Robinhood Markets (HOOD) Stock has authorized a $1.5 billion share repurchase program as its equity valuation struggles to regain momentum following a 54% correction from its October 2025 all-time highs.

The authorization, detailed in a Tuesday filing with the Securities and Exchange Commission, includes $1.1 billion in new capacity alongside unutilized funds from a previous mandate. This move signals a significant shift in capital allocation strategy, prioritizing shareholder return as retail trading volumes normalize after the speculative fervor of late 2025.

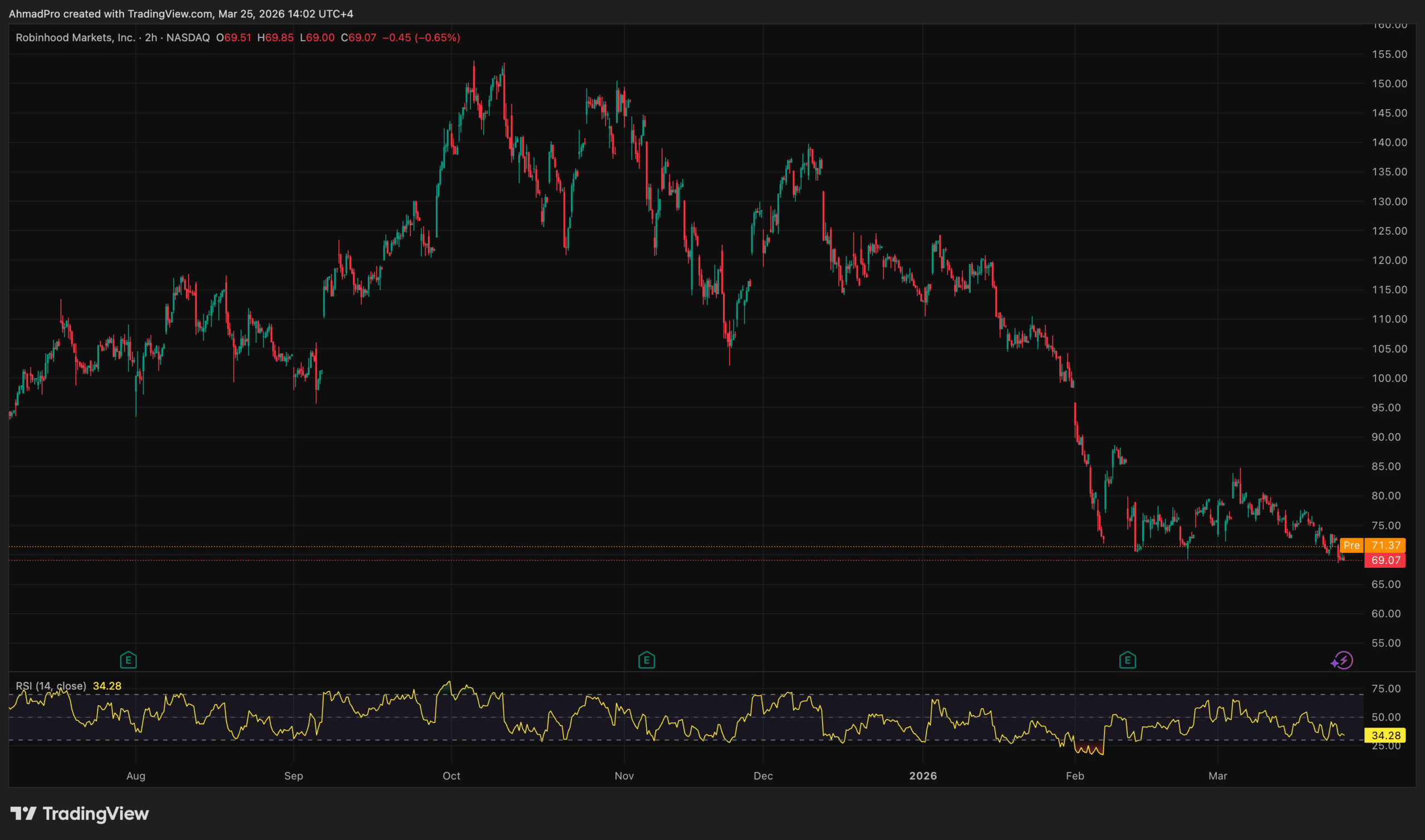

The announcement comes as the fintech platform grapples with a steep year-to-date decline, with shares falling to a 2026 low of $69.08 during Tuesday’s session. By committing capital to buybacks during a period of equity weakness, management is effectively attempting to floor the stock price while signaling that the company’s balance sheet remains robust despite broader geopolitical and macroeconomic headwinds.

ROBINHOOD INCREASES BUYBACK PROGRAM FROM $400M TO $1.5B.

“Robinhood is a generational company with a massive long-term opportunity,” said Shiv Verma, Chief Financial Officer of Robinhood. “This authorization reflects the confidence of our management team and board in our… pic.twitter.com/fGwlBmGRxv

— amit (@amitisinvesting) March 24, 2026

Robinhood Buyback Mechanics: Capital Allocation Under Pressure

The repurchase program is structured to deploy up to $1.5 billion over the next three years, though actual execution remains subject to management discretion and market conditions. To bolster its liquidity position while executing these buybacks, Robinhood Securities simultaneously entered into a $3.25 billion revolving credit facility with JPMorgan Chase, replacing a prior $2.65 billion agreement. This facility features an expansion option allowing total borrowing capacity to reach $4.87 billion, ensuring the company maintains operational flexibility even as it returns cash to shareholders.

Robinhood Chief Financial Officer Shiv Verma characterized the authorization as a reflection of the board’s confidence in the firm’s “long-term opportunity,” emphasizing the intent to deliver value while continuing to invest in product innovation.

Financially, the buyback serves as a mechanism to support earnings per share (EPS) as revenue growth decelerates from the triple-digit gains seen in 2025. This approach mirrors recent moves by other major crypto-linked public companies like Block Inc, which have had to make aggressive capital allocation and restructuring decisions to navigate market weakness.

The mechanism functions as a programmatic bid for the company’s own equity.

🇺🇸CLARITY ACT: ROBINHOOD CEO SAYS PRIORITY IS VALUE AND SAFETY

Robinhood CEO Vlad Tenev (@Vladtenev) is urging Congress to pass the CLARITY Act, declaring that Value and safety are key to determining stablecoin yields.

Tenev calls for regulatory clarity that lets stablecoins… pic.twitter.com/yEmi2c4u35

— BSCN (@BSCNews) March 21, 2026

By retiring shares at current valuations, management is betting that the current price-to-sales ratio—which hovered near 37x in mid-March—represents a discrepancy between market sentiment and intrinsic value. Typically, such aggressive buybacks are viewed as a signal that insiders believe the stock is undervalued, though the high valuation multiple relative to traditional financial services firms adds a layer of risk to the strategy.

EXPLORE: LATEST FINANCE NEWS

Retail Crypto Volumes and Robinhood Stock: The Correlation That Explains Everything

The trajectory of Robinhood’s stock remains inextricably linked to the velocity of the broader crypto market. Shares ended Tuesday trading down 4.7%, a decline that parallels the cooling of digital asset volatility in the first quarter of 2026. Despite the company’s diversification into credit cards, banking, and prediction markets via partners like Kalshi, crypto trading fees accounted for more than 50% of transaction-based revenue in late 2024.

When retail interest evaporates, Robinhood’s top-line suffers disproportionately.

(Source: Tradingview)

Bellwether assets for retail sentiment have retreated sharply; as of March 12, 2026, Dogecoin and Shiba Inu—historical drivers of Robinhood’s highest volume days—were down 48% and 64% respectively from their 52-week highs. While on-chain metrics suggest Bitcoin adoption is booming globally, this structural growth has not translated into the high-frequency speculative trading volume required to sustain Robinhood’s transaction revenue model. The platform requires volatility, not just adoption, to drive transaction fees.

The stock is effectively trading as a leveraged beta on retail crypto participation.

Risk Factors: When Buybacks Signal Conviction or Distress

Deploying $1.5 billion into buybacks carries significant opportunity cost if the stock continues to re-rate lower. As of mid-March, Robinhood traded at valuations well above the financial services industry average, suggesting the stock is still priced for perfection despite the 39% year-to-date decline. If the crypto market enters a prolonged consolidation phase similar to 2022, acquiring shares at these multiples could prove dilutive to long-term shareholder value.

Competition for retail assets is also intensifying.

With retail assets under management reaching $280 billion, Robinhood faces pressure from yield-generating competitors like Galaxy Digital, which are aggressively targeting the same demographic. The risk remains that Robinhood is purchasing its own shares near a cyclical valuation peak rather than a trough. This dynamic has played out elsewhere in the sector, such as when Gemini saw its valuation metrics tested severely during previous crypto winters, highlighting the danger of extrapolating bull market revenues into bear market capital planning.

Capital returned to shareholders is capital not spent on customer acquisition during a downturn.

DISCOVER: TOP CRYPTO EXCHANGES

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing “information gain” that cuts through market hype to find real-world blockchain utility.