OGphoto

Introduction

At our Conservative Revenue Portfolio service, we search for under-the-radar bargains. KMPB is one instance, and I’m the one In search of Alpha analyst protecting this very attention-grabbing and undervalued baby bond.

Kemper Company

Kemper Corp. (NYSE:KMPR) is a well known insurance coverage firm, truly a household of insurance coverage firms. The truth that their title is well-known could also be partly as a result of Kemper Open golf match which they sponsor. KMPR is a diversified insurance coverage firm that points not solely property/casualty insurance coverage insurance policies but additionally well being and life insurance coverage insurance policies. They’ve over $13 billion in property, have issued 5.3 million insurance policies, and are represented by 26,000 brokers and brokers. A.M Finest charges KMPR as A- (glorious).

Their auto insurance coverage phase was struggling like different auto insurers, and so they have been planning on elevating costs to repair this example. However not too long ago, they made the choice to easily exit the auto insurance coverage enterprise. In line with the three analysts on Yahoo Finance, earnings are anticipated to leap to $3.88 per share in 2024 in consequence. Simply a few days in the past, dealer Piper Sandler introduced that they have been sustaining their obese ranking on KMPR and boosted their value goal from $47 to $56 per share.

These earnings estimates are a bit stale and given the massive rally that we’ve had in bonds over the past a number of weeks, I’d count on KMPR to beat these estimates as, like nearly all insurance coverage firms, they maintain a big portfolio of bonds. So they’re seeing large good points of their portfolio now.

Kemper carries an funding grade credit standing of Baa3 from Moody’s and BBB- from S&P.

Kemper Child Bond

KMPB has issued just one child bond, and it’s an uncommon one. That’s as a result of, on its name date, the yield will reset based mostly on the U.S. 5-year Treasury word yield. Let’s take a look at among the numbers concerning this bond.

Final Value $19.45

YTM – unknown as a result of reset charge

Name Date 3/15/2027

Maturity Date 3/15/2062

Yield to Name 15.19%

Reset Charge On Name Date – 5-Yr T-note yield plus 4.14%

10.36% Yield to Maturity If It Resets At Right this moment’s 5-Yr Notice Yield of three.88%

Junior Bond

Credit score Ranking Ba1 From Moody’s and BB+ from S&P

An important factor to notice is that regardless of the 5-year word yield not too long ago falling from almost 5% to right this moment’s 3.88%, on 3/15/2027 the yield on KMPB will nonetheless soar to 10.36% if we’re at right this moment’s 5-year word yield. That’s an unbelievable yield for a bond from an funding grade firm in what’s now a decrease rate of interest setting for lengthy bonds. So though the maturity on the bond may be very lengthy at 2062, that is actually a play on this bond for the following 3.25 years till its name date.

With that form of reset charge, KMPB has a really excessive chance of rising considerably in value over time as we transfer towards 2027. The truth is, it was buying and selling over $25.00 previous to the Fed charge will increase. Though I feel it unlikely that KMPB will probably be referred to as, which would offer a 15.19% yield to name, I consider capital good points plus the present yield can present a 12% annual return or higher between now and its name date. And even at its present yield, pre-reset, it’s engaging relative to different bonds with the identical credit standing, which I’ll present later.

One factor to notice is that KMPB is a junior bond, which is why it’s rated one notch decrease than KMPR’s normal BBB-/Baa3 rated bonds. A junior bond permits curiosity funds to be deferred for as much as 60 months, however within the a long time I’ve been investing in fixed-income, I’ve by no means seen an organization defer funds on a junior bond and any deferred funds are cumulative. The credit standing already takes the truth that this can be a junior bond into consideration, so it may be in comparison with different bonds with the identical ranking.

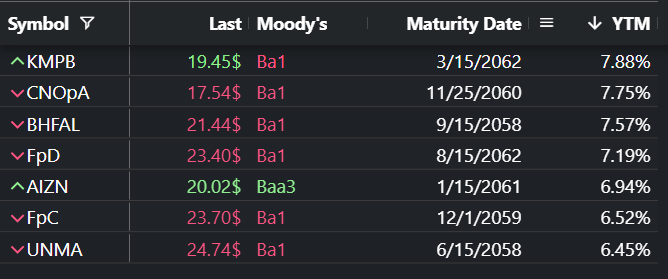

KMPB’s Undervaluation In contrast With Equally Rated Bonds

Creator

Above is a listing of all of the Ba1 rated child bonds with lengthy maturity dates like KMPB. AIZN exhibits a Baa3 ranking, however QuantumOnline.com exhibits that it’s a Ba1 rated bond, and S&P provides AIZN the identical ranking as KMPB. As a facet word, BHFAL can also be a junior bond like KMPB.

So even with out factoring in KMPB’s glorious reset charge, which is prone to transfer its yield manner above its friends, KMPB is undervalued. And on prime of that, KMPB is a a lot shorter play than these different bonds as we’re actually KMPB as a 3.25-year funding or shorter the place we count on to attain a big whole return. I do not consider this as a 39-year bond and do not count on to carry it past its name date until it’s nonetheless undervalued and yielding above its friends.

Though the above record exhibits that KMPB is considerably undervalued, it leaves out the truth that KMPB is the one certainly one of these that has a reset-rate which is able to doubtless considerably enhance its YTM sooner or later, making it very undervalued. So the market appears to be completely ignoring the precious reset charge when pricing KMPB. The reset-rate additionally supplies nice rate of interest safety, which the others haven’t got.

Interactive Brokers

It is a scatter plot of all long-term Ba1 rated conventional bonds. As you possibly can see, the common YTM is definitely nearer to six.5% making KMPB’s present yield greater than 1% larger than its Ba1 rated peer bonds, and once more, this offers no worth to KMPB’s reset-rate. It’s shocking how the market is completely overlooking its reset-rate, however the market’s blindness is our achieve.

KMPB’s Wonderful Curiosity Charge Safety And Unfold Over Treasuries

The great thing about KMPB is that it really works effectively if rates of interest rise and likewise in the event that they fall. This is essential on this unsure setting, and particularly for very long-term bonds, which may be crushed by larger rates of interest. We noticed banks that personal long-term treasury bonds and different long-term devices get crushed as the worth of their bond holdings crashed when charges rose. Beneath is a chart of an funding grade bond image MGRD to point out you what has occurred to its value because of larger rates of interest.

Yahoo Finance

As you possibly can see, it fell in value from $25 to $15 and has solely gained a little bit of that again as a result of giant drop in long-term charges we’ve seen in current weeks.

Not like different long-term bonds, the explanation KMPB will do nice if charges rise is that the reset charge at present charges is already 10.36% and that yield will rise in tandem with any rise within the 5-year word yield. If the 5-year word is yielding 6%, the reset yield on KMPB at its present value will turn out to be 13.33%. So completely no worries right here if charges rise. The truth is, this bond will do nice if charges rise and is an efficient defensive play in your portfolio to offset your different bonds that can do poorly if charges rise.

And since the present reset yield of 10.36% supplies a selection of 6.48% over the present 3.88% 5-year word yield, wherever charges go, even when they go decrease, that is a gigantic unfold over treasury yields for a bond from an funding grade firm. If the 5-year word drops to 2.25% by the reset date, the yield on KMPB will regulate to eight.4%. That will probably be an unlimited yield in a 2.25% rate of interest setting, and the value of KMPB ought to nonetheless see a superb measurement rise in value. The truth is, this safety was issued at $25 with a mere 5.875% yield, so this reset yield will probably be very engaging in a considerably decrease rate of interest setting. So we actually have a win/win scenario right here.

Abstract

It seems to be to me that the market is completely lacking that this bond (NYSE:KMPB) has a reset charge, which is why it trades so cheaply. As I wrote earlier, KMPB flies completely beneath the radar and I’m the one In search of Alpha analyst protecting this child bond. Even with out the reset charge, KMPB trades cheaply so when the reset charge is factored in, KMPB is very low-cost/undervalued.

Within the article, we confirmed that KMPB presently has the best yield of all Ba1 rated child bonds, and we seemed on the typical Ba1 rated conventional bond yields and located that KMPB’s yield is greater than 1% larger in yield.

However most significantly, KMPB can be a 3.25-year funding and never the lengthy bond funding that buyers appear to be targeted on. On its name date, it would reset to a yield of 10.36% at right this moment’s 3.88% yielding 5-year Treasury word. And we famous that the ten.36% reset charge is a big unfold over the present 3.88% 5-year Treasury word yield.

So we’ve an enormous winner if charges rise. If the 5-year word is 6% on its reset date, the yield on KMPB will skyrocket to 13.33% and will definitely see a big rise in its value with such an enormous unfold over treasuries. It might effectively be referred to as at $25 for a 15.19% annual return. If charges fall, the reset yield will even fall from 10.36%, however it would all the time be manner above the present treasury yield, which must also result in a pleasant value rise. Having a fixed-income safety which is able to doubtless go up whether or not charges go up or down is a precious safety.

KMPB was initially issued at a 5.875% yield at $25. It is rather laborious to see an rate of interest state of affairs that will not ship KMPB considerably larger over time as we head towards its name date in early 2027.