As President Donald Trump gets set to meet Chinese counterpart Xi Jinping this week, China’s technological prowess will be on display, but its state-led growth model has been slowing—and a rapidly expanding mountain of debt is a warning sign.

In fact, while the recent explosion in U.S. federal debt has raised numerous red flags, a broader measure of indebtedness across the public and private sectors shows borrowing as a share of GDP is actually down since 2010.

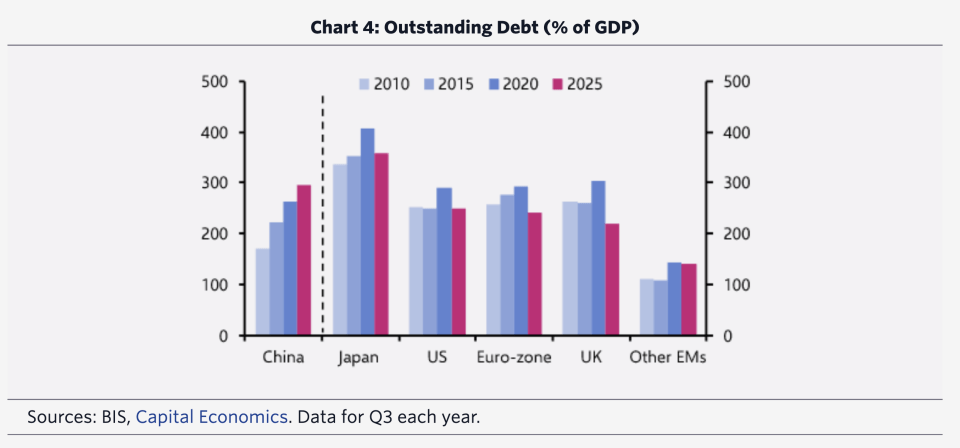

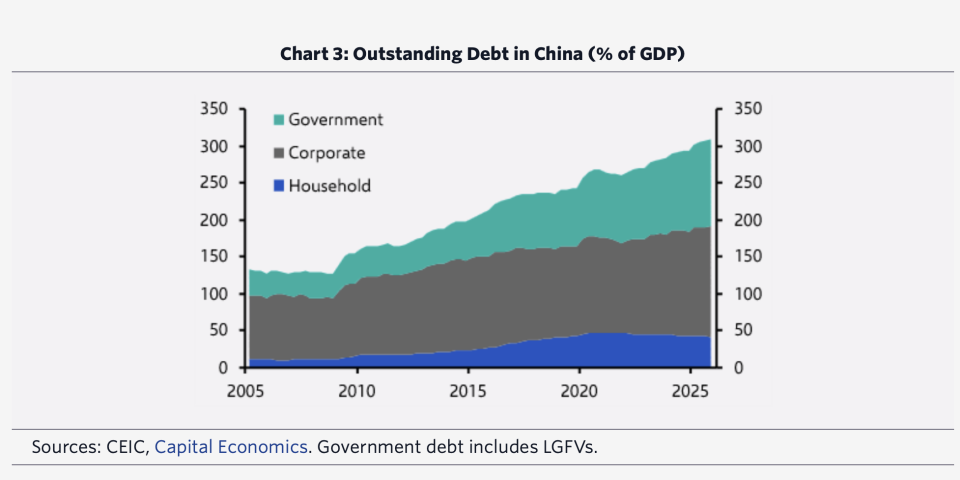

By contrast, China’s total debt-to-GDP ratio, excluding the financial sector, doubled in that span and has now topped 300%, according to Mark Williams, chief Asia economist at Capital Economics.

In a note late last month, he pointed out China’s debt surge has come despite weaker borrowing from households, which have been battered by the real estate market’s collapse.

But borrowing by companies as well as the central and local governments has continued to far outpace GDP growth, which has slowed in recent years, pushing the overall debt ratio higher.

Nearly 40% of outstanding debt is now owed by the public sector, including so-called local government financing vehicles, Williams calculated.

The result is total debt that surpasses the U.S., eurozone, the U.K., and other emerging markets. Aside from some smaller economies, only Japan has more debt.

“China’s current level of indebtedness puts it in a league of its own,” Williams said.

Of course, U.S. federal debt has set its own grim milestones, and is now more than 100% of GDP for the first time since the immediate aftermath of World War II.

But total public and private debt last year was about 265% of GDP, which has been robust lately. It’s also down sharply from pandemic-era highs, when governments unleashed a flood of stimulus. The eurozone and U.K. have similar trajectories.

Beijing is aware of its debt situation, particularly among local governments that often seek to boost favored industries like AI, electric vehicles, and robotics with low-cost loans.

Over the weekend, authorities vowed to ramp up efforts to ease local government debt risk with a restructuring program that helps borrowers meet payments on schedule.

Officials also called for preventing new hidden borrowing, along with strengthening the domestic economy and advancing infrastructure, according to Bloomberg, citing China Central Television.

But Chinese companies are borrowing more than they are selling. Business debt has doubled since 2019, while revenues are only 30% higher, according to Capital Economics.

Creditors continue to roll over loans to keep struggling firms afloat, even as nearly one-third of them are losing money, Williams noted. That worsens overcapacity and deflation, while preventing that capital from going to healthier borrowers.

China’s overcapacity and its support for manufacturers over consumers have stoked excess supply that drags down prices. An economy-wide price gauge shows China has been suffering from deflation for three straight years, the longest such streak since its transition to a market economy in the late 1970s.

The central government has tried to combat overproduction and excess competition, but China’s reliance on export-led growth continues to encourage more output.

In addition to the level of total Chinese debt as a share of GDP, Williams sounded the alarm on its rate of growth, noting the ratio increased by more than 120% of GDP over the past 15 years.

To be sure, this doesn’t necessarily mean China is on the brink of a Lehman Brothers-style crisis. The financial system survived a major stress test in the form of the property market crash, he noted.

High domestic savings and capital controls, plus the fact the state dominates the financial sector, also make China less vulnerable.

But even though the government’s outsized role in the surge debt helps lower the risk of a crisis, it’s not helping the economy.

“The irony is that one driver of both government borrowing and the lax lending standards of (state-owned) banks is the desire to prop up economic growth and prevent job losses,” Williams said. “But the product of a credit boom that has been underway for 18 years is a banking system propping up unproductive firms, widespread losses across industry and entrenched overcapacity.”