Ole_CNX

Whereas not with out dangers, Alphabet (NASDAQ:GOOGL) needs to be thought-about a core tech holding. The inventory at present seems to be undervalued in comparison with its mega-cap tech friends.

Firm Profile

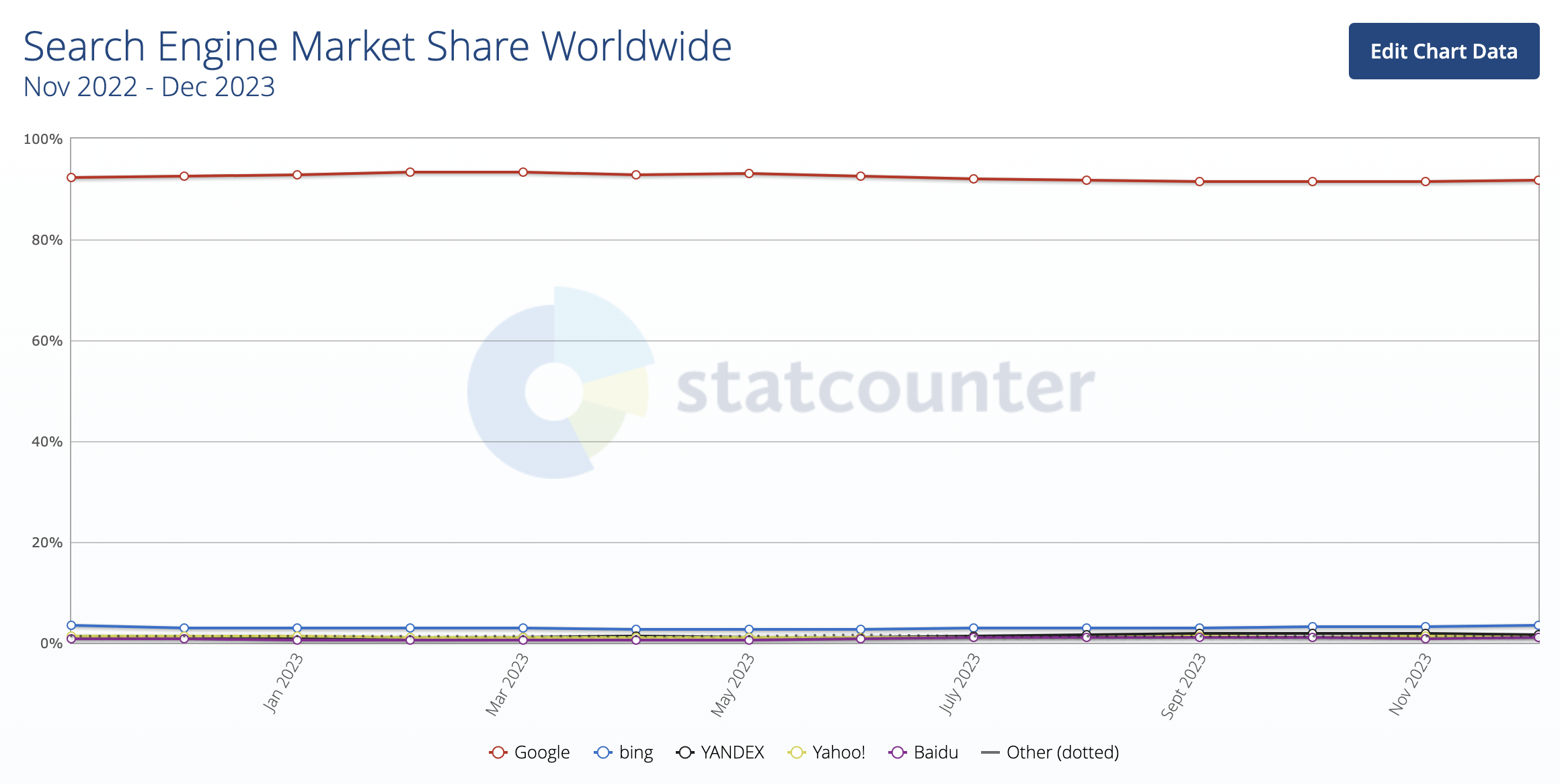

GOOGL owns a wide range of merchandise we use day-after-day. Its Google search engine holds a digital monopoly for search with an estimated over 90% international market share. Google Search generated almost $162.5 billion in promoting income in 2022 and $127.0 billion by means of the primary 9 months of 2023.

World Search Market Share (StatCounter)

Its YouTube video platform, in the meantime, is without doubt one of the largest on the planet. It generated $29.2 billion in income in 2022 and $22.3 billion by means of the primary 9 months of 2023. Not like different media platforms, it doesn’t have to spend so much on upfront content material prices, as an alternative utilizing a revenue-sharing mannequin with content material creators. YouTube Music and Premium surpassed 80 million subscribers as of the final reported numbers in 2022.

The corporate additionally serves up adverts by means of its focused promoting expertise through Google Community, which incorporates AdSense, AdMob, and Google Advert Supervisor. By these applications, the corporate will serve adverts to consumer web sites or apps primarily based on their content material, geographical location, and different elements. Google Networks generated $32.8 billion in income in 2022 and $23.0 billion by means of the primary 9 months of 2023.

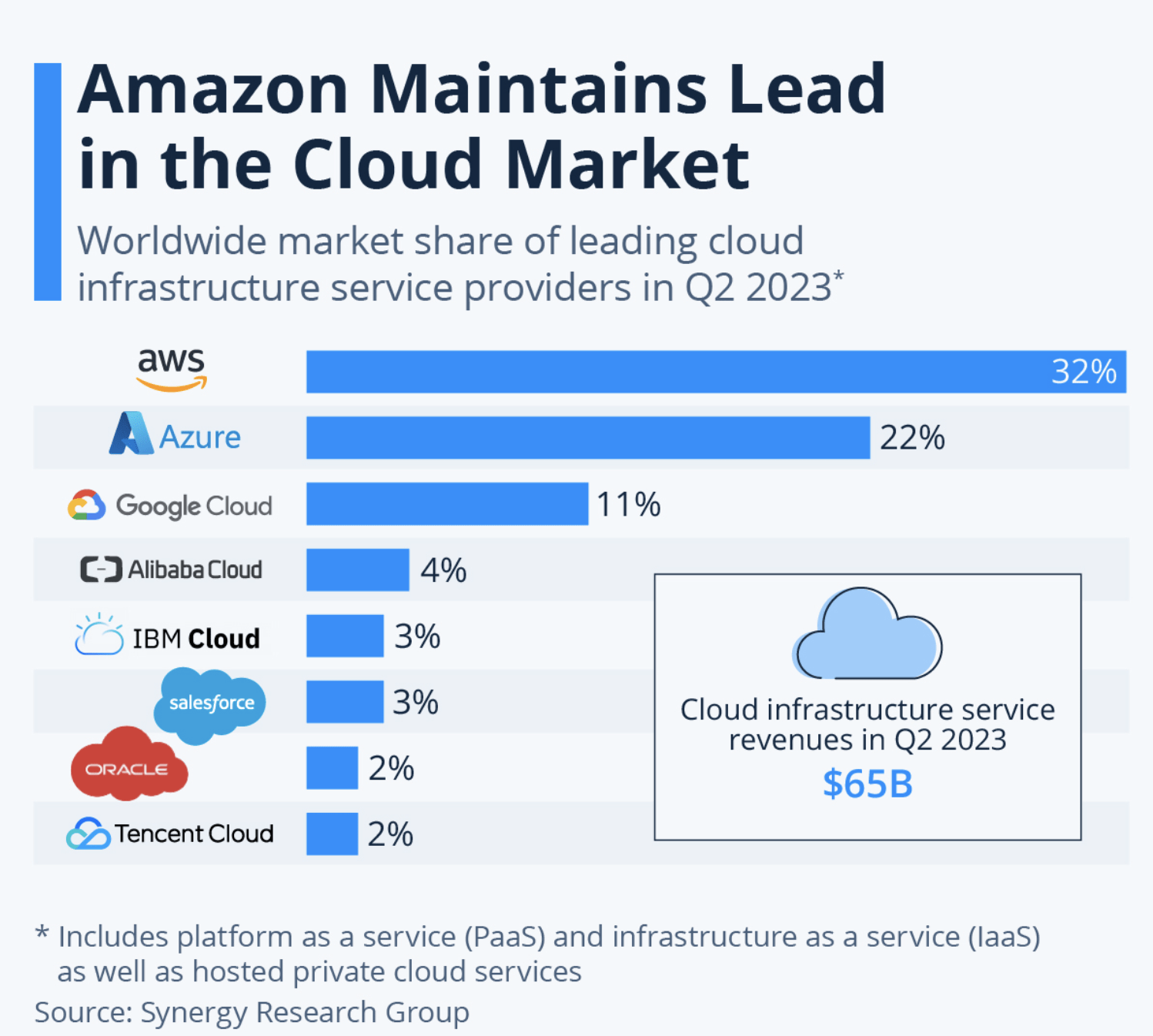

Google Cloud is the #3 cloud infrastructure firm behind leaders AWS, owned by Amazon (AMZN), and Microsoft (MSFT) Azure. It generated $26.3 billion in income in 2022 and $23.9 billion by means of the primary 9 months of 2023.

Cloud Infrastructure Market Share (Statista/Synergy Analysis Group)

As well as, GOOGL owns the Android working system, Gmail, the Chrome net browser, Google Classroom, navigation platforms Maps and Waze, and Google Images, amongst others. It additionally has a hand in {hardware} with its Pixel smartphone, sensible residence product line Nest, Chromebook, and streaming gadget Chromecast.

Lastly, it’s engaged on some extra pie-in-the-sky tasks similar to self-driving vehicles (Waymo), quantum computing (Sycamore), and sensible cities (Sidewalk Labs).

Alternatives & Dangers

GOOGL has a digital monopoly in search, which ought to proceed to be a development engine for the foreseeable future. Its potential to ship performance-based adverts, versus model adverts, is admittedly unmatched by most rivals.

Efficiency-based adverts are backside of the funnel and are usually extra resilient in comparison with model promoting. They’ve a way more direct and measurable correlation to gross sales, so firms like to make use of this sort of promoting, particularly when there are extra issues across the shopper. Efficiency promoting has additionally been getting a lift from the massive pushes of Chinese language firms like Temu, owned by PDD (PDD), and Shein, which have been attempting to attract in U.S. shoppers with low cost offers.

One other massive alternative for GOOGL is the monetization of YouTube Brief movies. With an estimated 2.7 billion energetic customers, YouTube is already fairly giant. Beforehand, Brief creators had no choices to earn cash from producing movies, not like with YouTube’s long-form movies. Beginning in 2023, GOOGL began sharing 45% of advert income with creators on its Companion Program. To qualify, creators will need to have 1,000 followers and 10 million Brief views over 90 days. Income shall be allotted to creators primarily based on their share of Brief views.

The purpose right here is to incentivize creators to supply content material for YouTube Shorts to compete with TikTok. In the meantime, the higher the group performs as an entire, the extra money creators can earn. It’s also value noting that creators shall be allowed to monetize their content material when utilizing standard music, which has been a sticking level prior to now.

Up to now, YouTube Shorts seems to be working. In July, the corporate famous that Brief video watchers had risen from 1.5 billion to 2.0 billion in a yr. In the meantime, in October, the corporate stated Shorts averaged 70 billion views a day and that the corporate was engaged on closing the monetization hole between lengthy type and brief type movies.

Google Cloud is one other alternative for the agency. Cloud continues to be one in all its strongest top-line drivers, rising round 26% to date in 2023. It has but to show a full-year revenue but, though it’s on observe to take action this yr. It’s a excessive fixed-cost enterprise and GOOGL is the #3 participant, so it continues to wish to scale the enterprise. If Google Cloud can proceed its momentum, it needs to be a pleasant backside line driver shifting ahead as nicely.

One space that GOOGL has closely invested in is synthetic intelligence (“AI”) and machine studying (“ML”). It’s trying to make use of this tech throughout the corporate, each with search, cloud computing, and different areas. Some explicit areas of focus are translation, pc imaginative and prescient, and pure language processing.

Discussing AI at a Scotiabank Conference last month, CTO of Google Cloud Will Grannis stated:

“Our experience is really approaching it from a full stack or a comprehensive approach. And what do I mean by that? The design principle behind Google Cloud’s approach to AI is offering a complete AI stack. What does that mean? It means that the research that goes into these novel techniques, it means that the processors, both ours and others in the semiconductors and the chips. The design and the optimization, we spend a lot of time there. But then we also spent a lot of time on the tooling. Machine learning ops is a significant burden. Gen AI ops, a significant burden for any organization. So we also take it upon ourselves to create a platform that allows people to, without even knowing how to code, start their journey in generative AI. But then it also kind of goes up to the top of the stack, like I spoke about before. We want to give you an always-on collaborator. So even if you’re operating in SaaS, like you’re in Workspace, and you’re like, you know what, like you’re a small business. Maybe you started a dog walking business. There’s still time for you if that’s your aspiration. And the good news is Generative AI is here to help. And what it can do is you can express a desire like, “Hey, I really want to track my clients, but I don’t know how to get started.” And you can give what we call Duet AI, that’s our always-on AI collaborator. You can give Duet AI that intent, and it will generate for you a tracking spreadsheet with the typical columns and the typical fields. If you’re trying to run a dog-walking business, for example, without you having to think through the structural components or get started.”

Whereas AI is a chance for GOOGL additionally it is a danger. OpenAI’s ChatGPT obtained plenty of buzz in 2023, and rival MSFT made a $10 billion funding into the AI agency and integrated its tech into its merchandise, together with Azure, Microsoft 365, and its search engine Bing. That upped the sport and will have rushed GOOGL into an AI race earlier than it needed to be in a single.

The most important danger from AI seemingly isn’t MSFT and ChatGPT, however from GOOGL cannibalizing its personal income. If customers can get data they want immediately from Google with out having to go to web sites, it may probably result in much less clicks on related adverts. The counter argument is that it may result in extra use of the Google search engine, and that Google may benefit from extra impressions whereas the corporate may create new types of adverts to learn from AI solutions.

Outdoors on AI and expertise disruption, the macroeconomy is one other danger. As a frontrunner in search and video, GOOGL makes the majority of its cash from promoting. As such, the corporate isn’t resistant to a slowdown in advert spending. Not like prior to now the place the secular development may simply outpace any macro weak spot, that isn’t essentially the case anymore.

In the meantime, whereas Google Cloud has began to show worthwhile, there isn’t any assure that it will proceed. You could have three enormous firms preventing for market share that might be prepared to compete on value if crucial. AMZN’s AWS development and working margins have each fallen to date this yr. By the primary 9 months to the yr, its working margins have been 26.2% versus 30.0% final yr. Progress to date in 2023, in the meantime, was 11% versus 32% throughout the identical interval in 2022. There is no such thing as a doubt AMZN will attempt to combat again, and it has proven a willingness to sacrifice some margin to take action prior to now.

Regulation is one other danger. The corporate has paid out a variety of latest authorized settlements lately. It lately agreed to pay $700 million and permit builders to supply direct funds on its Play app. It additionally settled a $5 billion lawsuit, phrases not disclosed, in a privateness lawsuit as a result of it tracked individuals who have been viewing in personal modes. Late final yr, it reached a $391.5 million settlement with 40 states associated to monitoring private knowledge.

The large danger, although, is the present DOJ case against the company that it’s a monopoly that illegally used its energy to its profit. A loss may result in an enormous high quality, a change in enterprise practices, and a harm to model status. It additionally would seemingly be adopted by the same case in Europe. Authorized dangers are at all times among the many most tough to quantify.

Valuation

GOOGL at present trades at about 11.5x 2024 EBITDA estimates of $139.9 billion. Stripping out its roughly $4.5 billion in losses on Different bets, the core enterprise is just buying and selling a 11.2x EBITDA.

Based mostly on the present 2025 EBITDA consensus of $158.3 billion, the inventory trades at a ten.2x a number of.

Income is projected to develop 11.3% in 2024 and 10.9% in 2025.

The corporate has rebounded nicely this yr, with income development accelerating by means of the yr, up 6% in fixed currencies in Q1, 9% in Q2, and 11% final quarter. It additionally expanded its working margin to twenty-eight% in Q3 from 25% a yr in the past.

GOOGL at present has a free money circulation yield of about 4.4% primarily based on FCF of $77.5 billion within the final trailing twelve months.

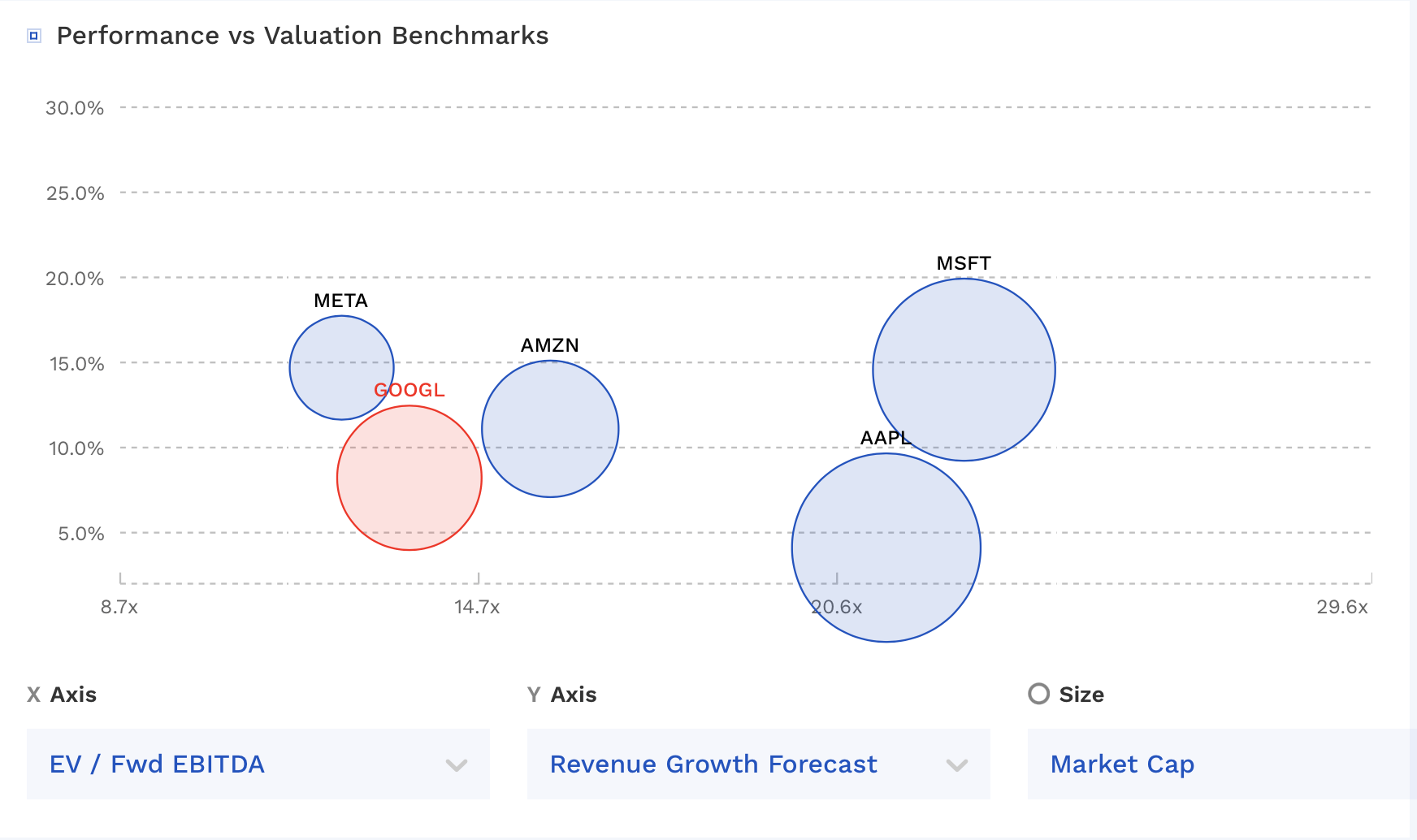

GOOGL is among the many cheaper mega-cap tech shares.

GOOGL Valuation Vs Friends (FinBox)

To get to a year-end 2024 honest worth, I’d place between a 12-15x a number of of 2025 EBITDA for GOOGL, whereas assuming it provides about $75 billion in money to its steadiness sheet or returns it shareholders by means of buybacks. That equates to a good valuation vary between $175-207.

Conclusion

On the subject of expertise, there’s at all times the chance of disruption. It’s a typical theme in tech that new upstarts ultimately come alongside and disrupt incumbents. Ranging from scratch provides these upstarts an enormous benefit, as legacy incumbents are sometimes weighed down by previous designs and infrastructure investments that result in inefficiencies as applied sciences shift. Nevertheless, the truth that GOOGL has been constructed by itself versatile infrastructure helps shield it. The corporate additionally pours cash into analysis and improvement to probably “disrupt” itself. We’re on the level the place that is beginning to play out, however GOOGL seems to be nicely ready.

GOOGL’s digital monopoly on search is motive sufficient to personal the inventory at present ranges. It is without doubt one of the largest and most dominant firms on the planet. Nevertheless, the corporate doesn’t sit on its laurels and regularly seems to be at new merchandise, companies, and monetization efforts to drive development.

Longevity will be the most important query round tech firms as they mature – it’s one motive why Warren Buffett has tended to keep away from the sector. Nevertheless, GOOGL has constructed a platform targeted on simplicity and adaptability, which ought to permit it to endure and proceed to prosper. On the similar time, it regularly pumps cash into R&D to each drive development and to assist future proof itself.

For those who have a look at the variety of merchandise, companies, and apps GOOGL provides, it’s really fairly staggering. GOOGL merchandise are actually ingrained in our on a regular basis lives and sometimes in our work lives as nicely. And it’s GOOGL’s potential to repeatedly innovate that may actually drive development shifting ahead.

As such, I take into account GOOGL a core, long-term holding. I’ve a “Buy” ranking and $190 value goal on the inventory.