Dilok Klaisataporn

Like many tech shares, Upstart (NASDAQ:UPST) has had an ideal 12 months – the inventory no less than. The corporate continues to face rate of interest headwinds however has nonetheless managed to ship unimaginable inventory returns. The latest rally has been so sturdy that I now have a extra pessimistic view of the enterprise mannequin high quality, because it seems just like the “zero interest rate policy” of the previous is a mandatory part of the expansion thesis. The corporate has made spectacular progress in slicing prices, which will help yield working leverage upon enhancing macro situations. It’s time to downgrade the inventory as a result of the valuation seems to already be pricing in a fabric restoration, and terminal multiples are more likely to be decrease than anticipated.

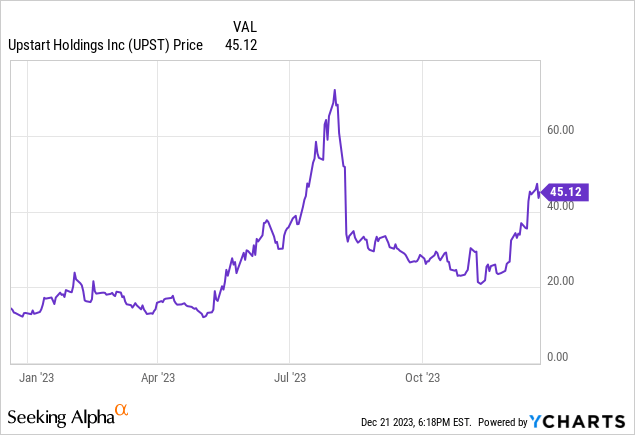

UPST Inventory Worth

UPST has delivered “multibagger” returns this 12 months after being decimated in 2022.

I last covered UPST in September the place I rated the inventory a purchase on account of the enticing valuation and enhancing basic story. The inventory has soared since then however I’m bowled over by the aggressiveness of the restoration.

UPST Inventory Key Metrics

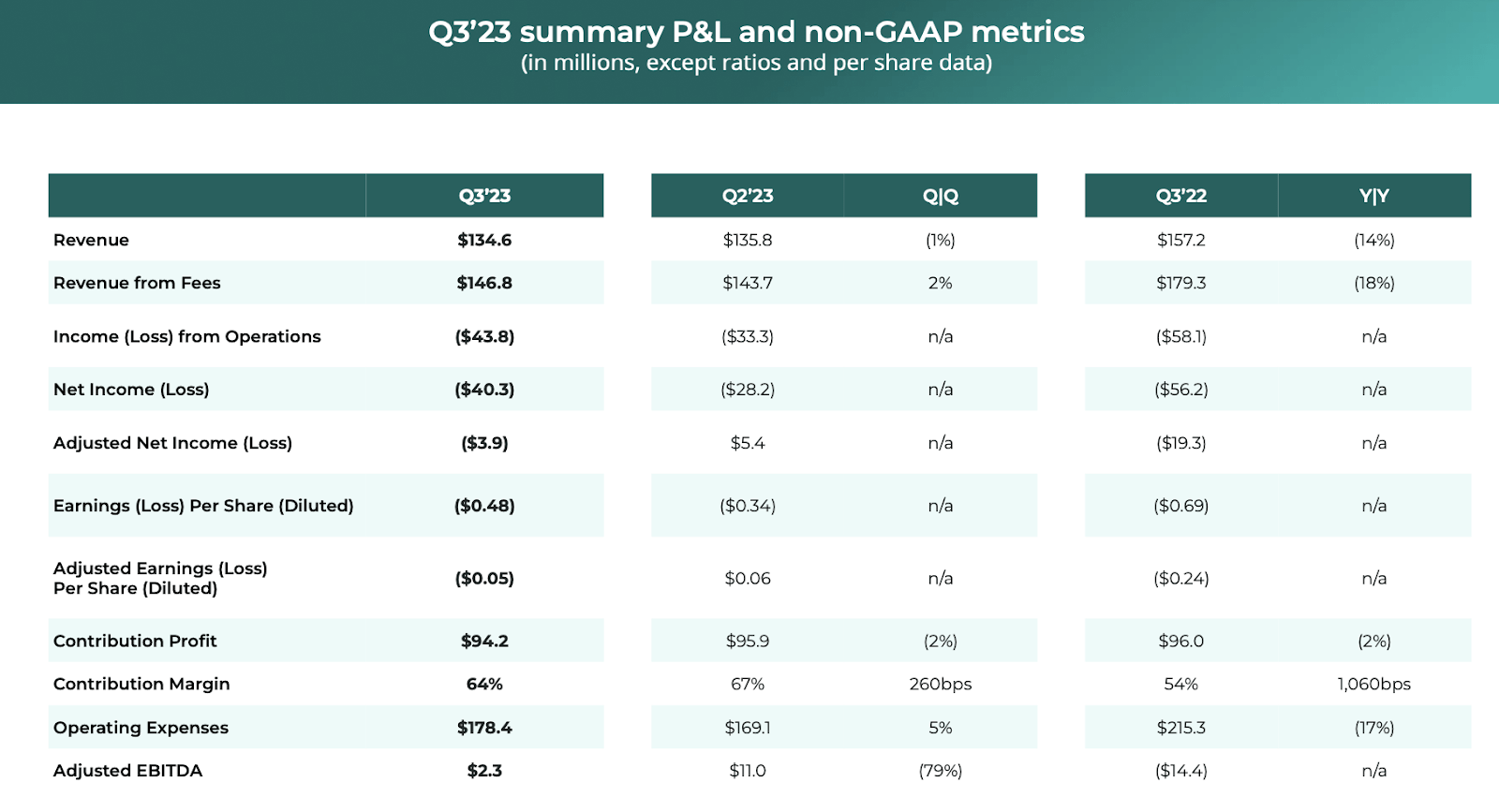

In its most up-to-date quarter, UPST noticed revenues decline 14% YoY, an enchancment from the 40% YoY decline seen within the second quarter.

2023 Q3 Presentation

Despite the top-line stress, UPST delivered $2.3 million in adjusted EBITDA, a giant enchancment from the $14.4 million adjusted EBITDA loss within the prior 12 months. Like many tech friends, UPST has sought to offset pressured top-line progress charges with working margin growth.

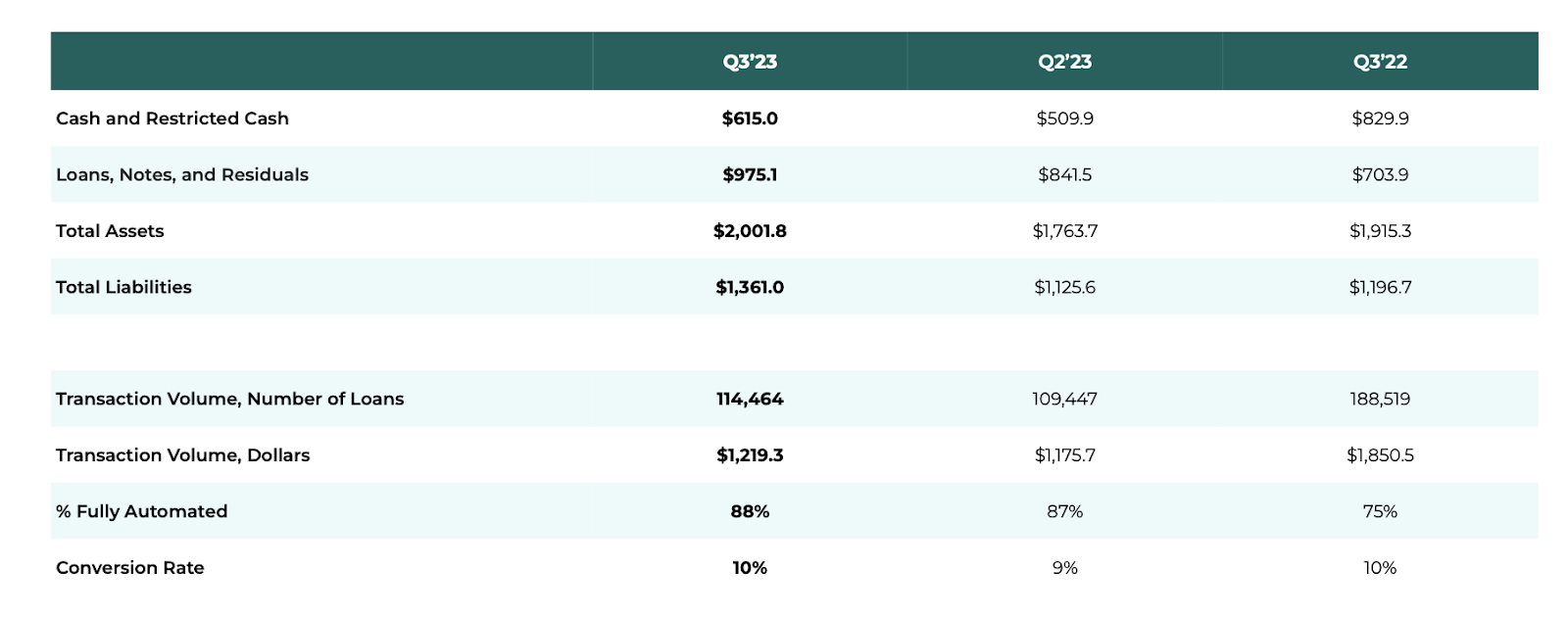

UPST ended the quarter with $516.6 million of money and $98.4 million of restricted money versus $1 billion of debt.

2023 Q3 Presentation

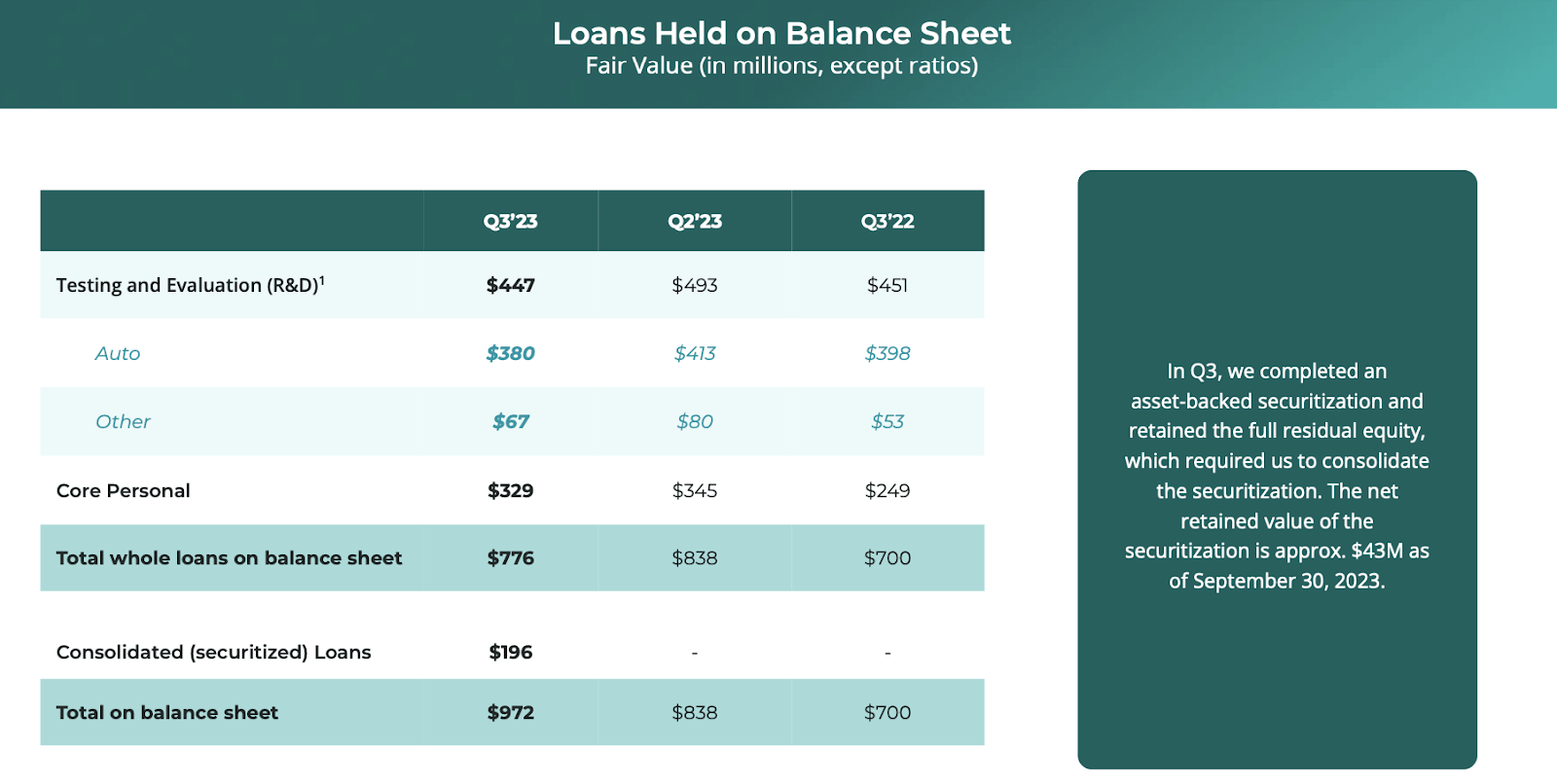

The corporate additionally had round $972 million of loans held on the steadiness sheet, with $447 million of that being thought of “R&D.”

2023 Q3 Presentation

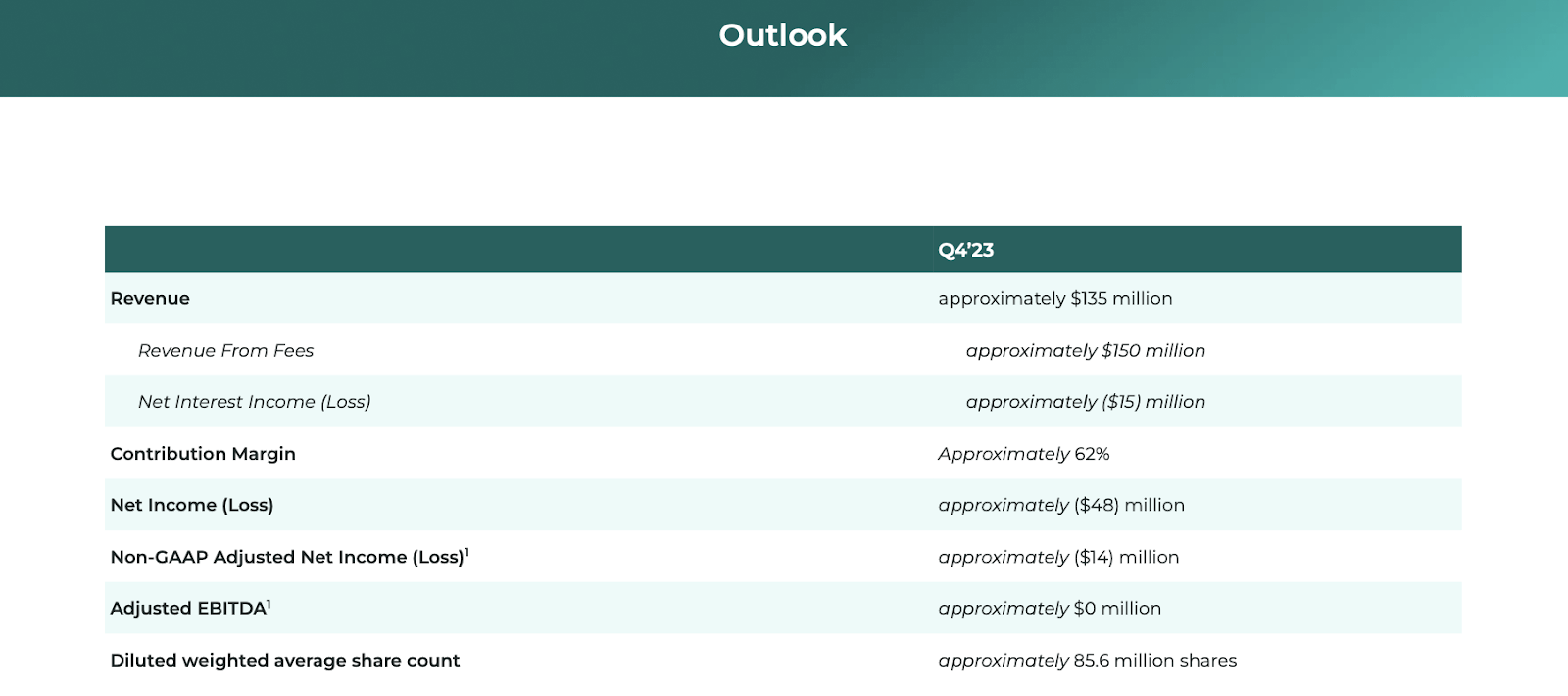

Trying forward, administration has guided for the fourth quarter to see revenues decline 8.2% YoY to $135 million, however for the adjusted web loss to say no from $55.3 million to $14 million.

2023 Q3 Presentation

On the conference call, administration talked up their ambitions in automotive lending, envisioning a future the place shoppers can seamlessly buy a automobile on-line and have it delivered on to their properties. Automated lending merchandise like these provided by UPST would go a protracted option to enabling such a future.

Administration additionally appeared optimistic as regards to their new dwelling fairness line of credit score product. Administration outlined expectations for very low annual loss charges of “1% or less” in addition to its “countercyclical” nature to their refinancing product. Administration expects their product to have benefits over rivals on account of HELOC purposes usually taking greater than a month on common for completion – UPST is aiming for “less than five days” end-to-end.

Administration continued guilty their pressured top-line progress on the upper rate of interest surroundings, noting that they’ve needed to make use of extra conservative underwriting requirements which has held again mortgage originations. Administration once more cited their 36% yield restrict as a headwind – the upper rate of interest surroundings has brought about UPST to easily outright reject many potential debtors if their calculated charge would have been above 36%. These headwinds are evident within the low conversion charges, which stood at round 8.5% within the quarter (after peaking round 24% throughout the pandemic).

UPST had beforehand garnered enthusiasm on account of securing “long” time period funding companions, however administration continues to carry substantial loans on the steadiness sheets, and acknowledged that they’ve “nothing explicit to really share” when it comes to their steadiness sheet technique transferring ahead.

Is UPST Inventory A Purchase, Promote, or Maintain?

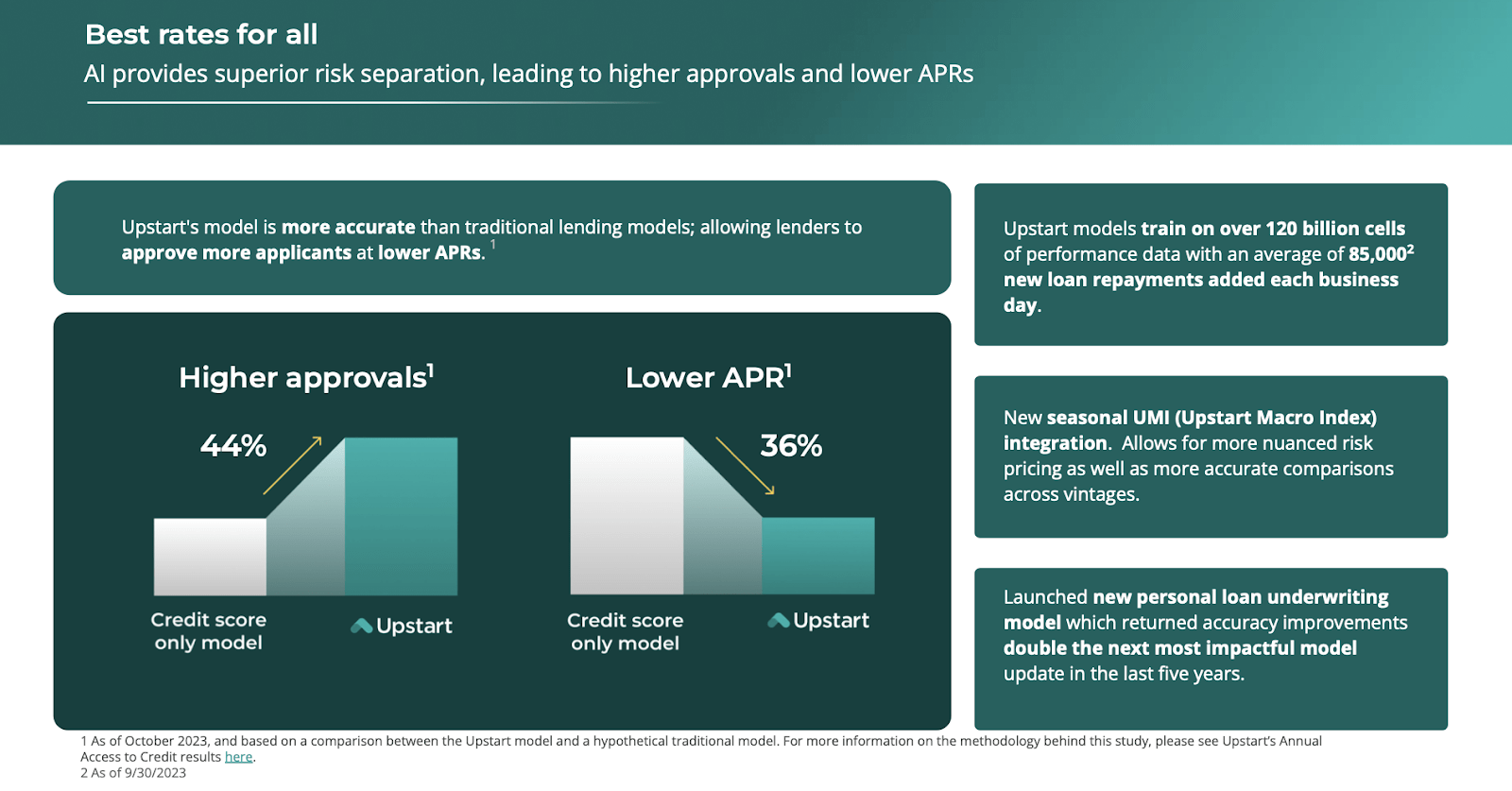

The sturdy latest value motion is clearly not because of the basic outcomes, which proceed to point out that the corporate struggles to seek out footing amidst the next rate of interest surroundings. As a substitute, I discover it doubtless that traders are hoping that the Fed’s recent comments regarding 2024 rate cuts might indicate an eventual return to a zero rate of interest coverage. UPST can also be benefiting from its positioning as an AI-first lender, as the corporate’s core mission has been to make the most of synthetic intelligence to be able to improve approval charges.

2023 Q3 Presentation

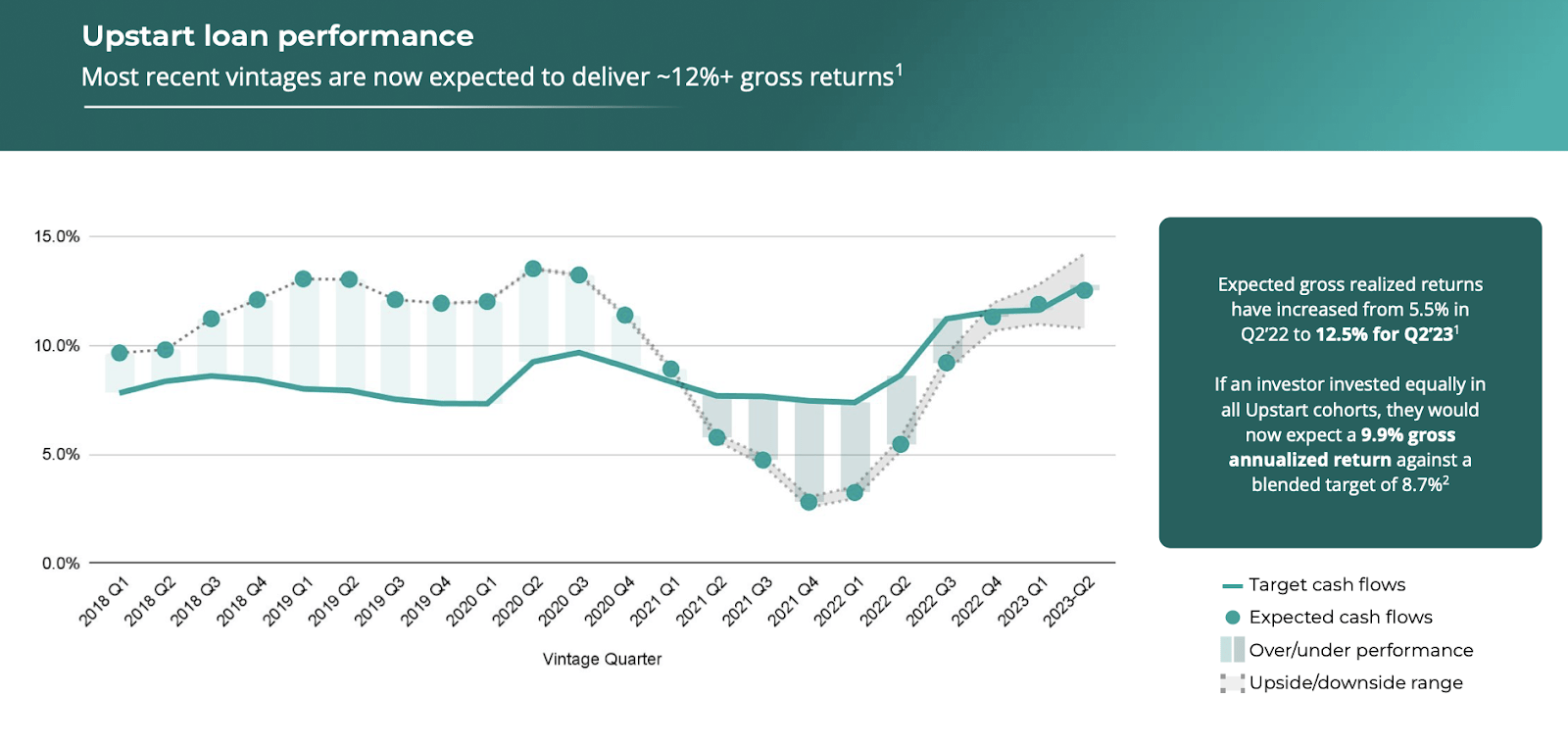

UPST noticed its threat algorithms underperform over the previous two years however these outcomes seem like normalizing as of late.

2023 Q3 Presentation

As of latest costs, UPST was buying and selling at round 7.3x this 12 months’s gross sales. Previous to the 2022 tech crash, UPST was considered by many (or no less than by yours really) as having secular progress on account of with the ability to take market share in mortgage originations on account of its AI-powered platform. At this level, such a view seems shaky at greatest, as the corporate has seen progress charges battle amidst funding points.

In search of Alpha

The corporate has been producing higher-than-typical contribution margins at nicely over 60%, however I view 45% to 50% as being a extra normalized charge as that’s what the corporate was reaching in 2021. A 50% web margin primarily based on contribution income seems like an affordable assumption long run, which equates to round a 25% web margin primarily based on revenues. If rates of interest can fall again to zero, then UPST may rapidly return to producing a $850 million income run-rate because it did in 2022. Progress may hover round 20% or greater as funding companions are desirous to earn the next yield on invested capital. At a 1.5x value to earnings progress ratio (‘PEG ratio’), I might see UPST buying and selling at round 7.5x gross sales, implying appreciable upside even at simply the 20% progress assumption.

Nevertheless, that view is ignoring the extra essential element: UPST has seen its enterprise mannequin battle mightily during the last many quarters amidst the rising rate of interest surroundings. The ever-present threat of rates of interest rising might imply that UPST deserves to commerce at extra discounted valuations. At a 0.75x PEG ratio, the inventory would commerce round 3.8x gross sales, implying that the inventory is already buying and selling as if rates of interest have collapsed.

A very powerful query is whether or not the corporate can ship sturdy and worthwhile progress even with out a decline in rates of interest. I view this to be an insurmountable process provided that funding companions could also be reluctant to commit capital to excessive yielding investments as the next rate of interest surroundings seemingly will increase recession dangers. Shopping for UPST immediately seems to be primarily based on hoping for each rates of interest to fall in addition to for the final funding group to rapidly neglect concerning the enterprise struggles of the previous 12 months. Sure, the inventory can ship unimaginable returns if it could garner premium valuations, however it’s troublesome to suggest shopping for this inventory on the present valuations with any type of conviction. Provided that the present inventory value seems to be pricing in an enchancment within the macro surroundings already, I need to downgrade the inventory to “hold” as I can not say with nice certainty that the inventory will outperform the broader market transferring ahead.