nathaphat

Thesis

I used to be initially desirous about shopping for Pfizer (NYSE:PFE) however after deeper analysis, I obtained increasingly more reluctant to tug the set off. So I’m ranking it a ‘Impartial/Maintain’ for now. Here is my narrative for Pfizer:

- Pfizer wants new income streams in a post-COVID world with patent cliffs on the horizon

- Patent cliffs are a sector-wide challenge for which M&A has been a software to replenish revenues

- Pfizer has usually paid excessive costs for M&A, above business norms

- Oncology has been a lagging enterprise for Pfizer regardless of being a scorching progress space

- Seagen could increase Oncology gross sales however the worth paid is hefty

- Administration’s execution file has been patchy

- Pfizer is comparatively costlier vs its friends

Pfizer wants new income streams in a post-COVID world with patent cliffs on the horizon

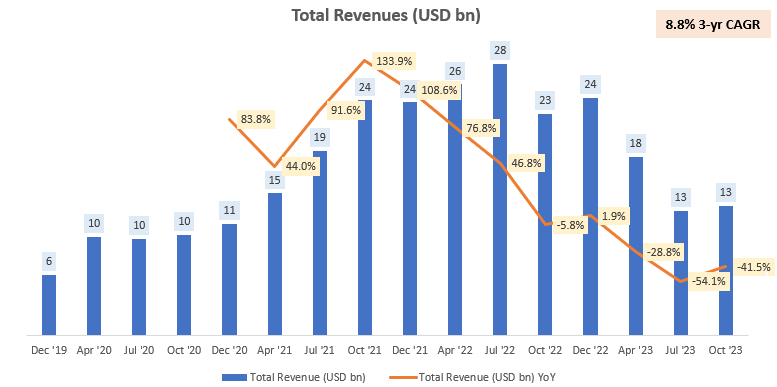

Pfizer’s revenues have been on a decline after a COVID-high:

Whole Revenues (USD bn) (Firm Filings, Writer’s Evaluation)

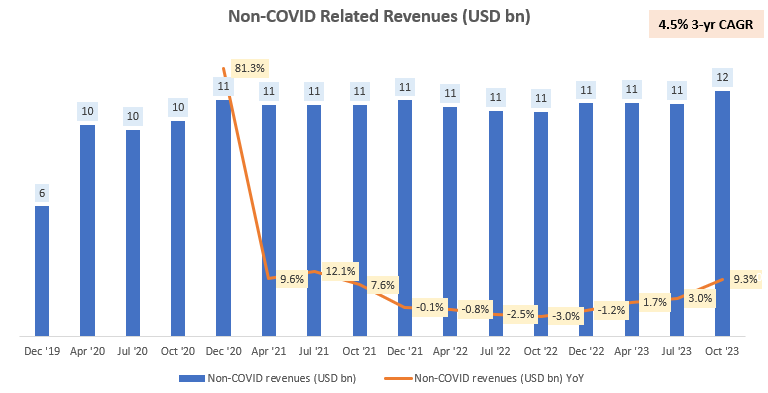

It is non-COVID associated revenues have grown at a paltry 4.5% 3-yr CAGR:

Non-COVID Associated Revenues (USD bn) (Firm Filings, Writer’s Evaluation)

Pfizer can also be marching in direction of a patent cliff. I had mentioned this in my SPDR S&P Pharmaceuticals ETF (NYSEARCA:XPH) article a yr in the past, estimating a $6.1bn income loss affect from patent expirations for Pfizer. Subsequently, Pfizer must desperately discover new income streams to replenish the medicine encountering lack of exclusivity (LOE), with out reliance any COVID-related booster to revenues (pardon pun).

Patent cliffs are a sector-wide challenge for which M&A has been a software to replenish revenues

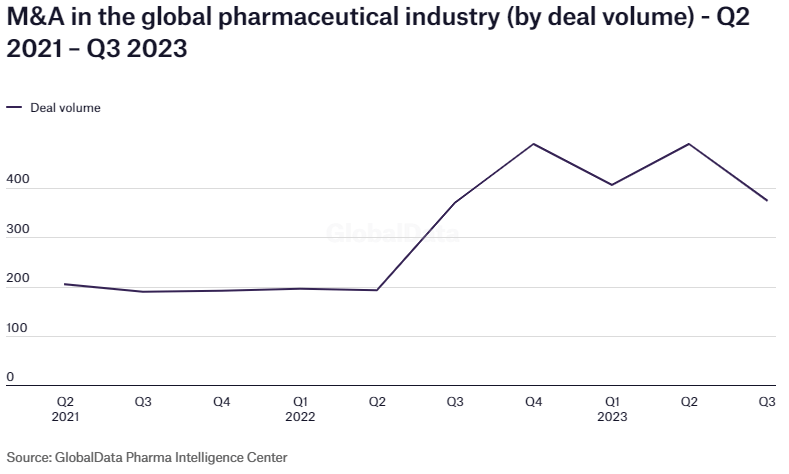

High pharmaceutical firms are dealing with dangers of dropping as much as 50% of general revenues from patent expirations. This has led to a flurry of M&A exercise within the world pharmaceutical business as firms search to replenish misplaced revenues. Discover the pickup in deal exercise since 2022:

Pharmaceutical M&A Deal Quantity (GlobalData Pharma Intelligence Middle)

Trade analysis from consultancy agency PwC and funding financial institution Leerink means that 2024 is more likely to see a continued rise in M&A exercise, notably large-deal exercise:

Regardless of a difficult rate of interest surroundings, PwC tasks the sector to see deal values starting from $225 billion to $275 billion.

At this level, let’s not overlook that most M&A deals fail. And the bigger the transaction, the more likely it’s to fail. That stated, M&A is usually vital and every deal in addition to the deal-making type should nonetheless be assessed independently:

Pfizer has usually paid excessive costs for M&A, above business norms

As is business observe, Pfizer has purchased smaller, unprofitable and typically even pre-revenue pharmaceutical firms. The worth paid has usually been above 20.0x revenues:

Pfizer Latest M&A Document (Firm Filings, Capital IQ, Writer’s Evaluation)

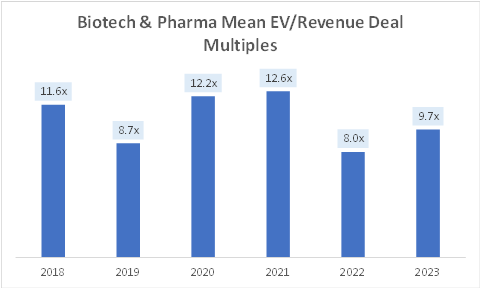

For context, in line with the Institute for Mergers, Acquisitions & Alliances (IMAA), the imply EV/Income deal multiples within the Biotech & Pharma sector has been round 10x over the identical time horizon (2019 – 2023):

Biotech & Pharma Imply EV/Income Deal Multiples (IMAA Institute, Writer’s Evaluation)

So Pfizer has usually paid a lot larger costs for its key acquisitions than business norms.

Oncology has been a lagging enterprise for Pfizer regardless of being a scorching progress space

Pfizer’s Oncology enterprise has lagged even non-COVID associated revenues, posting a 3-yr CAGR of just one.5%. That is regardless of Oncology being a hot growth area within the M&A transaction area.

Pfizer Oncology Revenues (USD mn) (Firm Filings, Writer’s Evaluation)

Pfizer’s administration is long-term bullish on Oncology as they’ve a sobering prediction about excessive most cancers charges:

As a reminder, 1 in 3 individuals can be identified with most cancers of their lifetime. Most cancers stays the second main reason for demise within the U.S., is a number one reason for demise worldwide and is the biggest progress driver in world drugs, bettering the lives of sufferers with most cancers could have huge, unimaginable affect on human.

– CEO Albert Bourla within the December 2023 Analyst & Investor Call

Because of this, they purchased cancer-curing company Seagen (SGEN), which I dig into right here:

Seagen could increase Oncology gross sales however the worth paid is hefty

Pfizer purchased Seagen for $45 billion or a 22.7x EV/Income deal a number of.

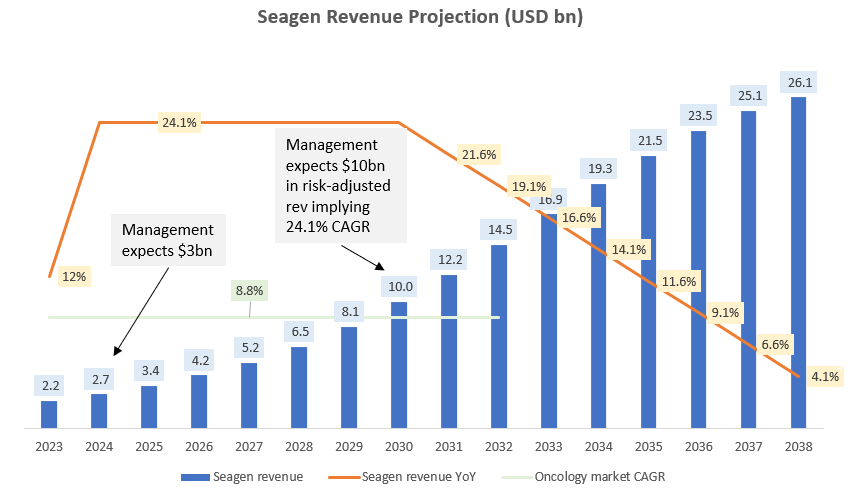

Seagen Income Projections (USD bn) (Firm Filings, Writer’s Evaluation)

Let’s set up an thought of base progress charges; the oncology market is anticipated to develop at a CAGR of 8.8% over the subsequent decade. Final yr, Seagen grew at 12% YoY. Administration anticipates 2024 to contribute $3bn and $10bn in risk-adjusted revenues (which means their base case estimate) by 2030. Utilizing these markers, it implies a roughly 24% income CAGR for Seagen until 2030; a lot sooner than the broader oncology market’s progress charges.

After 2030, I’ve assumed some moderation within the progress charges, again in direction of business ranges. I believe that is cheap.

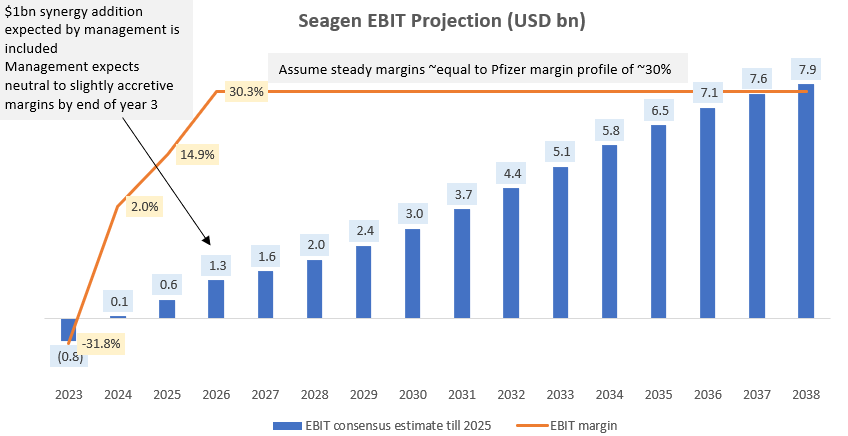

Seagen EBIT Projections (USD bn) (Firm Filings, Writer’s Evaluation)

On the margins aspect, Seagen is at the moment unprofitable with an EBIT loss of $750.6 million during the last twelve months (LTM). Administration expects $1bn in synergy advantages by the tip of 2026, which I’ve straight-lined over 3 years. By the tip of yr 3 or yr 4 after the acquisition, administration expects impartial to barely accretive margins, which is why I’ve focused round 30% EBIT margins (my estimate of Pfizer’s longer-term common) within the yr 2026. Since then, I’ve saved the margin profile fixed.

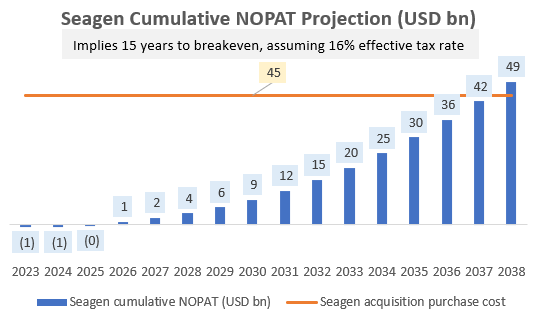

Seagen Cumulative NOPAT Projection (USD bn) (Firm Filings, Writer’s Evaluation)

Assuming an efficient tax charge of 16% (based mostly on industry-wide data and Pfizer’s longer-term historical past), the cumulative NOPAT crosses the acquisition consideration of $45 billion in 2038 which means 15 years until breakeven on the acquisition. This means a PE of ~15.0x. For context, the US Prescribed drugs sector is buying and selling at a 1-yr fwd PE of 10.41x. So the Seagen deal has occurred at a 44% premium to this worth. Relative to Seagen’s buying and selling worth, Pfizer paid a 33% premium for the deal.

On this evaluation, I’ve penciled in administration’s personal expectations and assumed what I imagine are cheap income and margin projections thereafter. But, the deal appears a bit costly. Now, here is a case for why administration’s base case could also be on the optimistic aspect:

Administration’s execution file has been patchy

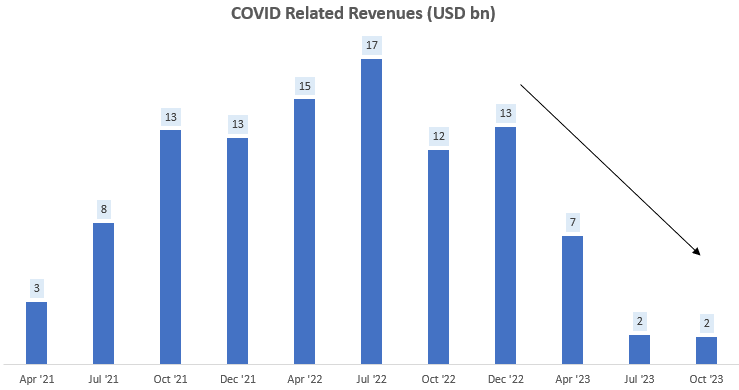

Administration has grossly overestimated COVID associated revenues, seeing a sharper fall than anticipated from $13 billion in This autumn FY22 to merely $2 billion in Q3 FY23:

Pfizer Non-COVID Revenues (USD bn) (Firm Filings, Writer’s Evaluation)

In Q2 FY23, Pfizer cut sales guidance for FY23 by $9 billion as a result of lower-than-expected COVID gross sales; $7 billion gross sales lower in Paxlovid and $2 billion gross sales lower in Comirnaty. Nonetheless, this revised expectation was nonetheless too optimistic. In Q3 FY23, Pfizer took:

$5.6 billion of noncash stock write-offs of COVID-related inventories

– CFO David Denton in Q3 FY23 earnings name

Subsequently, firm downgraded 2024 expectations on COVID-related revenues once more in Q3 FY23 to $8 billion. Consensus estimates stood at $12.5 billion earlier than that announcement.

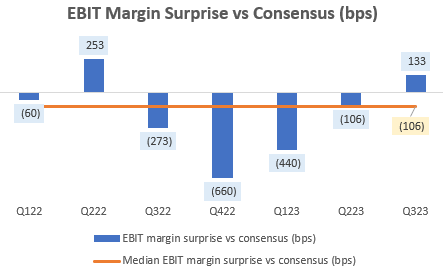

On the EBIT margins aspect, Pfizer has disenchanted the Road for a lot of the final 2 years, with a median shock of -106bps.

Pfizer EBIT Margin Shock vs Consensus (bps) (Capital IQ, Writer’s Evaluation)

General, these misses on revenues and margins undermine my confidence in believing administration’s phrase for a way they anticipate Seagen to carry out. The monitor file suggests that there’s draw back danger to their projections, which makes the acquisition appear much more costly than it already appears.

Pfizer is comparatively costlier vs its friends

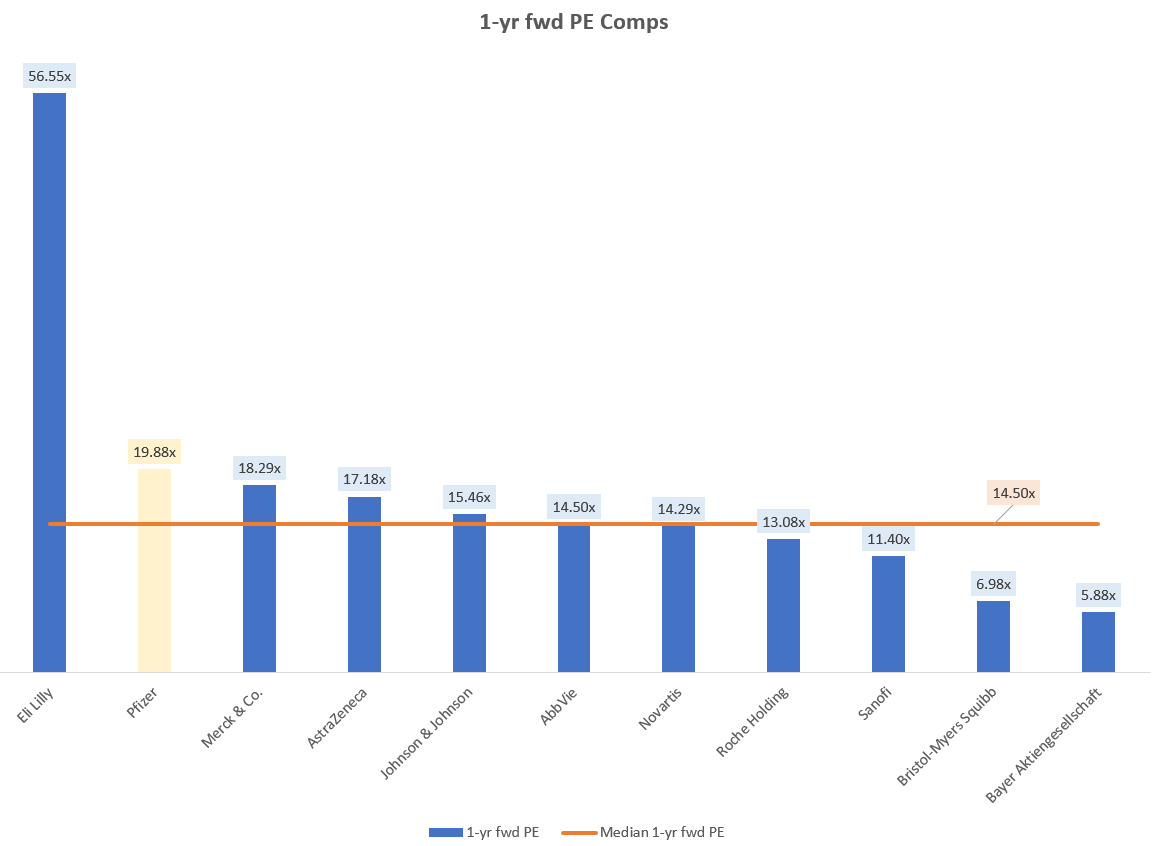

From a comparable valuations’ perspective, Pfizer is comparatively costlier than its friends, as it’s buying and selling at a 37% premium to the median PE of 14.50x:

1-yr fwd PE Comps (Capital IQ, Writer’s Evaluation)

Peer set consists of Eli Lilly (LLY), Merck & Co. (MRK), AstraZeneca (AZN) (OTCPK:AZNCF), Johnson & Johnson (JNJ), AbbVie (ABBV), Novartis (NVS) (OTCPK:NVSEF), Roche Holding (OTCQX:RHHBY) (OTCQX:RHHBF) (OTCPK:RHHVF), Sanofi (SNY) (OTCPK:SNYNF) (GCVRZ), Bristol Myers Squibb (BMY), Bayer Aktiengesellschaft (OTCPK:BAYZF) (OTCPK:BAYRY)

Contemplating the excessive buy worth danger, the upper comparable valuations do not assist the argument for buys.

Takeaway

Pfizer is attempting onerous to replenish and revive income progress. With the Seagen acquisition, it has made an enormous guess on Oncology. Nonetheless, my evaluation on the M&A purchase order worth patterns and execution monitor file leads me to acknowledge an elevated danger for a capital allocation blunder right here. As M&A within the pharmaceutical sector is anticipated to develop in 2024, I fear that Pfizer could make extra dangerous offers. The inventory can also be not buying and selling at an enormous low cost relative to sector median multiples, decreasing the margin of security. Therefore, I’m reluctant to purchase proper now. I say let administration show that they’ll meet the income and margin milestones for the Seagen enterprise. That may encourage extra confidence for contemplating preliminary buys.

Ranking: ‘Impartial/Maintain’

Easy methods to interpret Looking Alpha’s scores:

Sturdy Purchase: Anticipate the corporate to outperform the S&P500 on a complete shareholder return foundation, with larger than typical confidence

Purchase: Anticipate the corporate to outperform the S&P500 on a complete shareholder return foundation

Impartial/maintain: Anticipate the corporate to carry out in-line with the S&P500 on a complete shareholder return foundation

Promote: Anticipate the corporate to underperform the S&P500 on a complete shareholder return foundation

Sturdy Promote: Anticipate the corporate to underperform the S&P500 on a complete shareholder return foundation, with larger than typical confidence