Juan Jose Napuri

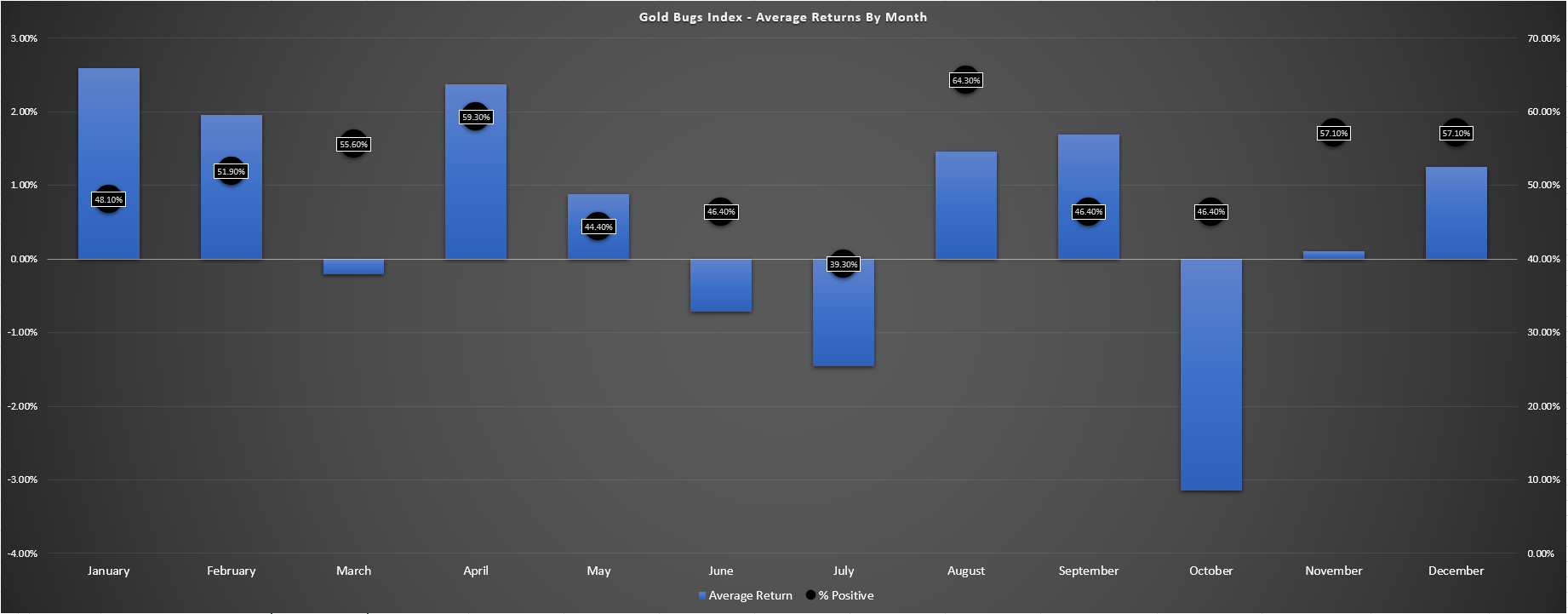

It has been a tough begin to the 12 months for the Gold Miners Index (GDX) in what’s sometimes one of the best month of the 12 months from a seasonal standpoint, with a mean return for the sector of ~2.6% in January over the previous 30 years. That is definitely disappointing for buyers, particularly with the gold worth registering a document seven weekly closes above the $2,000/ozlevel. The underperformance for miners will be defined by continued unfavourable sentiment, and even Lundin Gold’s (OTCQX:LUGDF) vital beat vs. annual steerage introduced in its This fall/FY2022 outcomes hasn’t helped the inventory to crawl out unfavourable territory year-to-date. Actually, Lundin has underperformed the peer group, down 300 foundation factors year-to-date vs. the GDX. On this replace we’ll dig into the This fall outcomes, current developments and its three-year outlook, and the place the inventory’s up to date purchase zone lies:

Gold Bugs Index – Common Return & % Of Time Constructive – Creator’s Knowledge & Chart (Gold Bugs Index – Common Return & % Of Time Constructive – Creator’s Knowledge & Chart)

This fall & FY2023 Manufacturing Outcomes

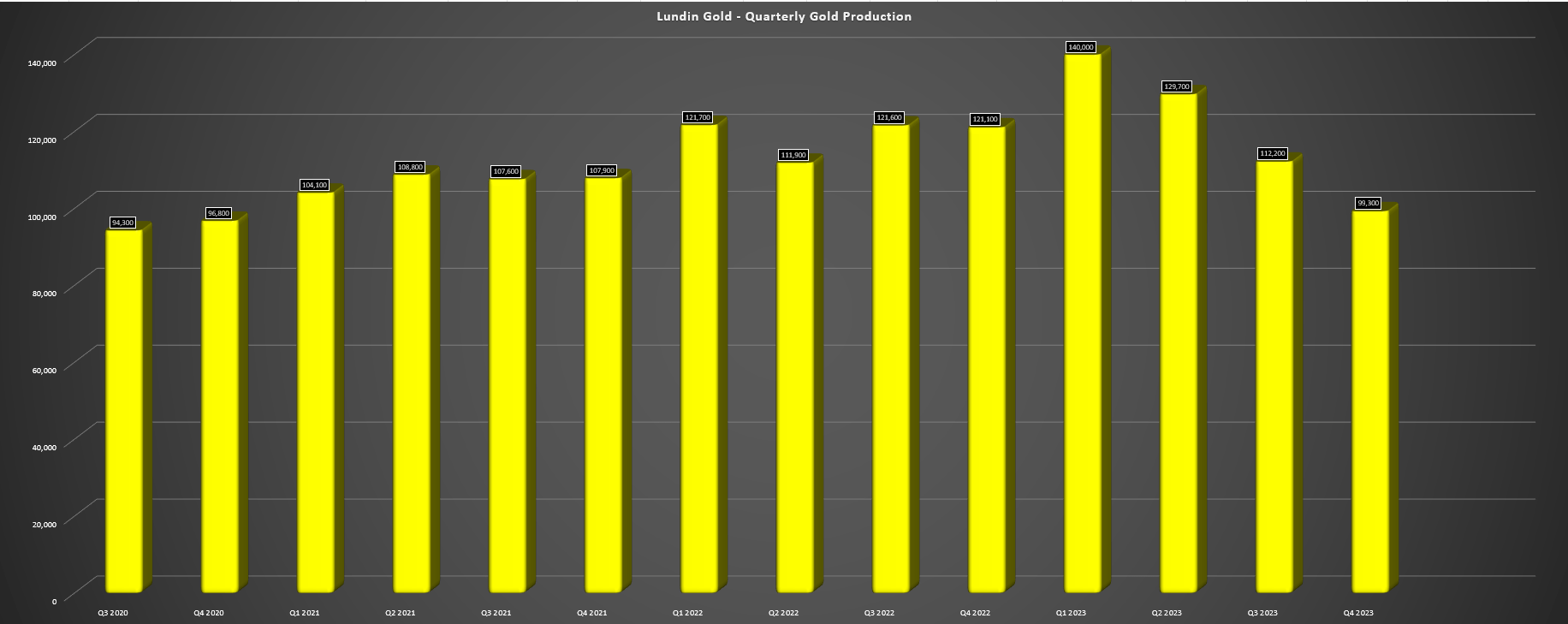

Lundin Gold launched its preliminary This fall and FY2022 outcomes earlier this month, reporting quarterly manufacturing of ~99,300 ounces, an 18% decline from the year-ago interval. Nevertheless, whereas this headline quantity may not appear that thrilling, it is necessary to notice that Lundin was lapping robust comps from the year-ago interval with a mean grade of 10.0 grams per tonne of gold (13% above its common reserve grade of 8.7 G/T), and one among its greatest manufacturing quarters of ~121,100 ounces, along with the advantage of greater recoveries. Therefore, there was no shock that Lundin noticed decrease output year-over-year. Nonetheless, 2023 was one other blowout 12 months general with manufacturing beating the already upward revised steerage midpoint of ~468,000 ounces, coming in at a brand new document of ~481,300 ounces, and smashing preliminary FY2023 steerage of 450,000 ounces.

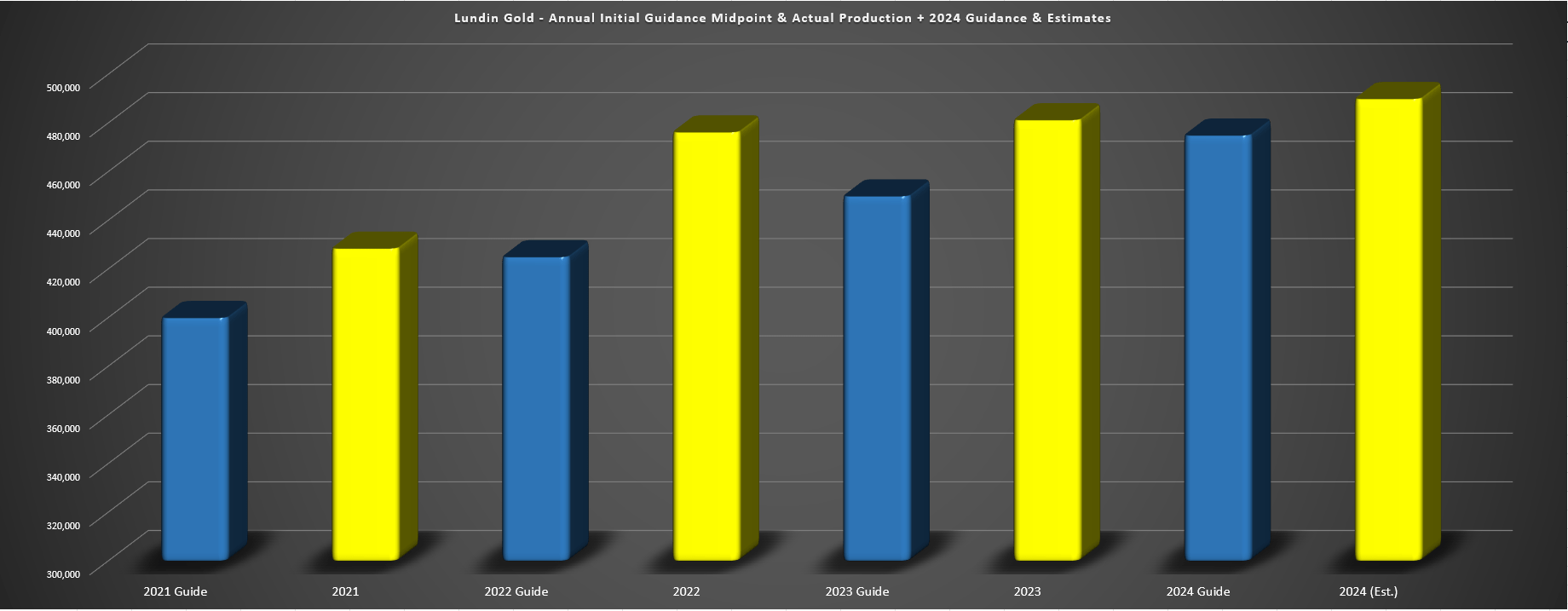

Lundin Gold Quarterly Manufacturing – Firm Filings, Creator’s Chart Lundin Gold Annual Preliminary Steering Midpoint vs. Precise Manufacturing + 2024 Steering/Estimates – Firm Filings, Creator’s Chart & Estimates

Actually, if we have a look at how Lundin Gold has carried out the previous three years, the corporate has a close to unequalled observe document of efficiency relative to steerage, with this being much like Kirkland Lake Gold within the Swan Zone days when it persistently over-delivered on guarantees. That is evidenced by the chart above which exhibits that Lundin Gold has overwhelmed its steerage midpoint by a mean of ~37,000 ounces over the previous three years and a median of ~31,000 ounces.

So, what occurred in This fall with the decrease manufacturing?

Whereas throughput was up year-over-year to ~427,700 tonnes, grades got here in beneath its common reserve grade at 8.2 grams per tonne of gold and recoveries had been additionally barely beneath nameplate at ~88.1%. This resulted in a major decline in output vs. ~420,800 tonnes at 10.0 grams per tonne of gold and 150 foundation level greater recoveries in This fall 2022, however full-year manufacturing benefited from greater throughput and high-grade stockpiles in Q1 with a 1.1% enhance in gold manufacturing year-over-year regardless of weaker recoveries. Nonetheless, if the corporate can keep its sample of over-delivery and even carry out at half of the median beat (~15,000 ounces), Lundin ought to see manufacturing are available nearer to 490,000 ounces this 12 months which might mark one other document 12 months for the corporate.

2024 & Three-Yr Outlook

Trying on the 2024 outlook and its up to date three-year outlook, Lundin has guided for 475,000 ounces on the mid-point in 2024 at industry-leading all-in sustaining prices of $820/ozto $890/oz. Nevertheless, Lundin has sometimes delivered beneath its value steerage mid-point as effectively, suggesting we’re prone to see one other 12 months of $1,100/oz+ all-in sustaining value [AISC] margins with AISC prone to are available at or beneath $850/oz. And whereas manufacturing ought to see a slight tick up year-over-year to my estimates of ~490,000 ounces, 2025/2026 manufacturing ought to transfer even greater to 500,000+ ounces every year primarily based on optimization work set to be accomplished this 12 months at a modest value of ~$36 million.

Digging into these enhancements, Lundin famous that pilot testing of Jameson Cell know-how has yielded optimistic outcomes, and the corporate expects that as a part of its progress plans, it can’t solely ramp as much as 5,000 tonnes per day (~4,500 tonnes per day presently), however ship a 300 foundation level enchancment in recoveries by including three Jameson cells to its operation. If we assume a continuing head grade of 9.0 grams per tonne of gold and a 5,000 tonne per day throughput price, a 3% raise in recoveries would translate to an extra ~15,800 ounces of gold recovered every year or over $30 million in income every year, making this a really excessive return funding.

“Yeah, the pilot work that we did really simulated, the three positions that we’re looking at, putting these, Jameson cells, ones at the head end of the flotation circuit, one sort of in the middle, and then one is at the end and we tried to introduce as much variability into the feed as we could to really understand the performance and so the modeling work that we’ve done and of course Glencore (OTCPK:GLCNF) Technology has taken the results and we’re estimating that we’ll see about a 3% recovery bump once these, Jameson Cells are installed. Based on current schedules, the Jameson Cells are to be in place at the same time as the ramp up to 5000 tons per day anticipated in Q4 next year”.

– Lundin Gold, Q3 2023 Convention Name

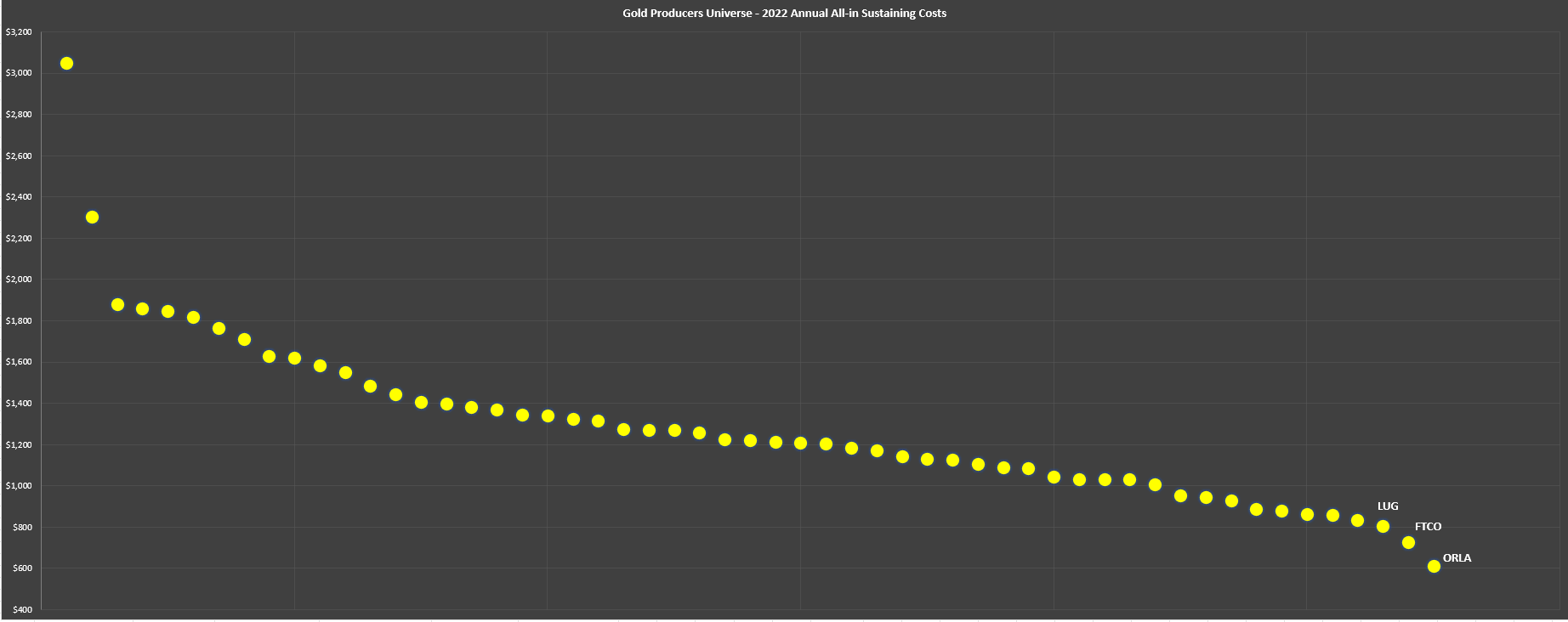

Lastly, as introduced final 12 months, Lundin Gold has authorized an growth to five,000 tonnes per day, and has a busy 12 months of exploration on deck with plans to drill 56,000 meters (near-mine and regional drilling). This elevated manufacturing profile is predicted to depart all-in sustaining prices at industry-leading ranges beneath $900/ozin 2025, they usually may decline to as little as $800/ozin 2026 or over 40% beneath the anticipated {industry} common in FY2026 (~$1,450/oz). General, this can be a vital improve from my earlier outlook that prices may rise with barely decrease manufacturing as grades normalized within the 2026 by means of 2029 interval, with the much less rosy outlook averted due to optimization to drive greater recoveries and throughput. In abstract, Lundin Gold ought to stay a top-5 producer from a margin standpoint with Tier-1 scale over the following a number of years, serving to to keep up a premium a number of vs. its mid-tier friends.

Gold Producers Universe 2022 AISC – Firm Filings, Creator’s Chart

Latest Developments

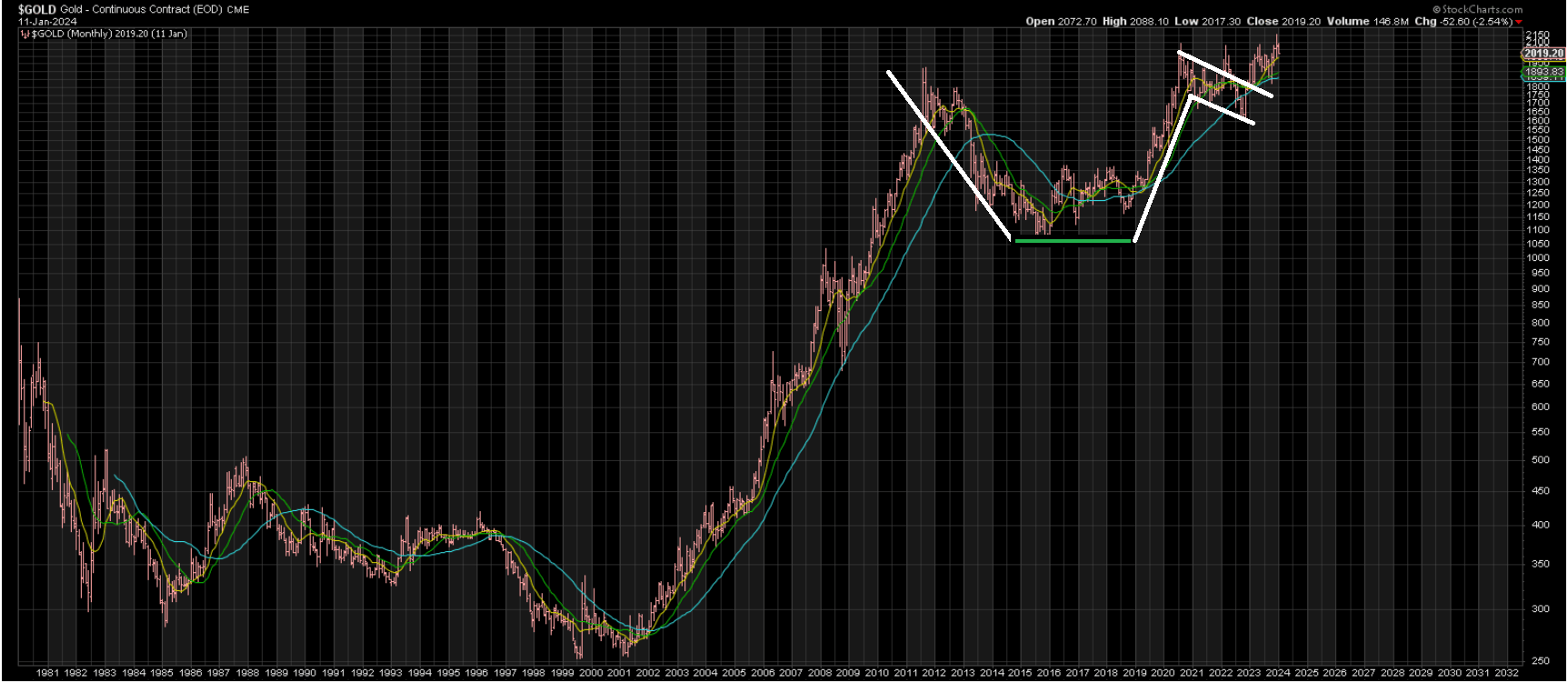

current developments, the energy within the gold worth is definitely a optimistic, with the yellow steel breaking out of an enormous cup & deal with base to new all-time highs in This fall after a false begin in Q1 2022. This definitely advantages Lundin Gold’s common realized promoting worth which ought to are available above $2,030/ozin Q1, up ~4% from its common realized promoting worth of $1,958/ozlast 12 months. This could profit Lundin’s margins that are anticipated to stay above 50% once more in 2024, and may ultimately translate into greater share costs for gold miners which have continued to commerce at comparatively depressed multiples in comparison with the place they’ve beforehand with gold sitting atop the $2,000/ozlevel. Simply as importantly, that is the most important breakout amongst any asset lessons in years, and breakouts of this magnitude (if confirmed) sometimes result in multi-year uptrends.

Gold 40 Yr Chart – StockCharts.com

Actually, the final main cup-style breakout in gold occurred from 1996 to 2005, with gold marching greater for one more six years and greater than doubling within the interval. Clearly, historical past would not need to repeat itself and there is no assure that gold triples this time round (not to mention beneficial properties 50%) however that is definitely one of the best that gold has appeared in years from a technical standpoint, suggesting that some publicity to the best-run gold miners is sensible. Plus, whereas there is no finish to the criticism about miners’ margins, an additional transfer greater within the gold worth would definitely offset almost the entire value creep we have seen from unprecedented inflation, serving to even the extra marginal miners generate optimistic free money stream and meaningfully growing the free money stream yield for the GDX (on prime of an already very enticing ~2.8% common dividend yield on million-ounce producers relative to previous cycles).

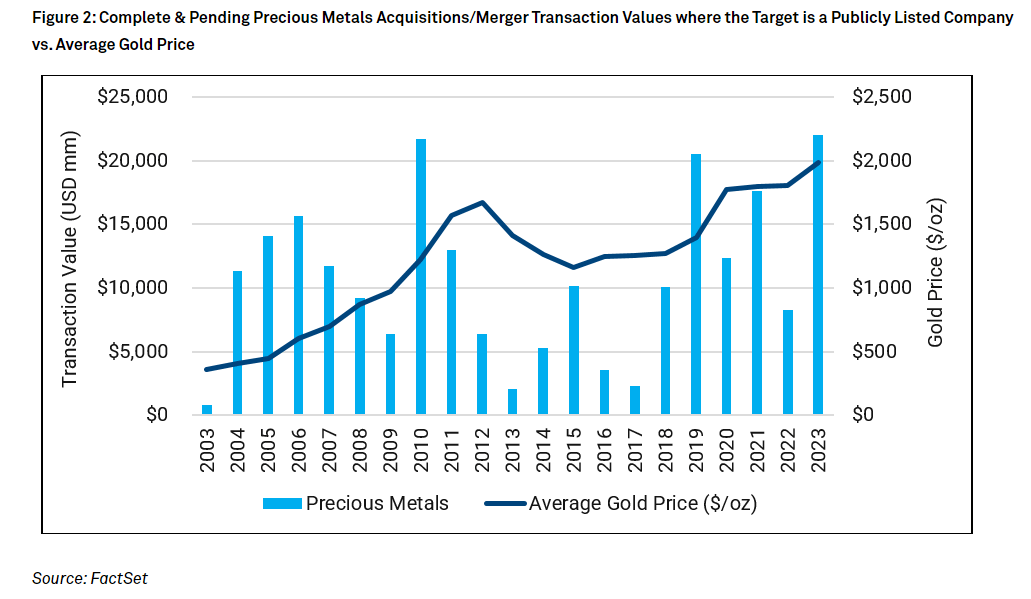

As for Lundin’s capital allocation and enterprise growth, the corporate has mentioned that it will have a look at M&A throughout previous calls, together with at its current Investor Day Presentation. And, given the openness to M&A, I am a little bit shocked that it hasn’t taken benefit of its well-priced foreign money to make an acquisition, particularly with it being a single-asset producer in a non Tier-1 ranked jurisdiction which may make it troublesome to keep up a double-digit free money stream a number of (no matter deposit high quality). Earlier commentary expressing Lundin Gold’s openness to M&A is as follows:

“Look, we’ve just gotta keep charging forward and so we’re looking at M&A opportunities, we’re obviously pushing the growth. Even after the payment of dividends and the repayment of the gold prepaid, we still retain a healthy treasury and continue to generate significant operating cash flow for other value generating activities such as the recently expanded near-mine and regional exploration programs, future throughput expansions, further debt reduction and M&A”.

– Lundin Gold, Investor Day 2023/Q1 2023 Conference Call

“Yes, we definitely are active [on M&A front]. We’re probably more active than we have been in the past. The team is doing an amazing job at site and looking for opportunities there. Andre has the exploration team, and that’s going really well with expanded rigs going. Yes, M&A is something we’re definitely looking at. And the challenge is, how do you add something that’s going to be as good as good or better than Fruta del Norte? That’s the challenge we’ve got. But the team is being creative. And as we’ve always said, as Lukas always pushed us and as Jack is pushing us, is you have to look at a lot of things. You just never know what might be the rose amongst all the dandelions”.

– Lundin Gold, Q4 2022 Conference Call

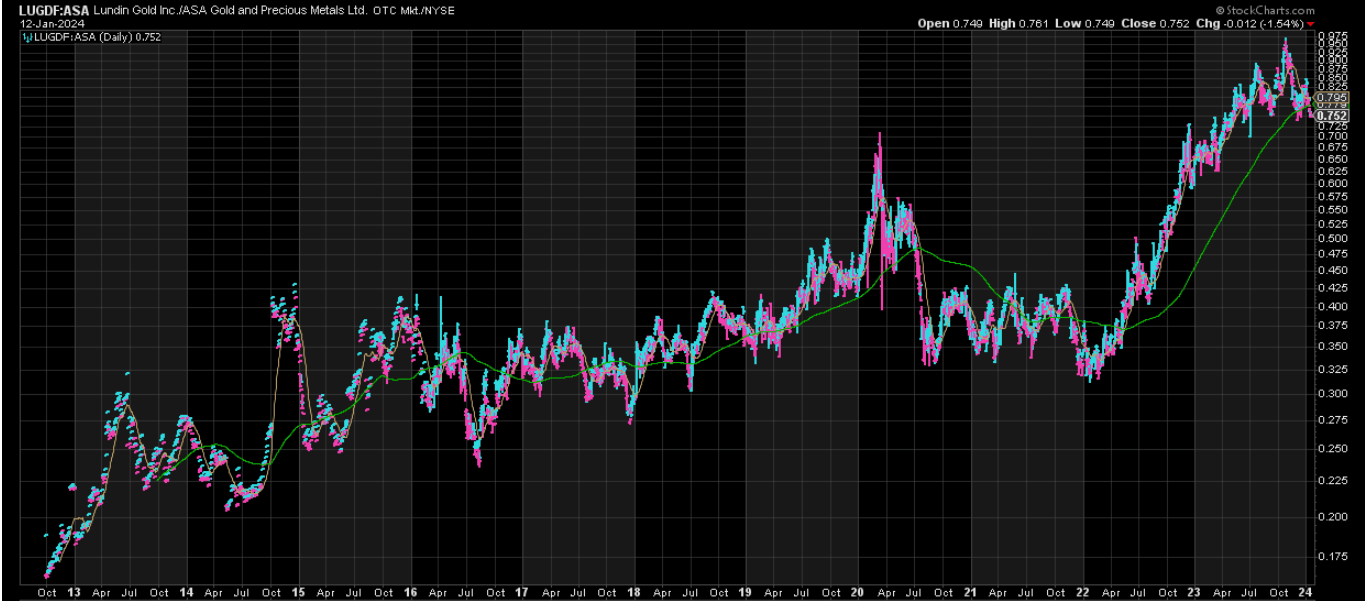

Fortuitously, Lundin Gold’s foreign money continues to be favorable, even the ratio between it and the ASA Gold and Treasured Metals Restricted Fund has declined by ~20% from 0.97 to 0.76. This continues to supply a good atmosphere for probably buying a small-cap producer or developer, particularly with builders buying and selling at their lowest multiples in years. Nevertheless, in Lundin Gold’s protection, it is not straightforward to seek out growth initiatives or smaller producers with comparable high quality belongings, and there definitely aren’t that many choices with sub $900/ozall-in sustaining prices to permit the corporate to keep up its industry-leading margins. And whereas Osisko Mining (OTCPK:OBNNF) definitely would have met this standards (Tier-1, high-margin, mid-scale), Gold Fields (GFI) made a transfer earlier this 12 months for half the undertaking, and different names have already been taken off the market like Osino, Marathon, and Sabina. Therefore, whereas Lundin Gold had its decide of the litter heading into 2023, the record has gotten a little bit smaller over the previous six months.

Lundin Gold vs. ASA Gold & Treasured Metals Fund – StockCharts.com M&A Exercise Gold House – FactSet

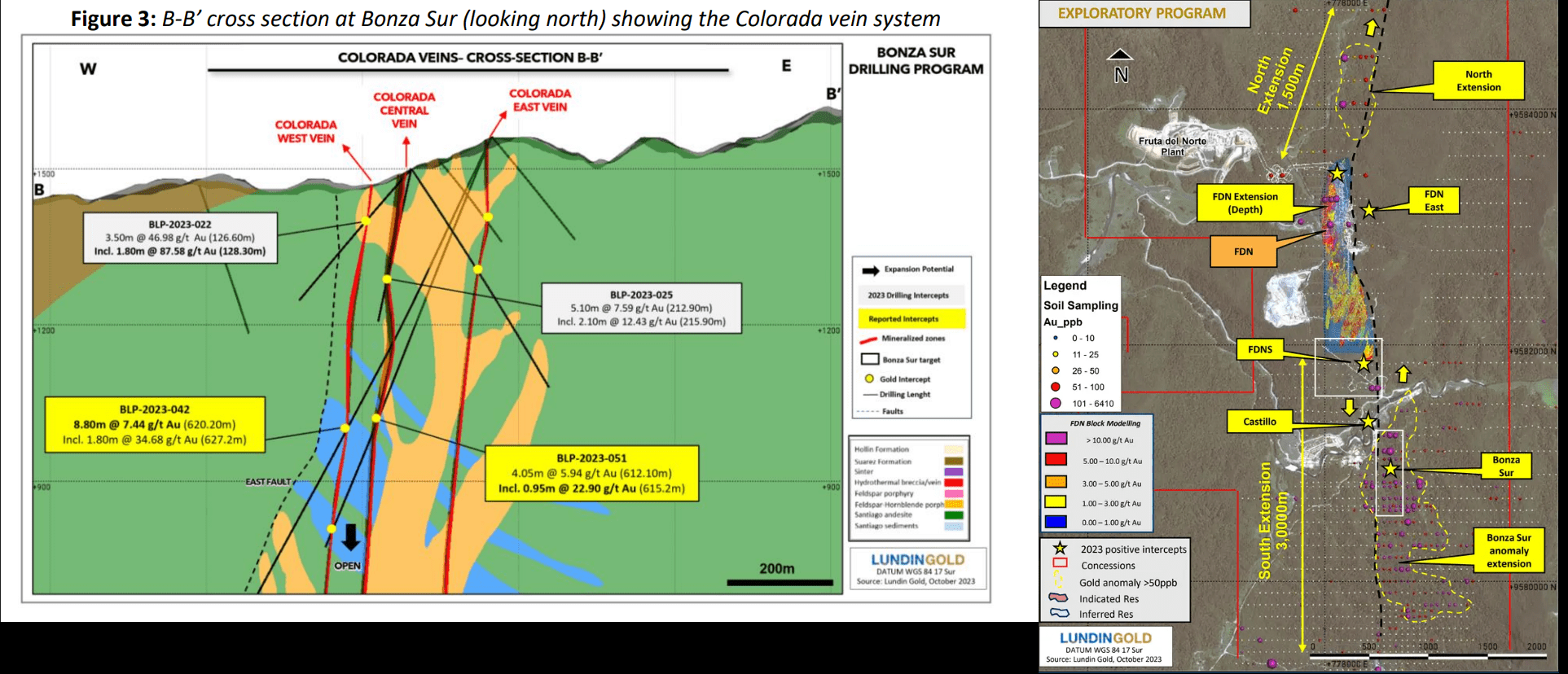

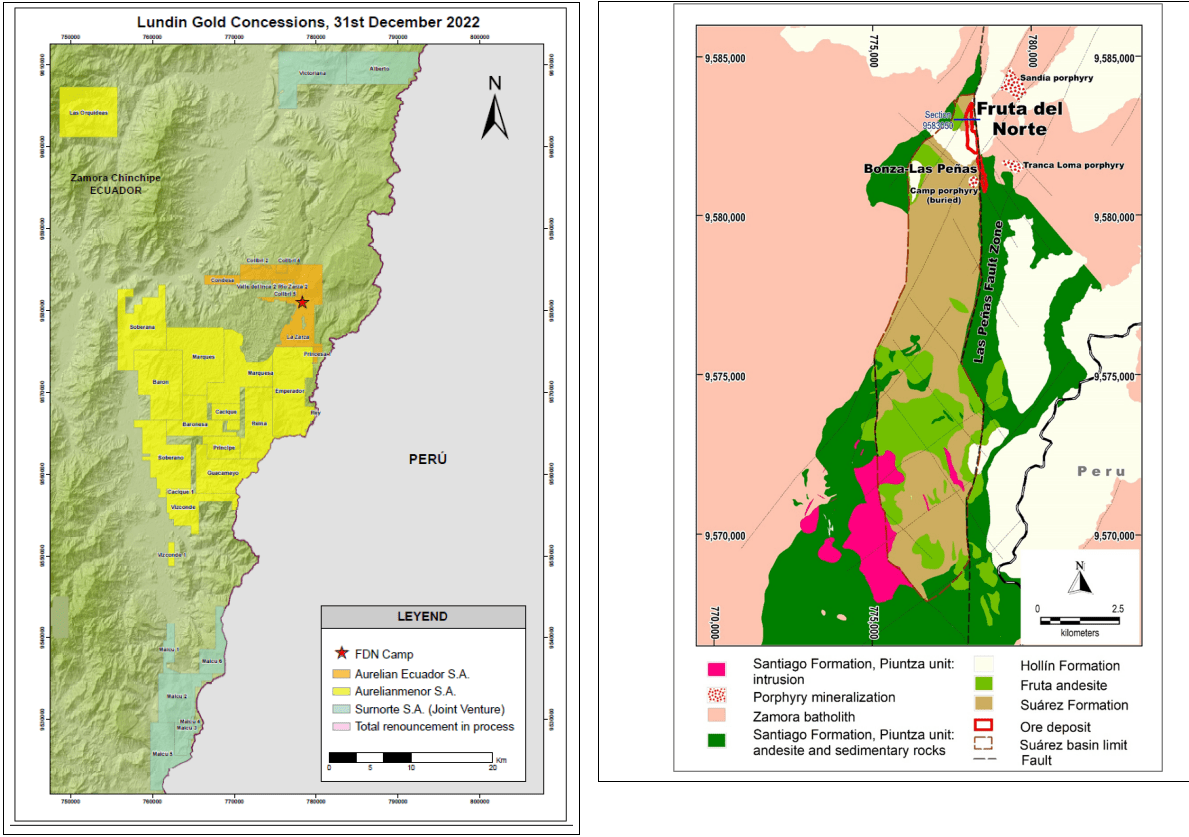

The final growth price noting is that Lundin enters the 12 months with a current new discovery on its arms at Bonza Sur (1 kilometer south of Fruta del Norte), with mineralization recognized over a 700+ meter strike and as much as 500 meters depths (deepest gap: 8.8 meters at 7.44 grams per tonne of gold). The corporate additionally hit mineralization instantly south of its useful resource base at Fruta del Norte South [FDNS], and has confirmed high-grade mineralization within the north-central sector near-mine just under its indicated useful resource base with spectacular intercepts like 12.4 meters at 10.1 grams per tonne of gold, 18.7 meters at 8.32 grams per tonne of gold, and 37.9 meters at 6.49 grams per tonne of gold with this presently outlined as inferred assets (not within the mine plan). Therefore, with a brand new discovery south of Fruta del Norte” with gold mineralization “within the same volcanic sequence discovered at Fruta del Norte“, and multiple new targets to be tested this year, this could be one of the most exciting years to be a Lundin Gold shareholder from an exploration standpoint.

Bonza Sur, Bonza Sur Anomaly Extension, New Targets (FDN East, North Extension, FDNS) & Bonza Sur Cross Section – Company Website

Valuation

Based on ~244 million fully diluted shares and a share price of US$11.50, Lundin Gold trades at a market cap of ~$2.75 billion. This places it well ahead of other 400,000 ounce plus producers like Equinox Gold (EQX), Torex Gold (OTCPK:TORXF), and OceanaGold (OTCPK:OCANF), which can partially be attributed to Lundin’s industry-leading margins, extremely high grades and track record of trouncing guidance over the past few years. Still, the current valuation leaves Lundin Gold trading at a large premium to its peers with a P/NAV multiple of ~1.0x, even if it now trades at one of the lower free cash flow multiples sector-wide.

Lundin Gold Concessions – 2022 TR

Using what I believe to be fair multiples of 1.1x P/NAV and 8.5x FY2024 cash flow estimates and using a 65% weighting to P/NAV and 35% assigned to P/CF, I see a fair value for the stock of US$14.50. And while this points to a 24% upside, I am looking for a minimum 35% discount to fair value to justify starting new positions in single-asset producers, especially if they don’t operate in Tier-1 jurisdictions. Hence, I don’t see nearly enough margin of safety at current levels, and I would need a pullback below US$9.30 to get more interested in the stock. Obviously, a pullback of this magnitude may not occur and any major new regional discovery across its massive land package (~64,000 hectares in the Zamora Copper-Gold Belt) or a move above $2,300/oz gold could send the stock soaring to new all-time highs. Still, I prefer to buy at the right price under a base case assumption or pass entirely, and I continue to see more attractive bets elsewhere in the sector currently.

Summary

Lundin Gold had another phenomenal year in 2023. This was evidenced by trouncing guidance for a third consecutive year, uncovering a new regional discovery in Bonza Sur, and setting itself up to maintain its ~500,000 ounce production profile with optimization work planned this year. Meanwhile, the company has retired all of its bank debt which will contribute to higher free cash flow margins this year, and investors can look forward to the most aggressive exploration program in Fruta del Norte’s history next year. That said, I prefer to buy at a deep discount to fair value and ideally below 0.60x P/NAV for small and mid-cap producers to ensure a margin of safety. So, while I think Lundin is one of the best run names sector-wide, I continue to prefer names like K92 Mining (OTCQX:KNTNF) that trade at ~0.50x P/NAV (upside case) and barely 4x FY2026 free cash flow estimates (~$280 million) with K92 having what I believe to be over 80% upside to fair value vs. Lundin at ~25% currently.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please pay attention to the dangers related to these shares.