate, whereas the demand for Maplewood’s property has seen occupancy for its stabilized portfolio above 90% since October and believes the portfolio will stabilize and improve its money circulate in 2024.

Omega Healthcare Buyers

Because of this I’m not fearful about OHI. I’m a long-term shareholder, and if shares go to $28 or $33 over the following 12 months, I’m not planning on promoting until my long-term funding thesis adjustments. OHI delivered the FAD information in December and did not warn a couple of dividend reduce. OHI traditionally goes ex-dividend for its Q1 dividend firstly of February and pays the dividend in the midst of February. OHI has over $500 million in money available, and the $350 million observe that was paid off was their whole debt obligation for 2023. There may be greater than sufficient money available to fulfill the 2024 debt obligations, and since OHI hasn’t mentioned a dividend reduce after warning about their FAD on the Q3 earnings name and delivering information about FAD once more in the course of the quarter, I do not suppose the dividend goes to be touched. OHI has a powerful stability sheet and has the flexibleness to navigate uneven waters a bit longer.

Omega Healthcare Buyers

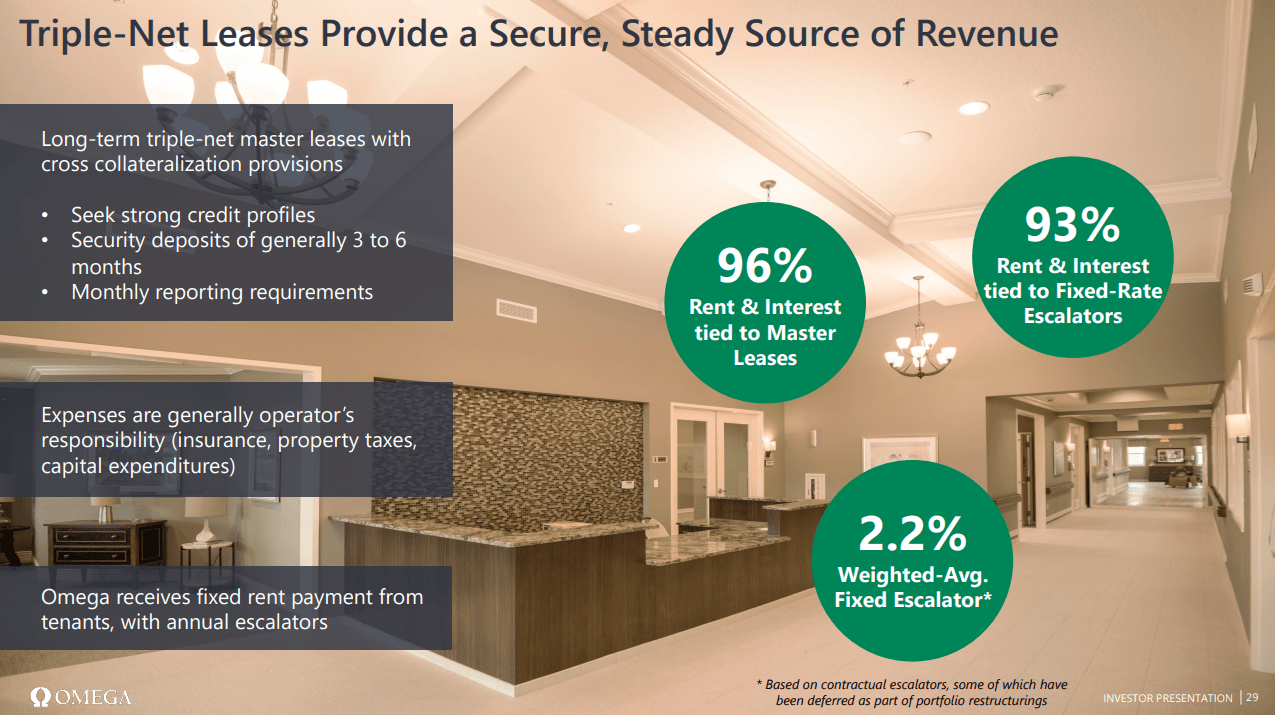

On the start of Q4, OHI had an asset portfolio of 883 services with roughly 86,000 working beds. Their services are run by 65 third-party operators and positioned inside 42 states and the UK. OHI is predominantly a triple internet lease (NNN) operator, which is a lease construction the place the entity renting a property is chargeable for all of the bills along with hire. This is without doubt one of the the reason why I’m so bullish on OHI for the long-term, as their tenants are chargeable for all of the payments, together with insurance coverage, upkeep, and actual property taxes. OHI has 96% of its hire and curiosity tied to grasp leases and 93% fastened to fixed-rate escalators at a median of two.2%. As soon as all of the hardships from the pandemic are alleviated, the construction of OHI’s leases may lead it again to rising the dividend as soon as once more. Throughout Q3, OHI accomplished $106M in new investments, together with $55M in actual property acquisitions, $26M in actual property loans, and $24M in capital renovation and building initiatives. Regardless of some unlucky conditions, OHI is positioning itself for the long run, and I need to be on the experience with them. Because the Fed begins to chop charges in 2024, I feel that a number of the hardships OHI’s operators have confronted shall be alleviated, which is able to assist OHI generate bigger quantities of income and FFO. As capital flows into the market from the sidelines when the risk-free price of return declines, I feel that buyers will look towards REITs and different high-yielding property to recreate the yields they had been accustomed to. I feel that OHI’s administration staff has executed a wonderful job navigating the enterprise in the course of the pandemic and thru the post-pandemic surroundings. Until one thing adjustments, I’m assured that OHI will get stronger as time progresses.

Omega Healthcare Buyers

I’ve compounded my method into excessive double-digit income and wrote lined calls to extend the revenue generated

I’ve a piece of my portfolio allotted towards revenue investments, and OHI was one of many first REITs I invested in. I maintain OHI in a number of accounts, and these are the analytics on the primary group of shares I bought. Towards the top of 2017, I bought 100 shares of OHI on this account, then firstly of 2018, I bought one other 63 shares as its share worth declined. I initially invested $4,875.37 in OHI as I bought 163 shares at a median of $29.91 per share.

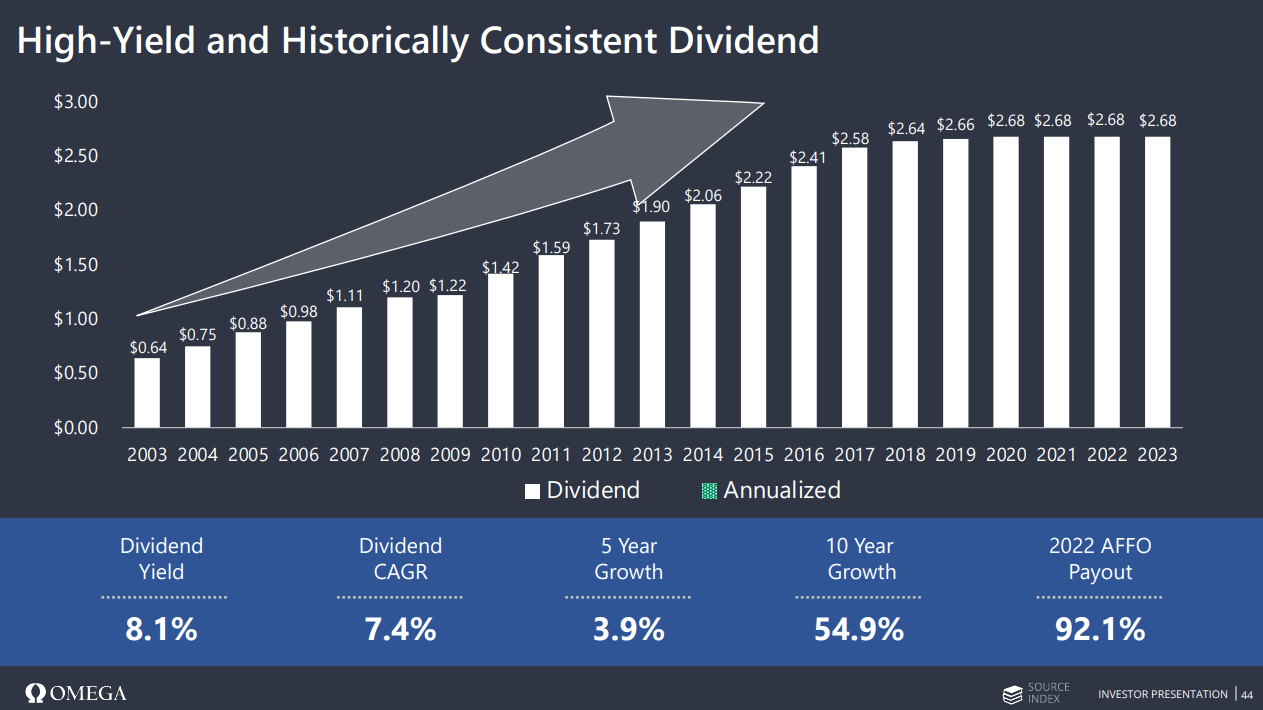

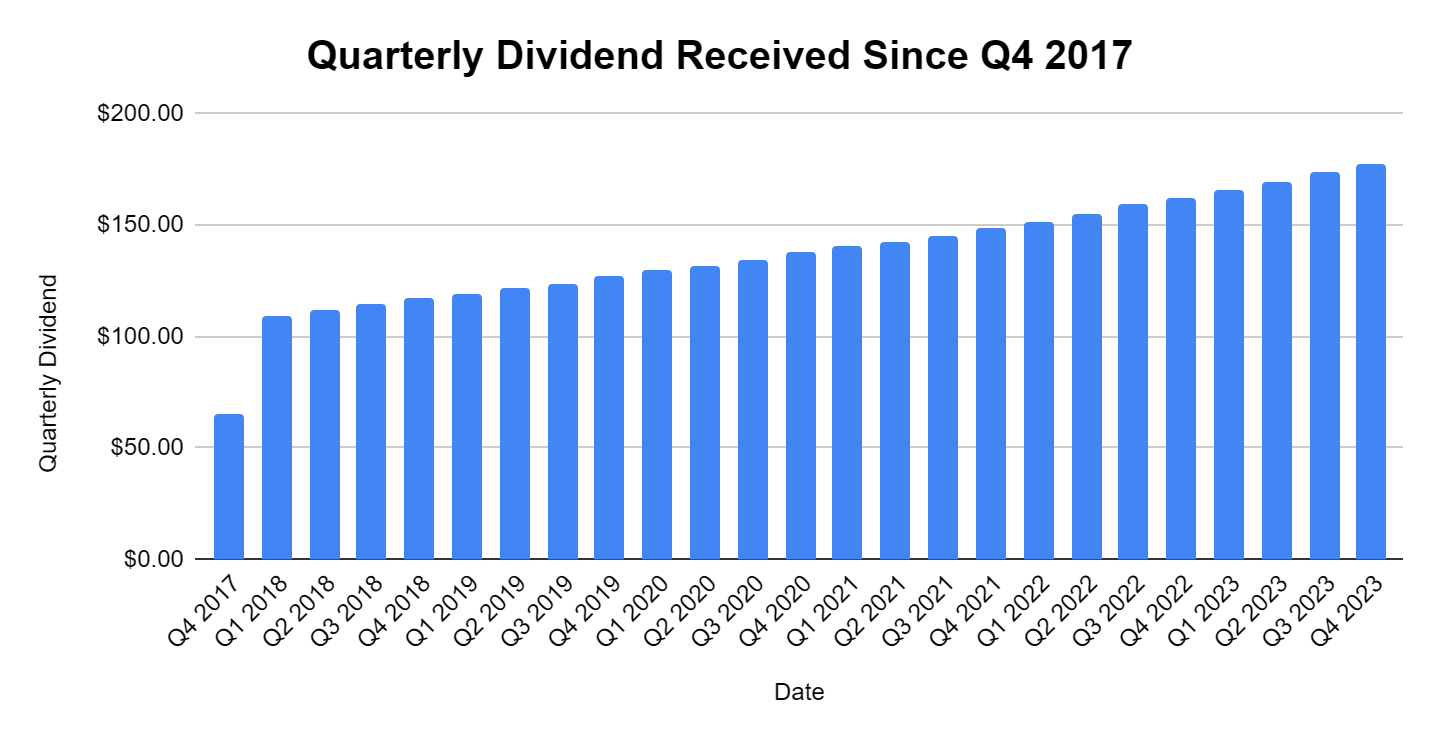

Since then, I’ve collected $3,435.83 in dividend revenue, which is 70.47% of my authentic funding. Each dividend has been reinvested, bringing my whole share rely on this account to 271 shares. Shares of OHI have appreciated by 2.71% from my common worth per share, however as a consequence of reinvesting the dividends, this funding is now price $8,325.12, which is a 70.76% ROI. I’ve collected 108 new shares from dividends, and the mixture of further shares, and the dividend development of $0.08 has elevated my ahead annual dividend revenue by 71.37%. Initially, the 163 shares generated $423.80 in ahead dividend revenue, and now the 271 shares generated $726.28 in ahead dividend revenue. Since I added 63 shares after accumulating my first dividend, I’ll use the second dividend for the following statistic. Because the second dividend that was paid, my quarterly dividend has elevated by 62.62% with ongoing QoQ development. I’ll proceed to compound my method into a bigger place and bigger ahead dividend revenue as I sit again and reinvest each dividend. That is considered one of many investments on the dividend aspect of my portfolio, and I’m excited to see how this funding grows over the following a number of years. Until my funding thesis on OHI adjustments, I plan on being a shareholder for many years to return.

Steven Fiorillo

I additionally write lined calls to generate further revenue from a number of the positions I maintain. If anybody is fascinated with lined calls, please do your individual due diligence and be sure you perceive each facet of the technique. Choices include their very own set of dangers, and I’m merely displaying how I make the most of lined calls to extend the quantity of revenue a few of my positions generate. I’m conscious of the dangers, and lined calls on this case match inside my threat tolerance.

The explanation I like to jot down lined calls on OHI is as a result of I can considerably enhance the quantity of revenue I’m producing from the place. I wish to cowl two dividend cycles in a lined name on income-producing property, so in OHI’s case, I wished to cowl the Q1 and Q2 2024 dividends, which needs to be paid in February and Could. I wrote two lined calls in opposition to 200 shares on the 6/21/24 possibility chain at a $37 strike worth. I had collected an extra $0.32 in premiums, which labored out to $0.3134 in premiums per share after the charges. If I do that twice per 12 months, I can successfully enhance the quantity of revenue every share generates by $0.63. After I take a look at the overall revenue, the dividend per share is $2.68, and once I add two lined calls to that, the extra $0.63 in premium brings the overall revenue produced per share as much as $3.31. Primarily based on the share worth of $30.72, this enables me to generate about an additional 2% of yield yearly as the present dividend has a ahead yield of 8.72%, and by accumulating an extra $0.63 in premium by two lined calls, the yield would enhance to 10.77%.

Investing in OHI comes with dangers

Simply because I’m bullish on OHI does not imply there aren’t dangers. The scenario with FAD may worsen and put the dividend in danger. If the dividend will get lowered, it may create a scenario the place shares sharply decline, as there shall be different high-yielding alternatives that grow to be extra engaging. It may additionally ship a adverse message to the shareholder base in regards to the long-term viability of the dividend. A few of OHI’s operators which are going by restructuring may face further challenges that make them flip over the keys again to OHI, and OHI’s revenue may take one other hit. Operators that aren’t in present hazard may face hassle that has lagged and put them in a scenario the place they have to go on a money foundation as effectively. Whereas OHI has executed a superb job managing threat, this has been a tough enterprise, and there are nonetheless potential headwinds on the horizon.

Conclusion

I’m bullish on OHI over the long run and suppose one other alternative is happening for revenue buyers. Shares of OHI can actually decline additional, however I really feel administration has confirmed that they’ll handle the enterprise by tough conditions and enterprise cycles. Whereas there are dangers on the horizon, I feel issues may get higher as 2024 progresses. Now we have a Fed that appears like they are going to pivot, and as the price of capital declines, operators which are having points might be able to restructure their debt maturities to extra favorable phrases. I feel OHI has the flexibility to develop its income, FFO, and FAD by 2024 and presumably get again to dividend development over the following two years. I’m bullish on OHI as I feel it can stay a strong revenue funding with prospects for capital appreciation sooner or later.