Editor’s word: In search of Alpha is proud to welcome Akim Guerreiro as a brand new contributor. It is easy to turn out to be a In search of Alpha contributor and earn cash in your greatest funding concepts. Energetic contributors additionally get free entry to SA Premium. Click here to find out more »

Wachiwit

Enterprise Overview And Current Modifications

Tripadvisor, Inc. (NASDAQ:TRIP) is an American on-line journey firm that operates in all the spectrum of journey steering: lodging, eating places, experiences, airways, cruises together with internet hosting tons of of hundreds of thousands of travellers’ evaluations and 1000’s of dialogue blogs on its platform. The corporate is applied in 48 nations and 28 languages, and continues increasing yearly. The corporate was based in 2000, with the rise of the web, giving it an vital first-mover benefit.

And but, I’m not overly bullish within the short-term on the inventory. Certainly, Tripadvisor has been struggling to return to a path of excessive development: the income in 2022 was at the very same degree because the 2015 income ($1.49 billion). It is on this context that Matt Goldberg stepped in as CEO to try to flip round this journey gem again to a path of excessive development. The medium-term to long-term narrative could also be completely different and will make as we speak’s entry worth (roughly $20 per share) a lovely alternative for the following 3 to five years.

Funding Thesis – The Resurgence of a Firm and its (Low cost) Inventory

Is 2024 the 12 months for a resurgence of this tech firm? I do see huge upside with restricted draw back for the inventory, however the traders shopping for into it should be affected person – actually affected person. I fee the inventory as a Sturdy Purchase that would materialize in a stable return within the subsequent 3 to five years. Certainly, with the latest change in administration with a brand new CEO changing the previous co-founder CEO and the improved monetary efficiency, the corporate appears to be again on double digits’ development in income and in EBITDA.

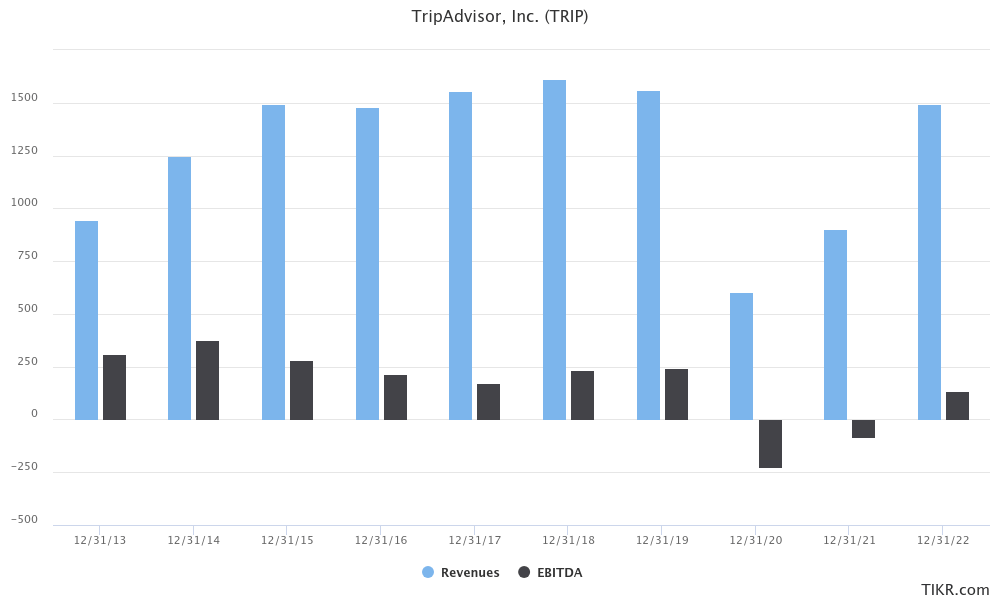

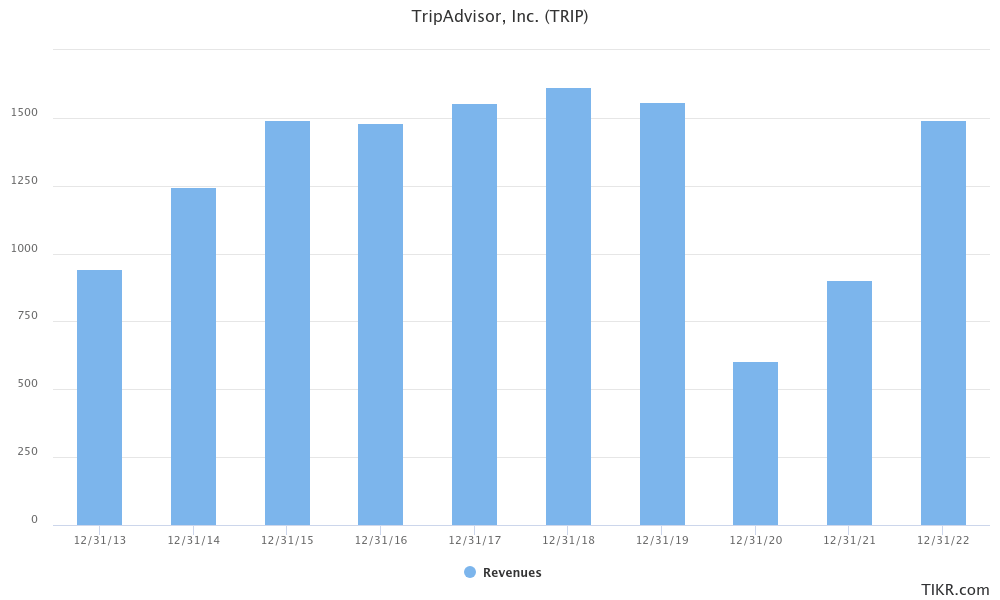

Certainly, Income Development Has Stalled

Tripadvisor was on a path of double digits’ development till the tip of 2015, when basically the corporate reached the glass ceiling of the segments it operates in.

www.tikr.com

EBITDA has struggled to indicate any development development since 2014, and it has been declining ever since. The best way I see it, the big quantity of layoffs induced by the covid market setting in 2020 (25% of the workers was minimize that 12 months alone) may treatment an inert EBITDA development and increase the inventory valuation.

www.tikr.com

After I take a look at the final quarters, the corporate is wanting more and more enticing with an EBITDA development development seeming to emerge, particularly because the arrival of the brand new CEO in Q1 of 2022 (extra on that later on this article).

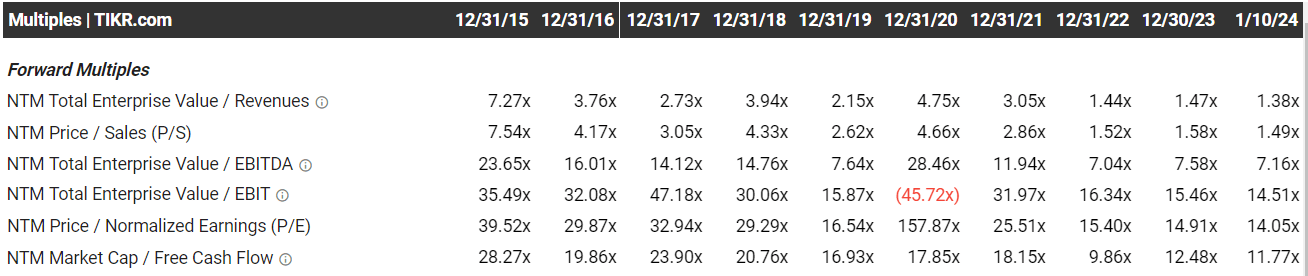

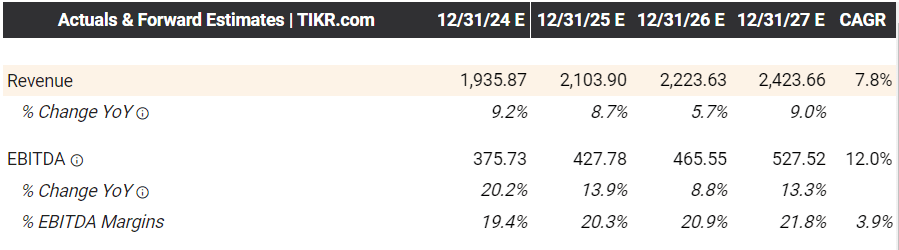

Valuation & Estimates Present The Inventory Is Actually Low cost Now

From the valuation perspective, I imagine we’re proper within the candy spot. The valuation is effectively beneath historic ranges, discounted for the previous couple of years of covid-related drop in income, and it has not captured but the latest quarters’ development regardless of exhibiting indicators of pick-up (the inventory worth elevated by +17% within the final 6 months).

www.tikr.com

By virtually each forward-looking metric, the inventory is a robust purchase now. It even acquired extra enticing after the primary buying and selling days of the 12 months because of an total tech-led drop of a few p.c. Evaluating with

Booking Holdings Inc. (BKNG) utilizing Seeking Alpha’s comparison tool, a a lot bigger competitor that has already had its personal effectivity turnaround a number of years again, Tripadvisor is buying and selling at a big low cost. The place Tripadvisor trades at a ahead 7.16x EV/EBITDA, Reserving Holdings is buying and selling at a ahead 17.34x. Moreover, based mostly on the median observed in the worldwide software sector, shares had been buying and selling in 2023 at round 15.88x. If Tripadvisor is ready to persuade the markets that it’s on a turnaround monitor, the inventory may commerce at round $40-50 in 2-3 years time in keeping with the market multiples above – if EBITDA’s double digits’ development is confirmed and the corporate reinvents itself into an modern software program firm, which was what the corporate was about when it was based in 2000 with the rise of the web.

One more reason I imagine we’re as we speak within the candy spot is as a result of the traders, maybe nonetheless shaken from the covid crash, haven’t taken but under consideration a budget valuation in relation to the estimated income development and, maybe extra curiously, the EBITDA development outperforming income development.

www.tikr.com

This outperformance of EBITDA in relation to income development may point out the corporate is on monitor to elevated effectivity, and doubtless it has one thing to do with the brand new senior administration modifications.

The time hole between previous financials, future estimates and delayed market response is precisely the place the alpha resides. That is for me motive sufficient to purchase the inventory now and to carry it for 3 to five years.

New Administration, New Hope?

In my view, Administration lead by the co-founder Stephen Kaufer acquired too comfy within the previous methods (he declared “we got too comfortable” already in 2014) and has failed to grasp that an organization has to reinvent itself and innovate when income development stalls (except it is as a result of macro setting). The newest covid debacle with 900 layoffs in 2020, the 2020 sale of a number of Tripadvisor-held manufacturers to Hopjump and the restrictions from the Chinese language authorities on the app have all led traders to panic, and the inventory worth reached an all-time low in 2023.

And but, I feel the inventory is a purchase. The change in senior administration with Matt Goldberg as CEO since 2022 is what the corporate wanted already since 2016. Matt Goldberg is an unique choose within the sense that he has not constructed his profession in Tripadvisor, and his expertise is for essentially the most half in segments resembling commercial (The Commerce Desk (TTD)) and on-line purchasing (Qurate (QRTEA)). And these experiences from the CEO may assist Tripadvisor to faucet untapped income development pockets. It’s no coincidence that the corporate has proven a median YoY development of 42% per quarter because the arrival of the brand new CEO, albeit it might be powered by a catch-up impact on the covid years’ drop. Apparently, the layoffs in 2020 might be useful as the corporate is basically compelled again into effectivity with out the brand new CEO needing to do the worst a part of the function. Time will inform if the corporate is again on monitor to a double digits’ development.

Danger Elements And What Might Make It Lose My Sturdy Purchase Ranking

The principle dangers I see that would make me reassess the Sturdy Purchase Ranking is synthetic intelligence (AI) and the brand new CEO’s efficiency over time. As proven on this article printed on In search of Alpha, AI might be an unlimited enhancer for on-line journey corporations to faucet new sources of income by integrating the expertise in enhancing the journey reserving expertise, making it a a lot smoother course of for the patron, and in concentrating on advertisements in a greater method. Ought to Tripadvisor fail to combine the brand new AI developments in its ecosystem, it may trigger it to lag behind its important opponents for some time longer. Moreover, if the brand new CEO fails to persuade current traders that Tripadvisor is again to development and never solely catching up from the covid interval, the markets may hand over on the inventory. The following couple of quarters shall be decisive to exhibit that the uptrend is certainly actual.

Backside Line

After difficult years because of covid and an previous administration workforce led by the co-founder since 2000, Tripadvisor had lacked innovation and effectivity. Income had stalled and EBITDA had turned unfavourable.

However with the brand new CEO since early 2022, a development development appears to emerge, and a return to double digits income and earnings development appears within the playing cards for the following couple of years.

The valuation has not but mirrored the turnaround, and the markets have but to choose up on this chance. The celebs are actually in alignment for the inventory to outperform the market.

The inventory is unquestionably a lovely play in a portfolio that desires to have elevated publicity in each the journey and the tech sectors, and it’s appropriate for each development and worth traders at this time limit.