Robert Manner

Thesis

Lululemon Athletica Inc., (NASDAQ:LULU) generally referred to as Lululemon, is a Canadian-American multinational athletic attire retailer headquartered in British Columbia and integrated in Delaware, United States. The inventory has carried out exceptionally effectively, gaining greater than 50% in worth in 2023. Whereas it trades at a wealthy valuation of near 60 instances earnings, I consider the inventory continues to be undervalued with optimistic catalysts reminiscent of its pricing energy, progress in market share, and the fast tempo of progress in worldwide markets as its tailwinds.

Catalysts

Consistency and Attainable Growth in Gross Margins

Considered one of Lululemon’s strengths is its pricing energy. That is very effectively mirrored in its gross revenue margins remaining fixed at round 56-58% since 2018. This exhibits that the corporate didn’t must considerably low cost its items to promote them. I see this as an indication of robust model worth and client loyalty. The corporate has at all times targeted on high-quality products and its customer insights. Through the years, it has achieved to construct a cult-like following. The corporate additionally invests closely in analysis and growth, in addition to in advertising and marketing, to construct a robust model picture.

Lululemon has fostered robust model loyalty via distinctive advertising and marketing and community-focused methods. Clients are engaged via platforms just like the “Lululemon Addict” weblog and experiences like free yoga courses and working golf equipment. These initiatives create a way of neighborhood and connection to the model. Moreover, the corporate enhances buyer loyalty by providing free transport for on-line orders and personalised experiences like free alterations in shops, additional personalizing the buying expertise and fostering a loyal buyer base.

All the above contribute to the next value level for its merchandise. Lululemon’s enterprise mannequin has allowed the corporate to carve a distinct segment for itself in a crowded market. Even when uncooked materials costs elevated in the course of the post-COVID inflationary interval, the corporate’s gross revenue margins remained unaffected. Unlike Nike and other competitors, Lululemon’s merchandise are nearly completely offered in its retailer or web site. Lululemon doesn’t depend on retailers for gross sales, due to this fact, permitting it to cost its merchandise on favorable phrases and enhance margins

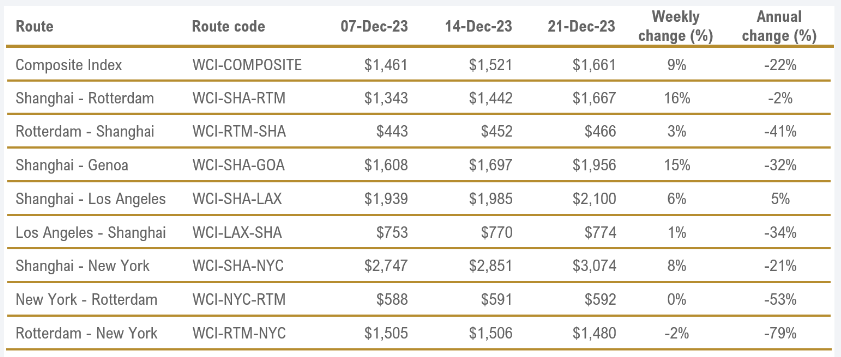

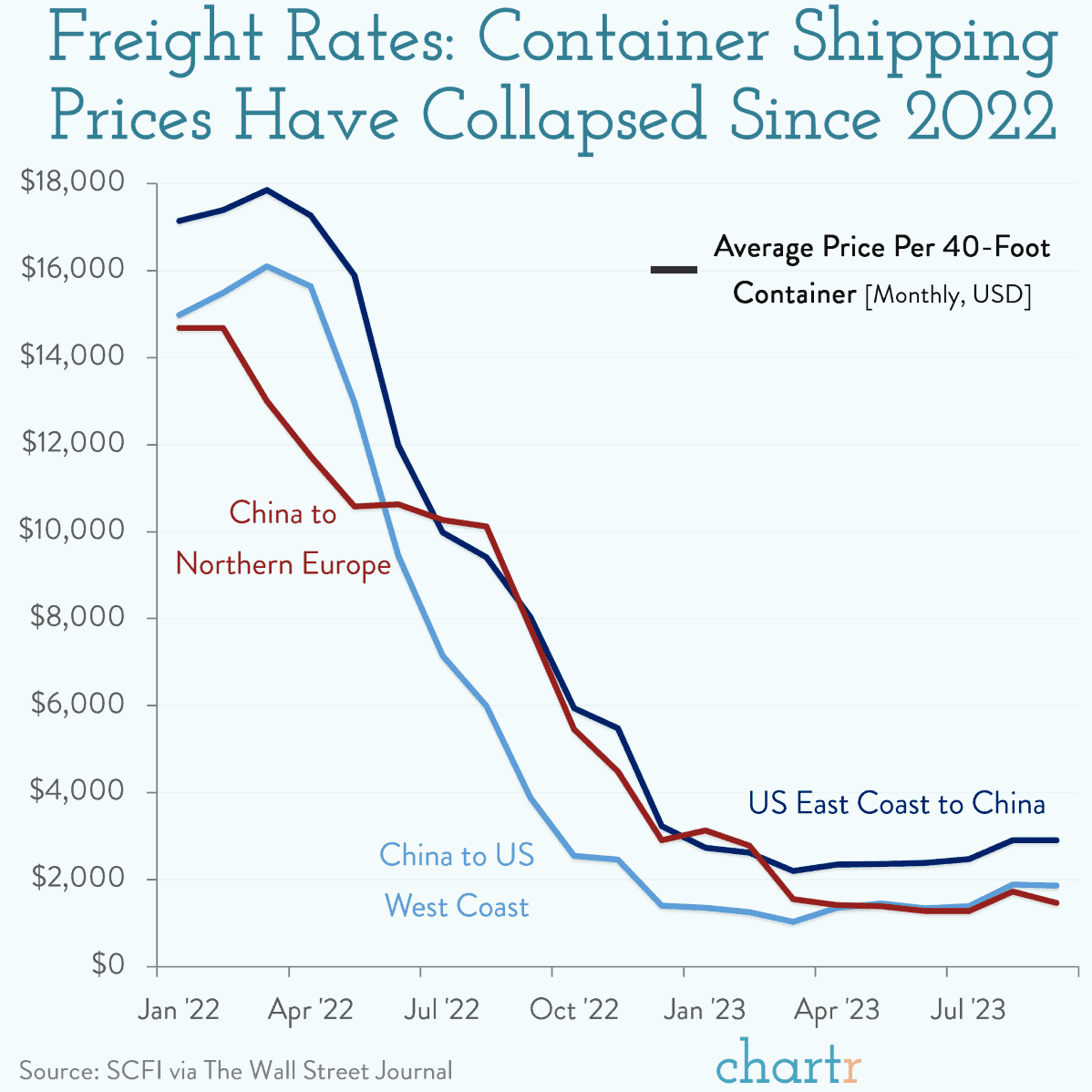

Going ahead, I anticipate that Lululemon’s Gross Margins will proceed to develop with the worst of enter inflation behind and freight prices dropping sharply since early 2022. As per PYMNTS, container transport charges have dropped almost 90% since late 2021/ early 2022. Whereas ship operators face challenges, the decline in transport charges advantages transport shoppers, significantly giant retailers, per the report. The beneath picture from Drewry Provide Chain Advisors exhibits the 12 months-over-12 months change in Transport Container Charges for various places.

Drewry Provide Chain Advisors Chartr/SCFI by way of Wall Avenue Journal

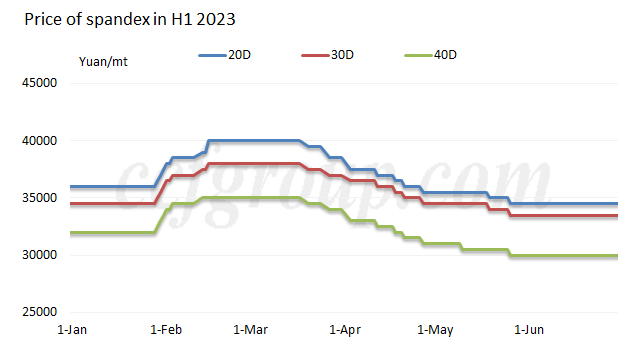

The corporate can also be set to learn from a decline in textile costs. World cotton provide is outpacing demand and this has led to a discount in costs. Even on the Commodities exchanges, Cotton Futures have declined 10% for the reason that finish of August 2023. As for Lycra or Spandex which is mostly utilized in athletic attire, costs for Spandex have collapsed in China due to what’s being referred to as a market stoop. The beneath graph exhibits the drop in costs of Spandex materials in H1 in 2023, priced in Yuan per metric tonne.

CCF Group

The corporate has guided gross margins to develop 90 to 120 foundation factors in This fall 2023 relative to This fall 2022. I anticipate margin enlargement to be larger within the following quarters as This fall sometimes includes plenty of markdowns owing to the vacation season reductions.

Gaining Market Share + Massive Scope for Development

Lululemon has been capable of develop its revenues sooner than its key opponents and the general trade common which has meant that the corporate has grown in market share. The global sportswear market is valued at $380 billion at this time. It’s forecast to be value $455 billion in 2027. This interprets to an annualized achieve of simply 3.7% for the general trade. Lululemon, alternatively, has boosted its prime line at a compound annual price of 21.7% between fiscal 2016 and financial 2021.

As per the management’s target for FY2026 (ending in January 2026), the corporate ought to earn $12.5 billion in income. This can take the corporate’s world market share from round 2% to shut to 2.8%. Investing in companies which can be a part of increasing industries is one factor. Discovering firms which can be rising their gross sales at a sooner price than the trade is much more advantageous. That is the primary objective of accelerating market share. Said in a different way, it is claiming a bigger share of the pie. That is precisely what Lululemon will likely be doing via its enlargement in World markets, increasing brick and mortar footprint, the fast progress price in China, and enlargement into health equipment.

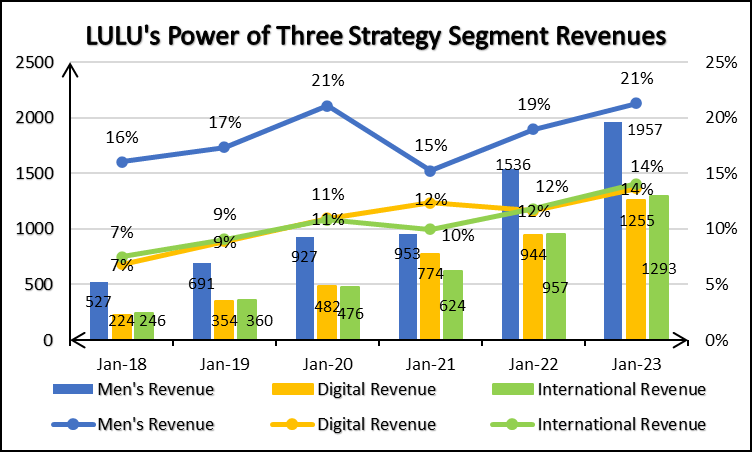

A big driver of progress up to now has been Lululemon’s ‘Power of Three Growth Strategy’. In April 2019, newly appointed CEO Calvin McDonald (ex-CEO for LVMH’s America division) introduced the ‘Power of Three’ Development Technique to double the corporate’s digital income, double its males’s income, and quadruple its worldwide income from fiscal 2018 throughout the following 5 years. Lululemon achieved its digital and males’s targets forward of schedule in fiscal 2021. This April, Lululemon launched a brand new five-year progress plan referred to as “Power of Three x2.” The objectives are the identical: it plans to double its digital income, double its males’s income, and quadruple its worldwide income from fiscal 2021 throughout the following 5 years. In Q3 2023, Males’s income grew 15% YoY, Digital Income grew 19% and Worldwide Income grew 49% YoY.

The precise technique to develop gross sales is not recognized. These had been targets that they had set for the talked about segments. The technique could possibly be the prioritization and enlargement into these markets within the first place the place Lululemon was not very energetic. The beneath graph exhibits the evolution of the revenues of the three goal segments as per Lululemon’s Energy of Three Technique in absolute phrases and expressed as a proportion of the corporate’s whole income.

LULU Quarterly Earnings Assertion

Because it did with the primary part of the Energy of Three Development Technique, I anticipate the corporate to realize its targets forward of schedule owing to its fast worldwide progress. We should additionally not neglect that 2 of three targets have already been achieved within the second part of the Energy

This can replicate how I worth the corporate.

Worldwide Development Speedy + Fav. Foreign exchange tailwinds

McDonald stated its worldwide enlargement — one of many “key pillars” of its new Energy of Three plan — was already off to a “great start.” Its worldwide grew almost 50% YoY in Q3 2023, sooner than anticipated, led by China and elements of Europe.

Lululemon’s forward-looking statements are extremely optimistic. A planned expansion of market penetration, particularly within the Asia-Pacific and Europe, Center East, and Africa areas, the place model consciousness continues to be within the single digits, helps the optimism. Moreover, the enterprise is devoted to its Energy of Three x2 progress technique, which is anticipated to drive progress in each class. The corporate continues to speculate behind its strategic initiatives to construct model consciousness amongst extra investments it has accelerated to gas our Energy of Three x2 highway map. The corporate can also be banking on its capability to extend its brand awareness in world markets, which presently stays in single digits or low double digits.

The greenback has weakened almost 4% for the reason that finish of October and this makes US items cheaper overseas which suggests the corporate advantages from elevated gross sales (in fixed phrases) in addition to the purely foreign exchange a part of revenues. I anticipate these tailwinds to proceed and sure strengthen because the US Federal Reserve’s dot plot predicts rate cuts whereas different central banks stay hawkish. This can lead to a weaker greenback and profit firms reminiscent of Lululemon which earn income from outdoors the US.

Valuation

After trying on the optimistic catalysts that Lululemon stands to learn from, let’s take a look at the valuation of the corporate.

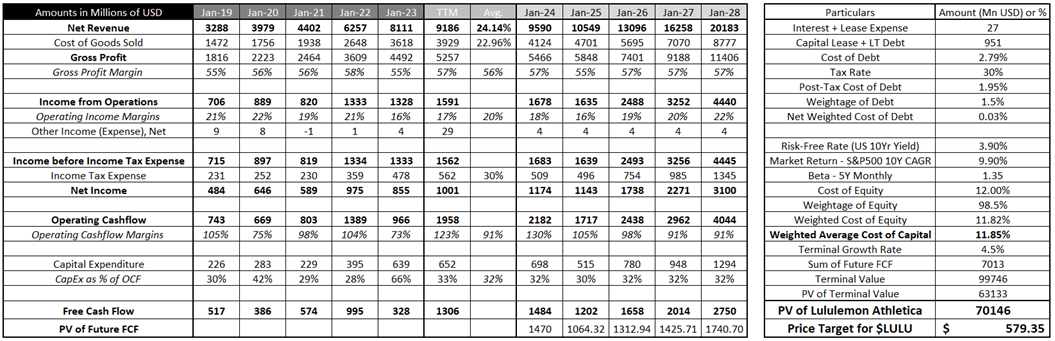

Income Development: Whereas the market is pricing in 14-15% income progress as per analysts’ consensus which is in keeping with the administration’s steering, I consider that once we take note of the pricing energy, the speed of worldwide progress and the rise in market share, income can proceed to develop on the common price noticed since 2019. It received’t be the primary time that precise income progress might exceed the administration’s targets in addition to analysts’ consensus estimates, as we’ve seen as soon as with the primary version of the Energy of Three Development Technique. I anticipate income progress to be 10% within the subsequent fiscal yr owing to rising macroeconomic challenges. Nonetheless, past that, I anticipate the corporate to proceed rising income at ~24%. Gross Margins have been assumed to stay regular between 55%-57%.

My Monetary Projections

Consistent with gradual progress subsequent yr, I’ve assumed margin contraction for the upcoming fiscal yr however enlargement again to the long-term common. For the Fiscal 12 months ending January 2028, the margin enlargement might come as and when the corporate’s strategic investments within the manufacturing course of repay and the corporate expands globally and limits payroll bills by studying via working (doing) shops overseas. The profit might additionally come from developments in expertise that cut back the worker necessities in a retailer.

Working Money Circulation Margins imply the conversion ratio of Working Earnings to Working Money Circulation. It’s as excessive this yr due to the impairment to goodwill and different property. It was taken from present ranges and assumed to slowly lower in direction of the long-term common, to estimate Working CashFlow. CapEx was estimated utilizing a median % of Working CashFlow spent on Capital Expenditure during the last 5 years (excluding the fiscal yr that led to January 2023 as a result of it seems to be an outlier). Free Money Circulation was then discounted on the Weighted Common Value of Capital calculated utilizing the Capital Asset Pricing Mannequin.

As per these calculations, the estimated current worth of Lululemon Athletica Inc. is $70.15 billion or the equal of $579.35 per share of $LULU.

Dangers

Overestimating progress

Probably the most elementary assumptions I’ve taken, that separates me from Wall Avenue analysts’ consensus estimates is the expansion price in income. I’ve assumed 10% for subsequent yr, and 24% for the years after that, in comparison with analyst consensus estimates of 13-14% progress. If I had been to alter the expansion price to twenty%, 15%, and 12% then we’d get fair-value estimates of $554, $525, and $508 respectively.

If Lululemon’s Energy of Three x2 progress technique will not be profitable in assembly the administration’s targets, then that may have a big influence on the honest worth estimates of the corporate’s inventory. This could possibly be elements reminiscent of points with the provision chain, or worth chain as was throughout COVID of which a brand new pressure appears to be surfacing. There might also be one other competitor that comes up providing an analogous high quality of products for extra enticing costs, which can outcome within the firm dropping some market share.

Nonetheless, holding in thoughts the present price of progress which has been talked about within the catalyst part, I don’t think about this risk to be a big risk to my valuation mannequin.

Declining Margins – Working stage

As will be seen from the valuations sections, I anticipate Lululemon Athletica’s working margins to extend and revert to the long-term common. The underlying assumption was that the corporate would in the end notice that its Gross sales, Normal and Administrative bills have been rising as a share of its income and the corporate’s hand could be pressured to scale back these bills, or that technological developments would allow the corporate to scale back worker headcount and restrict its working bills. Whereas common investments that the corporate is making relate to opening new shops and growing model consciousness to discover progress alternatives, those that the corporate is making that may allow enchancment in margins pertain largely to upgrades within the Direct-to-Shopper community, IT Infrastructure and expertise concerned within the Supply Chain Network.

If working earnings are decrease, then as per my mannequin, working money flows will even be decrease which can then lead to decrease free money flows. This may occasionally additionally power me to scale back terminal progress charges. In consequence, the honest worth estimates for the corporate will even have to be revised decrease considerably.

Moreover, some revenue margins have been briefly chipped off resulting from goodwill impairment. Bills regarding impairment of goodwill lower with time which can lead to re-inflation of working revenue margins.

Conclusion

To conclude this report, I want to place an Chubby advice on Lululemon’s inventory as my honest worth estimate of $579 presents a 13.5% upside to its closing value of $510 as of twenty second December. This displays the catalysts – pricing energy, progress in market share in addition to worldwide enlargement.