Justin Sullivan/Getty Photos Information

One central theme impacting markets in the present day is the weak efficiency of many client staples corporations. Final week, I covered Hormel (HRL), which has misplaced appreciable worth after dropping revenue margins by its failure to cross rising enter prices onto its product costs. That is one in every of many examples seen amongst client staples corporations, most of which have detrimental publicity to the inflation we’re seeing in the present day. Particularly, the “supply side” inflation is pushed extra by labor and uncooked supplies shortages than extra demand.

One other comparable instance of this difficulty could also be McCormick & Firm (NYSE:MKC), primarily recognized for its herbs and spices. The corporate additionally sells many condiments, and round 40% of its sales come from non-consumer taste options. Since 2020, the corporate has managed to develop its gross sales, however they’re stagnant in comparison with the worth index. Extra importantly, its gross revenue margins and general working margins have declined dramatically and are displaying minimal indicators of restoration.

MKC misplaced round 18% of its worth in 2023 and has decreased by simply over 30% because the finish of 2021 when inflation started to spike. Its EPS and revenue outlook have additionally slipped, although its ahead “P/E” valuation stays excessive at ~25X. The corporate has additionally seen a notable growth in curiosity expense and an increase in inventories, pointing towards potential steadiness sheet dangers. Nonetheless, the corporate has continued to raise its dividend and has steady revenues. As such, I imagine it is a wonderful time to look carefully at McCormick’s scenario in the present day to find out whether or not it should get well shortly.

McCormick’s Revenue Margin Pressures Mounting

Basically, a client staples agency will be extra dangerous in sure circumstances than the “cyclical” sectors. The scenario we’re seeing throughout many client staple corporations has much less to do with the financial cycle as a result of demand for merchandise like spices and condiments will not be significantly cyclical. Nevertheless, when the costs of these merchandise proceed to rise quicker than inflation, individuals are turning into extra price-sensitive, in search of lower-cost producers. For probably the most half, McCormick faces vital competitors within the spice and herb classes as a result of consumers can simply pick the bottom value merchandise for any herb or spice. That’s much less true for condiments, however it stays a difficulty on account of rising enter prices.

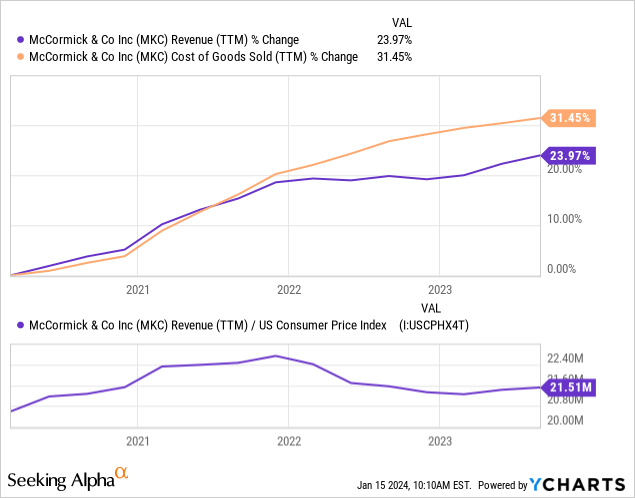

Amid this difficulty, McCormick has confronted some detrimental publicity on account of a research that discovered potential meals safety issues in its spices, leading to a lawsuit that was dismissed however nonetheless resulted in a good quantity of negative publicity for McCormick and some of its opponents. I imagine this can be one partial motive for the corporate’s battle to take care of revenue margins. Nevertheless, the broader difficulty is the sharp value enhance from imported flavors on account of rising labor prices in producing international locations and delivery costs. Since 2020, the corporate has been unable to develop its gross sales after inflation and has seen its COGS rise a lot quicker than its costs. See beneath:

Attributable to its improvements and acquisitions, McCormick had a good quantity of “real” income progress earlier than 2020. Since then, its gross sales have solely stored up with inflation. To be honest, many corporations haven’t seen their gross sales rise as a lot as inflation, however McCormick’s gross sales would possible be decrease if it had elevated its costs to match rising enter prices.

McCormick is uncovered to a very inflation-exposed and comparatively advanced provide chain. It sources uncooked supplies from all around the world, however the international locations across the Indian Ocean area specifically. In India and plenty of locations round these areas, spices have fallen right into a significant shortage, with excessive native inflation. Producing herbs and spices, particularly vanilla, is extraordinarily labor intensive. With international locations reminiscent of India seeing strong financial progress in recent times, it should naturally comply with that McCormick can be paying extra for merchandise as employee wages enhance with the economic system.

Additional, the pure taste market is very uncovered to transportation costs, a difficulty as outdated as the worldwide delivery business as a result of lengthy voyages the merchandise should take. Thus, greater gasoline costs will disproportionately hurt McCormick. Much more, commerce and delivery points, reminiscent of these within the Purple Sea in the present day, are potential points. Around 20% of the corporate’s gross sales come from the EMEA area, that means it might now be paying a lot greater prices on these gross sales as container delivery routes shift round Africa. I’d not say this can be a huge difficulty for the corporate in the present day, however any escalation in conflicts across the Indian Ocean may finally have huge detrimental penalties for McCormick. Basically, on account of geopolitical and financial troubles in that a part of the world, managing a provide chain as advanced as McCormick’s won’t be straightforward.

McCormick’s Notable Stability Sheet Points

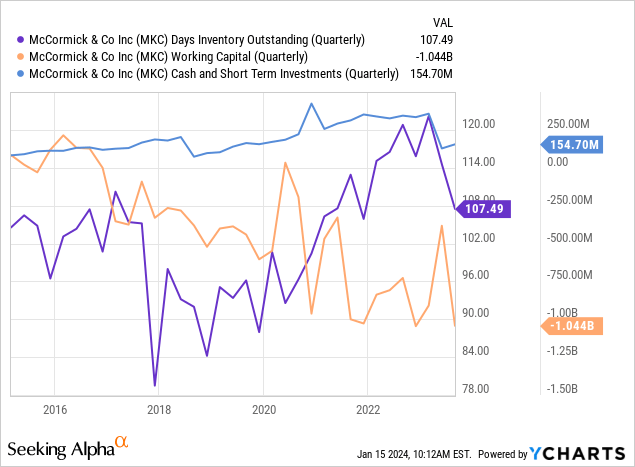

Additional, McCormick has seen some will increase to its stock ratio, although that difficulty started to unwind final quarter. Nonetheless, its inventories are a bit excessive from a seasonal standpoint, which nearly all the time negatively pressures gross margins. The corporate has a considerably poor liquidity place, with simply $154M in money and -$1B in working capital. See beneath:

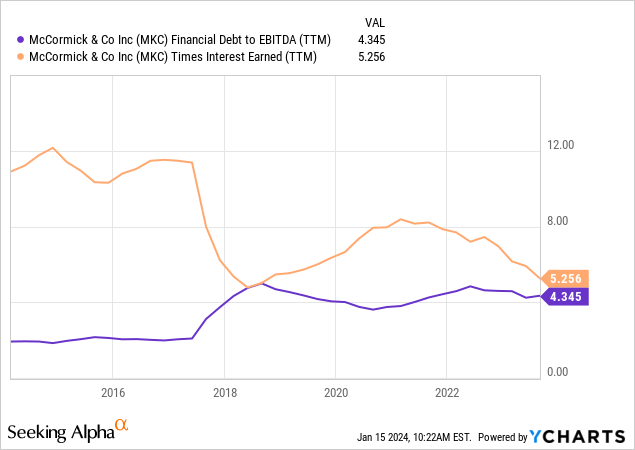

The mixture of low liquidity metrics and excessive stock factors towards one other quarter of doubtless weakened margins and potential wants for exterior financing or a diminished dividend. McCormick actually doesn’t have an excellent steadiness sheet. Following its collection of acquisitions, its leverage stage is a bit excessive, with a monetary debt-to-EBITDA ratio of 4.3X and a instances curiosity earned of 5.2X. See beneath:

Once more, neither of those ratios, significantly its Occasions Curiosity Earned, is regarding. Nevertheless, its leverage is elevated, and with rates of interest elevated, its TIE will naturally decline, possible taking internet earnings down and unbiased of its gross margin pressures. As famous in its final 10-Q, the corporate faces a $700M maturity of three.15% notes due in 2024. With its BBB credit standing, refinancing that debt will possible increase the speed to about 6%, theoretically decreasing its revenue by round $20M per 12 months; it isn’t an enormous loss, however it should add to the quite a few points harming its revenue. Moreover, with its money place typically low, its curiosity prices might rise extra shortly because it may make the most of different borrowings.

Revenue Outlook By 2026

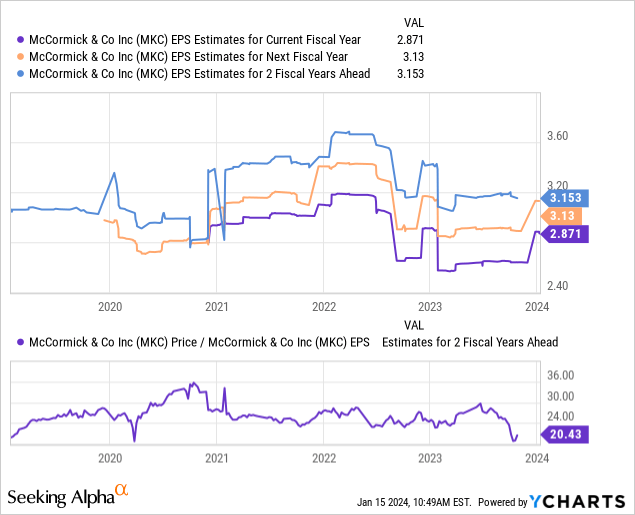

Most MKC analysts imagine the corporate will see a rebound in its EPS, with the determine anticipated to rise to $3.15 over the subsequent two fiscal years. From a valuation standpoint, which might give MKC the bottom ahead “P/E” since its 2020 crash, although its valuation was a bit elevated in recent times. See beneath:

Personally, even at a 20X “P/E,” I don’t imagine MKC is a superb deal on account of its excessive leverage and publicity to the various supply-side inflationary points on the earth. That isn’t essentially the measured US inflation folks see on headlines, however the basic disproportionate rise in labor and delivery prices in different international locations, significantly in growing international locations the place most of MKC’s merchandise in the end come from.

Additional, I don’t see a powerful trigger pointing to a rebound in McCormick’s revenue. For one, it should face an increase in curiosity prices so long as charges stay the place or close to the place they’re. Additional, its greater stock ratio signifies some continued battle to boost costs to match bills. It could attempt to take action, however that would put it in an uncompetitive place for consumers, who train extra discretion on account of rising prices. The identical applies to the corporate’s B2B taste enterprise, as corporations will possible look extra towards lower-cost corporations to attenuate COGS inflation. Certainly, I imagine it might be extra possible that its EPS will proceed to slide by 2026.

The Backside Line

Total, I imagine there’s a lot motive to be bearish or cautious about MKC in the present day. Because the firm is at a relative valuation low cost based mostly on its present outlook, I’d not guess towards it. That mentioned, I’m mildly bearish on MKC as a result of I don’t imagine even this “discounted” valuation is justified in comparison with its high-income dangers.

There are two primary points I see in McCormick in the present day. For one, on account of its option to develop aggressively over the previous decade, its debt stage may be very excessive, giving it detrimental publicity to extended excessive rates of interest and elevated fairness dangers related to its steadiness sheet. Secondly, exterior of the corporate’s speedy management, many points in these international locations across the Indian Ocean will possible proceed contributing to a disproportionate enhance in McCormick’s enter prices, which will not be simply handed ahead as Western patrons turn into extra price-sensitive amid rising prices.

I imagine MKC can be extra pretty valued at a 15X ahead “P/E,” eradicating the premium given to it as a “low risk” client staples agency, on condition that its EPS danger profile seems to be extra just like that of a client discretionary agency. Increased-cost pure taste objects have gotten a luxurious or discretionary good, given they don’t seem to be almost as low cost as they was once and can possible proceed to turn into costlier on account of their supply-side points. Thus, my value goal for MKC is ~$40 per share. That mentioned, I don’t count on MKC to fall to that value shortly, as few buyers appear to agree with my sentiment that it’s dropping its “staple” standing amid greater costs.