shapecharge

Funding Thesis

Diamond Hill (NASDAQ:DHIL) goes to report its FY23 numbers in the beginning of February. I needed to try what has occurred since I lined the corporate final, which was March ’23. The corporate’s share worth went nowhere in comparison with the general market, as the corporate continued to see its AUM lower within the latest quarters, nonetheless, I might count on significantly better numbers for This fall as the general market noticed a good rally within the final 3 months. Nonetheless, I’m sticking to my maintain ranking for the corporate, as I consider we’ll see additional volatility within the inventory markets and more money outflows due to it.

Replace on Financials

Since I lined the corporate again in March of ’23, the corporate’s share worth went nowhere towards the S&P500’s 25% advance. So, let’s have a look at how the corporate’s metrics have developed over the past 12 months nearly.

As of Q3 ’23, the corporate had round $210m in money and investments (LT investments), which is identical as of the tip of FY22. The corporate has no debt to fret about so that may be a constructive signal, that ought to appeal to many debt-averse traders, however that may not be the one factor that issues in an funding, since I do not thoughts when corporations tackle debt to finance their development and operations, so long as it is manageable.

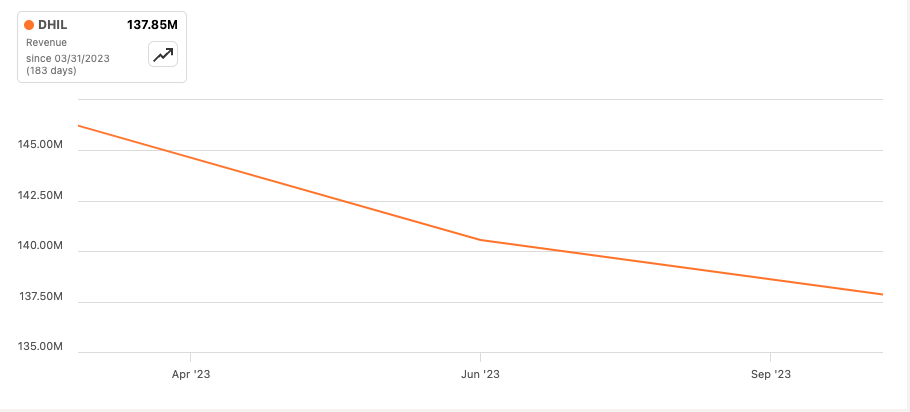

When it comes to revenues, the corporate’s trajectory has been clear. It has had a variety of problem sustaining it and we are able to see a transparent downtrend, with no obvious bounce as of the most recent quarter, wherein the corporate noticed one other 7% lower y/y.

Revenues over the past 12 months (Searching for Alpha)

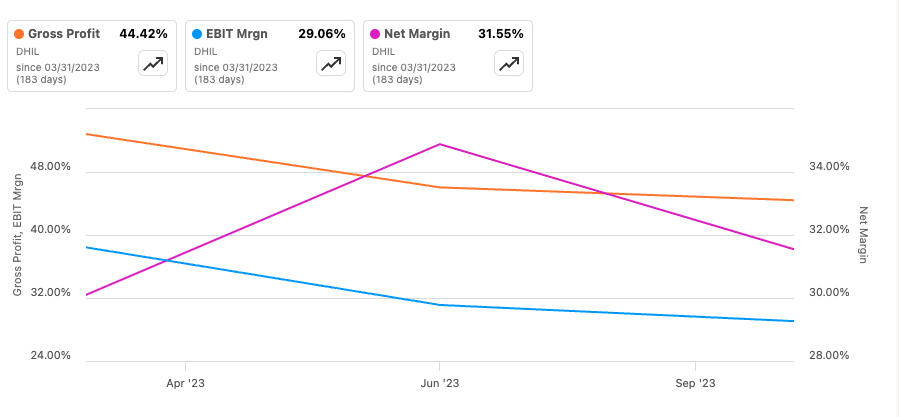

Over the identical interval, we are able to see the corporate’s margin has additionally taken successful. Gross margins noticed a whopping 840bps lower in a single 12 months, EBIT margins noticed round 700bps decline, whereas plainly web margins have considerably improved barely, round 150bps, so it isn’t all unhealthy. The large declines in gross and EBIT didn’t translate to the bottom-line deterioration. Plainly the corporate managed to navigate the turmoil considerably efficiently as web margins improved.

Margins over the past 12 months (Searching for Alpha)

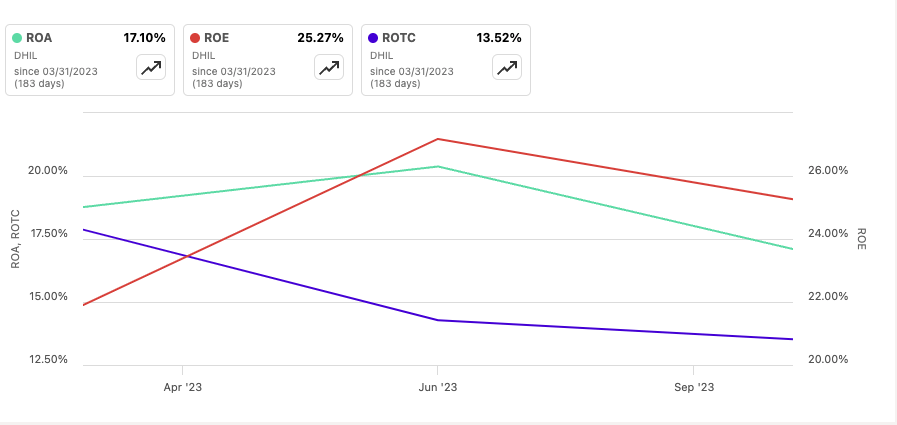

Persevering with on effectivity and profitability, the corporate’s ROE and ROA have barely improved since March of final 12 months however are on a downtrend over the past two quarters as soon as once more, which signifies that the corporate’s property and shareholder capital aren’t getting used very effectively, because the tougher macroeconomic instances persist. Moreover, the corporate’s return on complete capital has seen fairly a decline since March, which signifies that the corporate is dropping its aggressive edge and its moat, and it would not appear to bounce but.

Effectivity and Profitability (Searching for Alpha)

Total, the corporate’s efficiency has been lackluster. It’s no marvel that the corporate’s share worth additionally went nowhere mainly.

The reason for all of it

So, what has occurred? The corporate can not cease bleeding. Belongings underneath administration, or AUM have been experiencing a really risky time. The first quarter of ’23 noticed web inflows of round $84m and the market appreciated across the identical, nonetheless, within the 2nd quarter of the year, DHIL noticed web outflows of round $103m, however to counteract that, the market appreciated round $1.2B, so the corporate nonetheless noticed its AUM improve. Quick ahead to Q3 ’23, the corporate continued to see outflows from their funds improve, and on prime of that the market worth of the property declined $740m, giving a complete of $1B lower in AUM for the quarter. These final three intervals clarify the photographs above fairly properly. We will see will increase in the beginning of the 12 months via Q2, then every thing takes a nosedive.

Feedback on the Outlook

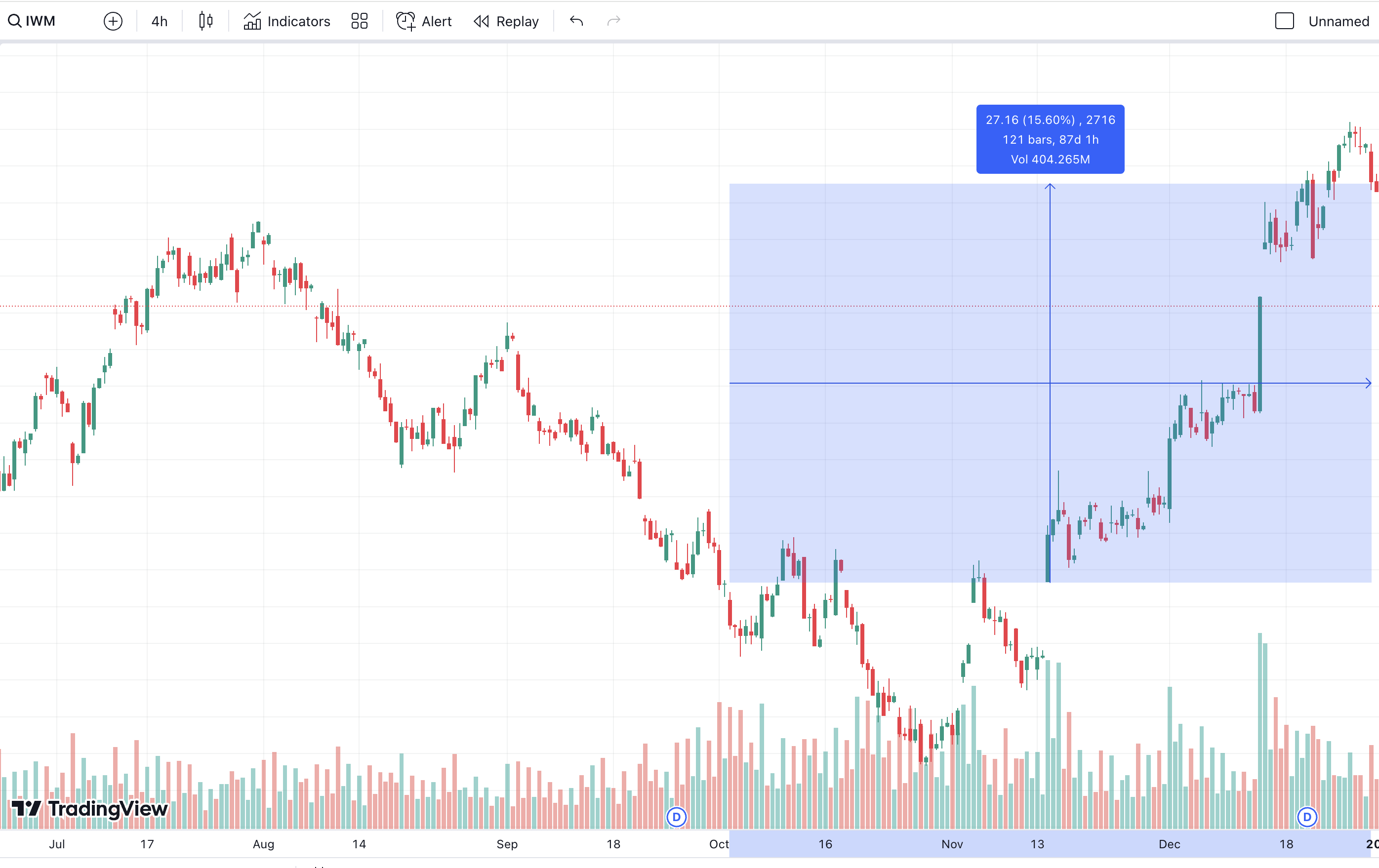

The corporate goes to report its 4th quarter in the beginning of February. I’m anticipating good outcomes by way of market worth appreciation. Russell 2000 (IWM) for the reason that finish of September ’23 is up round 16%, which signifies that the corporate needs to be up equally roughly. The key indices noticed a good end-of-the-year rally, which boosted many corporations and DHIL ought to report nice numbers right here.

IWM rally (Buying and selling View)

I wish to see AUM money outflows come to an finish, the macroeconomic setting could make lots of people skittish, which might carry more money outflows going ahead, till we see some extra certainty within the economic system, by way of rates of interest, and the place they’re headed. Whether or not they’ll be raised extra, lower quickly, or linger at these ranges for for much longer. We do not know what is going on to occur, which isn’t what traders like. I like the truth that even with such a drop in gross and EBIT margins, the corporate managed to take care of a good backside line. If the corporate can proceed to navigate such a tricky time within the markets, the corporate ought to see a restoration inside the subsequent 12 months or two, which can all depend upon the macroenvironment. If we go right into a recession, the inventory market will plummet, which DHIL is clearly part of.

Closing Feedback

So clearly, the corporate is just not trying nice for now, nonetheless, as soon as all of the uncertainty within the markets goes away and issues begin to enhance, I might count on the corporate’s efficiency to enhance but once more. My PT for the long term has not modified, which is round $180 a share, nonetheless, I’m nonetheless sticking to my maintain ranking for now, despite the fact that, the corporate ought to report respectable numbers for FY23. I do not suppose we’ve got seen the tip of it simply but, because the volatility within the markets stays excessive. Uncertainty is prevalent, and the U.S. economic system continues to be going too robust for the Fed, which suggests they may do every thing it takes to tame inflation, and rate of interest hikes aren’t off the desk simply but.

I’ll tune in to the corporate’s FY23 annual earnings and see what the corporate sees within the close to future.