Ivan-balvan

The AMD Funding Thesis

Fueled by the AI hype, Superior Micro Gadgets, Inc. (NASDAQ:AMD) has had a unbelievable yr when it comes to its inventory worth. By promoting CPUs, GPUs, and licensing expertise to different corporations, AMD captures the spirit of the occasions. Its high-performance, value-priced merchandise enchantment to prospects starting from information facilities and enormous enterprises to people and players.

Mixed with vitality effectivity and excessive reliability, this helps AMD keep a loyal buyer base and compete for market share. Regardless of this, AMD remains to be underestimated, despite the fact that they’ve an distinctive R&D observe report and have taken on Goliath earlier than within the type of Intel (INTC). And this time, the Goliath is NVIDIA (NVDA).

AMD Vs. Intel In The CPU Market

What many by no means thought potential was that AMD would be capable to break Intel’s stranglehold on the CPU market, however AMD has finished it. There was a time when Intel dominated all of the benchmarks and had superior expertise. However as of today, AMD’s Ryzen 9 7950X3D might be the perfect gaming processor, and the AMD Ryzen 9 7950x is the perfect on the subject of multi-core utilization. Nonetheless, Intel’s Core i9 14900k with 24 cores is the quickest single core. The 8 efficiency cores and 16 environment friendly cores work effectively to assist Intel win the neck-and-neck race on this phase.

Nonetheless, AMD has a brand new HEDT with the Ryzen Threadripper 7000 that’s presently nearly unequalled within the workstation market, however HEDTs usually are not a mass product as they’re very costly. The 7980X, for instance, prices $4999. However general, AMD processors are undoubtedly higher at multitasking as a result of they have an inclination to have extra cores, threads, and reminiscence, and they’re extra vitality environment friendly. However Intel has its strengths too, as its single-core processors are nonetheless the perfect, however AMD might declare that title sooner or later. A giant win for AMD, for instance, was their Ryzen 7 5700k, which beat the Core i5 and thus secured AMD the win within the cheaper price phase.

Normally, nevertheless, I imagine that each corporations will proceed to dominate the CPU market as a result of they’re far forward of the competitors on this phase and the demand for CPUs is excessive and can stay so. Nonetheless, the marketplace for CPUs for cell phones will most likely turn into extra vital as effectively, the place there are different robust gamers.

AMD’s focus on Chiplet has clearly helped them up to now, because the waste fee is far decrease in comparison with Intel’s monolithic method. Intel has seen this as effectively and launched the primary Chiplet lineup with Meteor Lake. However AMD clearly has a bonus as a result of they’ve been working with this expertise longer and extra deeply.

AMD Vs. NVIDIA In The GPU Market

One of the vital carefully watched battles proper now could be NVIDIA vs. AMD within the GPU market, particularly when it comes to AI purposes. After buying ATI in 2006, AMD started to compete within the graphics card market the place NVIDIA has clearly set the traits and requirements for years. Raytracing, Upscaling DLSS, and G-Sync are just some of the improvements in recent times which have helped NVIDIA keep on high and dominate the benchmarks with its flagship fashions. This enables NVIDIA to justify the premium worth of its GPUs, though there are some who say that AMD typically provides higher worth.

AMD is dedicated to creating its applied sciences obtainable to as many customers as potential, and FSR is even appropriate with graphics playing cards from the competitors. Their method is to be open supply and to make use of trade requirements. NVIDIA takes a special method. Improvements are sometimes not backward appropriate, e.g. DLSS V3 is just appropriate with RTX 40 sequence playing cards, and NVIDIA undoubtedly doesn’t have an open supply method. As well as, NVIDIA has an ecosystem that’s clearly designed to lock prospects into the NVIDIA ecosystem and create excessive obstacles and prices to switching.

Each approaches have their benefits and drawbacks, however I’d say that NVIDIA’s CUDA presently has a aggressive benefit as a result of it’s simpler to implement and the efficiency is barely higher than AMD’s open supply ROCm. So on the software program aspect, NVIDIA remains to be forward in the mean time. However a few years in the past, everyone thought Intel was a number of years forward of AMD and AMD was underestimated, and that might be the case on this state of affairs as effectively. Though NVIDIA might be stronger than Intel was then. However AMD is already making an attempt to push Ethernet as the usual for AI networks and to displace NVIDIA’s InfiniBand in an effort to weaken NVIDIA’s aggressive benefit.

Within the mid-range of graphics playing cards, the RX 7800 XT may be even higher than the 4070 sequence, and the RX 7800 usually has a unbelievable worth/efficiency ratio. However on the subject of most efficiency, the NVIDIA GeForce 4090 might be the perfect card on the market proper now. However AMD has its strengths in vitality effectivity and value effectivity. Normally, I feel the main focus shouldn’t be on who’s stronger, however that the scenario is just like Visa (V) and Mastercard (MA). That’s, each exist aspect by aspect and each profit from the growing demand. The market is sufficiently big for each to generate unimaginable shareholder returns over the following 10 years.

AMD’s partnership with HP and Lenovo within the pocket book area ought to drive gross sales, and AMD’s CDNA with Infinity Material Expertise and high-bandwidth reminiscence is delivering vital enhancements in AI efficiency. Particularly, CDNA 3 delivers improved efficiency and effectivity.

AMD had a powerful exhibiting with their MI300x once they launched it on December sixth and confirmed that it outperformed NVIDIA’s AH100. NVIDIA responded by releasing their very own benchmark that reveals the AH100 remains to be higher with the best settings. AMD responded by releasing a brand new benchmark that after once more confirmed the MI300X outperforming with the best settings. Which settings are right and whether or not AH100 or MI300X is stronger is secondary in my view. The vital truth is that AMD can compete with NVIDIA on this space and that each corporations have extremely highly effective options for AI. And are subsequently completely positioned for the long run.

AMD’s Metrics and Steadiness Sheet

With $5,785 million in money + ST investments versus $1,715 million in LT debt, AMD has a very secure balance sheet. The debt might be simply serviced with money and subsequently the draw back threat is protected when it comes to stability sheet high quality. And if we have a look at the income statement, we see that curiosity earnings is increased than curiosity expense, one other signal of monetary stability.

- Curiosity Revenue: $179m

- Curiosity Expense: $98m

What’s not so good, nevertheless, is that shares excellent are steadily growing, and SBC had extremely giant will increase in 2022 and 2023. SBC elevated from $379 million in December 2021 to a TTM worth of $1,325 million. That is practically a fourfold enhance in two years.

Adjusted TTM FCF is subsequently $2,758 – $1,325 = $1,433 million, which is just half of what it seems like at first look.

AMD’s Capital Allocation And ROIC

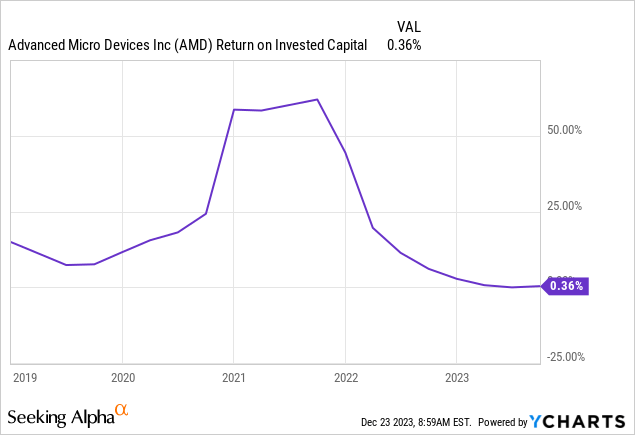

If somebody had been to make use of a easy display for prime ROIC corporations, AMD wouldn’t seem proper now. Below regular circumstances, I’d have a look at the ROIC-WACC unfold, however on this case, it doesn’t make sense as a result of with an ROIC that’s virtually zero, the unfold is unfavorable. Nonetheless, given the significance of R&D and mental property within the industries wherein AMD competes, I count on AMD’s ROIC to extend within the coming years as its investments bear fruit. So I count on them to have a powerful unfold in some unspecified time in the future within the subsequent 3 to five years. And allow us to not neglect that corporations that enhance their ROIC are among the many finest investments if we can rely on Professor Mauboussin’s research.

AMD’s Reverse DCF

Creator

AMD’s reverse DCF is a difficult one. The TTM diluted EPS just isn’t acceptable and we should always use a normalized one as a result of quickly growing revenues, value of gross sales, and working bills. So, with normalized EPS of $2 and a hurdle fee of 15%, the inventory has priced in an EPS CAGR of 25% over the following 10 years.

The required development fee is certainly very tough to attain, however AMD has the expansion alternative to do it. However will probably be a hell of a job even with the TAM they’ve.

What might EPS appear to be in 5 years?

I might see $4 to $5 EPS in 5 years. However with an organization like AMD in such a fast-growing and altering market, it’s like enjoying the lottery to present an EPS estimate 5 years out. I feel it’s higher to take a look at their place within the CPU and GPU market and that they’re within the high 2 in each and subsequently will profit from all the expansion. And even when the EPS is decrease in 5 years, they might nonetheless make a really engaging return primarily based on development and the market atmosphere.

Conclusion

AMD is in two very important industries the place they’ve a powerful aggressive presence. Very excessive obstacles to entry within the type of know-how and a small pool of people who find themselves actually consultants on this space will defend revenues. Even with limitless sources, it’ll take years for the competitors to succeed in the extent of NVIDIA, AMD, or Intel.

Nonetheless, dependence on key suppliers equivalent to chip producers provides corporations equivalent to TSMC (TSM) some bargaining energy. On a optimistic be aware, nevertheless, the truth that Meta (META) and Microsoft (MSFT) wish to purchase AMD’s latest AI chip as an alternative to NVIDIA’s undoubtedly speaks in favor of AMD’s chips. Due to this fact, I feel AMD remains to be underappreciated once we have a look at their success with the newest AI chips, their market share improvement over the previous few years within the CPU and GPU market, and the potential for market share beneficial properties sooner or later.

And even when AMD stays the perennial quantity 2 within the GPU market, that must be sufficient to develop earnings and income at an unimaginable fee. There are numerous examples the place being the second-best firm in a market has additionally been an incredible funding. And in the event that they proceed to execute with excellence, AMD nonetheless has a shot at difficult NVIDIA’s lead.