alengo

Introduction

M-tron Industries (NYSE:MPTI), a micro-cap play, makes a speciality of producing sure standardized and customised digital elements which can be instrumental in monitoring and addressing the frequency and spectrum of digital circuit indicators.

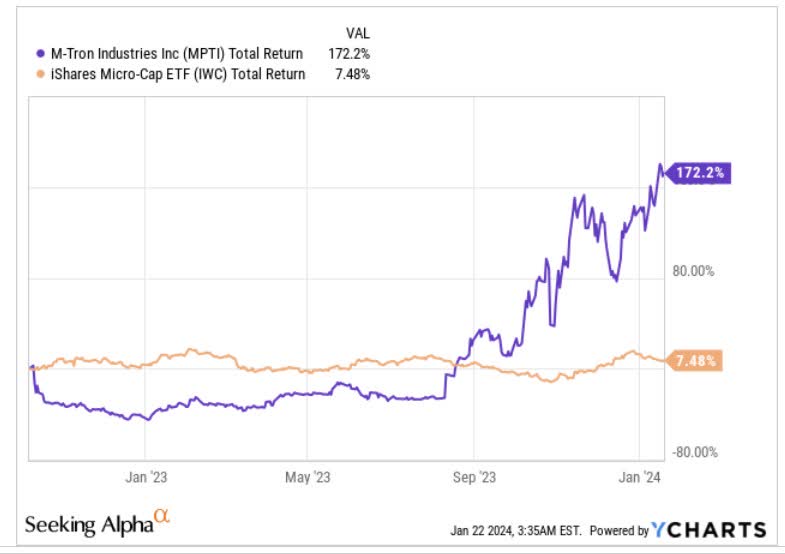

Till Q3-22, MPTI was part of the LGL Group, however in October 2022, it received separated into an unbiased firm and made its debut on the markets. Since its itemizing debut, MPTI has confirmed to be an impressive supply of alpha for its shareholders, delivering exorbitant returns of 172% at a time when micro-caps, on common, have solely delivered single-digit returns.

Return

MPTI- What’s To Like

Exploring the world of MPTI, it isn’t tough to see why the market loves this inventory, because it has loads of issues going for it.

Firstly, be aware that despite the fact that it could have solely made its itemizing debut just a few years again, it has constructed up an enormous stage of experience within the area of RF (Radio frequency) elements and companies, one thing which it has been concerned in since 1965!

Crucially while RF elements, are utilized in an entire host of industries, it helps that the industries that predominantly depend on MTPI’s portfolio are these that aren’t prone to the vicissitudes of financial cycles, however those who render important companies within the modern-day period. We’re speaking in regards to the likes of the protection and aerospace industries which account for 58% of MPTI’s complete enterprise, and also you don’t get to cater to those segments except you’ve constructed up enough area experience over time. MPTI additionally companies the who’s who of the sector with the likes of Raytheon (RTX), Lockheed Martin (LMT), and Northrop Grumman (NOC) all making up the shopper roster, and enterprise alternatives listed here are simply usually stickier.

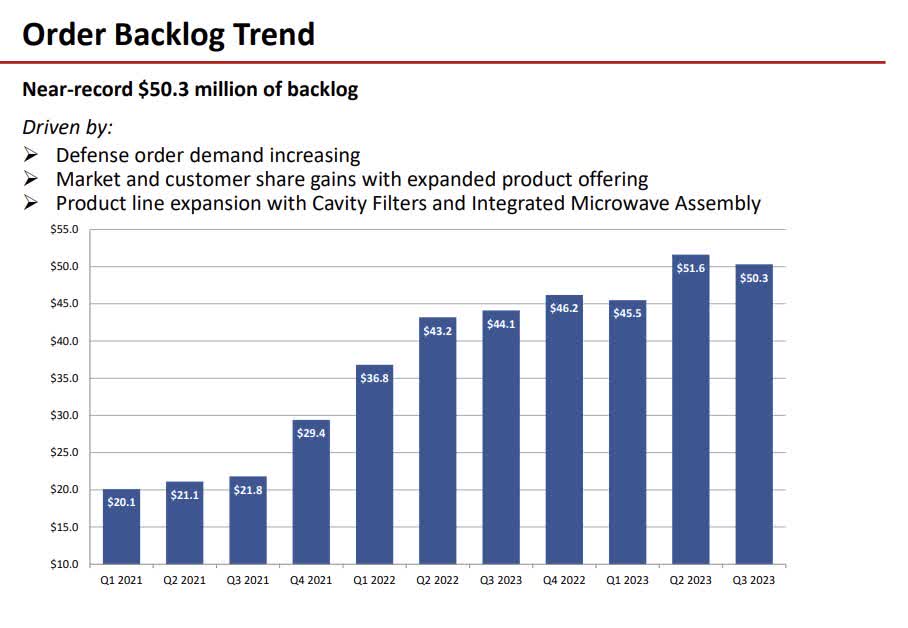

Not solely does MPTI cater to steady industries, it is usually witnessing large progress within the progress of its backlog, and the tempo at which its high line is rising (31% progress as of 9M, and consensus estimates level to the same trajectory for the entire yr)

A few years in the past, MPTI’s backlog used to hover across the $20m mark, however since then it has greater than doubled and is at the moment trending on the $50m mark.

Jan 2024 Investor Presentation

MTPI is at the moment producing round $10-$11m of topline per quarter, and provided that the backlog sometimes interprets to income over 12-24 months, you’re taking a look at 4-5 quarters of strong income visibility.

Apart from, given how integral MPTI’s companies are to its finish markets, this backlog will not be static and can develop over time. Nonetheless, subsequent yr’s topline estimates counsel mid-teens income progress,

Traders additionally want to acknowledge the altering texture of this backlog. Beforehand MPTI was bidding for a lot smaller alternatives, however lately they’ve been concentrating on a lot bigger applications, which speaks to their rising stature available in the market.

Once you become involved with bigger applications, volumes and ASPs are usually increased (on a TTM foundation, MPTI witnessed whopping ASP progress of 117% as of Sep 2023), and there’s innately simply higher move by means of on the margin stage, if you may get your price base proper.

In that regard as effectively, MPTI deserves nice credit score as they have been exiting low-margin companies, and deepening their automation impetus vis-à-vis labor. It additionally helps that there’s an effort to implement focused value will increase. All this has been mirrored within the large gross margin progress seen over the past 2 quarters. In Q2, the group gross margin expanded by over 400bps YoY, and in Q3, the progress was much more spectacular coming in at over 1000bps increased YoY.

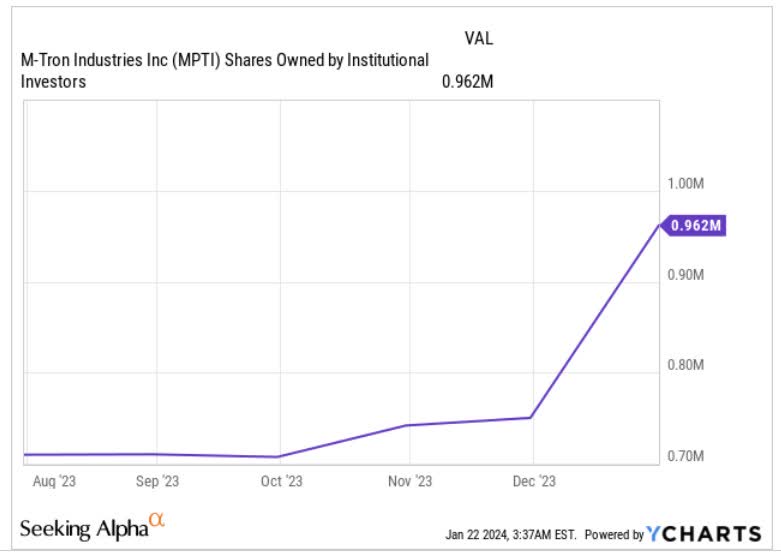

What’s additionally encouraging to notice is that the good cash seems to be paying attention to MPTI’s progress and over the past 6 months alone, they’ve elevated their stake within the inventory by over 35%. Rising institutional participation will probably be key for MPTI to get higher visibility from greater fund homes and transition from a micro-cap play (present market cap is a bit over $115m) to a small-cap play.

YCharts

Closing Ideas- Is M-tron Industries A Good Purchase Now?

Regardless of among the favorable themes related to the enterprise of M-tron Industries, we’re not too satisfied that the inventory would make an excellent purchase at these ranges.

Firstly the valuation quotient comes throughout as fairly expensive, and it’s questionable if one is getting enough earnings progress for that elevated P/E a number of.

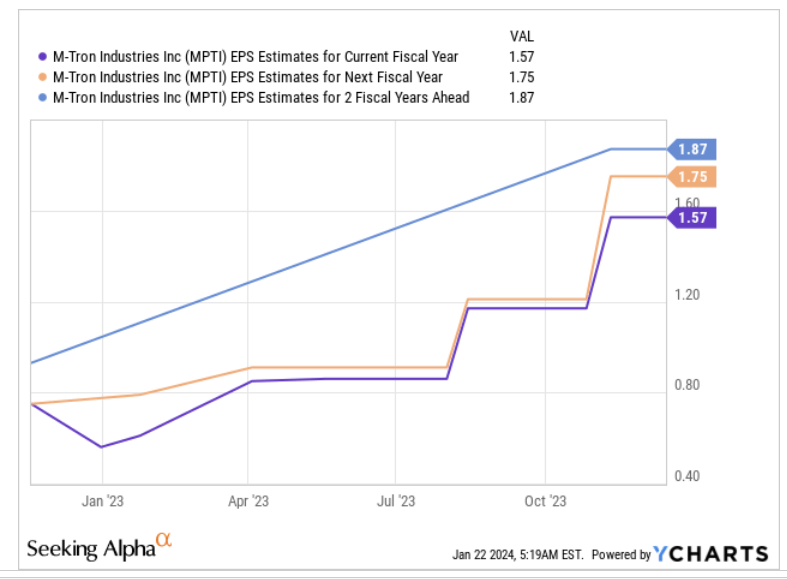

Based mostly on YCharts earnings expectations for the subsequent two years, one is principally coping with a enterprise that’s poised to ship earnings CAGR of 9% by means of FY25.

YCharts

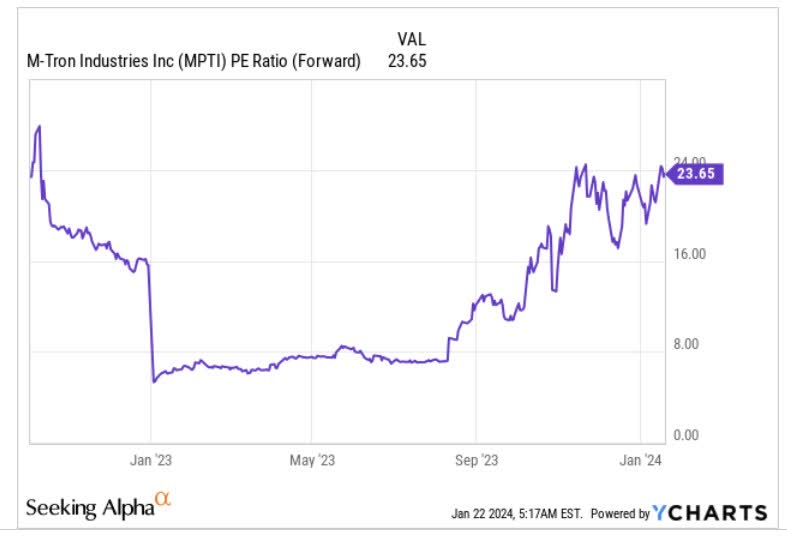

In mild of the medium-term trajectory of solely single-digit earnings progress, it feels a bit beneficiant to shed out a ahead P/E a number of of 23.6x. What makes the valuation quotient much more unfavorable is the truth that MPTI’s different digital element friends are at the moment buying and selling at a mean ahead P/E of roughly 20x, which interprets to an 18% low cost.

YCharts

Then buyers specializing in rotational trades throughout the broad micro-cap universe are unlikely to search out the MPTI inventory too enticing at this juncture. Be aware that the relative energy (RS) ratio of MPTI to the iShares Micro-cap ETF is at the moment round 65% increased than the mid-point of its buying and selling vary and will witness some mean-reversion. It additionally seems to have pivoted away from the highs seen in November final yr, from the place it struggled to construct momentum.

Stockcharts

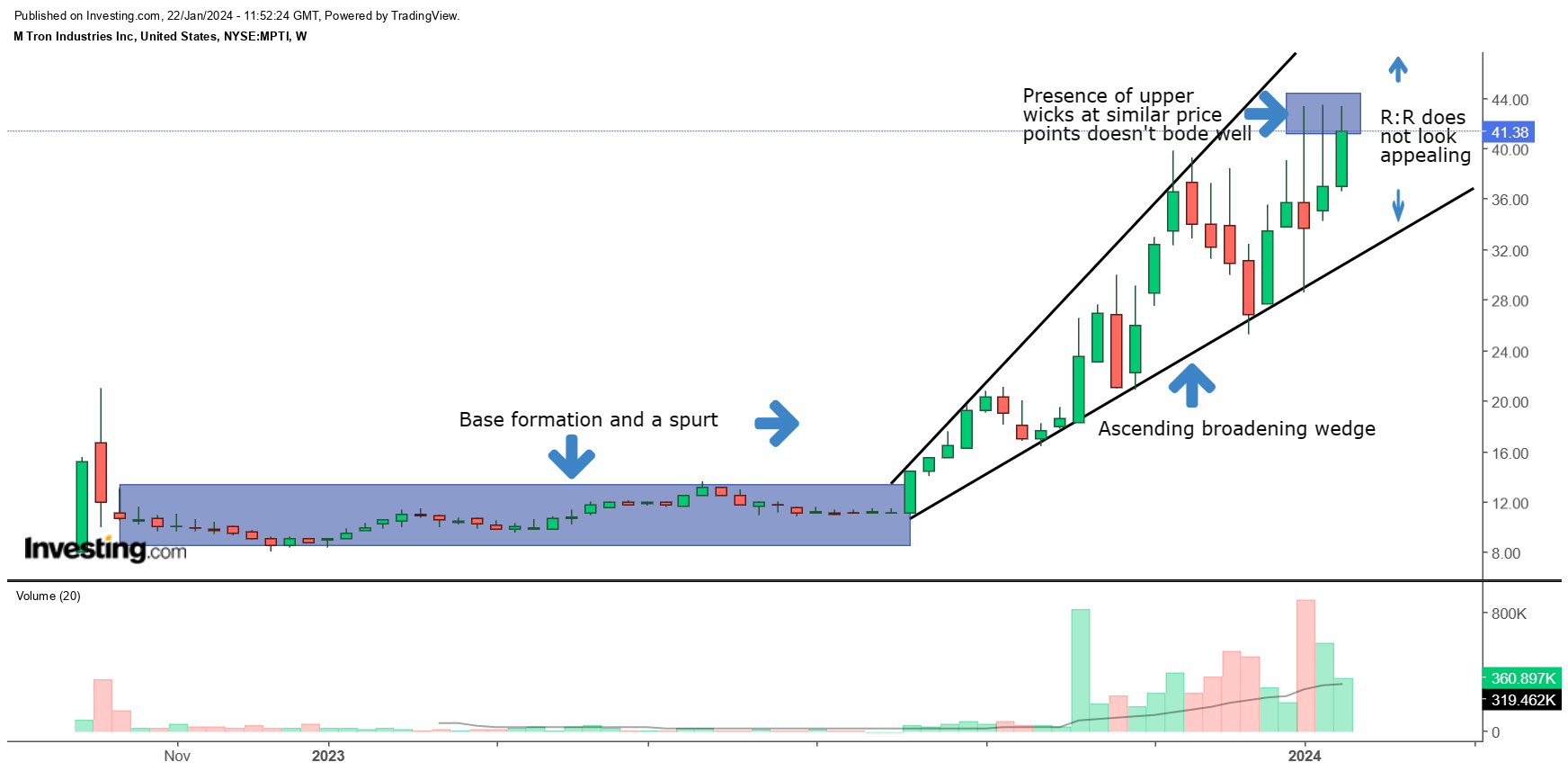

Lastly, if we take a look at MPTI’s personal value imprints on the weekly chart, we expect it might make sense to not be too bullish right here. The chart exhibits us how the inventory had constructed an extended base from Oct 2022 till July 2023 after which we noticed a drastic shift within the vary of its candles. Principally from August final yr, till now, the inventory has been trending up within the sample of an ascending broadening wedge, which on the face of it isn’t essentially the most excellent sample to construct scale.

Investing

Inside this channel, the reward to danger at present value ranges doesn’t look too interesting and even in any other case discover that the final 3-4 weekly candles have been characterised by some lengthy higher wicks, which counsel fatigue at increased ranges, and the tenuous however rising optimism of the bears.

All in all, contemplating the valuation and technical narratives, we don’t really feel that MPTI would make an excellent purchase proper now.