Nikada

PennantPark Floating Price Capital (NYSE:PFLT) is a slightly typical BDC, which seeks to generate high-yielding streams of present earnings and, to a lesser extent, NAV appreciation.

PFLT, as most BDCs, targets core center market funding alternatives. The investments are made in firms, that are primarily backed by PE homes. By way of the financing options, PFLT is theoretically versatile to offer capital throughout numerous segments reminiscent of senior secured debt, junior debt, subordinated debt, non-controlling fairness and so on.

In response to PFLT’s funding coverage, the Fund incorporates a few overarching ideas in its funding decision-making:

- Deal with capital preservation.

- Identification and bias in direction of sturdy money flows.

- Sponsor-backed.

In lots of circumstances BDCs are inclined to assume further danger (on prime of personal credit score issue) by allocating into riskier companies with an try to seize incremental foundation factors in yield.

Nonetheless, right here it’s price underscoring PFLT’s consideration to money producing firms with comparatively predictable and secure enterprise fashions, which clearly implies decreased publicity to VC-type, speculative investments.

Let’s now discover PFLT’s underlying portfolio and attempt to decide whether or not PFLT appears to be like enticing contemplating the dangers and potential return profile.

Portfolio construction

As acknowledged a bit earlier, there’s nothing extraordinary with PFLT’s portfolio within the context of common BDC gamers.

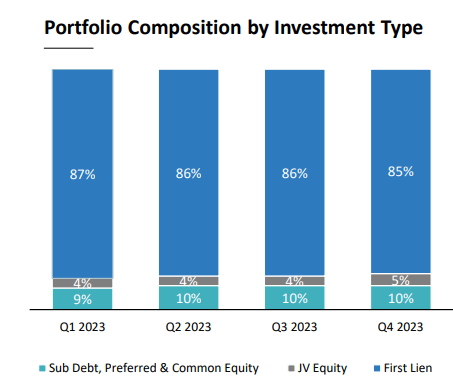

For instance, the portfolio construction by funding sort signifies stability and an enormous skew in direction of first lien investments.

PFLT Investor Presentation

The truth that the lion’s share of PFLT’s portfolio is defined by first lien investments and solely a comparatively minor half is attributable to different and inherently extra dangerous funding sorts confirms that on a elementary degree PFLT performs a conservative recreation.

Usually, amongst different BDCs the primary lien bucket constitutes 70-80% of the whole AuM, so from this attitude, we may argue that PFLT is positioned its enterprise in a barely extra defensive method than common BDC title.

PFLT Investor Presentation

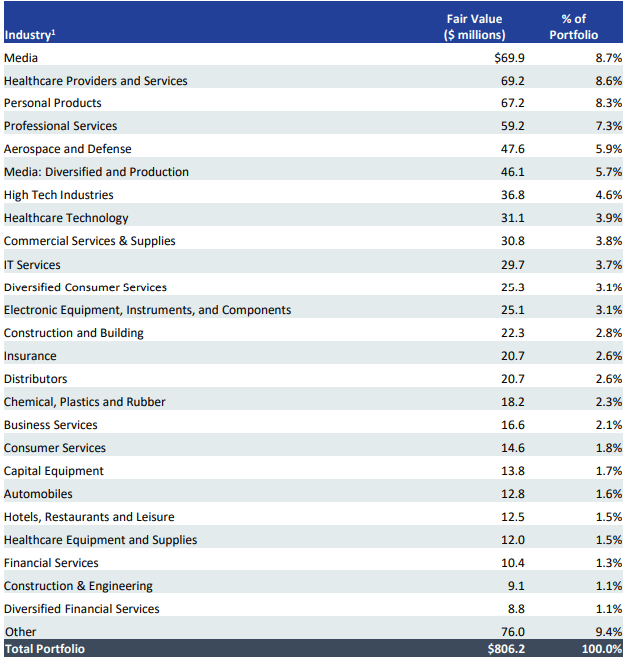

Furthermore, if we categorical PFLT’s portfolio in industry-level, we are going to discover a really diversified image with no important focus dangers in particular industries or financial segments.

A very powerful takeaway from the desk above is that there is no such thing as a materials publicity in direction of inherently speculative industries reminiscent of high-tech, building and life sciences.

Lastly, as PFLT’s title already implies, all the fastened earnings based mostly investments are structured with variable price part permitting PFLT to completely seize the advantages of upper rate of interest surroundings.

Thesis

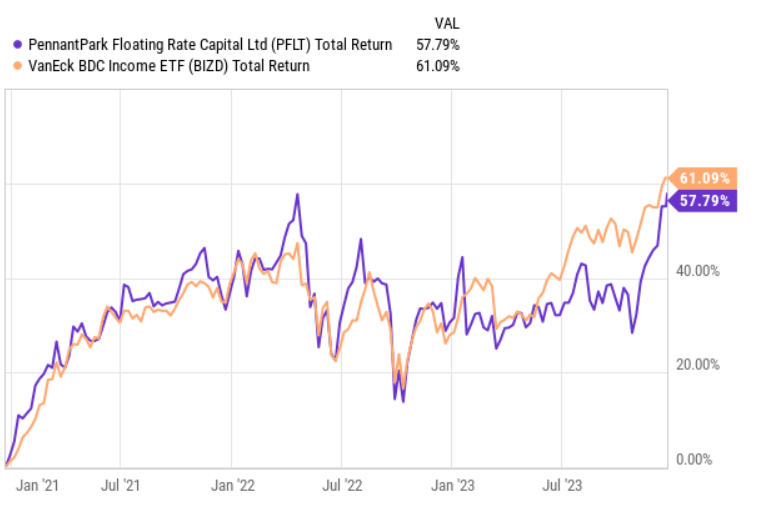

Up to now 3-year interval, PFLT has carried out according to the general BDC market benefiting from the favorable surroundings that’s related to increased rates of interest and stronger demand for personal credit score options.

YCharts

It’s fascinating that PFLT has not managed to seize an alpha contemplating that your complete portfolio relies on floating devices, which has not been the case for different BDCs. In different phrases, theoretically, PFLT ought to have registered a bit higher returns since there was no component of fastened price funding, which has imposed difficulties for many BDCs to completely profit from extra enticing SOFR.

The offsetting issue, for my part, has been the defensive focus of PFLT to keep away from overly dangerous investments, which have these days carried out fairly properly (e.g., life science companies, excessive tech and so on.). Particularly, up till now now we have not observed a significant uptick in bankruptcies of money burning or speculative companies that has helped extra risk-seeking BDCs to maintain amassing increased yielding coupons.

With that being stated, I feel that there are two further causes on prime of the defensive portfolio construction that make PFLT an fascinating BDC.

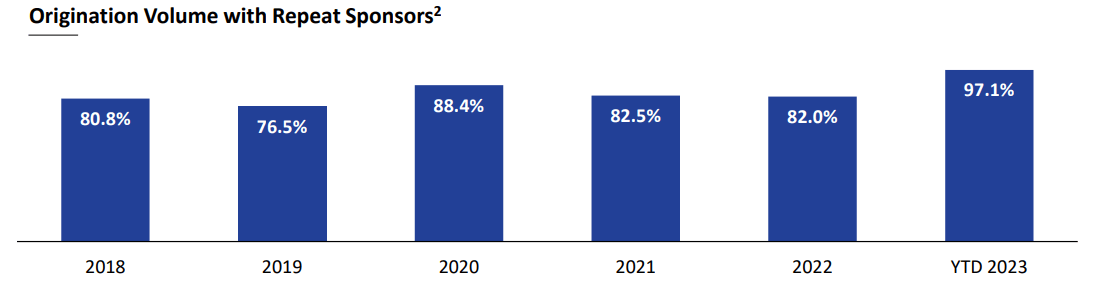

First is the historic monitor document of repeat sponsor transactions.

PFLT Investor Presentation

Since 2018, over 75% of PFLT’s offers have been with repeat sponsors, which introduce efficiencies and total predictability of the additional investments. The truth that PFLT can to a big extent depend on the identical sponsors is important, particularly on condition that PFLT is thought for its portfolio high quality (i.e., with very minimal write-downs).

In the newest earnings call, Artwork Penn – Founder, Chairman & CEO, captured this reality properly:

Our credit score high quality since inception over 10 years in the past has been glorious. PFLT has invested $5.3 billion in 468 firms and now we have skilled solely 18 non-accruals. Since inception, PFLT’s loss ratio was solely 15 foundation factors yearly.

Plus, within the Q4, 2023, PFLT did document any write-down in any respect.

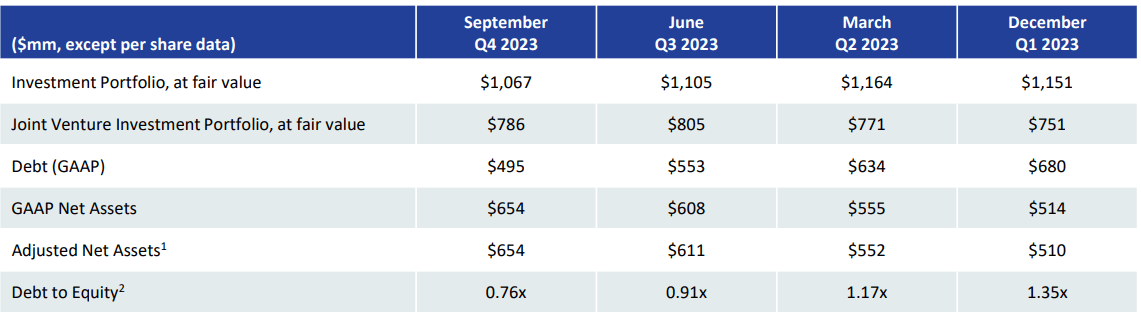

Second component, which renders PFLT’s funding case fairly interesting is the extent of exterior leverage.

PFLT Investor Presentation

Since Q1, 2023, PFLT has constantly decreased its reliance on exterior debt, whereas sustaining its dedication to dividends and in addition managing to extend its web asset base.

A debt to fairness under 1x may generally be deemed as a protected degree in comparison with common indebtedness within the BDC sector. In PFLT’s case, the leverage is considerably under that signaling better security and decrease danger of experiencing notable write downs throughout recessionary market situations.

Now, although PFLT appears to be like extra protected and resilient from the important thing points reminiscent of funding sort, {industry} focus and leverage, the present yield is definitely not that low.

Presently, PFLT distributes 10.4% in yield, which is completely according to the BDC average that might be achieved by way of passive technique.

The one caveat when it comes to the dividend yield is the ratio between NII and dividend per share. The dividend protection within the final two quarters stood at ~96%, which clearly signifies a low margin of security.

Nonetheless, it’s extremely unlikely that PFLT must revisit its present dividend. I’d anticipate PFLT to go up a bit within the leverage so as to accommodate new investments, which, in flip, ought to present a lift to the NII part. In actual fact, prior to now convention name Artwork Penn gave unambiguous alerts on rising deal exercise going ahead:

We’re seeing a rise in deal move in comparison with the primary half of 2023 and have a rising pipeline of fascinating and enticing funding alternatives. Since quarter-end, we have continued to be energetic from September 30 by way of November 10, we have invested $76 million into new and current investments and are persevering with to see sturdy deal move going into year-end.

The underside line

In my view, PFLT provides an interesting alternative for BDC buyers to seize above 10% yield together with stable and resilient underlying fundamentals.

Presently, PFLT’s yield is on the identical degree as for the general BDC sector. But, if we take a deeper have a look at the portfolio and financials, it’s evident how PFLT is a far more safer BDC automobile than common participant on this sector. For instance, PFLT carries a lot decrease exterior debt load, there is no such thing as a large publicity to speculative industries and the state of affairs of no write downs speaks for itself.

In a nutshell, PFLT provides an excellent danger and return profile by way of which I’d go lengthy on the BDC issue.