wildpixel/iStock by way of Getty Photographs

Be aware: All currencies are denominated in USD until in any other case acknowledged.

For these readers who should not that conversant in Constellation Software program (OTCPK:CNSWF, TSX:CSU:CA), which I’ll abbreviate as CSI, I would counsel reviewing my previous article the place I deeply lined the corporate’s background, its enterprise mannequin, anticipated progress, and administration.

On this article, my focus will probably be on the third quarter’s outcomes, the latest acquisitions, and the issuance of debentures.

Funding Thesis In A Nutshell

CSI has been constructing a extremely defensive and well-diversified enterprise mannequin for over 20 years within the vertical market software program (VMS) business by buying over 800 completely different enterprise models.

The corporate continues to be led by its founder Mark Leonard together with an impressive and well-experienced administration workforce, which has set the precise incentives for its workers and adopted finest practices to pursue new acquisitions on the proper hurdle charges.

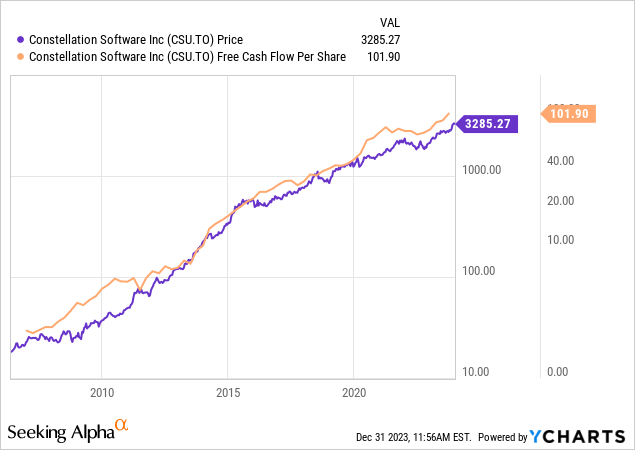

Some of the frequent issues buyers face when analyzing CSI is the corporate struggling to deploy all of its free money circulation into new acquisitions as its dimension expands, however as I am going to present on this article, this isn’t one thing we must always fear about but, and I anticipate progress charges above 20% within the coming years.

Q3 Outcomes Overview

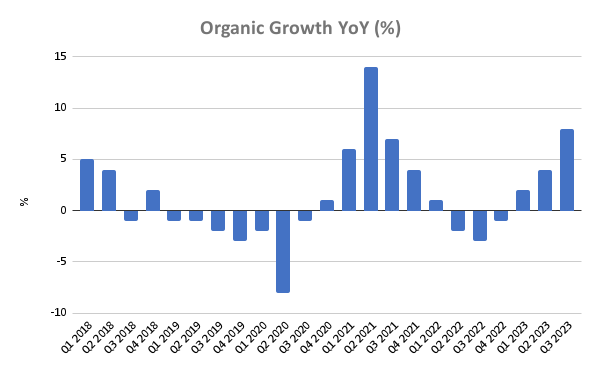

Last quarter’s results introduced us an impressive 8% income natural progress (6% foreign money adjusted), effectively above its historic common (1.4% since 2007), and one of many highest natural progress charges lately:

Writer (Information from Constellation Software program’s Monetary Statements)

You will need to observe that the irregular natural progress in Q2 2021 (14%, 8% foreign money adjusted) was considerably impacted by the U.S. greenback appreciation towards the opposite currencies during which the corporate operates.

Remarkably, the upper natural progress has been achieved with out rising the R&D bills over the past quarters, which has stayed round 14%, according to the historic common. One of many explanations for the upper natural progress may very well be the higher-than-average inflation charges we had throughout final 12 months. Since a lot of CSI’s contracts incorporate clauses to regulate costs primarily based on inflation, the corporate has been capable of cross a rise in costs to its clients.

I consider this development might persist throughout subsequent quarters because of the mission-critical nature of CSI’s merchandise, restricted churn charges, and the strategic method to extend costs regularly. Lots of CSI’s relationships with its shoppers have been constructed over a few years, many years in some circumstances, and it could be simpler to extend costs by 4-5% throughout three years than translating a one-time 10% worth improve.

Generally, you will have these very massive clients which have contracts that restrict the quantity of will increase. And in addition, it is the managers. Generally the managers are on the shopper facet and so they do not wish to give them a rise that equals or exceeds inflation, particularly since we have gone by means of the final decade or extra at type of 2%, 2.5% inflation and to go and swiftly give your buyer a ten% improve or 8% improve.

Source: Dexter Salna (Member of the Board of Administrators at CSI and Perseus). Analyst Name Might 2023.

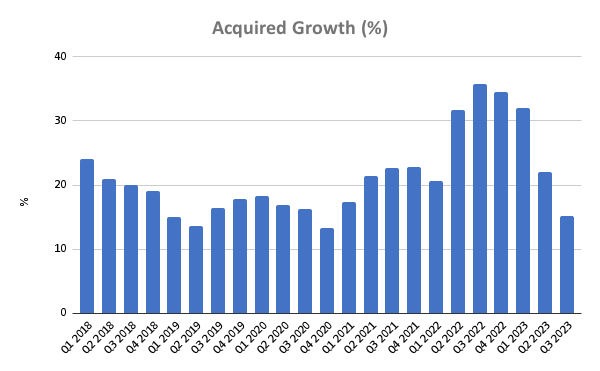

On the acquisitions facet of the enterprise, which I am going to cowl intimately within the subsequent part, there are some necessary changes to be made.

Writer (Information from Constellation Software program’s Monetary Statements)

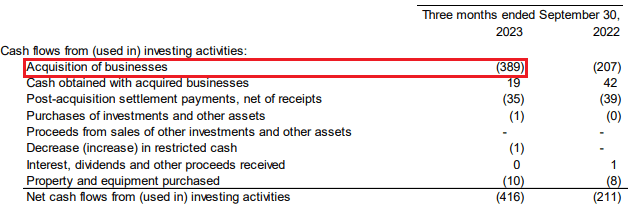

The most important acquisition realized throughout final quarter was the Optimum Blue enterprise and the Empower mortgage origination system (LOS) from Black Knight, Inc. (BKI) for a complete consideration of $742M.

Of the total consideration, $40M has been paid in money for the Empower LOS, and $201M for the Optimum Blue enterprise (plus a $1M money holdback). The remaining $500M has been paid by means of a promissory observe issued to Black Knight, which isn’t mirrored within the money circulation assertion as money utilized in investing actions.

When trying on the quantities spent on acquisitions, we must always embody the $500M to get a greater image of the acquisition tempo through the quarter.

Supply: Constellation Software program Q3 2023 Monetary Statements

When including the observe issued to Black Knight, this Q3 has been the second-biggest quarter in CSI’s historical past concerning capital deployed into acquisitions following Q2 2022 with the Allscripts acquisition. Mixed, the income progress through the quarter was at 23%, reaching over $2.1B.

Concerning bills, employees prices elevated by 20%, barely behind the income improve, leading to an enchancment in working margins from 13.8% a 12 months in the past to the present 15.5%. Non-cash bills such because the redeemable most well-liked securities of Lumine Group (LMN:CA) (OTCPK:LMGIF) and the Topicus (TOI:CA) (OTCPK:TOITF) legal responsibility continued rising through the quarter, which is constructive given CSI’s pursuits in each firms.

The $1M impairment is nothing to be involved about since it’s associated to the Optimum Blue acquisitions, the place CSI recorded an allowance for money flows not anticipated to be collected.

On the much less constructive facet, finance prices elevated through the quarter, from $29M the identical interval final 12 months to the present $50M. The rise is expounded to a better quantity of debt below its credit score facility and better rates of interest through the interval. Given its debentures are linked to inflation, the corporate is paying greater than ever pursuits, which is able to cut back subsequent 12 months as inflation decreases.

Constellation Software program Q3 2023 Monetary Statements

On the underside line of final quarter’s financials, money from operations and free money circulation out there to shareholders elevated by 60% to $513M and $367, respectively.

Issuance of Debentures

In October, CSI issued an extra tranche of its unsecured subordinated floating charge debentures Sequence 1 maturing in 2040, a product the corporate has used prior to now.

The proceeds have been allotted to pay down indebtedness below its current credit score facility, which totaled $686M on the finish of the quarter, nearing the $840M restrict.

Earlier than explaining the traits of the product, I would like to supply a little bit of background. The preliminary issuance of the debentures was in 2014 at a worth of C$95 per C$100, offering buyers with a 5% low cost to face worth and receiving total proceeds of $81.2M, which have been used to pay down debt associated to the TSS acquisition.

In 2015, CSI issued one other tranche, this time with a premium at C$115.00 per C$100 principal, accumulating $159.7M. The principal quantity excellent below the unsecured subordinated Sequence 1 stood at $208M earlier than the most recent issuance.

With the most recent tranche, CSI collected $209M issuing at C$133.00 per C$100.00 principal quantity, rising considerably the premium paid at subscription.

Phrases and Pursuits

CSI issued one subscription proper per share, entitling to a subscription of C$100 principal quantity for each 3.03 rights. To make it easy, shareholders have been entitled to subscribe C$100 for each three shares owned.

Because the debentures are redeemable on the possibility of CSI, the corporate distributed to its shareholders a warrant that neutralizes the redemption rights, which was mandatory to ensure that some debt was subscribed. In any other case, it could be dangerous for an investor to subscribe debt at a 33% premium to par worth, understanding it won’t have time to obtain sufficient curiosity to cowl the premium.

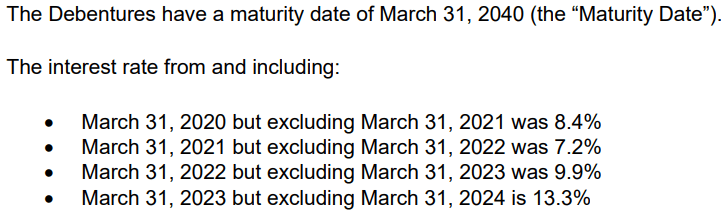

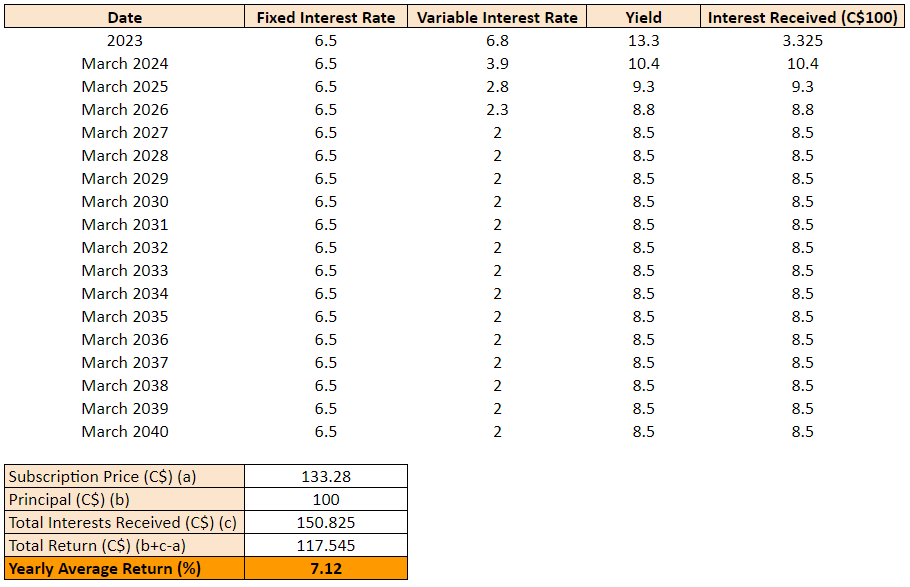

The debt carries a variable rate of interest calculated as a set 6.5% curiosity plus the annual common proportion change within the CPI Index. From issuance to March 2024 it carries a 13.3% rate of interest, after which it’s reset each March till maturity in 2040.

Though it might appear like an abnormally excessive rate of interest, there are a number of factors to take note of. The primary is the excessive premium to par worth, and the second, is the character of the debt, which is unsecured, which means that if the corporate was going bankrupt, it could come after the Credit score Facility.

The debt is buying and selling within the TSX below the image CSU.DB, and as proven within the chart under, it has been buying and selling above par for the reason that first issuance.

TMX Cash. Information from QuoteMedia

Pursuits are payable quarterly and if the change in CPI is unfavourable, will probably be deducted from the mounted 6.5%, however the rate of interest relevant won’t ever be lower than 0%.

Throughout 2023, till November, the average change in CPI has been at 3.9%, so for the following 12 months I anticipate the rate of interest to be reset to 10.4%. The anticipated return is introduced within the desk under, though it’s assuming the subscription through the providing, and it could be greater if the debentures are purchased now out there because of the present worth of C$129.

Writer

Because of the excessive premium to par worth, the yearly common charge of return assuming a 2% inflation (per the common since 1998), could be 7.12%.

Fitch has assigned a BBB score to the debt, the 4th highest of Fitch’s 11 score classes, which I discover fairly conservative considering CSI’s defensive enterprise mannequin, recurring revenues, and monetary ratios.

Buying At A Good Tempo

Over the last quarter, CSI was capable of deploy a major quantity of capital because of the opportunistic acquisitions from Black Knight, but when we exclude this massive acquisition the variety of smaller firms acquired has barely decreased in comparison with the primary half of the 12 months or 2022.

Based mostly on the press releases and information printed by CSI’s working teams, I estimate the full quantity of acquisitions has been round 25 throughout Q3. When excluding the biggest acquisitions, CSI has deployed $164M into the acquisition of smaller software program firms with a median worth of ~$8M, being Harris and Jonas essentially the most energetic working teams with 7 and 6 acquisitions introduced through the quarter respectively.

Though the variety of smaller firms acquired has barely decreased in comparison with the primary half, CSI’s third quarters have on common the bottom spending on acquisitions. Over the last 5 years, the third quarter spending on acquisitions is on common 35% decrease in comparison with the second quarter, which tends to be essentially the most energetic.

Black Knight’s divestitures

CSI was capable of pursue an opportunistic acquisition over the past quarter, which I consider is the results of a few years of constructing sturdy enterprise relationships and changing into a trusted firm within the business.

Following the announcement of the acquisition of Black Knight by Intercontinental Change (ICE), the Federal Commerce Fee (FTC) sued to dam the transaction claiming it could give ICE a major place out there for mortgage origination software program.

To maneuver ahead with the acquisition, the FCT and Black Knight agreed to divest a few of its belongings, which led to CSI buying a high-quality enterprise at an ideal worth.

Optimal Blue’s software permits market members to cost, lock, hedge, and commerce mortgages, and is the business chief utilized by 1000’s of originators to lock roughly 40% of mortgages within the U.S. The enterprise was initially acquired by Black Knight for nearly $3B (60% in 2020, and the remaining 40% in 2022).

Empower is a cloud-based mortgage origination system that automates repetitive processing duties primarily based on the lender’s configurations, displays for any information adjustments through the mortgage course of and triggers a separate work merchandise when an exception happens, which alerts the person that further critiques are wanted.

CSI has been capable of purchase each firms for simply $742M, paying 2x 2023 sales and lower than 6x EBITDA. The market was valuing the 2 firms at $3.3B as a part of Black Knight, and the divestiture reduced the worth paid by ICE by $1.4B.

I anticipate these acquisitions to generate revenues of $370M through the subsequent 12 months and working money flows of ~$125M with considerably greater margins than the common CSI enterprise.

Anticipated Progress

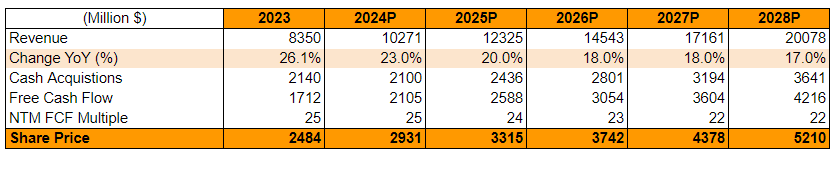

Whereas Q3 has been comparatively quiet concerning smaller acquisitions, to this point the corporate has been capable of deploy nearly $1.8B in acquisitions with one quarter remaining, the place I anticipate one other $340M to be spent in acquisitions, reaching $2.14B for the total 12 months (in comparison with $1.6B in 2022).

In This autumn, there was an analogous quantity of smaller acquisitions alongside the medium-sized acquisition of Medhost, Inc. by the Harris working group. Although the worth paid has not been disclosed, primarily based on revenues I anticipate the full cost to be round $180M.

Topicus accelerated its acquisition tempo in Europe throughout This autumn in comparison with final quarter, since there have been already six acquisitions announced in verticals such because the digital element distribution market, debt restoration, parking administration options, healthcare, native authorities, and safety.

For the second half of the 12 months, I felt quick in my earlier article, the place I anticipated complete revenues for the 12 months of $8.1B, whereas they are going to in all probability be above $8.3B.

Looking forward to 2024, I foresee a considerable improve throughout Q1 with the acquisitions of the Curbside Administration and Public Security Companies for ~$260M (8x TTM EBITDA) from Conduent Inc. (CNDT), and Nokia’s Machine and Service Administration Platform for €185M (plus a contingent consideration of as much as €35M).

As for now, there have already been bulletins for $464M deployed into acquisitions throughout Q1, main me to anticipate an acquisition spending above $2B for the total 12 months. This projection includes a 20% acquired progress plus a 3% natural progress, above historic common charges primarily based on the present momentum.

Writer

Closing Remarks

All through the current quarter, CSI has been capable of maintain an ideal tempo buying VMS firms at a great worth. Though the second half of the 12 months tends to be much less energetic concerning acquisitions, the corporate deployed a great quantity of its working money flows (with out reducing its hurdle charge) because of the opportunistic acquisitions of Optimum Blue and Empower, capitalizing on the FTC’s intervention within the ICE/Black Knight transaction.

Whereas finance prices have seen a rise, a decline in rates of interest and inflation would possibly ease the curiosity funds for the following quarters. So long as CSI continues to seek out nice companies with a dominant place of their specific area of interest at an affordable valuation, this method stays essentially the most optimum capital allocation.

CSI has just lately introduced the retirement of Dexter Salna, who has been with the corporate since 1995 and was a key contributor to the event of the Perseus working group. He’ll stay on the board of administrators and for the reason that enterprise tradition is effectively unfold throughout the group, I’m positive the precise particular person will probably be discovered to proceed main CSI’s excellent progress.

Lastly, on the natural income facet of the enterprise, CSI can be rising effectively above its historic common, and I anticipate this development to proceed for some quarters forward. Given the current developments and opportunistic acquisitions, I anticipate the corporate to proceed rising its revenues above 20% through the subsequent two years and ship common returns of ~16% CAGR over the following 5 years.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.