carterdayne

Intro

We wrote about West Fraser Timber Co. Ltd. (NYSE:WFG) in July of this yr once we said that momentum would proceed within the lumber firm after its second-quarter earnings outcomes. Though the corporate’s Q2 earnings miss prompted a short lived topping out within the inventory value, West Fraser’s convincing Q3 earnings beat which was introduced on the tail-end of October has introduced shares proper again as much as $85+ degree which suggests overhead resistance of between $87 & 89 per share) will almost definitely be examined on this newest bullish transfer. Due to this fact, as we stand, WFG stays down roughly 3.85% (once we embody dividend distributions) since our most up-to-date commentary in July. We, nevertheless, are reiterating our bullish stance in WFG for the next causes.

Technical Evaluation

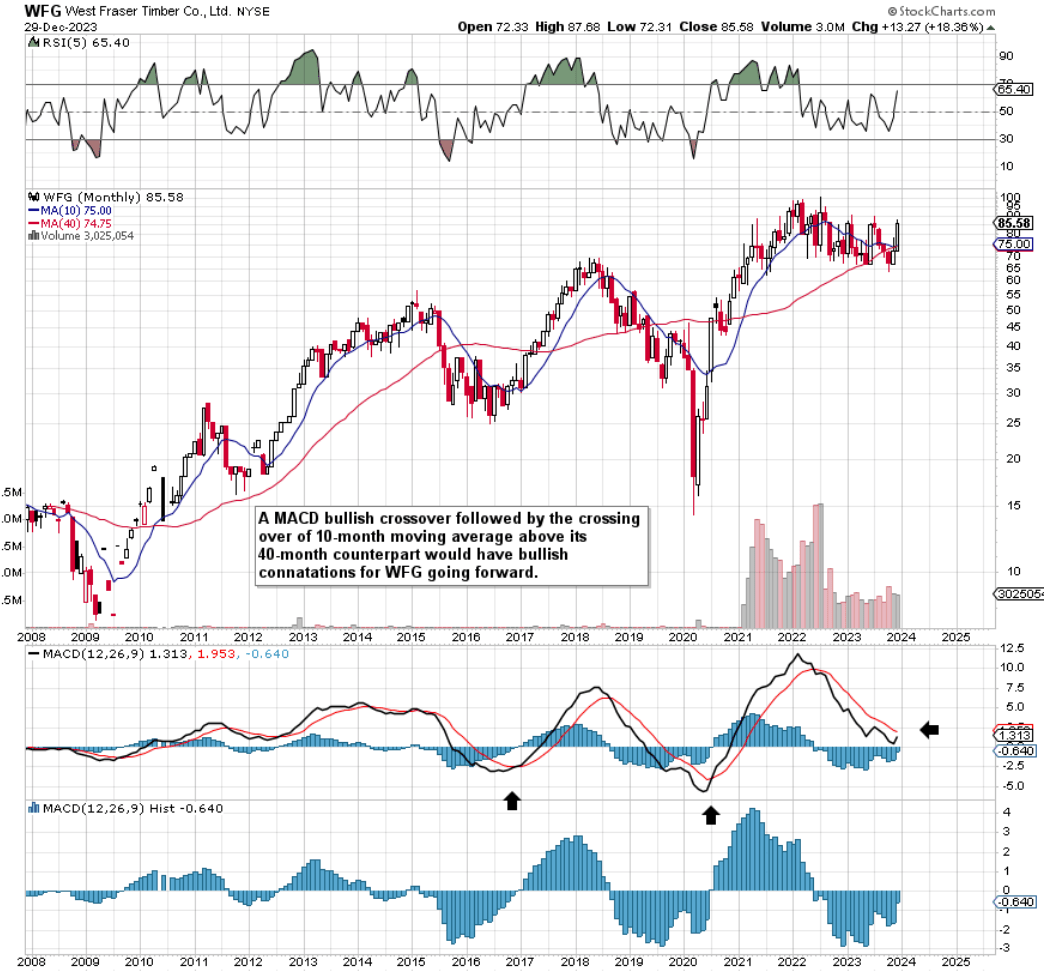

If we pull a long-term chart of WFG, we see that two long-term shopping for alerts look to be at hand. The primary is the MACD which may be very near giving a long-term shopping for sign because of the converging nature of the indicator’s trendlines. MACD crossovers are particularly noteworthy on long-term charts because of the twin function of the indicator (momentum & pattern) in addition to the sizable quantity of knowledge that will get digested within the course of. Moreover, if we are able to mix a MACD crossover with a crossover of the inventory’s 10-month-moving common above its 40-month counterpart, this is able to stack the percentages in favor of a sustained bullish pattern in WFG over the following couple of years.

WFG Lengthy-Time period Technicals (Stockcharts.com)

Intermediate 5-Yr Chart

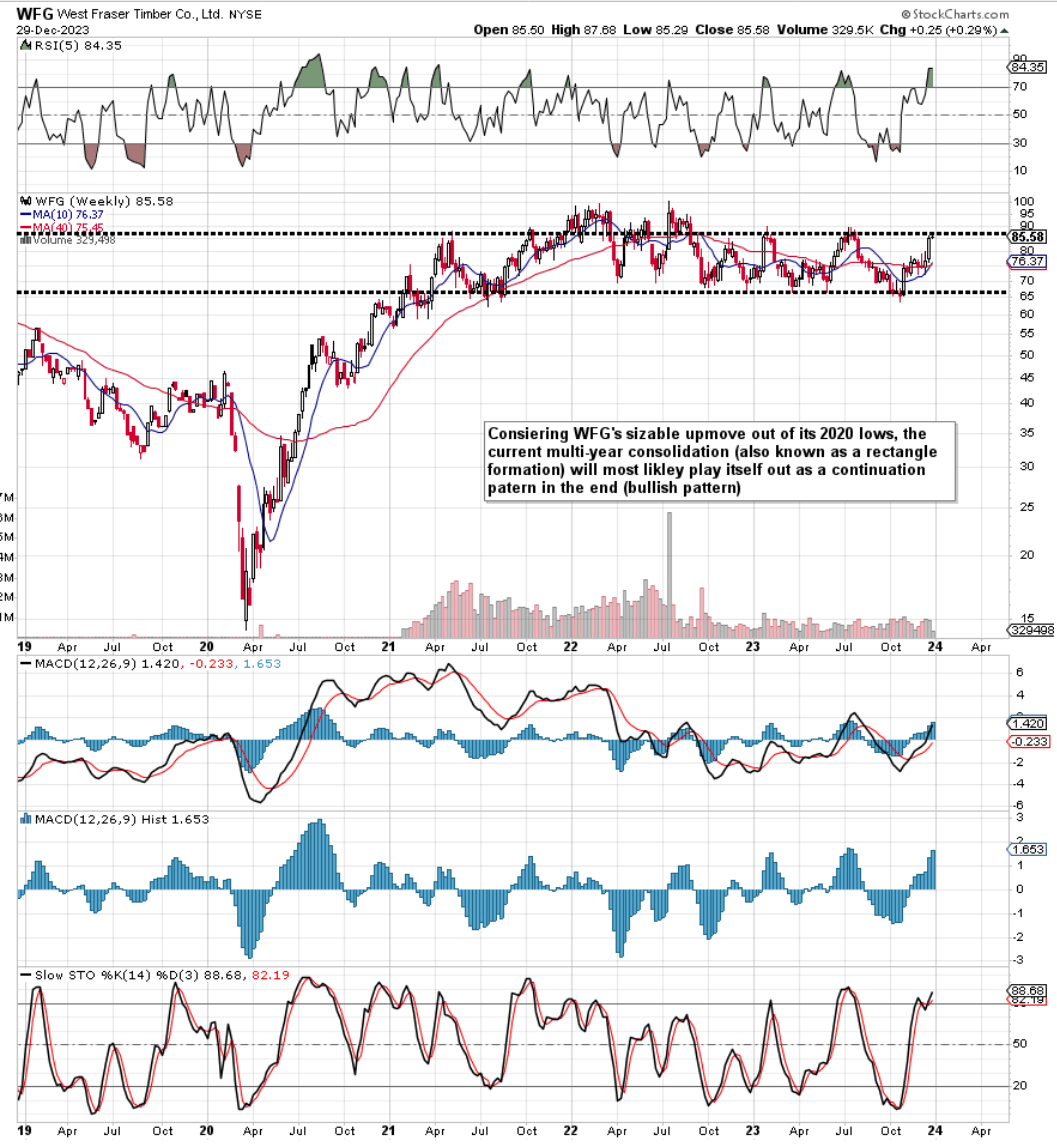

As we see beneath, shares of WFG have been consolidating for nearly 3 years now. Because the consolidation (rectangle formation) started to take form after the numerous upmove out of the inventory’s 2020 lows, we see this sample enjoying itself out as a continuation sample (bullish) over time. A decisive shut above the inventory’s all-time highs (February’2022 highs of $99+ per share) would affirm the sample. Moreover, it’s the peak of the sample that ought to curiosity buyers in that the forecasting worth could be WFG buying and selling at $120 per share minimal if certainly a breakout is on the playing cards.

WFG Intermediate Technicals (Stockcharts.com)

Funding Case

As chartists, we consider WFG’s technicals are the summation of each recognized piece of knowledge (be it basic or in any other case) on West Fraser Timber at this second in time. Due to this fact, despite the fact that the latest determination to divest a number of pulp mills & purchase a sawmill might not be totally up to date within the firm’s steadiness sheet as of but, the market has already digested the ramifications of how WFG continues its quest to work in the direction of being a flagship renewable wooden constructing provider for its clients.

We proceed to consider WFG is undervalued as outlined in its key valuation multiples beneath. Though the corporate’s earnings & cash-flow multiples might not be at ranges the place buyers would love (GAAP earnings a number of is definitely destructive over a trailing 12-month foundation), we advocate buyers focus extra on how low-cost WFG’s property are. As we see beneath, (when in comparison with the sector at giant in addition to WFG’s historic averages), the corporate’s trailing 12-month e book a number of is priced at a major low cost to what we’ve got change into accustomed to on this inventory.

| Valuation A number of | Trailing 12-Month | Sector Median | WFG 5-Yr Common |

| Value To E-book | 0.95 | 1.75 | 1.50 |

| Value To Gross sales | 1.10 | 1.25 | 0.95 |

| Value To Money-Circulate | 12.47 | 8.73 | 10.91 |

| Value To Earnings | NM | NM | NM |

Steadiness Sheet Energy

In WFG’s most up-to-date quarter, shareholder fairness surpassed $7.5 million which suggests e book worth has basically tripled because the finish of fiscal 2020. Suffice it to say, when a inventory is buying and selling beneath e book worth (E-book-value per share is available in at $90+ per share at current), has destructive debt when the money steadiness is taken under consideration, and is anticipated to develop earnings aggressively, it stacks the percentages in favor of a rising share-price over time. WFG actually ‘made hay’ when lumber costs spiked in 2021 & 2022 and though that anomaly could not occur once more for a while, the corporate’s monetary place has improved no finish in recent times. We reiterate our level that so long as WFG can generate sufficient gross sales (from its low-cost property) to generate earnings and money circulate, then this exact same money circulate can be utilized to develop the corporate over time by way of investments even when lumber demand slackens off in sure durations going ahead. Due to this fact, taking the above under consideration plus the corporate’s robust forward-looking growth path, we preserve that WFG stays a ‘Purchase’ at this second in time.

Conclusion

To sum up, we’re reiterating our bullish stance in West Fraser Timber resulting from its bullish technicals, robust progress curve, low valuation in addition to destructive debt place. We’re on the lookout for the pattern regarding the firm’s robust EBITDA progress quantity in Q3 to proceed into fiscal 2024. We stay up for continued protection.