Darren415

Welcome to a different installment of our CEF Market Weekly Evaluation, the place we talk about closed-end fund (“CEF”) market exercise from each the bottom-up – highlighting particular person fund information and occasions – in addition to the top-down – offering an outline of the broader market. We additionally attempt to present some historic context in addition to the related themes that look to be driving markets or that traders must be conscious of.

This replace covers the interval by the second week of January. Remember to try our different weekly updates masking the enterprise improvement firm (“BDC”) in addition to the preferreds/child bond markets for views throughout the broader revenue house.

Market Motion

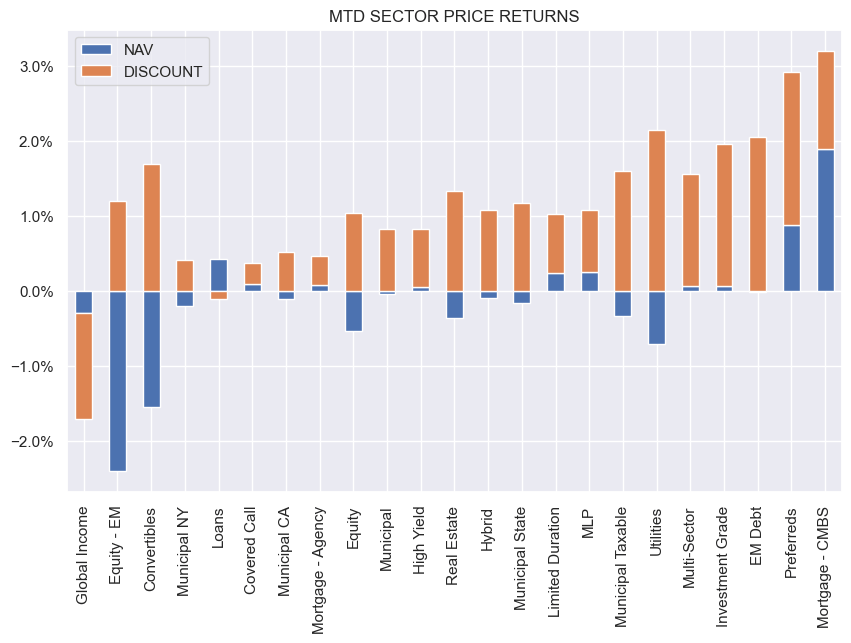

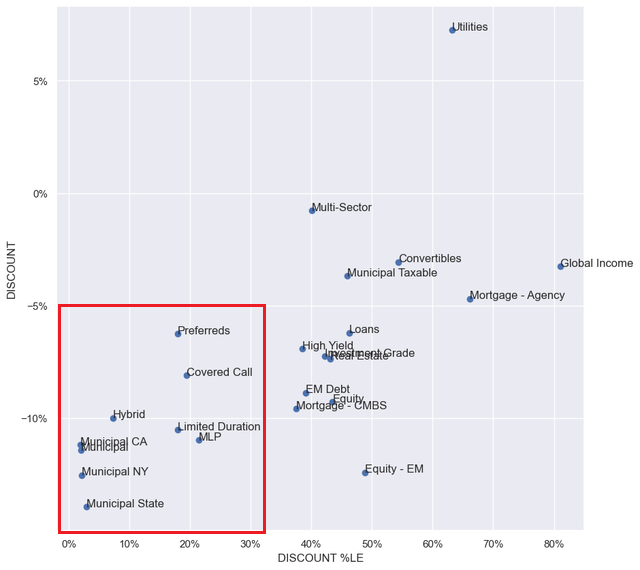

Most CEF sectors had been up on the week as each shares and Treasuries rallied. Month-to-date, nonetheless, NAV efficiency is combined. CMBS has to date delivered the perfect return – a pointy turnaround of its 2023 relative efficiency. Reductions, nonetheless, have tightened throughout all however one sector, indicating renewed investor confidence within the house.

Systematic Earnings

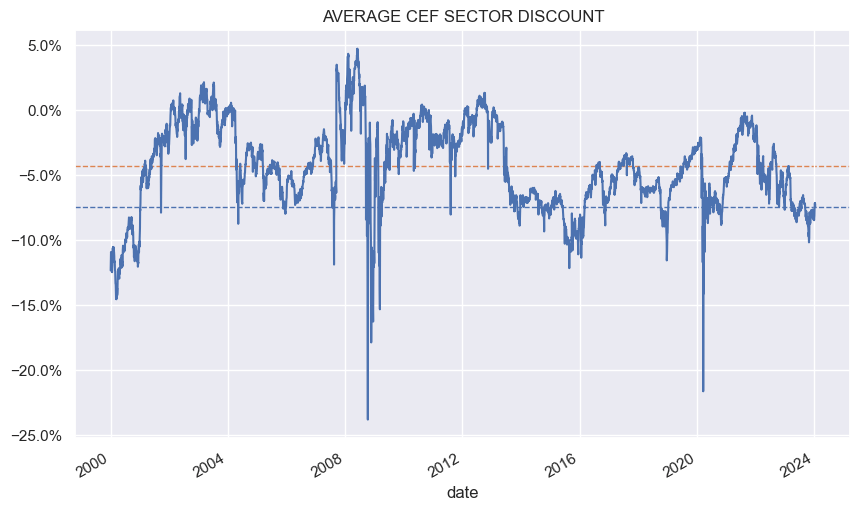

On a mean sector foundation, reductions have tightened a number of share factors because the backside final 12 months.

Systematic Earnings

Sectors like Munis, Hybrids and Preferreds proceed to commerce at double or excessive single-digit reductions. In addition they commerce at low low cost percentiles, which means their reductions are huge relative to their very own historical past.

Systematic Earnings

Market Themes

This week CEF sector designations got here on up on the service. Particularly, there was a query of why a fund just like the DoubleLine Earnings Options Fund (DSL) is positioned within the Multi-Sector class in our CEF Software whereas it sits in World Earnings on CEFConnect.

Actually there are numerous variations between our sector placement and that of CEFConnect. That is due to, roughly talking, straightforward circumstances and exhausting circumstances. As an example, a fund like John Hancock Premium Dividend Fund (PDT) is positioned within the Preferreds sector by CEFConnect whereas we have now it within the Hybrid sector. PDT is a straightforward case – its allocation is sort of half in widespread inventory with preferreds making up lower than 1 / 4 of the portfolio. There isn’t any manner it needs to be allotted to the preferreds sector.

JH

There are additionally exhausting circumstances such because the Ares Dynamic Allocation Fund (ARDC). Its allocation has been roughly evenly break up between mounted and floating-rate belongings. For instance, it was 40% mounted in 2019 which elevated to 50% mounted in mid 2021 and is now 45% mounted. CEFConnect locations the fund within the Mortgage sector whereas we have now it as a Multi-sector CEF.

The Loans sector placement is clearly questionable as traders could be evaluating it to funds which are predominantly allotted to loans. Multi-sector is arguably the precise place for it although it is not excellent as many Multi-sector CEFs are inclined to allocate to many various kinds of credit score sectors similar to ABS, Businesses, investment-grade and high-yield company bonds, Treasuries, Munis and others – belongings which ARDC principally avoids.

Coming again to DSL – what’s the proper sector for the fund? DSL is one other exhausting case in our view. The explanation we do not view World Earnings as the precise sector for the fund is that World Earnings tends to face in for non-US developed market bonds which DSL would not maintain a complete lot of.

Roughly talking, there are three world bond sectors – US, developed non-US and Rising Markets. Funds that primarily allocate to EM bonds similar to EDF or EDD sit within the EM CEF sector as anticipated. Funds that allocate to excessive or medium-quality bonds of G7 (and comparable) nations are typically positioned within the World Earnings sector.

From its allocation, DSL might arguably be positioned within the EM sector reasonably than World Earnings which tends to be a synonym for developed non-US. Nonetheless, its EM allocation is under 40% which means that it’s higher described as a Multi-sector fund notably because it holds many different credit score sectors similar to loans, ABS, MBS and CLOs. This level is clearly debatable however both Multi-sector and EM are higher matches for DSL than World Earnings.

DoubleLine

The consequence of this dialogue is two-fold. One, CEFs that may be completely positioned of their sectors are arguably within the minority. Some sectors like Munis and Fairness are pretty “clean” from this attitude however many credit score funds are much less so. And two, this implies evaluating funds inside the sector is difficult as each efficiency and valuation may very well be impacted by variations in allocation. Traders ought to pay attention to a given fund’s allocation profile and the way it differs from its sector counterparts when evaluating its metrics.

Market Commentary

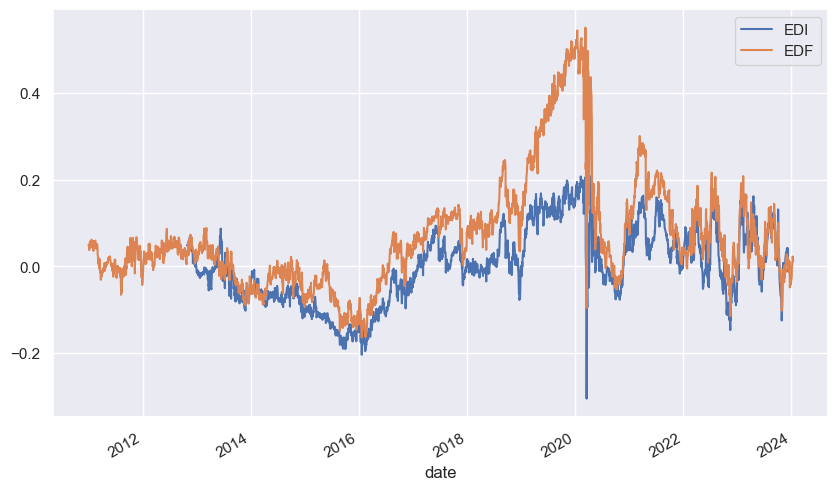

Final month two Virtus Stone Harbor Rising Market debt CEFs – (EDI) and (EDF) – merged with the latter being the surviving fund. The 2 funds have been an instructive curio within the house for a number of causes.

For one, they’ve tended to commerce at very excessive premiums, spending a lot of their time at double-digit ranges and infrequently buying and selling at reductions. That is regardless of fairly abysmal returns. As an example, EDF has a 5Y whole NAV return of round zero whereas its 10Y whole NAV CAGR is round 1%. An enormous a part of this has to do with the struggles of the fund’s broader sector – hard-currency and local-current Rising Market debt – however a few of it’s clearly as a result of funds’ lack of alpha.

Two, as a result of the funds’ EM debt holdings are comparatively excessive beta they’ve suffered from serial compelled deleveraging which repeatedly compelled the funds to promote low and buy-back greater, damaging the NAV.

Three, their low distribution protection underlined the truth that the excessive distribution charges had been unfounded. Poor longer-term whole NAV returns, serial deleveraging and low distribution protection finally compelled the funds to chop their distributions a number of occasions, pushing the premiums decrease and locking in everlasting financial losses for holders.

One other oddity is that, regardless of being practically similar funds, they’ve tended to commerce at very completely different valuations. This needed to do with very unusual distributions the place EDF’s NAV distribution fee was a lot greater than EDI’s for no good purpose. This precipitated EDF to constantly commerce at the next premium than EDI – generally shifting out to a premium 25% greater than EDI.

Systematic Earnings

Clearly this finally and absolutely corrected with the merger announcement, additional punishing traders who thought they had been getting a juicier yield.

Stance And Takeaways

The current run-up in CEF efficiency has been good to see nonetheless we aren’t chasing the rally. That mentioned, we proceed to see worth in funds just like the CLO Fairness-focused Carlyle Credit score Earnings Fund (CCIF) and the credit score and power targeted PIMCO Dynamic Earnings Technique Fund (PDX) in addition to the Flaherty suite of most popular CEFs like (PFO) whose valuations have pushed out to double-digit ranges. As soon as the Fed will get going with its coverage fee cuts, PFO and its sister funds ought to begin to reverse their earlier distribution cuts.

Editor’s Word: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.