da-kuk

Expensive readers,

I’ve been pretty bearish on Nvidia (NASDAQ:NVDA) ever because the inventory reached $400 per share, following the unimaginable steering that administration issued of their Q1 2023 earnings name. The rationale has primarily been valuation and a few stage of doubt whether or not the corporate might truly ship on such aggressive steering.

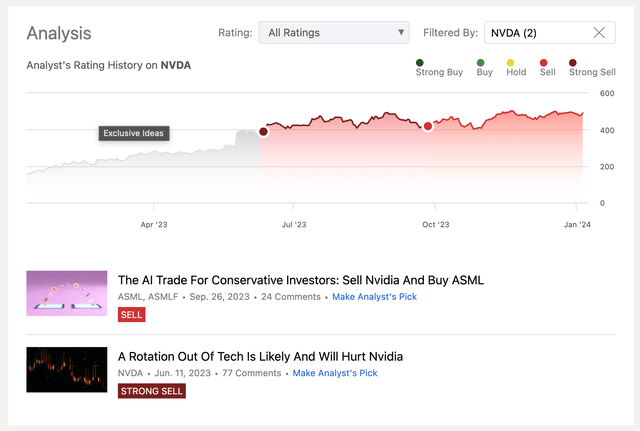

Most not too long ago I revealed an article in September, the place I urged buyers to affix me in a pairs commerce – promoting NVDA and shopping for ASML Holding (ASML). I thought of ASML to be a a lot safer funding on account of a decrease P/E and a a lot much less bold progress forecast. To this point, the commerce has paid off, with ASML returning 24.2%, whereas NVDA has “only” returned 18.8% over the identical interval.

In search of Alpha

Nvidia has surpassed Wall Avenue’s and my expectations

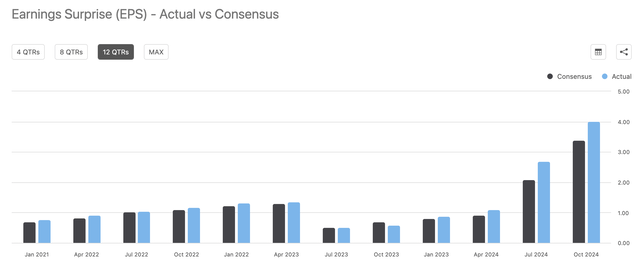

Since these articles, nonetheless, NVDA has revealed extra earnings experiences (most not too long ago Q3 2023) and has constantly beat consensus estimates. And we’re not speaking small beats both as the corporate adopted an 18% beat in Q1 by a 29% beat in Q2 and an 18% beat in Q3.

In search of Alpha

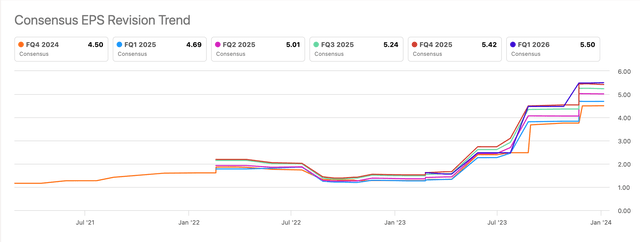

Furthermore, with each earnings launch, administration has upped their ahead steering and analysts have elevated their ahead consensus expectations. Particularly, following the Q2 earnings launch, ahead earnings expectations have elevated by about 60%. Extra not too long ago, following the Q3 outcomes announcement, they jumped by extra 20%.

In search of Alpha

As a result of NVDA’s earnings have grown so quick, the inventory not trades at 50x 2023e earnings because it did once I wrote my first article. The truth is the P/E relative to 2023e earnings has dropped to 39x.

And whereas that is nonetheless excessive, if we glance out one yr and assume that NVDA will ship on the consensus forecast for 2024 of extra 66% progress, the ahead P/E stands at simply 25x. That is considerably under ASML’s ahead P/E of 34x and a discount for an organization of NVDA’s caliber.

As a result of NVDA has been in a position to ship vital optimistic EPS surprises in Q2 and Q3, my conviction that NVDA will attain the bold forecast EPS of $20 per share subsequent yr has elevated considerably. I am removed from leaping all in right here, however I’ve to confess that my head has turned a little bit bit on NVDA.

Key threat elements

There are a number of elements that may decide whether or not NVDA hits the 2024 forecast and extra importantly what occurs to earnings past, these are:

1 – Demand for chips

There isn’t any doubt that NVDA’s chips are second to none in the case of coaching AI fashions. That is why they’ve a virtually 90% market share. However there’s a fear that the latest hype has led NVDA’s clients to over-order effectively over their short-term wants to ensure they’ve the GPUs wanted for initiatives sooner or later. Whereas the precise influence of that is laborious to estimate, if it’s the case, then NVDA might see a lot decrease earnings progress post-2024 and earnings would possibly even decline considerably which might make the ahead P/E relative to 2024e skewed to the draw back.

2 – Competitors

AI is the speak on the town proper now and understandably competitors will attempt to seize a few of NVDA’s market share which is more likely to put stress on NVDA’s trade main margins. Superior Micro Gadgets (AMD) is more likely to be robust contender with their Mi300x chip and most large tech corporations, together with Alphabet (GOOGL) and Microsoft (MSFT) have already introduced that they are going to be creating their very own chips.

Foremost Avenue Knowledge

3 – Use circumstances for AI

One of many greatest deciding elements for NVDA’s future earnings will probably be precise AI use circumstances. This can decide if the latest hype has been a bubble or the true factor. Over the course of final yr, the variety of viable use circumstances has surpassed 100. As we enter 2024, it is going to be fascinating to see corporations speak about methods to implement AI into their course of to drive extra profitability and it is going to be much more necessary to see these beginning to be carried out. It is too early to inform which method it should go, but it surely sounds believable that AI might result in considerably greater productiveness and earnings. Furthermore, information facilities give a strong indication that corporations are on the brink of launch their AI purposes, as capability demand at most information facilities has been robust currently.

4 – Geopolitical dangers

AI might be very highly effective and subsequently international locations are understandably preventing to maintain it inside their very own borders. Nowhere is that this extra evident that the tensions between the U.S. and China. The U.S. authorities prohibited chip corporations, together with Nvidia, from exporting cutting-edge know-how chips to China. That is clearly not good for enterprise, however identical to AMD with their RX7900 chip, Nvidia has been engaged on designing a barely weaker chip particularly for the Chinese language market. Whereas the danger is tough to disregard, it isn’t a dealbreaker for my part, particularly if you happen to consider that AI and its use circumstances are going to drive huge productiveness enhancements.

Backside line

Evaluating Nvidia is hard, as a result of the choice whether or not to purchase depends upon your view of future earnings, particularly past 2025. I used to be skeptical at first that the corporate might not ship on the 2023 and 2024 forecast, however following robust earnings beats and elevated steering and consensus on each name in 2023, I’ve grown extra bullish.

I do consider that AI will permit for a lot of helpful use circumstances, however I do see over-ordering as an actual threat to earnings past 2024. In consequence, I do not suppose buyers ought to put an excessive amount of weight on the ahead P/E of 25x, as a result of it might rise subsequent yr if actually it turns into clear that over-ordering was a difficulty.

Because of this, I am no able to challenge a BUY ranking on Nvidia, however I do improve the inventory to a HOLD for the explanations mentioned and I will probably be watching This fall 2023 outcomes carefully on February 21 to verify my view that the corporate can ship on its bold forecast.