Drew Angerer/Getty Pictures Information

Thesis

I feel Block (NYSE:SQ) has an excellent plan to right-size their price construction and pursue development. I’m bullish however ready for some proof of execution momentum earlier than initiating any buys. My ‘Impartial/Maintain’ stance is after consideration of those key factors:

-

The macros level to blended indicators for top-line restoration

-

Block’s cost-cutting program could make its workforce effectivity extra in-line with friends

-

Block is buying and selling at a reasonable premium vs its friends

Understanding Block’s Enterprise Drivers

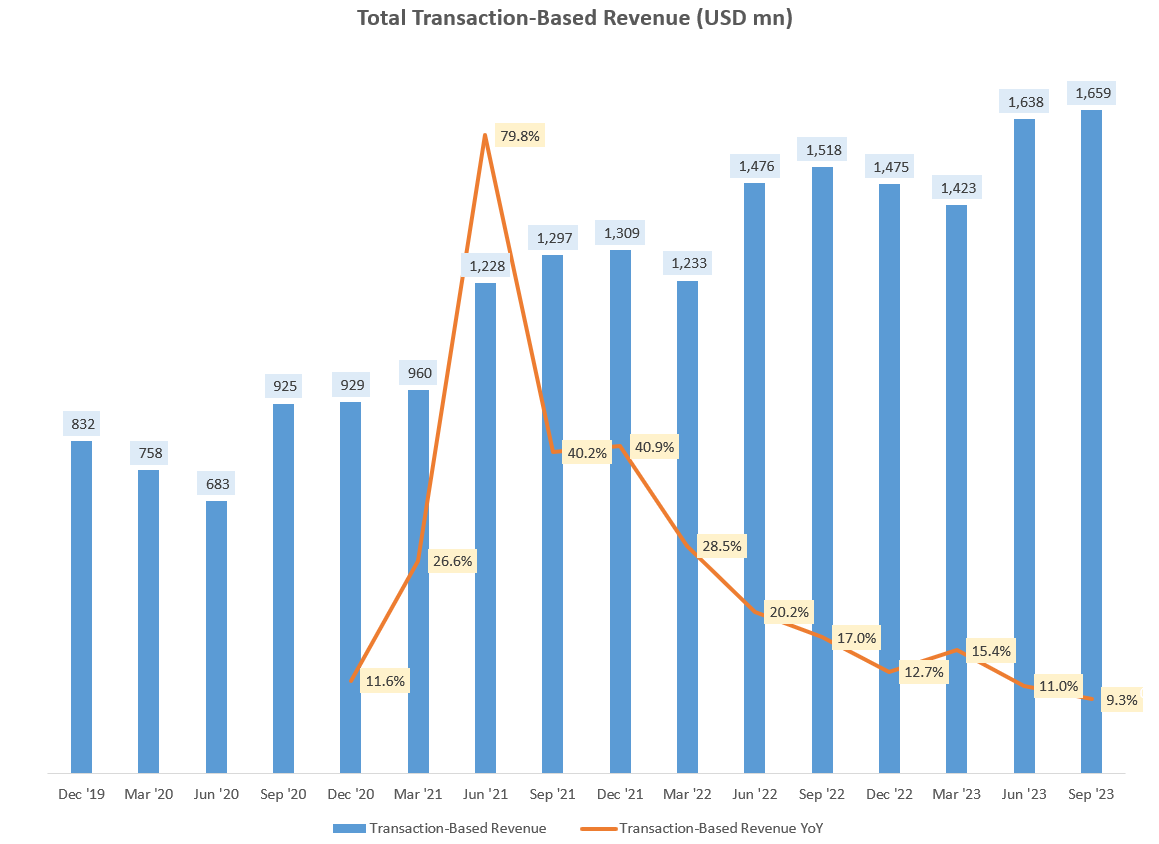

Complete Transaction-Primarily based Income (USD mn) (Firm Filings, Creator’s Evaluation)

Block’s transaction revenues have seen a pointy development moderation from 40% YoY ranges to sub-10% as of Q3 FY23. Transaction income make up round 30% and 35% of the general income and gross revenue combine respectively. I might say it’s the 2nd highest high quality income after Subscription and Providers (which is rising handsomely at a 25%+ YoY development charge; no points there).

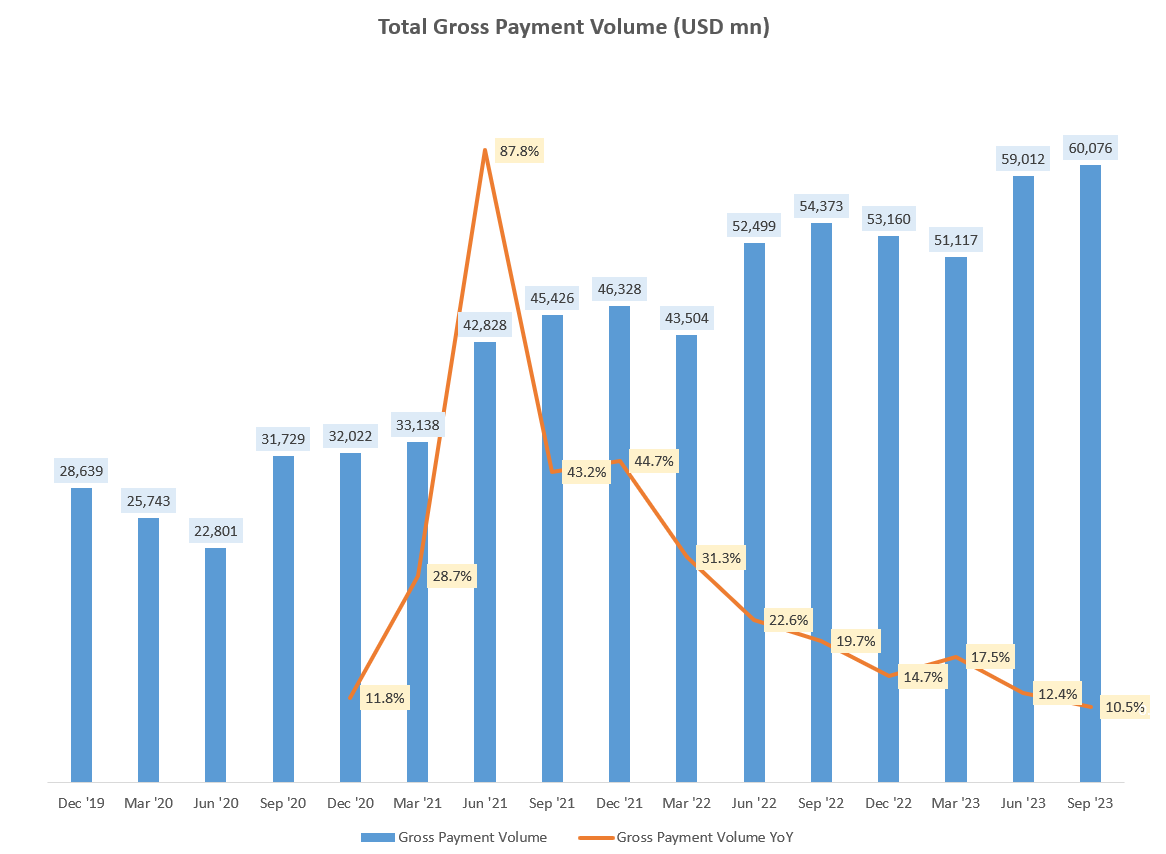

Complete Gross Cost Quantity (USD mn) (Firm Filings, Creator’s Evaluation)

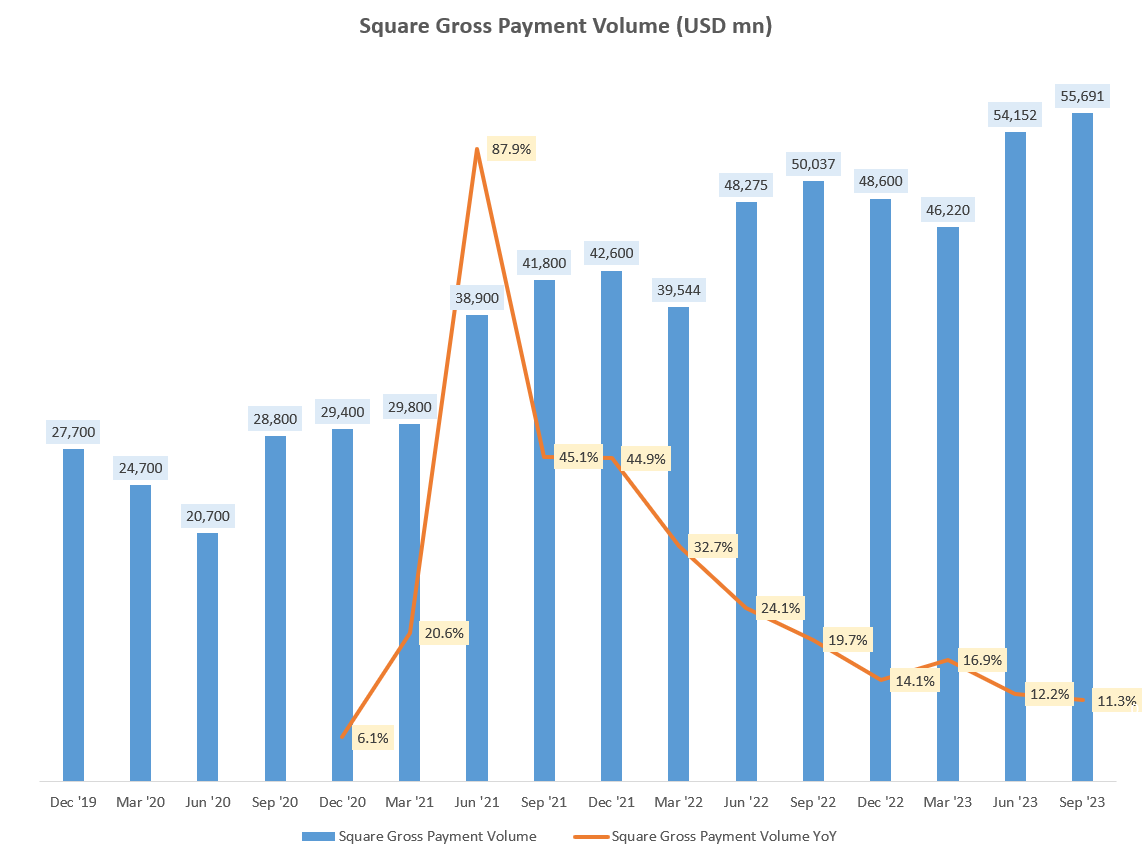

The steep deceleration in transaction income development is attributed to whole gross cost volumes (GPV), which has seen an analogous fall from 30-40% YoY development charges to round 10% ranges as of the newest quarter. Transaction take charges have remained secure within the excessive 2.7-2.8% vary. GPV development has proven an analogous decelerating profile in each the merchant-facing Sq. enterprise (which makes up virtually 93% of whole GPV):

Sq. Gross Cost Quantity (USD mn) (Firm Filings, Creator’s Evaluation)

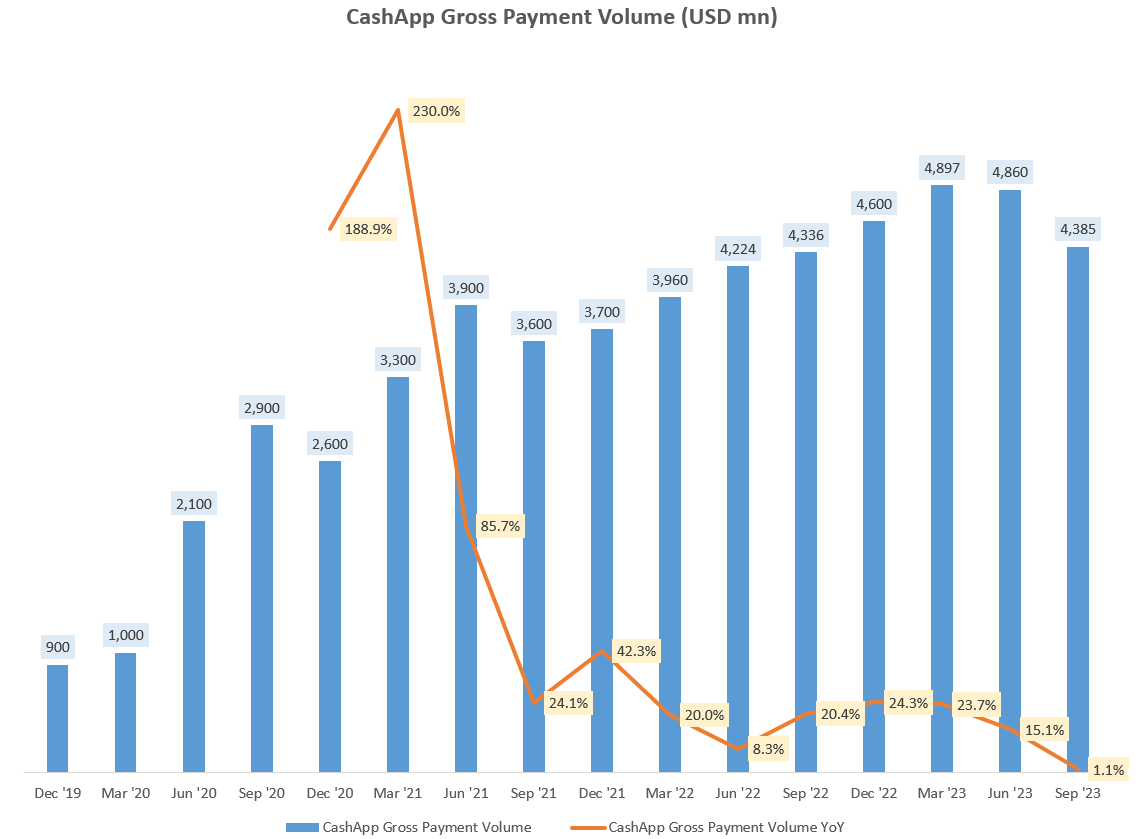

And in addition the consumer-facing CashApp enterprise:

CashApp Gross Cost Quantity (USD mn) (Firm Filings, Creator’s Evaluation)

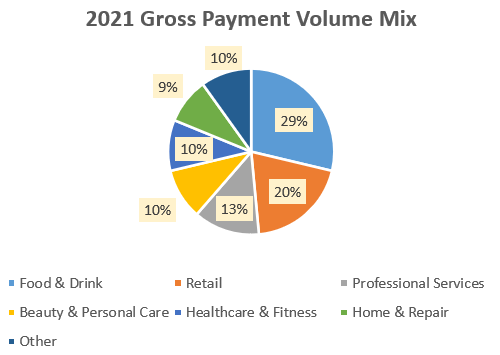

Block’s 2021 Gross Cost Quantity Combine (Statista, Creator’s Evaluation)

As you possibly can see above, virtually 60% of Block’s GPV is comprised of the meals and beverage, magnificence and different retail classes. The important thing level is that Block’s GPV may be very aligned to the efficiency of the US Retail sector, notably the discretionary-spending facet as they do not serve client staples classes equivalent to groceries and gas. The info for this combine is a bit dated as it’s from 2021. Nonetheless, the combination and focus verticals for the corporate has not materially modified. For instance, administration lately highlighted:

We’ll prioritize two verticals, specifically, meals and beverage. And in addition companies equivalent to magnificence.

– Co-Founder Jack Dorsey within the Q3 FY23 earnings call

In actual fact, administration has a technique to go deeper inside these focus verticals, focusing on bigger franchises:

Franchise and multi-entity sellers are key to our upmarket technique as they often use extra merchandise and generate better gross revenue than non-franchise sellers.

– Block’s Q3 FY23 Shareholder letter

The macros level to blended indicators for top-line restoration

I consider US macroeconomic knowledge releases equivalent to Client Sentiment and Retail Gross sales give us main indications of Block’s GPV and Transaction Revenues outlook. Administration has validated the concept that the macro traits have an effect on their enterprise within the newest earnings name:

Now we expect the same-store development, the slowdown there’s comparatively consistent with broader macro traits throughout discretionary verticals… Once you take a look at GPV per vendor, that is the place we consider the latest moderation we have seen has been macro-related.– processing volumes at current sellers had been decrease within the third quarter in comparison with the prior 12 months. We consider it is macro-driven because the latest outcomes of monitor directionally with different third-party spend indicators that we measure after we modify for our mixture of verticals given our better mixture of discretionary spend.

– COO and CFO Amrita Ahuja within the Q3 FY23 earnings name, Creator’s bolded highlights

US knowledge is most related for Block as a result of this geography is chargeable for 93% of general revenues.

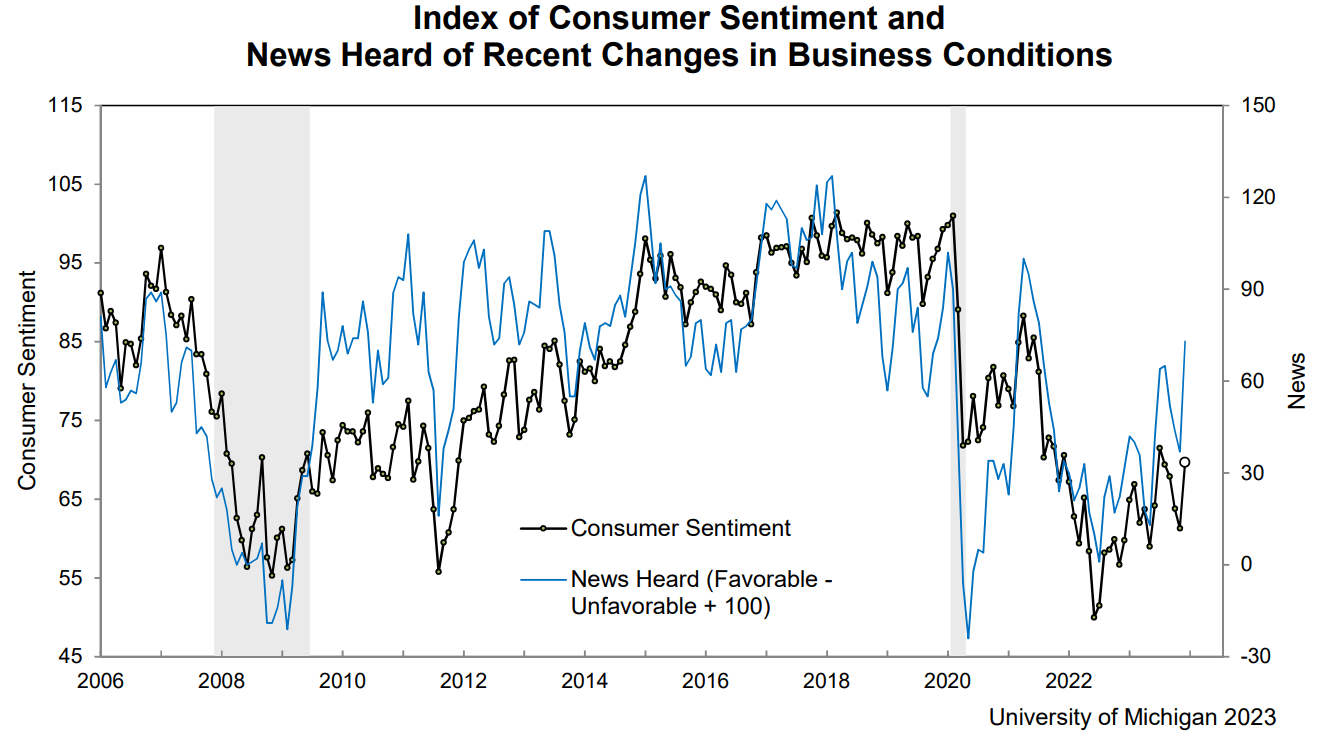

Index of Client Sentiment (College of Michigan Client Sentiment)

Client Sentiment is clearly rebounding very strongly in keeping with the College of Michigan Client Sentiment Index. In December 2023, it printed 69.7 in comparison with 61.3 within the month prior. Noteworthily, the index of Client Expectations additionally went up very strongly from 56.8 in November 2023 to 67.4 in December 2023. This means buoyant Client Exercise, which is pertinent and bullish for Block as it’s finally a B2C enterprise (even its B2B Retailers enterprise Sq.’s exercise is very depending on end-consumer habits).

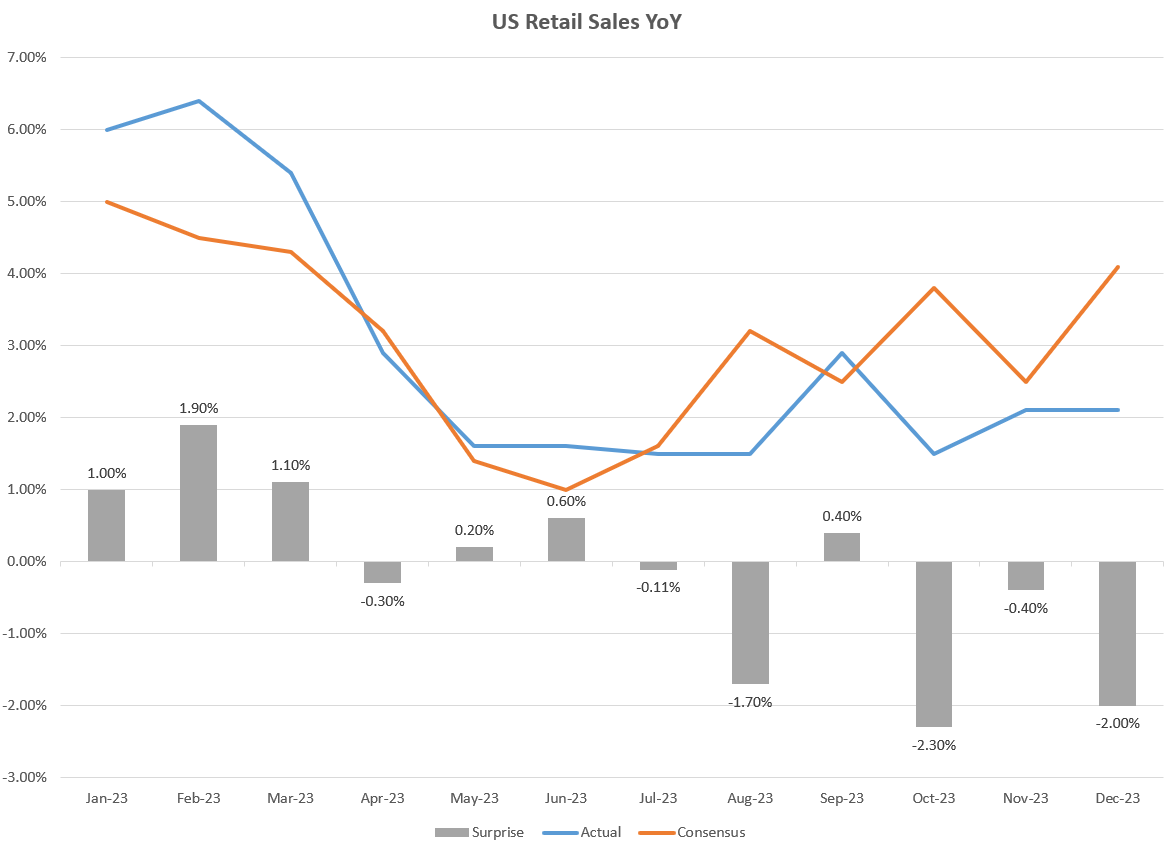

US Retail Gross sales YoY (MyFXBook, Creator’s Evaluation)

On the Retail Gross sales facet nevertheless, regardless of consensus expectations anticipating a significant development rebound since H2 FY23 (which appears affordable as Client Sentiment has been exhibiting promise), precise outcomes have for essentially the most half fallen quick, with 3 unfavourable surprises within the final 5 months. On a YoY development foundation, US Retail Gross sales are chugging alongside at an underwhelming 2.00% as of December 2023. Subsequently, this knowledge doesn’t paint an optimistic image for Block’s GPVs.

General, the macros are giving me blended indicators on the main indicators of Block’s GPV efficiency.

Block’s cost-cutting program could make its workforce effectivity extra in-line with friends

As I dug in by each the lens of Sq. and likewise our funding framework, I simply discovered loads of silos, loads of redundancy, loads of type of an absence of need for groups to work collectively.

– Cofounder and Sq. Head Jack Dorsey’s evaluation of the enterprise within the Q3 FY23 earnings name

The numbers affirm Dorsey’s observations:

Present Worker Productiveness (USD) (Firm Filings, Creator’s Evaluation)

Administration revealed that Block at present has a bit greater than 13,000 staff. By way of worker productiveness metrics, Block’s opex (R&D and SG&A prices) per worker is persistently not less than 100% increased than comparable friends – PayPal (PYPL), World Funds (GPN), Shift4 (FOUR) and Toast (TOST). As a small counterpoint, Block makes extra income per worker too. Nonetheless as you possibly can see on the final row within the snapshot above, on a GAAP Gross Revenue – Opex per worker foundation, Block is persistently worse than all its friends besides Toast, which nonetheless must transition towards profitability.

Block administration has an aggressive cost-cutting plan to put off 1,000 staff (7.7% of the overall workforce):

Our cap of 12,000 folks compares to our present measurement of simply over 13,000 folks as of the top of the third quarter. We consider constraining staff measurement will allow us to be more practical in how we drive efficiency and repair of our clients and accountability on our enterprise methods.

COO and CFO Amrita Ahuja within the Q3 FY23 earnings name, Creator’s bolded spotlight.

Let’s run some eventualities to get an concept of how this may have an effect on the bottom-line. If Block managed to ship Q3 FY23 with 12,000 staff as an alternative of 13,000 that might end in a 66% Gross Revenue – Opex per worker productiveness metric. And while this may nonetheless be a bit worse than PayPal, it could examine a bit extra favorably vs friends equivalent to GPN and FOUR:

Worker Productiveness with 1000 fewer staff (Firm Filings, Creator’s Evaluation)

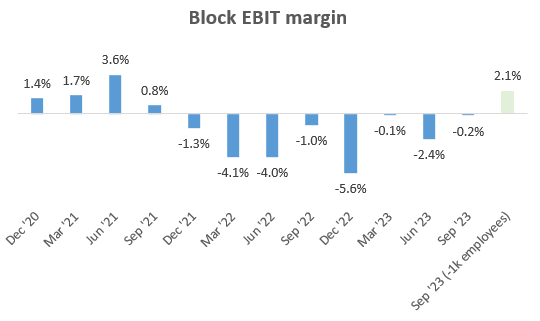

Below the identical state of affairs, Block’s EBIT margins can be +2.1% as an alternative of -0.2% for the newest quarter:

Block EBIT Margins (Firm Filings, Creator’s Evaluation)

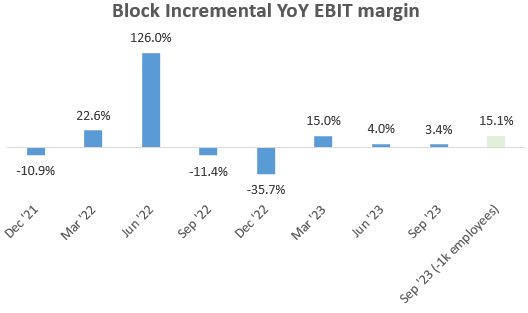

Extra importantly, the incremental YoY EBIT margins can be a lot more healthy at shut to fifteen%:

Block Incremental YoY EBIT Margin (Firm Filings, Creator’s Evaluation)

It is a a lot more healthy margin profile for Block’s type of enterprise. For context, PayPal’s EBIT margin profile hovers round an analogous 15-16% vary. So I feel administration has the precise intentions. And they don’t seem to be doing one thing notably distinctive. 2022 and 2023 already established a playbook for creating significant margin growth through a rationalization of the workforce. For instance, Elon Musk minimize 80% of the workforce at Twitter with none main unfavourable penalties. In his own words:

There have been lots of people that did not appear to have loads of worth. I feel that is true at many Silicon Valley firms. I feel there’s the chance for vital cuts at different firms with out affecting their productiveness, in reality growing their productiveness.

Possibly Dorsey – founder and former head of Twitter – has picked up this playbook from Musk…

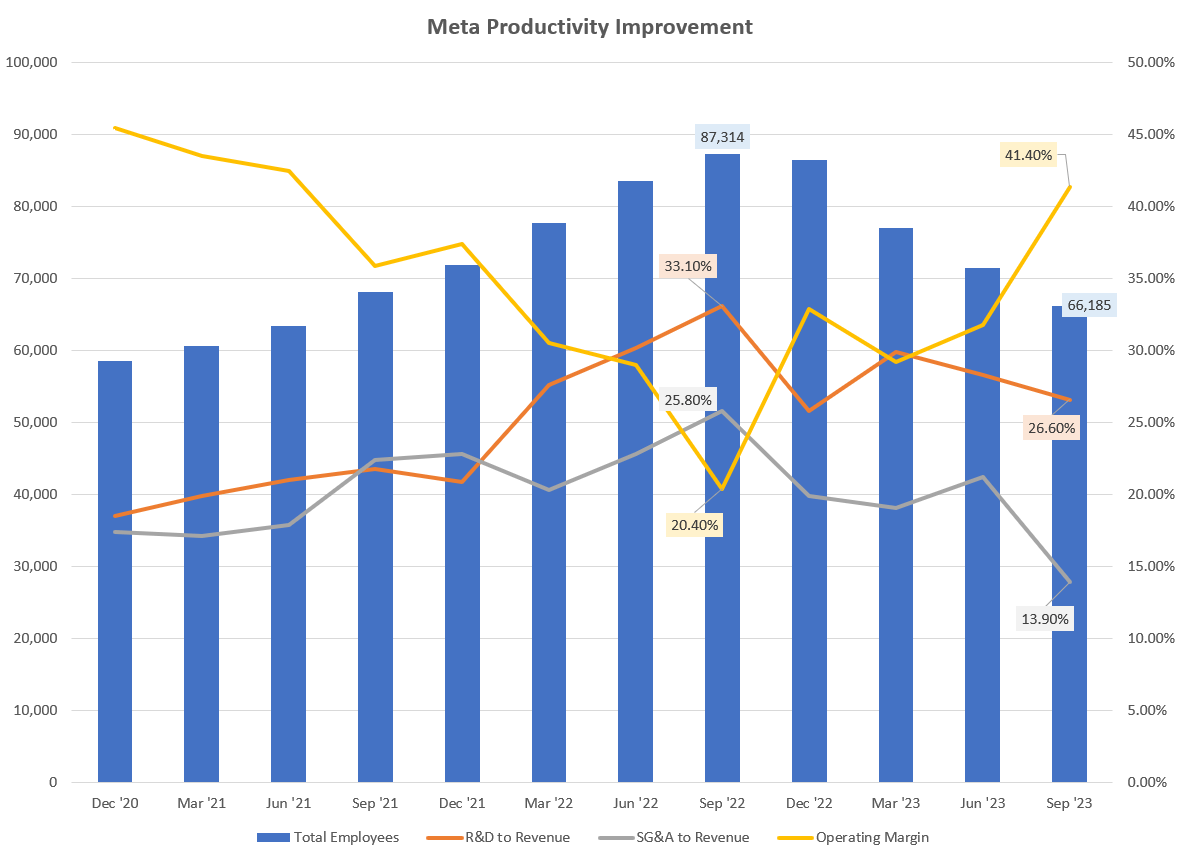

Different expertise firms have efficiently executed this technique too, stunning many analysts (including me) as can been seen in Meta’s (META) productiveness enhance success:

Meta Productiveness Enchancment (Firm Filings, Creator’s Evaluation)

The one query then is whether or not Dorsey and co can play the identical strikes properly to comprehend margin advantages through a leaner Block. One factor to notice about Dorsey’s management fashion is that he prefers selections to be taken by his management group in a real decentralized trend, which is a superb fascination he holds given his give attention to cryptocurrency and decentralized applied sciences. Dorsey apparently doesn’t like selections creeping its strategy to the highest. Nonetheless, some argue that it’s exactly this management fashion that led to slack in his former firm Twitter:

Each time he needed to decide, he stated he noticed it as a “failure” of the enterprise, preferring to permit staffers to thrash out concepts themselves. Nevertheless it was this lack of regular hand and ensuing indecision, his critics argue, that left Twitter suffering from gradual innovation, briefly challenged by activist investor Elliott Administration and finally susceptible to Musk.

Has Dorsey tailored his fashion? Would Block’s administration be capable to efficiently make the corporate extra productive? I feel it is prudent to attend for some indicators of proof right here.

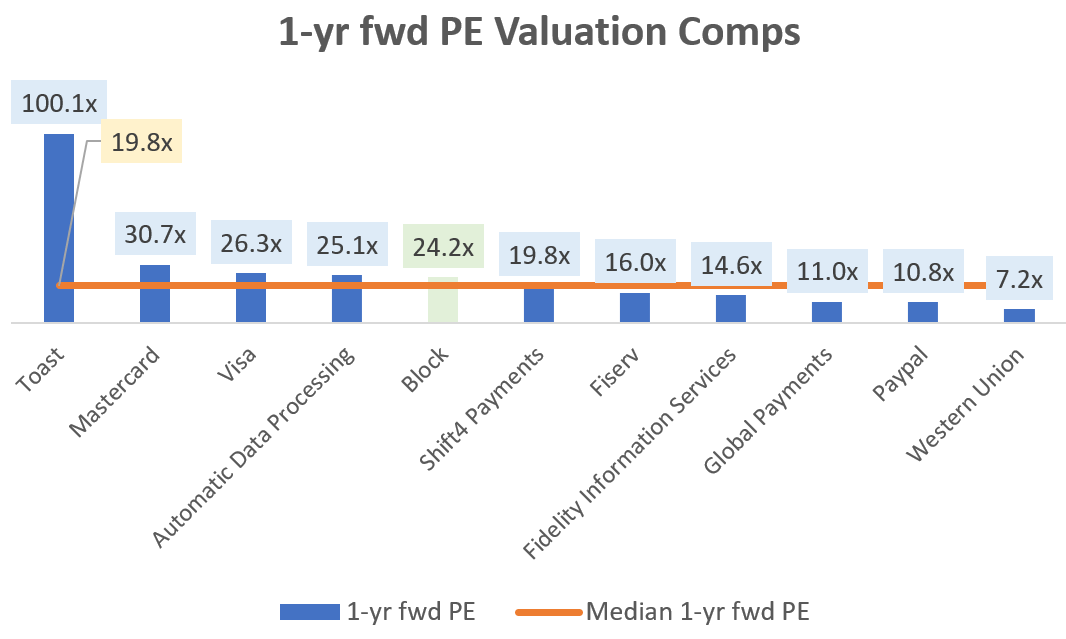

Block is buying and selling at a reasonable premium vs its friends

1-yr fwd PE Comps (Capital IQ, Creator’s Evaluation)

Peerset contains Toast (TOST), Mastercard (MA), Visa (V), Computerized Knowledge Processing (ADP), Shift4 Funds (FOUR), Fiserv (FI), Constancy Nationwide Data Providers (FIS), World Funds (GPN), PayPal (PYPL) and Western Union (WU)

Block is at present buying and selling at a 1-yr fwd PE of 24.2x; a 22% premium above the peer-group median of 19.8x. Given the unclear macro outlook for Block’s top-line and my choice to attend for some proof of execution on administration’s formidable cost-cutting plan, I deem this premium to lack a adequate margin of security for buys.

Takeaway & Positioning

The macro indicators on US Client Sentiment level in the direction of a bullish outlook for Block. Nonetheless, underwhelming US Retail Gross sales knowledge undermine that view. As Block’s transactions enterprise (virtually a 3rd of general revenues and gross income) is linked to customers and retail exercise, this casts doubt on visibility of a development re-acceleration.

On the prices and margins facet, I consider administration has the precise plan to chop virtually 8% of the workforce. My calculations reveal that this may dramatically change the worker productiveness metrics to be extra in-line with friends, and make GAAP-EBIT profitability extra appropriate for a stable fintech enterprise. Block doesn’t have to do something new; Twitter and Meta have already supplied a playbook and set the mannequin for unlocking margin enhancements through workforce rationalization. Nonetheless, Dorsey is thought to be a not-so-hands-on chief; which is critical for driving transformative change. So I consider it’s prudent to first wait and see some progress on Block’s execution of its margin enchancment objectives to realize confidence on a profitable turnaround.

Given this stance, Block’s 22% premium valuations relative to the sector median’s 1-yr fwd PE don’t go away a lot margin of security. Therefore, I charge the inventory a ‘Impartial/Maintain’ for now.

interpret Looking Alpha’s rankings:

Sturdy Purchase: Anticipate the corporate to outperform the S&P500 on a complete shareholder return foundation, with increased than typical confidence

Purchase: Anticipate the corporate to outperform the S&P500 on a complete shareholder return foundation

Impartial/maintain: Anticipate the corporate to carry out in-line with the S&P500 on a complete shareholder return foundation

Promote: Anticipate the corporate to underperform the S&P500 on a complete shareholder return foundation

Sturdy Promote: Anticipate the corporate to underperform the S&P500 on a complete shareholder return foundation, with increased than typical confidence