RgStudio

Ares Capital (NASDAQ:ARCC) is without doubt one of the market’s main enterprise improvement firms or BDC. It final traded at a market cap of $11.4B. With a ahead core earnings a number of of 8.5x, it is also forward of its friends’ median of seven.8x, suggesting a relative premium. I urged traders to keep away from the recession fears in my previous update, as ARCC bottomed out in late October.

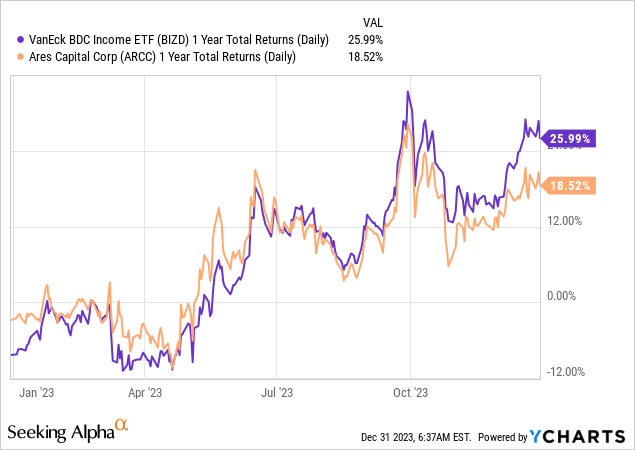

Regardless of its market-leading scale, ARCC’s whole return efficiency has disenchanted over the previous yr, underperforming its friends represented within the VanEck BDC Earnings ETF (BIZD). Regardless of this, it is nonetheless a decent efficiency, as ARCC delivered a complete return of practically 19%.

With the Fed anticipated to have reached the height of its charge hike regime, issues are mounting in regards to the firm’s portfolio efficiency shifting forward. Buyers ought to word that Ares Capital’s portfolio is based totally on floating charges. Primarily based on the corporate’s third-quarter or FQ3 earnings update in late October, 97% of its new investments are attributed to floating charges. Consequently, it is doable that Ares Capital’s core earnings development might come underneath stress in 2024 because it laps the robust comps in opposition to FY23’s outstanding earnings development.

Analysts’ estimates recommend that Ares Capital might ship core earnings development of 15.6% in 2023. Nevertheless, Wall Avenue would not count on the momentum to be carried ahead in 2024. Consequently, Ares Capital’s earnings development might have peaked in 2023, as analysts penciled in a 0.1% decline in 2024.

Regardless of the expansion normalization, the drop-off is not anticipated to be dramatic, suggesting a resilient 2024, even because the Fed might execute three charge cuts this yr. Subsequently, a higher-for-longer Fed continues to be anticipated, which is smart because the financial system has remained resilient. Moreover, administration argued that it had adjusted its hedges to react to probably decrease rates of interest shifting forward.

Accordingly, Ares Capital was famous to have swapped its maturing fixed-rate debt right into a “floating-rate debt instrument” at its Q3 earnings convention. The corporate careworn that the transfer was meant to align extra intently to its “predominantly floating rate asset portfolio, indicating a strategic matching of assets and liabilities.” As well as, administration underscored its expectation that “interest rates might remain higher but eventually trend downwards.” In different phrases, Ares Capital stays poised for a higher-for-longer posture however is able to swing towards a lower-rate atmosphere.

I consider credit score should be attributed to administration’s foresight and execution on this side. It is evident now that the market has positioned for a decrease charge atmosphere, supported by the Fed’s communication of three charge cuts. Nevertheless, primarily based on Ares Capital’s earnings convention in late October 2023, the 10Y (US10Y) surged above the 5% mark. Consequently, it wasn’t that clear then. Subsequently, administration’s potential to anticipate appropriately ought to present extra credibility to its execution because it makes an attempt to take care of its core earnings resiliency in expectation of a higher-for-longer atmosphere.

Primarily based on ARCC’s efficiency because it bottomed out in October 2022, I consider the market has already considerably discounted laborious touchdown dangers. Given the publicity to center market firms that might be affected worse by a recessionary impression, the market appears satisfied that such dangers aren’t anticipated to be the bottom case.

Moreover, Ares Capital is just not anticipated to face imminent dangers in its strong ahead dividend yield of 9.7% on the present ranges. In different phrases, until traders count on the Fed to chop charges considerably, hurting its core earnings projections, earnings traders are anticipated to proceed shopping for vital dips on the BDC chief.

Primarily based on the present projections, Ares Capital is anticipated to see a extra substantial decline in its core EPS in 2025 by greater than 6%. With ARCC nonetheless valued at a premium in opposition to its BDC friends, I view the danger/reward on the present ranges as fairly balanced, given the anticipated peak in its earnings development charges in 2023.

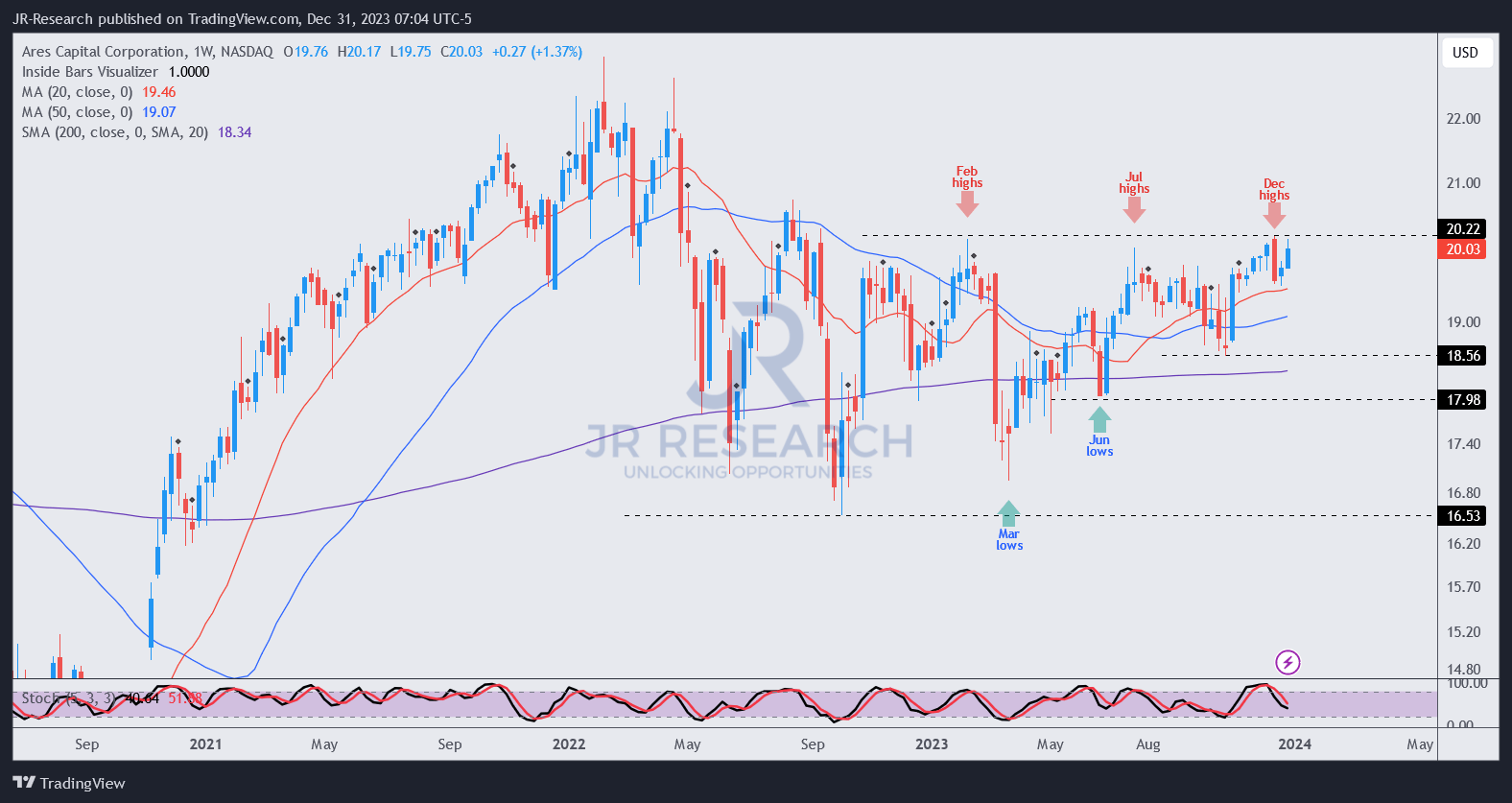

ARCC worth chart (weekly) (TradingView)

As well as, from a complete return perspective, ARCC would possibly proceed to underperform. I assessed it is going through resistance on the present ranges. It is necessary to contemplate that ARCC has regained its medium-term uptrend. With ARCC nonetheless buying and selling at a discernible low cost in opposition to its 10Y common of 10x, I do not see substantial draw back dangers on the present ranges.

Furthermore, the upper lows and better excessive worth buildings recommend it might assist ARCC proceed grinding larger because it seems to interrupt decisively out of the $20 degree. Nevertheless, I would like to observe the response to ARCC’s resistance degree earlier than assessing one other extra enticing shopping for alternative.

Given ARCC’s relative premium and fewer constructive worth motion, I consider the chance for ARCC to outperform on the present ranges might face extra vital challenges. Nevertheless, a steeper pullback might present a extra enticing entry level for earnings traders seeking to purchase into its enticing dividend yields.

Ranking: Downgraded to Maintain.

Essential word: Buyers are reminded to do their due diligence and never depend on the knowledge offered as monetary recommendation. Please all the time apply impartial pondering and word that the ranking is just not meant to time a particular entry/exit on the level of writing until in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a important hole in our view? Noticed one thing necessary that we didn’t? Agree or disagree? Remark under with the purpose of serving to everybody in the neighborhood to study higher!