kafaca/iStock through Getty Pictures

Introduction

Usually talking, I’m not a giant fan of restaurant shares, which explains why I’ve by no means mentioned Chipotle Mexican Grill (NYSE:CMG) on In search of Alpha or anyplace else.

What has stored me from shopping for restaurant shares is my give attention to wide-moat companies. As a rule, eating places are uncovered to extreme competitors on high of the standard financial dangers like shopper well being and enter inflation.

In accordance with BinWise (emphasis added):

Roughly 60% of eating places fail inside the first yr of operation and 80% fail inside the first 5 years.

These numbers could appear off-putting, however the remaining 20% of eating places go on to seek out long-term progress and success.

Apparently, eight out of ten eating places fail inside 5 years!

That is brought on by components like unhealthy areas, inexperienced administration and staff, inflated prices, pricing issues, an absence of advertising, and disorganization, which is said to inexperience.

Having that stated, if we give attention to the 20% of profitable gamers, we will purchase some actual gems.

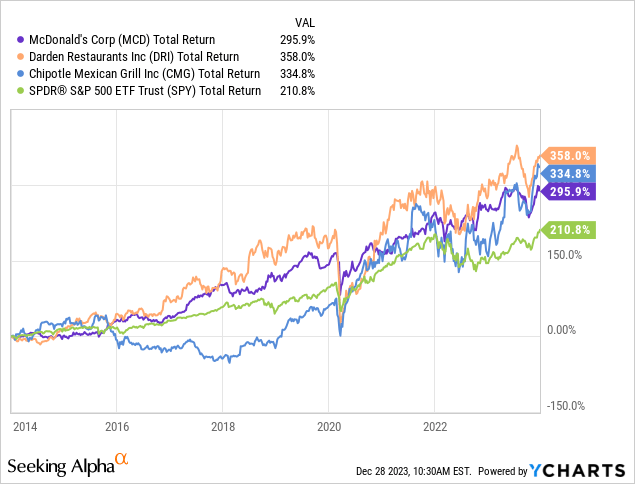

The three greatest that come to thoughts are McDonald’s (MCD), Darden Eating places (DRI), which owns all kinds of manufacturers, and Chipotle, the star of this text.

Each single certainly one of these gamers has outperformed the S&P 500 over the previous ten years.

The explanation I made a decision to cowl Chipotle is as a result of I’ve put a while into understanding its enterprise mannequin. Like McDonald’s, it jogs my memory a little bit of a “utility.”

By that, I imply they’re in all places, and clients know what they’ll anticipate once they set foot in certainly one of their eating places.

That is the proper foundation to construct a profitable world enlargement that would doubtlessly result in elevated future features on high of the 24% annual features traders have loved because the firm’s IPO in 2007.

So, let’s dive into the main points!

What Makes Chipotle So Distinctive?

Based in 1993 in Denver, Colorado, Chipotle began this yr with greater than 3,100 owned and operated eating places in the USA and barely greater than 50 worldwide areas.

On a aspect be aware, this exhibits that Chipotle remains to be a really U.S.-focused enterprise, which, I consider, is sensible, as the recognition of Mexican meals varies per area. McDonald’s and Domino’s (DPZ), to call one other profitable operator, have meals gadgets which might be a lot simpler to scale globally.

Nonetheless, that is not essentially a nasty factor. It is like saying, “Ferrari (RACE) has a model that is hard to scale as the average consumer cannot afford it.“

With that in thoughts, Chipotle’s mission revolves round “Cultivating a Better World,” specializing in 5 key methods:

- Working Profitable Eating places: Emphasizing a people-accountable tradition for Meals With Integrity and delivering distinctive in-restaurant and digital experiences.

- World Class Individuals Management: Growing and retaining numerous expertise in any respect ranges.

- Expertise and Innovation: Amplifying digital progress and productiveness by know-how and innovation.

- Model Visibility and Love: Enhancing total visitor engagement by making the model seen, related, and liked.

- Entry and Comfort: Accelerating new restaurant openings to develop entry and comfort.

Though Chipotle is way from low-cost, it is aware of it may well cost higher costs, as it’s positioning itself as a spot for higher quick meals, to place it bluntly.

Basically, Chipotle emphasizes serving high-quality, responsibly raised meats and responsibly grown produce.

In accordance with the corporate, its dedication to sustainability and animal welfare is clear in its “Responsibly Raised” branding for meats.

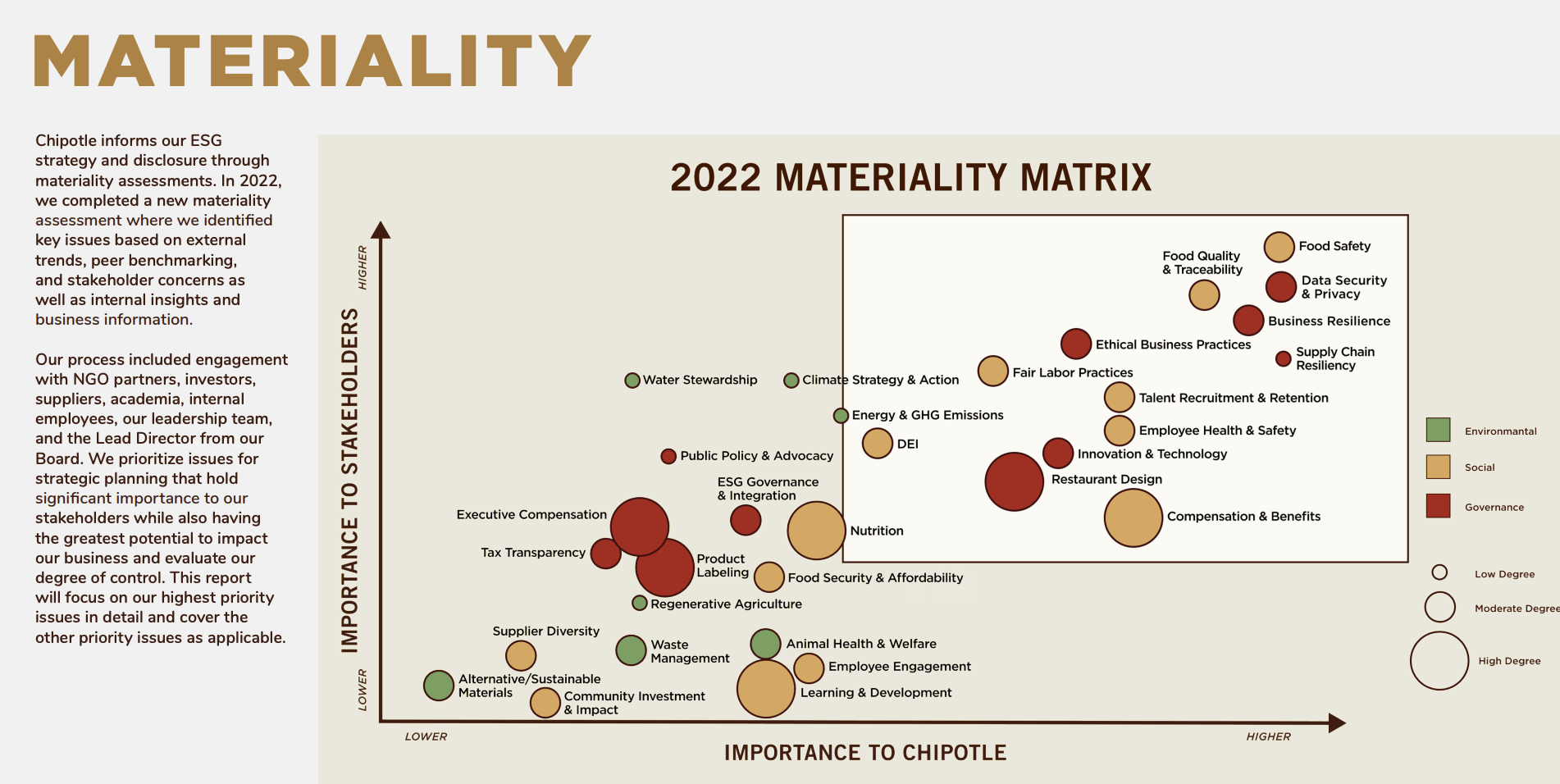

On its web site, it has a really lengthy sustainability report, which incorporates charts just like the one beneath, which clarify how the corporate addresses key sustainability points whereas satisfying as many stakeholders as doable.

Chipotle Mexican Grill

To fulfill the demand of its eating places, the corporate operates 26 regional distribution facilities whereas rigorously choosing suppliers based mostly on high quality, value, and adherence to Meals With Integrity requirements.

With that in thoughts, scaling any enterprise these days entails know-how.

The corporate has enhanced digital capabilities, together with the digitization of restaurant kitchens, expanded partnerships with third-party supply companies, and the introduction of Chipotlanes for buyer pick-up.

What Is Chipotle As much as And What Does It Imply For Shareholders?

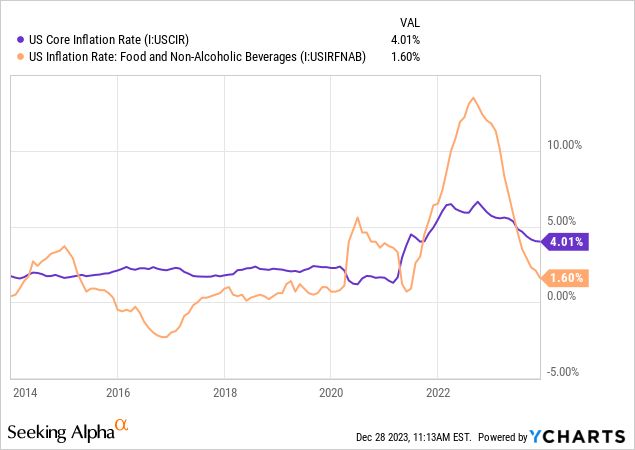

As virtually everybody is aware of (and feels), inflation remains to be a problem. Though inflation charges have come down, core inflation remains to be at 4.0%, twice the Fed’s 2.0% inflation goal.

Moreover, whereas meals inflation is right down to 1.6%, that is on high of double-digit in 2022, which explains why so many individuals are battling costly groceries and meals typically.

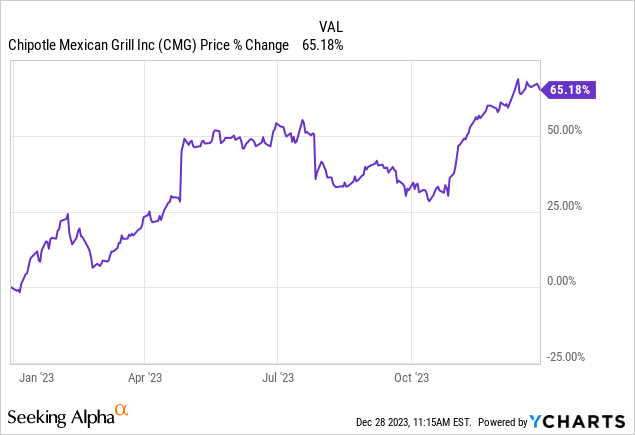

Regardless of common weak point in shopper sentiment, CMG shares are doing properly.

Yr-to-date, CMG shares are up 65%, making it among the finest performers in the marketplace.

The corporate’s outcomes affirm this.

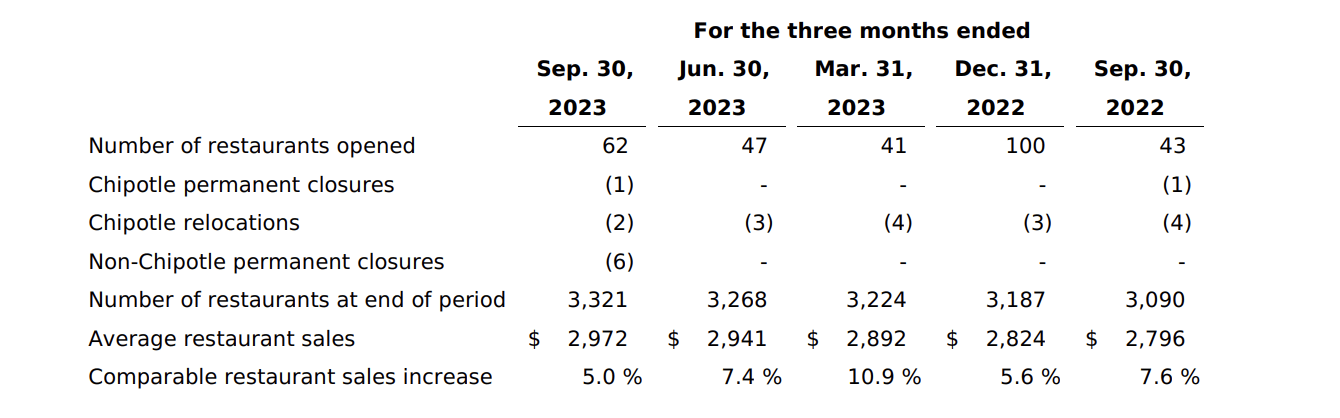

- Gross sales within the third quarter grew over 11% year-over-year to succeed in $2.5 billion.

- Comparable gross sales elevated by 5%, pushed by a 4% progress in transactions.

- The restaurant-level margin was 26.3%, up about 100 foundation factors from final yr.

Earnings per share, adjusted for uncommon gadgets, have been $11.36, representing a 19% year-over-year progress. The third quarter incurred $1 million in uncommon bills associated to company restructuring.

One driver of EPS progress was price management.

The price of gross sales within the quarter was 29.7%, a lower of about ten foundation factors from final yr. Menu value will increase benefited, however inflation in meals prices, notably beef and queso, offset a few of these features. This autumn price of gross sales is anticipated to be round 30%.

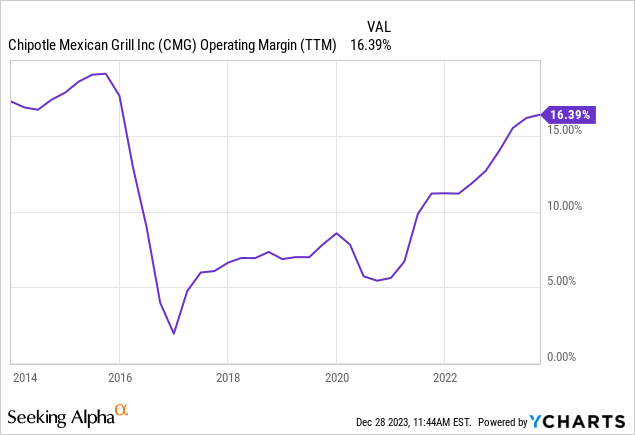

Trying on the chart beneath, we see that the corporate has significantly grown its working margins over the previous few years.

It is usually increasing its footprint.

In Q3, 62 new eating places have been opened, with 54 that includes Chipotlanes.

The corporate stays on observe to open between 255 to 285 new eating places this yr and plans to open between 285 and 315 new eating places in 2024, with no less than 80% having drive-through capabilities.

Whereas allowing and inspection delays are impacting the timeline, the corporate goals to strategy 10% new restaurant openings by 2025.

Chipotle Mexican Grill

Its enlargement plans additionally embrace an even bigger give attention to smaller elements of the U.S., that are underrepresented markets, so to talk.

Wall Avenue Journal

As reported by the Wall Street Journal (be aware the feedback relating to its distribution community, which I briefly talked about as properly):

Chipotle is reaching into some cities removed from any of its present areas, together with locations with roughly 10,000 residents, akin to Newton, N.J., and Covington, La. Attracting a Chipotle can increase cities’ broader growth and brings an amenity that caters notably to youthful residents, native officers stated.

[…] Chipotle depends on recent meals in its eating places, which has typically led to outages of components, the corporate stated. Stretching into new terrain may result in provide challenges and prices, although Chipotle probably has sufficient sway with its distributors to mitigate interruptions, stated Bob Goldin, co-founder of the food-industry consulting agency Pentallect.

Based mostly on this context, Chipotle launched two key initiatives to reinforce throughput.

The primary entails adjusting the cadence of digital orders to higher stability labor deployment.

The second is a renewed give attention to throughput coaching in eating places.

In accordance with the corporate, optimistic suggestions signifies that these initiatives are bettering the variety of entrees served throughout peak durations.

Moreover, with regard to the aforementioned technique to enhance model consciousness and “love,” the corporate’s advertising efforts centered on attaining precisely that.

For instance, the reintroduction of the carne asada limited-time provide obtained an enthusiastic response.

The corporate additionally engaged in sports activities partnerships, leveraging the Actual Meals for Actual Athletes platform. Artistic gaming integrations, such because the Chipotle IQ digital trivia sport, have been utilized to attach with followers.

Moreover, progress was reported on the event of an automatic digital makeline examined on the domesticate heart.

Partnerships with Hyphen and Autocado purpose to extend capability, pace, and accuracy in meals preparation. Whereas nonetheless within the testing section, these improvements may contribute to a extra environment friendly and balanced operation between the entrance and digital makelines.

It additionally has a wholesome stability sheet, which is anticipated to finish up with $700 million in internet money on the finish of this yr. This implies the corporate has more money than gross debt.

On a aspect be aware, and with regard to its partnerships and know-how implementation, CMG founder Steve Ells is understood for combining restaurant niches with superior know-how/companies.

He is presently within the technique of growing his new business referred to as Kernel, which focuses on meat-free sandwiches, salads, and associated.

I’ll maintain a detailed eye on that, as I am curious how he’s going to develop a enterprise in an excellent harder area of interest: vegetarian/vegan.

Valuation

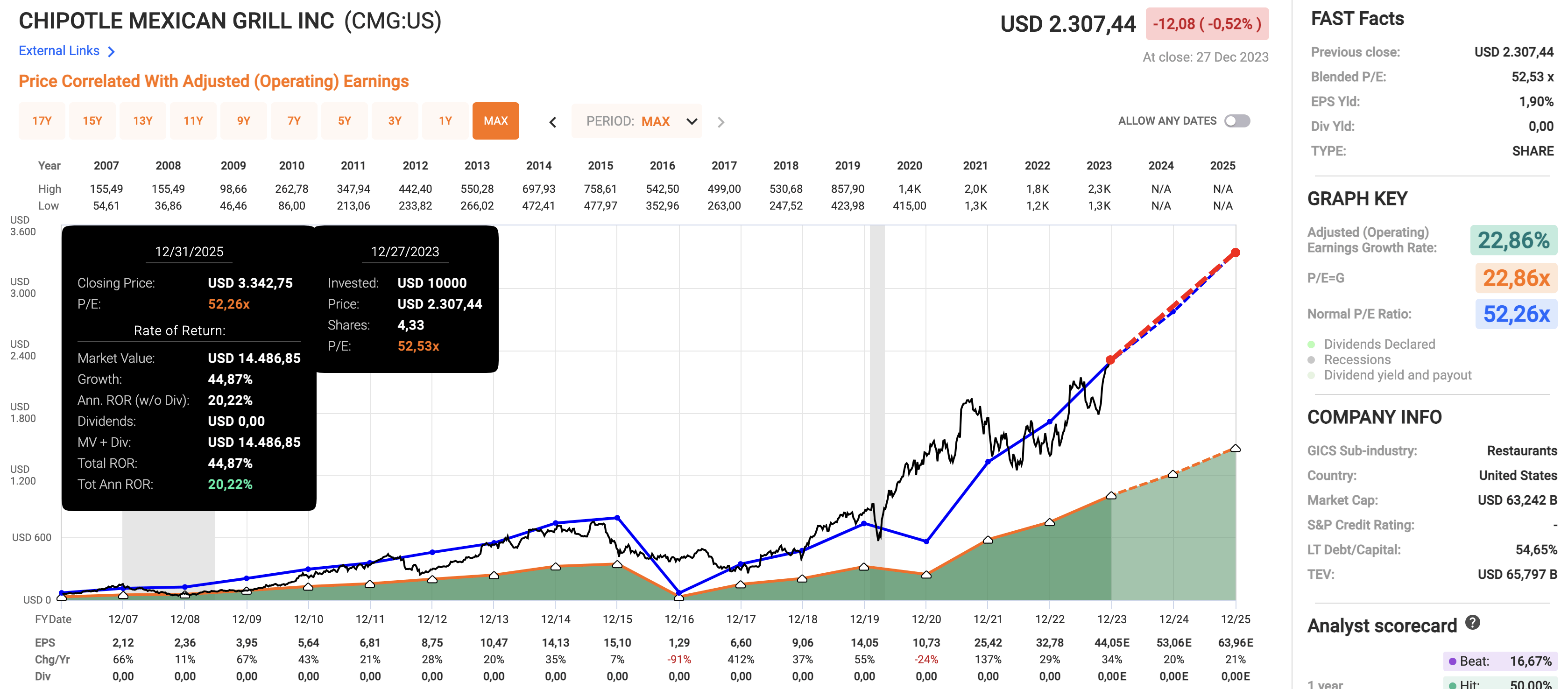

On this article, I discussed that CMG shares have returned 24% per yr because the IPO. Odds are that elevated complete returns proceed.

Utilizing the information within the chart beneath:

- CMG is presently buying and selling at a blended P/E ratio of 52.5x.

- Its long-term normalized P/E ratio is 52.3x.

- This can be an “elevated” P/E ratio. Nonetheless, this yr, the corporate is anticipated to develop EPS by 34%, adopted by 20% potential progress in 2024 and 21% progress in 2025.

- These numbers warrant an elevated P/E ratio and will recommend 20percentish annual returns if the corporate maintains its present valuation.

FAST Graphs

I am clearly not promising that it will occur, as macroeconomic developments may influence each progress expectations and traders’ willingness to use elevated multiples.

Nonetheless, the inventory stays in an amazing spot to proceed producing elevated returns, even when traders begin to slowly modify the valuation a number of to the low-40x vary over time.

Going ahead, I wish to personal CMG. I simply have not found out how a non-dividend payer matches into my technique, particularly in gentle of my give attention to firms that function greater up the provision chain.

Nonetheless, the takeaway right here is that I anticipate CMG’s recipe for fulfillment to do its job for a lot of extra years, doubtlessly resulting in elevated returns for traders.

Takeaway

Regardless of my typical reservations about restaurant shares, CMG stands out with its profitable mannequin akin to a “utility.” The dedication to sustainability, accountable sourcing, and know-how integration positions it as a pacesetter backed by stable outcomes.

The current monetary efficiency is spectacular, with shares up 65% year-to-date, reflecting strong gross sales progress, increasing margins, and strategic enlargement plans.

Regardless of a seemingly elevated P/E ratio, CMG’s anticipated EPS progress suggests continued potential for traders.

Whereas I am but to include a non-dividend payer into my technique, the takeaway is evident—CMG’s recipe for fulfillment may yield elevated returns for years to come back.