andresr

As I comb by means of gold miners, I got here throughout the mineral exploration firm New Discovered Gold Corp. (NYSE:NFGC). Of the 4 analyses written on it in 2023 right here on In search of Alpha, two have been Buys, and two have been Holds. I, nonetheless, suppose the firm is a SELL.

The explanations for which might be easy, so I will additionally spend this text giving concepts on when shares of NFGC may grow to be a Purchase.

Historical past Since IPO

Exploration

The corporate solely not too long ago had its IPO in 2020 on the Toronto Inventory Change. It later turned obtainable on NYSE in 2021. Its solely vital asset is the mineral licenses for the Queensway web site, situated in northern Newfoundland, Canada. It’s a giant space, protecting 1,662 sq. km.

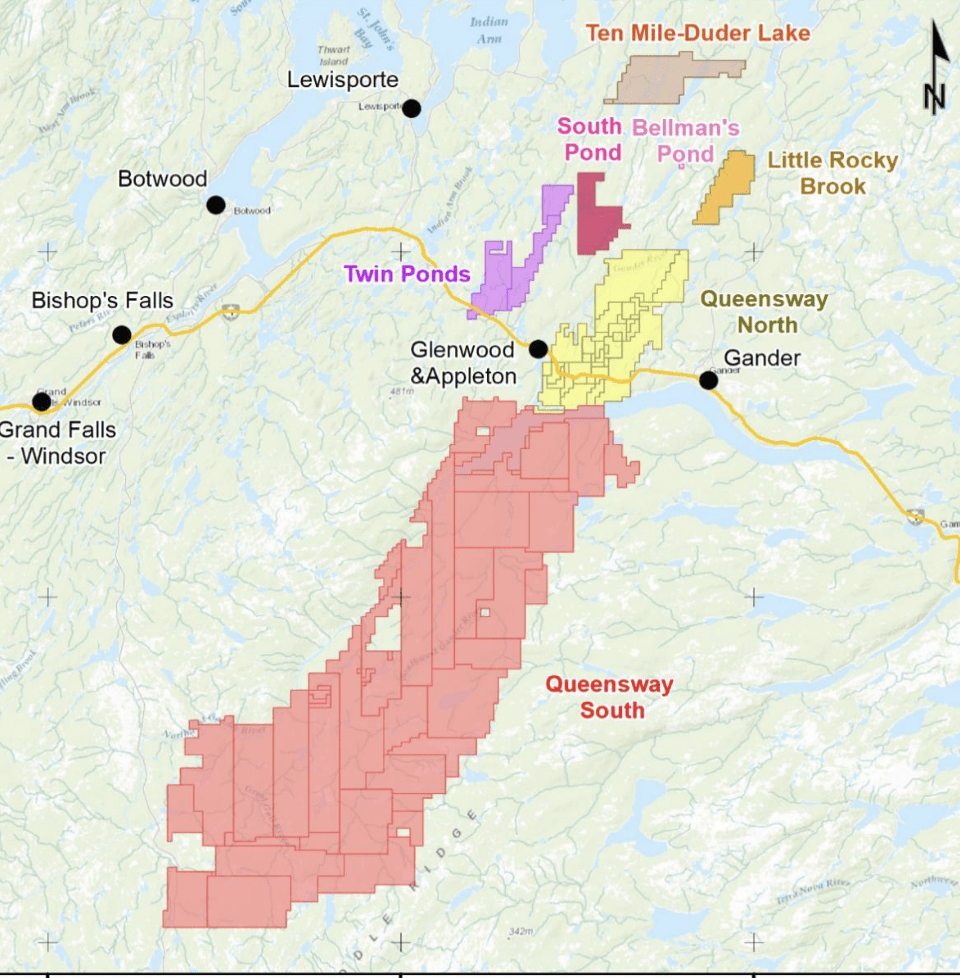

Over the past three years, the northern portion of the property has undergone quite a few drilling and exploration tasks of the world. The Q3 2023 MD&A launch reveals how the location is damaged down.

Q3 2023 MD&A

As this reveals, a lot of the land is but to be explored. Let’s take a look at the assorted websites which were drilled and assessed.

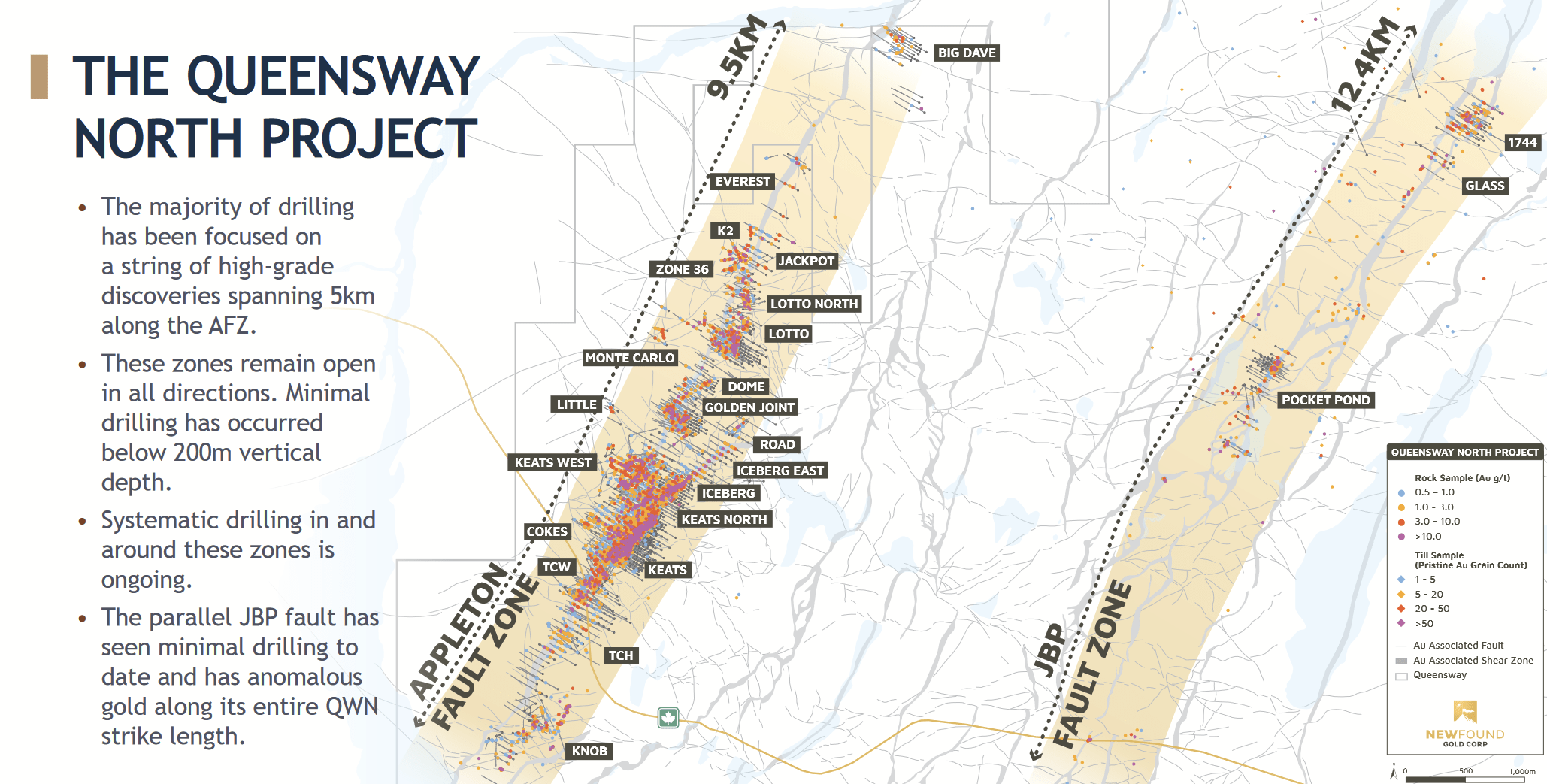

Firm Presentation

Primarily based on these samples that they’ve used to map out the world, the corporate believes a number of deposits of high-grade gold exist alongside the Appleton and JBP fault zones within the northern portion.

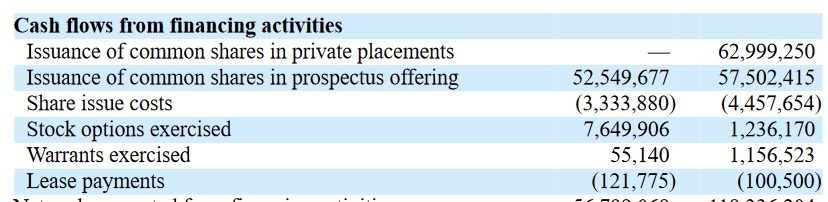

Monetary State of affairs

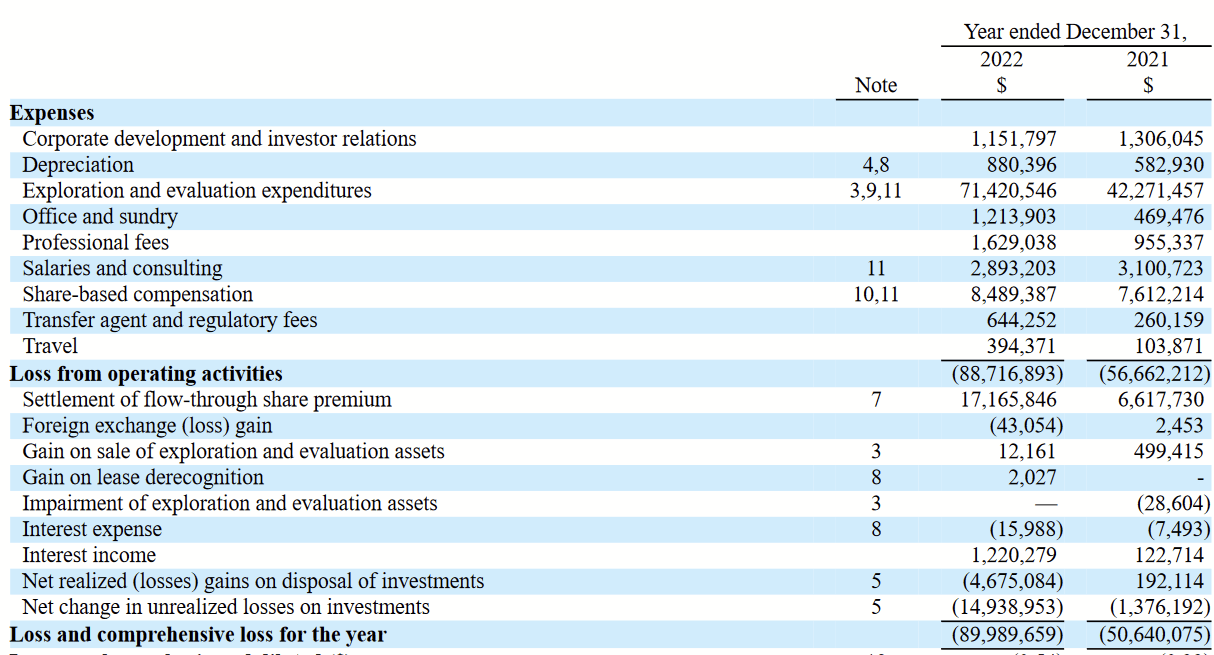

Because the revenue assertion reveals (and as its exploration tasks indicate), the corporate has no revenues, solely working bills.

2022 Annual Report

In 2022, they reported a lack of virtually $90m in CAD. To be able to fund operations with none revenues to help them, the corporate has been elevating capital by promoting shares.

2022 Annual Report

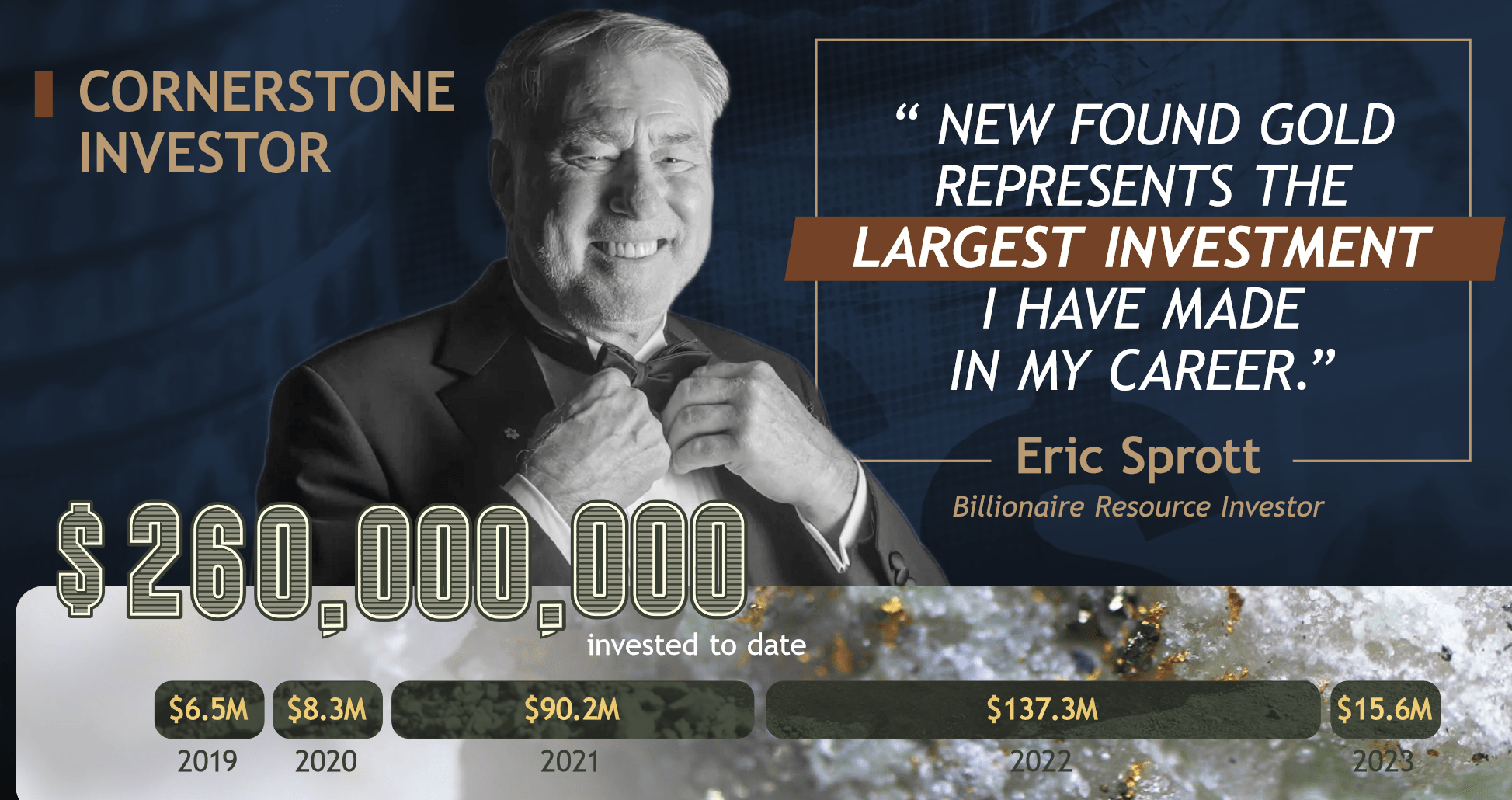

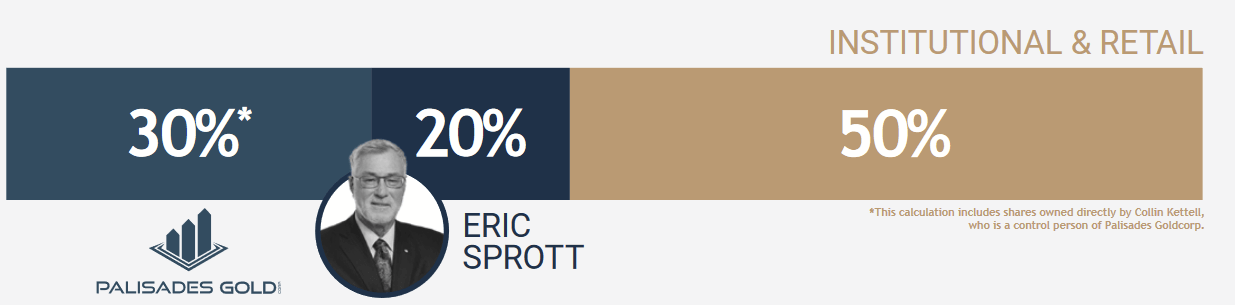

A major quantity of this has come from billionaire Eric Sprott, because the slide under reveals.

Firm Presentation

He stepped up his investments in 2022, with complete contributions of just about $258m.

Firm Presentation

This offers him about 20% of the corporate and has made him the most important particular person shareholder. But, the money has been necessary to keep up the exploration of the property, which is persistently exhibiting indicators of gold deposits.

Administration has not at the moment given indications of plans to develop the properties for mining. As such, it doesn’t at the moment describe itself as a mining firm however as a “mineral exploration company,” per its final annual report.

A Look to the Future

Conserving the Enterprise Going

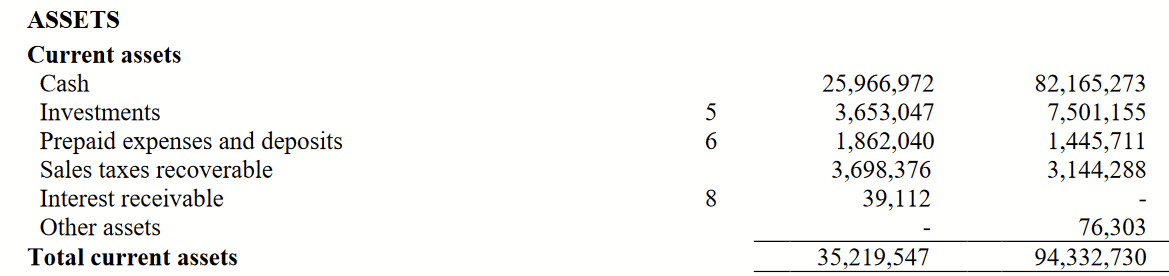

At the moment, the corporate doesn’t have satisfactory money to keep up its operational wants.

Q3 2023 Monetary Report

Money declined from $82m to $26m from the tip of 2022 to the tip of Q3 2023. Provided that bills have been in extra of $70m annually, this won’t be sufficient to proceed annually. This implies extra capital will should be raised. In its Q3 financial report, administration even acknowledged:

Administration is actively focusing on sources of further financing by means of alliances with monetary, exploration and mining entities, or different enterprise and monetary transactions which might guarantee continuation of the Firm’s operations and exploration applications. To ensure that the Firm to fulfill its liabilities as they arrive due and to proceed its operations, the Firm is solely dependent upon its capacity to generate such financing. These things give rise to materials uncertainties which can forged a big doubt on the Firm’s capacity to proceed as a going concern.

Historic knowledge present simply how main dilution of shareholders has been to maintain this firm going.

In search of Alpha

I do consider that, with Eric Sprott’s substantial, private stake, the possibilities of the corporate missing funds is decrease than your common would-be miner. But, he won’t be diluted by such a transfer; he’ll largely be the one diluting in my view.

Even when we could be moderately positive that this firm will develop into one thing that produces income, I feel the dilution present house owners would face will likely be higher than the advance in monetary outcomes, even for long-term traders.

The Transition to Revenues

This firm would not have income, and it is not clear at this second when that can change. Provided that it covers a reasonably substantial swath of land with excessive grades of gold detected, there’s a lot potential right here.

Sooner or later, the corporate might want to transition into growth and manufacturing, producing money from the sale of its ores. That course of hasn’t began but. It doesn’t should be lots both. The corporate can begin with modest growth at simply one of many websites they’ve recognized and use the money from that to fund the event of newer mines and proceed exploration with the bigger, extra southerly stretch of Queensway. Assuming the preliminary growth generates constructive money flows, I feel this could clear up the dilution downside.

When To Purchase

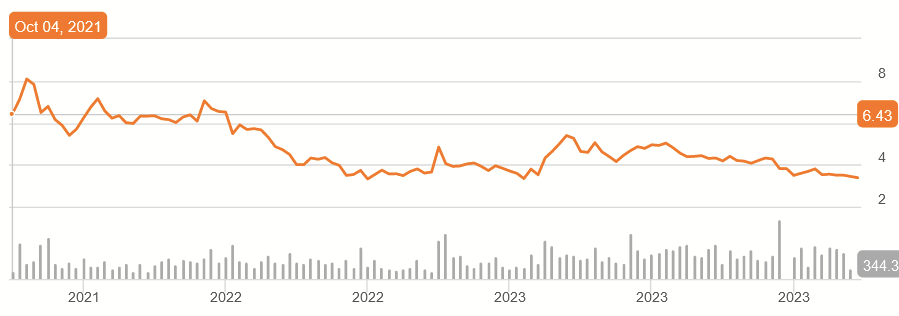

People who purchased in in the course of the IPO are doubtless disenchanted. Check out the chart.

In search of Alpha

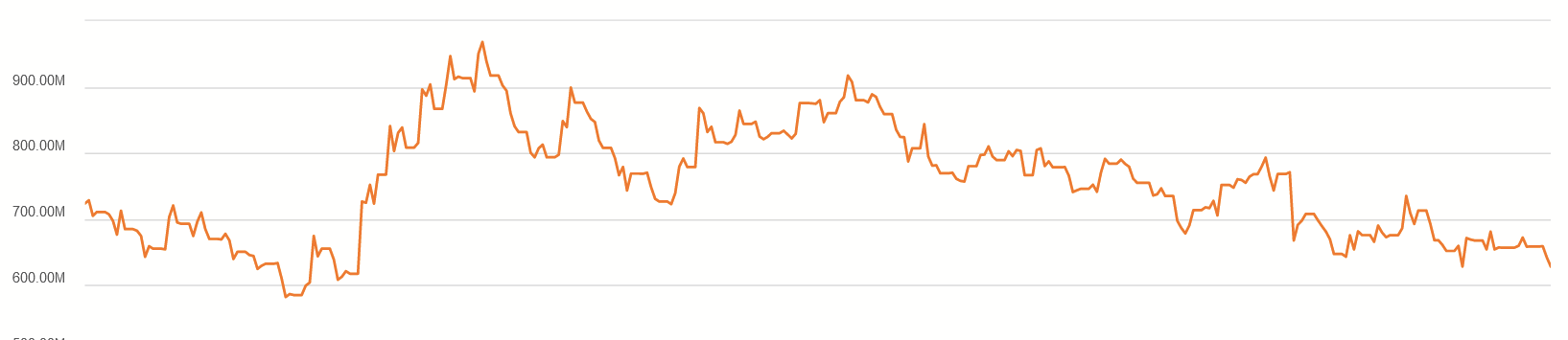

But, whereas the inventory is at the moment about half of the place it began, the market cap has not declined as a lot.

In search of Alpha

It is a decline, sure, however we additionally noticed a interval the place the worth of the corporate as a complete was increased. The market appears to be orbiting round a perception that this firm is price someplace between $600m and $800m. After I see a market cap for an organization that has no earnings, I interpret that as a P/E of 10 for the potential earnings. Might a single mine produce $60m – $80m for the corporate annually? I consider so, as I’ve seen mines that do this and since there’s quite a lot of ore over a big space right here, nevertheless it’s all a matter of A) when a mine is began and B) when that mine turns into worthwhile. Within the meantime, I do not suppose NFGC is price something as a result of there are merely no earnings to make use of as a foundation for valuation.

Even when the market sticks to its normal valuation, dilution will proceed, and I consider the share value will decline accordingly. Holding this inventory is not useful to the long-term investor till the basics change to the place the corporate is being profitable. At that second, I feel this firm will likely be price shopping for. I feel it might simply be 5 years earlier than one thing like that even occurs.

Conclusion

Money circulation is king. It is a tenet once I make investments. After I take a look at an organization with persistently destructive money flows, I look forward to issues to vary earlier than I purchase it. If any of us have been to begin our personal companies, whether or not it is a web site or perhaps a lemonade stand, we’d accomplish that provided that we consider we’ll make more cash than we put into it.

On this case, we now have an organization whose money flows are destructive, would not even have revenues, and whose operations are years away from reaching that time. It should proceed to lift capital by means of share dilution. There is not any positive factors to be made right here, so it is not even price holding for my part. If the corporate offers up, then I consider the shares might doubtlessly be price zero.

NFGC might show to be a really profitable funding, maybe even a staple dividend inventory. That is effectively into the longer term, and it is price retaining our eyes peeled for that day to return. Within the meantime, the dangers of capital loss are too nice, so NFGC is a straightforward SELL.