Love Worker/iStock through Getty Pictures

Gritstone bio’s (NASDAQ:GRTS) power lies in its best-in-class antigen prediction, pushed by a proprietary synthetic intelligence (AI) platform known as EDGE. This platform allows the identification of crucial T-cell targets, a key part within the design of novel vaccine codecs. Moreover, Gritstone employs next-generation vectors, together with ChAd and self-amplifying mRNA (samRNA), to induce robust and sturdy immune responses suited to varied scientific contexts. Notably, Gritstone was the pioneer in introducing samRNA into scientific trials again in 2018.

In my first Gritstone bio article, I mentioned my bull thesis which is centered on the corporate’s technique and the ticker’s discounted valuation.

Background On Gritstone

Gritstone bio is a biotech firm with a particular concentrate on advancing immunotherapies. Gritstone’s power lies in its best-in-class antigen prediction, pushed by a proprietary synthetic intelligence (AI) platform known as EDGE. This platform allows the identification of crucial T-cell targets, a key part within the design of novel vaccine codecs. Moreover, Gritstone employs next-gen vectors, together with ChAd and samRNA, to set off strong and sturdy immune responses applicable to a number of scientific circumstances. Notably, Gritstone was the pioneer in introducing samRNA into scientific trials again in 2018.

Gritstone bio saMRNA Benefits in Infectious Illnesses (Gritstone bio)

The corporate’s objective is to unleash the formidable energy of the immune system towards most cancers and infectious illnesses. That is completed utilizing Gritstone’s precision drugs strategy with the identification and focusing on of tumor-specific neoantigens and strategic integration of AI into its platform. This technique creates a synergy that propels its endeavors in predicting and prioritizing neoantigens, thus enabling the event of personalised most cancers vaccines and immunotherapies.

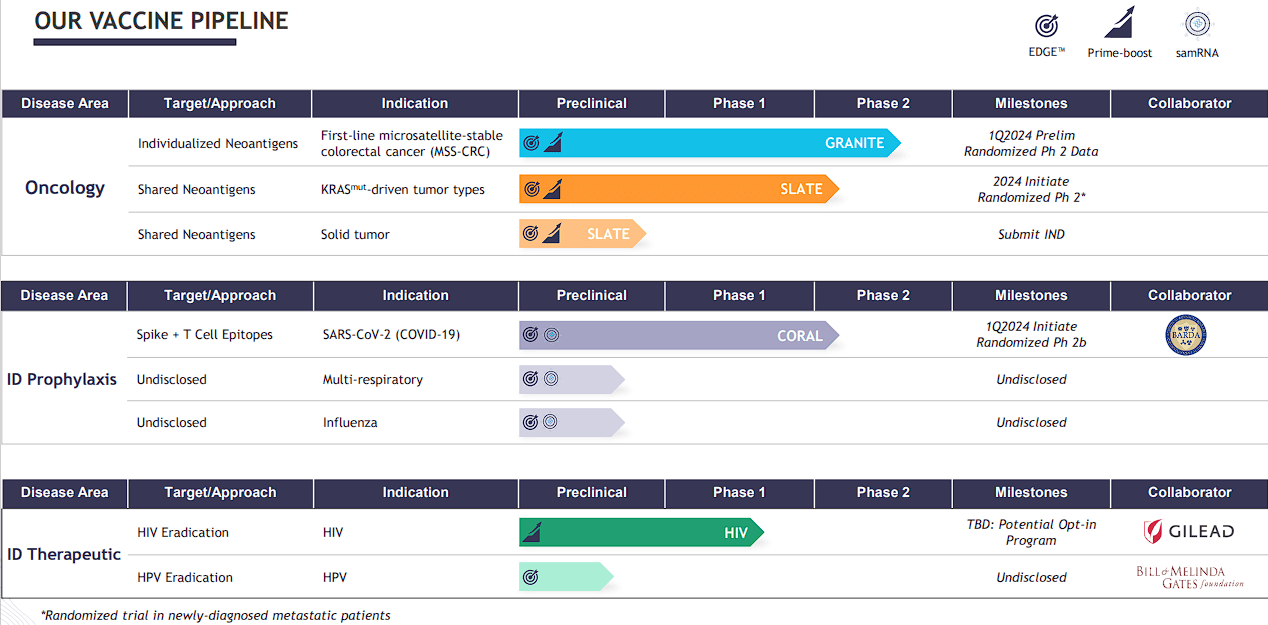

Gritstone bio Pipeline (Gritstone bio)

Gritstone can also be working in collaboration with Gilead (GILD) for a vaccine-based immunotherapy for HIV with a deal worth reaching as much as $785M, inclusive of royalties. The partnership capitalizes on Gritstone’s adenoviral and samRNA vaccine platform applied sciences, supported by promising preclinical information highlighting strong anti-SIV CD8+ T-cell reactions and protracted T-cell reminiscence. Gilead is actively engaged in a Section I examine and holds accountability for all analysis and growth elements. The settlement outlines an upfront cost of $60M, with attainable milestones amounting to $725M tied to scientific, regulatory, and business achievements. Moreover, Gilead is obligated to make a $40M milestone cost for Section II opt-in. The phrases of the association additionally stipulate mid-single-digit to low double-digit tiered royalties on internet gross sales post-commercialization. This collaboration underscores a strategic initiative to advance HIV therapy by revolutionary vaccine approaches, with substantial monetary incentives tied to developmental milestones and business success.

Gritstone bio and Gilead HIV Collaboration (Gritstone bio)

Current Updates

Within the firm’s current earnings report, Gritstone highlighted their progress within the CORAL program, which mixes samRNA with distinctive B and T cell targets. The current information highlights Gritstone’s samRNA-based strategy to yield sustained extraordinary neutralizing antibody responses and T cell activation noticed throughout Section I research. Not solely did the info present the vaccine’s potential for long-lasting protection towards COVID-19, however it additionally suggests it’s a frontrunner within the next-gen COVID-19 vaccine race.

Gritstone bio CORAL Section I Outcomes (Gritstone bio)

Furthermore, Gritstone was awarded a BARDA contract in September, which is value as much as $433M. The corporate introduced that they’ve a Section IIb comparative examine set to start in 1Q 2024, which is able to consider Gritstone’s samRNA candidate towards an accepted COVID-19 vaccine. This positions Gritstone as a key participant within the next-gen COVID-19 vaccine house and validates their samRNA expertise to supply superior vaccines to different mRNA expertise.

Gritstone’s GRANITE and SLATE oncology packages are nonetheless making progress. Gritstone’s flagship oncology program, GRANITE, a bespoke neoantigen vaccine is progressing by a randomized Section II/III examine in first-line metastatic, microsatellite steady colorectal most cancers (MSS-CRC). The Section II part of the examine is anticipated to yield early efficacy information in 1Q of this yr. If the info is constructive, GRANITE has the potential to be a breakthrough in treating ‘chilly’ strong tumors proof against present immunotherapies.

Gritstone’s “Off-the-Shelf” or share neoantigen vaccine program is partnered with the Nationwide Most cancers Institute (NCI) to evaluate an autologous T cell remedy along with the “off-the-shelf” most cancers vaccine for KRAS mutation cancers. The NCI-run Section I examine acquired the IND again in October of 2023. Gritstone’s intention to provoke a randomized Section II scientific trial in 2024. If profitable, Gritstone may need a most cancers vaccine tech that may have a broader business readiness in contrast their personalised strategy.

One other notable growth is Gritstone’s collaboration with Genevant Sciences, which provides Gritstone the non-exclusive proper to make use of Genevant’s principal lipid nanoparticle (LNP) expertise for the event and commercialization of Gritstone’s samRNA infectious illness vaccines.

Wanting To 2024

Like a lot of the biotech firms within the Compounding Healthcare “Bio Boom” portfolio, Gritstone has the potential to disrupt their business with a novel expertise. The corporate has the prospects to disclose their potential to reshape each the COVID-19 vaccine and most cancers vaccine landscapes in 2024.

The Section II/III GRANITE-1L examine is anticipated in Q1 of 2024, which might confirm their potential to supply a vaccine with neoantigens, particular to a affected person’s tumor. Thus, permitting for a person strategy, rising the efficacy and lowering potential unwanted side effects.

Then, we’ve Gritstone’s samRNA COVID-19 vaccine program in a head-to-head battle with an accepted vaccine in a BARDA-funded 10,000-subject Section IIb randomized examine. This transfer positions Gritstone on the forefront of the worldwide effort to fight COVID-19, with potential benefits over current vaccines.

Gritstone bio BARDA Particulars (Gritstone bio)

Traders are maintaining an in depth eye on the initiation of the Section IIb head-to-head examine, slated for Q1 of 2024. Success on this endeavor might solidify Gritstone’s place as a key participant within the struggle towards infectious illnesses, offering a considerable enhance to its market worth.

Traders are eagerly awaiting the preliminary information and examine initiations as a result of they is perhaps key drivers for the inventory, as constructive outcomes might pave the best way for growth into further illness sorts, broadening Gritstone’s market outlook. As well as, constructive outcomes from these research might de-risk the corporate’s platforms, instilling confidence and doubtlessly attracting additional funding within the coming years at a probably increased valuation for his or her probably best-in-class platforms.

Weighing The Dangers

Regardless of Gritstone’s upside prospects, buyers want to concentrate on the unstable biopharma setting, which is inherently fraught with dangers from the challenges related to scientific growth. Unexpected security considerations, fickle efficacy outcomes, and regulatory hurdles pose hindrances that might influence the headway of the corporate’s candidates by the event pathway. Gritstone’s success hinges on its potential to navigate these challenges and efficiently advance its candidates by the rigorous phases of scientific growth. One setback might have a dramatic influence on the share value.

One other danger to think about is the aggressive enviornment of most cancers immunotherapy. Gritstone faces formidable competitors from established firms similar to Moderna (MRNA), BioNTech SE (BNTX), and others, that are actively engaged in advancing their very own revolutionary approaches to most cancers therapy. The success of Gritstone bio will rely upon its potential to distinguish its platform expertise and therapeutic candidates from these of its rivals. As well as, the corporate’s manufacturing prowess will probably be put to the check to maintain up with these bigger firms. Furthermore, Gritstone must take them on for market positioning, IP, and strategic collaborations, which is able to play pivotal roles in figuring out Gritstone’s aggressive edge on this unstable enviornment. It’s attainable that Gritstone is profitable within the clinic, however is outclassed by their friends.

Final however not least… Financials. On the finish of Q3, Gritstone bio reported $90.5M in money, money equivalents, marketable securities, and restricted money, which is from $185.2M on the finish of 2022. R&D bills moved as much as $32.8M, whereas G&A bills rose to $7.4M throughout Q3. Collaboration, license, and grant revenues for a similar interval totaled $1.6M. So, the corporate is burning by a major amount of money to maintain their pipeline shifting. At this level, we do not know the way the BARDA contract will offset any of the money burn, and the way their oncology packages will influence their bills. The corporate did file for a $250M shelf providing, so we are going to seemingly see some dilution in some unspecified time in the future in 2024. Contemplating we must always see some information in Q1, I anticipate to see an providing coming instantly after.

Contemplating these dangers, I’m sustaining my GRTS conviction degree of 1 out of 5 right now. Nonetheless, will revisit this grade as soon as we see the GRANITE information and we’ve a transparent understanding of how the corporate goes to make use of that $250M shelf providing.

My Plan

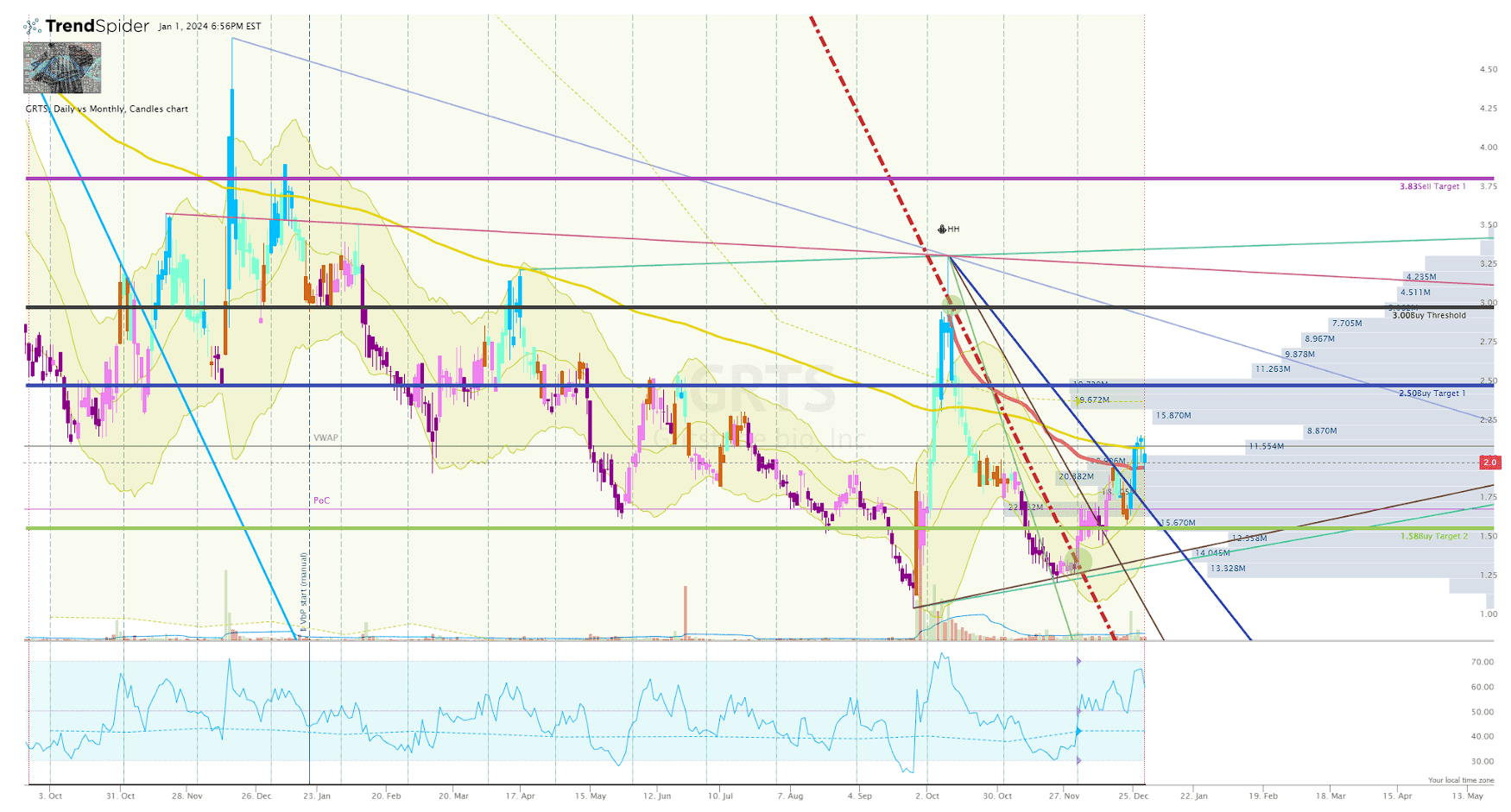

Though GRTS has been buying and selling beneath my Purchase Threshold for many of 2023, my GRTS place has been dormant because the ticker skilled relentless promoting strain with out a high-conviction reversal setup. Now, I’m wanting so as to add to my dormant GRTS place following the BARDA announcement again in September, which generated a pleasant reversal setup on the Every day Chart at $2.00 per share. Plus, the ticker is now bullish on the Go-No-Go Indicator and is buying and selling above the anchored-VWAP from the current excessive.

GRTS Every day Chart (Trendspider)

So, I will probably be seeking to place a purchase order within the coming days or perhaps weeks on a purple day for biotech. Admittedly, I’m not seeking to make a large addition at this level as a result of unknown response to the upcoming GRANITE information and certain subsequent choices.

Then again, I will probably be seeking to guide revenue if the share value responds positively to the info and hits my Promote Goal 1.

Nonetheless, if the info is constructive and Gritstone decides to tug the set off on an upsized providing, I’ll as soon as once more look to be a purchaser round $1.50 per share.

As with all my “Bio Boom” tickers, I’m seeking to commerce the GRTS all through its lifetime as a speculative ticker in an effort to develop a “house money” place for a long-term funding.