ECB Governing Council member Kocher says a June rate hike is unavoidable if the Hormuz Strait remains closed, warning prolonged conflict will push eurozone inflation materially higher.

Summary:

- Kocher said if the Hormuz Strait remains closed and the Middle East conflict continues, “there is no way around a rate hike” at the June 11 ECB meeting, according to Austrian state broadcaster ZiB2, , according to finanzen.at

- The Austrian National Bank governor said the ECB’s task is clear: if policymakers conclude that 2% inflation is no longer achievable, a rate rise must follow, per the ZiB2 interview

- Kocher said predicting full-year inflation is impossible for anyone, as the outcome depends entirely on how long the conflict lasts and how long the Strait of Hormuz remains closed to shipping

- Despite weak data, Kocher said the Austrian economy held up relatively well in the first quarter and that full-year growth of 0.5% remains possible if the Iran conflict does not prove prolonged

- Kocher noted that Austria’s planned budget consolidation has become significantly more difficult in the current environment, and that governments face limited options when confronted with an external shock of this nature, according to ZiB2

- He was careful to note the June 11 meeting is still three weeks away, leaving room for conditions to change before any decision is taken

The European Central Bank will have little choice but to raise interest rates at its June 11 meeting if the Strait of Hormuz remains closed and the Middle East conflict shows no sign of resolution, ECB Governing Council member Martin Kocher said on Tuesday evening. Speaking on Austrian public television, Kocher delivered his most direct signal yet on the June policy decision, stating that if the current situation in the region persists and oil, fertiliser and chemical shipments through the strait continue to be blocked, a rate increase cannot be avoided.

Kocher, who serves as governor of the Austrian National Bank, framed the ECB’s logic in straightforward terms. The central bank’s core mandate is medium-term price stability, and if policymakers conclude that returning inflation to 2% is no longer achievable under current conditions, then a rate hike must follow. He stopped short of calling it a done deal, noting that three weeks remain before the Governing Council convenes in Frankfurt, and that much depends on how the geopolitical situation develops in the interim.

On inflation, Kocher said it was impossible for anyone to put a reliable figure on where the eurozone will end the year, given that the outcome is almost entirely contingent on the duration of the conflict and the length of the Hormuz closure. The longer hostilities continue, he said, the higher inflation is likely to run. He drew a deliberate contrast with the post-Ukraine invasion period, when Austrian inflation exceeded 7%, noting that the current situation remains well below those levels for now, though the trajectory will depend heavily on events in the coming weeks.

Despite the external shock, Kocher said the Austrian economy had shown reasonable resilience in the first quarter, and he did not rule out full-year growth of around 0.5%, conditional on the Iran conflict not becoming a prolonged affair. He acknowledged that the government’s options in the face of an external supply-side shock are limited, noting that some fiscal measures, including a VAT reduction on food, are helping to ease price pressures, while others such as a new parcel levy are adding to them. The net effect on inflation he described as mildly positive.

The remarks represent a notable escalation in Kocher’s guidance. As recently as 13 May, in an interview with Econostream, he had said a June hike should not be considered the baseline and that the Governing Council was deciding meeting by meeting. Tuesday’s comments, delivered in a prime-time television setting rather than a specialist financial media outlet, carry considerable weight and suggest the threshold for action is lower than markets may have assumed.

—

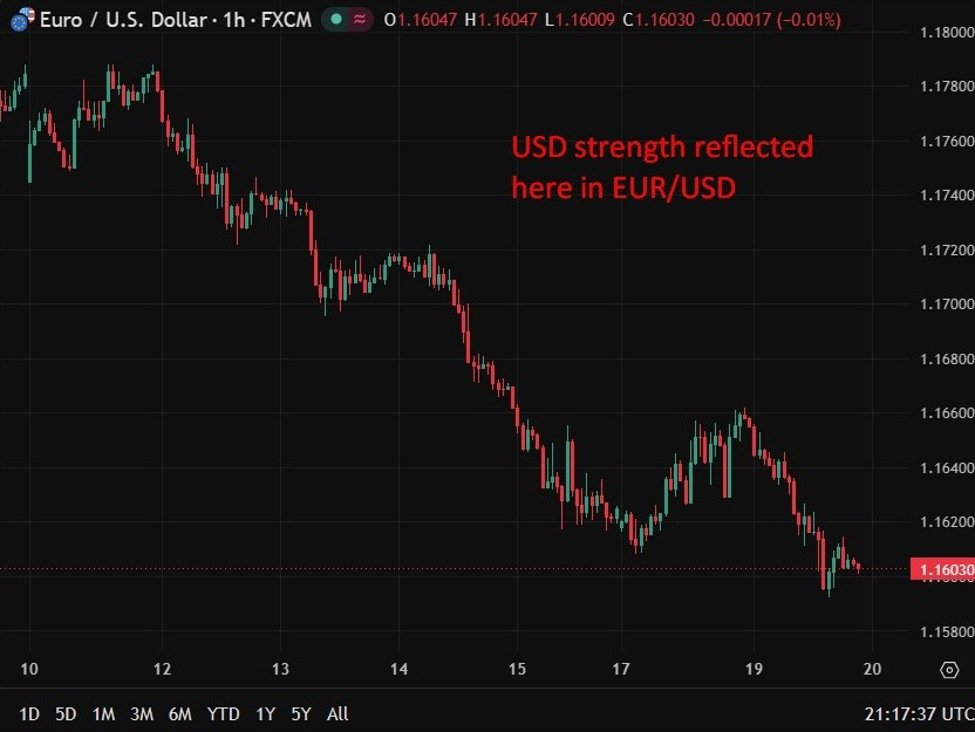

A June ECB rate hike, if delivered, would mark a significant hawkish pivot for a central bank that has held rates steady since last summer, and would likely strengthen the euro further at a time when it has already gained 14% against the dollar over the past year. For oil markets, the signal is doubly meaningful: elevated energy prices are the primary driver of the inflationary pressure Kocher is warning about, creating a feedback loop in which sustained Hormuz disruption both pushes crude higher and raises the probability of rate action that could dampen growth and demand. Bond markets across the eurozone would face selling pressure on any firming of June hike expectations, with peripheral spreads particularly vulnerable. The conditional framing leaves three weeks of headline risk before the June 11 decision.