The outside of a NAPA auto components retailer. slobo

Lately, I’ve added a twist of secular progress to my investing technique. This may be noticed with my purchases of the likes of Amazon (AMZN) and Alphabet (GOOGL) within the final couple of years.

At my core, nonetheless, I stay a dividend progress investor targeted on shopping for qualitative companies at favorable valuations. That is exactly why my portfolio is loaded with dozens of Dividend Kings and/or Dividend Aristocrats.

Over time, Dividend Aristocrats and Dividend Kings do fall from grace. Nevertheless, I imagine {that a} well-diversified portfolio and occasional monitoring of such companies (e.g., promoting as fundamentals deteriorate) permits for outperformance over the long term.

Hartford Funds – The Energy Of Dividends

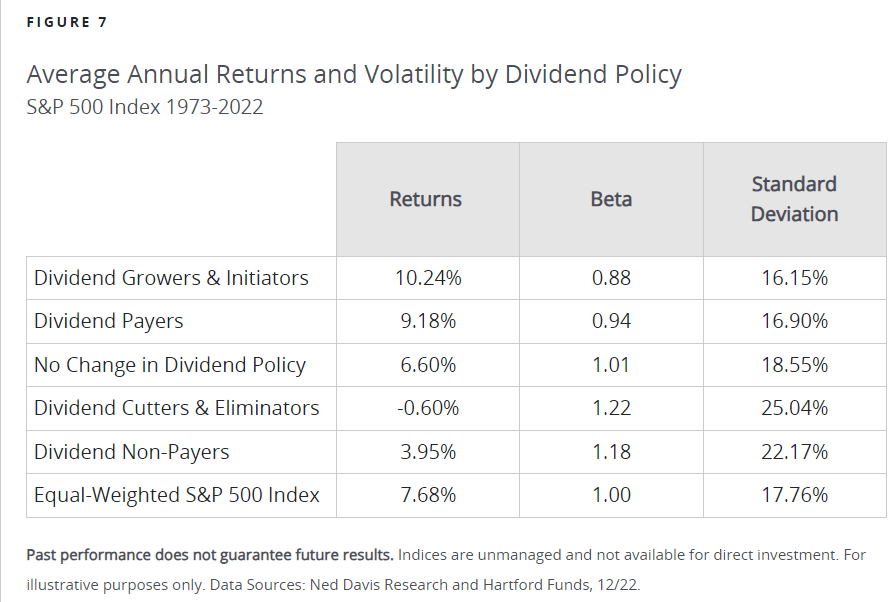

From 1973 to 2022, dividend growers and initiators, as a category delivered 10.2% annual total returns. That is considerably higher than the 7.7% annual whole returns that an equal-weighted S&P 500 (SP500) index generated. Put one other approach, an funding quantity within the dividend growers and initiators would have turn out to be 3.5X extra useful than the identical funding within the S&P 500 by the top of the interval.

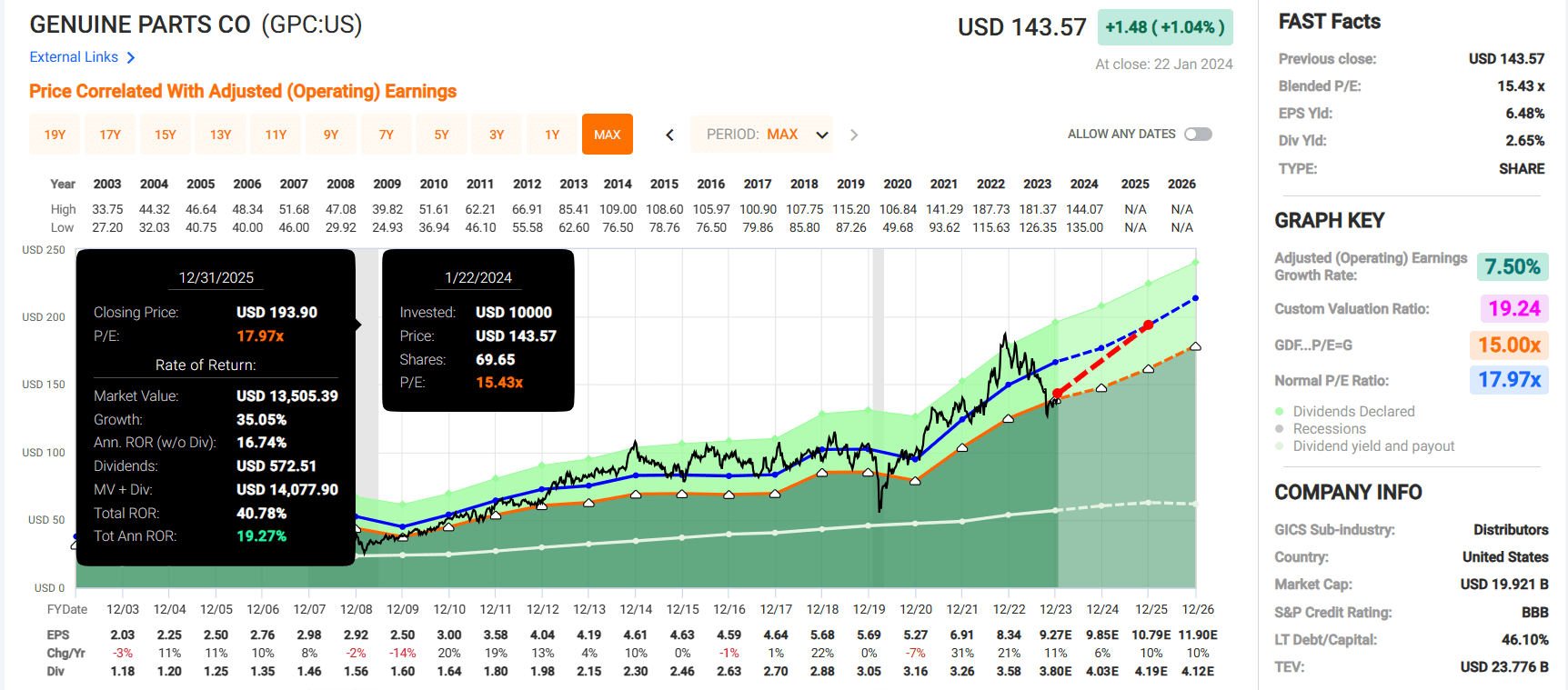

Real Elements Firm (NYSE:GPC) is a Dividend King, with 67 consecutive years of dividend progress to its credit score. The final time that I lined the Dividend King was in June 2021, once I rated it a maintain. At the moment, I favored Real Elements’ fundamentals. Nevertheless, I did not just like the valuation. As my dialogue of fundamentals will bear out, I nonetheless imagine that it’s nonetheless a basically sound enterprise. However the valuation stays a bit an excessive amount of for my liking to justify an improve to a purchase score.

Dividend Kings Zen Analysis Terminal

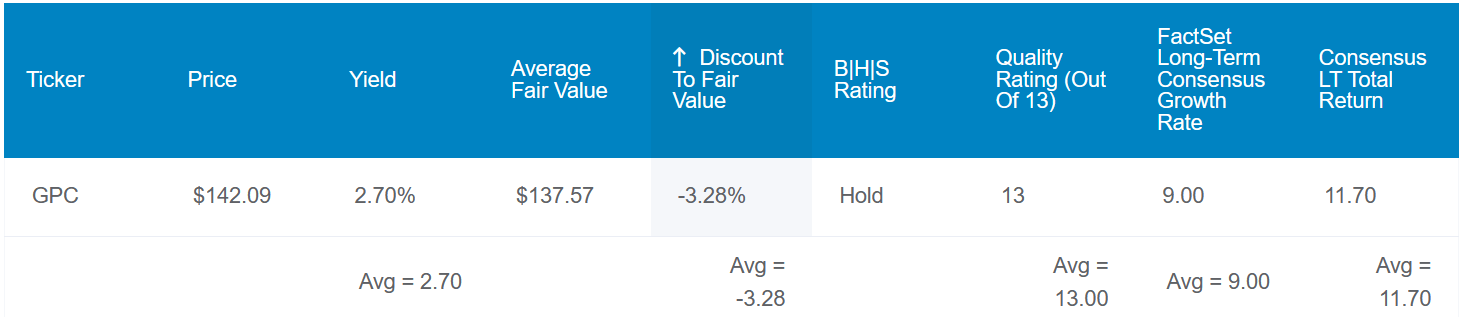

Real Elements’ 2.7% dividend yield is fairly engaging when stacked up towards the 1.4% yield of the S&P 500. That is very true when contemplating that it ought to have ample room to increase its dividend progress streak for the foreseeable future.

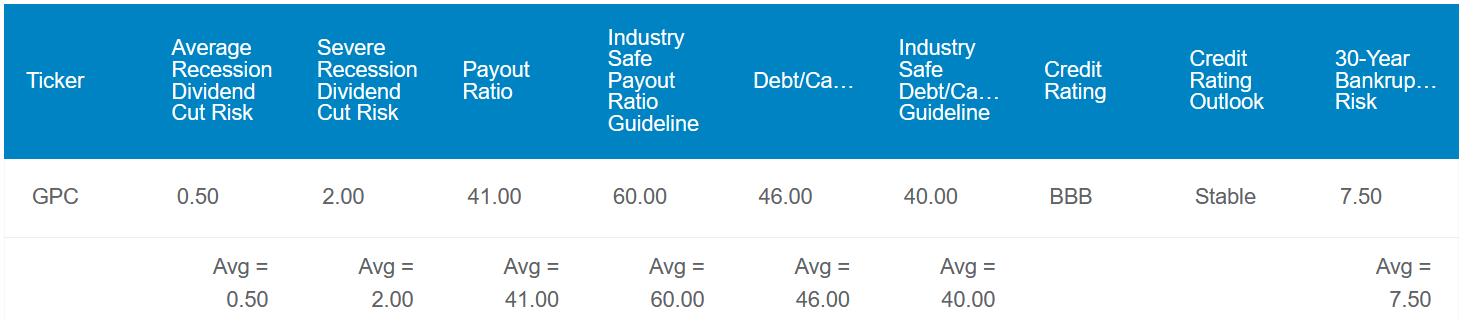

That’s as a result of, for one, the 41% EPS payout ratio is nicely beneath the 60% EPS payout ratio that score businesses need for Real Elements’ {industry}. The 46% debt-to-capital ratio can also be barely elevated past the 40% that score businesses need. Thus, Real Elements’ debt is rated BBB by S&P on a secure outlook.

The corporate’s 0.5% threat of a dividend reduce within the subsequent common recession is the bottom allowed worth within the Dividend Kings Zen Analysis Terminal. Even in a extreme recession, this threat rises to simply 2% – – greater than the 1% flooring, however not considerably so. For some perception into how these dividend reduce threat estimates are calculated, they’re based mostly on quite a lot of metrics. These embrace an organization’s payout ratio and debt-to-capital ratio versus the industry-safe ratios set forth by score businesses.

Dividend Kings Zen Analysis Terminal

The largest downside to Real Elements could also be its valuation. Utilizing the historic dividend yield and P/E ratios as a proxy (i.e., a mean of 10-year and 25-year valuation metrics), its shares might be price $138 every. Within the case of Real Elements, I imagine these metrics to be honest since fundamentals (e.g., progress) are about the identical versus these durations per a take a look at FAST Graphs. Relative to the present $142 share worth (as of January 23, 2024), that means Real Elements is 3% overvalued.

If the corporate grows as anticipated and reverts to its honest worth, listed below are the overall returns that it may ship over the approaching 10 years:

- 2.7% yield + 9% FactSet Analysis annual progress consensus (affordable in my view given Real Elements’ low- to mid-single-digit internet gross sales progress, margin enlargement, and share repurchases) – 0.3% annual valuation a number of contraction = 11.4% annual whole return potential or a 194% 10-year cumulative whole return versus the 9.8% annual whole return potential of the S&P or a 155% 10-year cumulative whole return

A Blended Quarter However Robust Outcomes Nonetheless

Real Elements Q3 2023 Earnings Press Launch

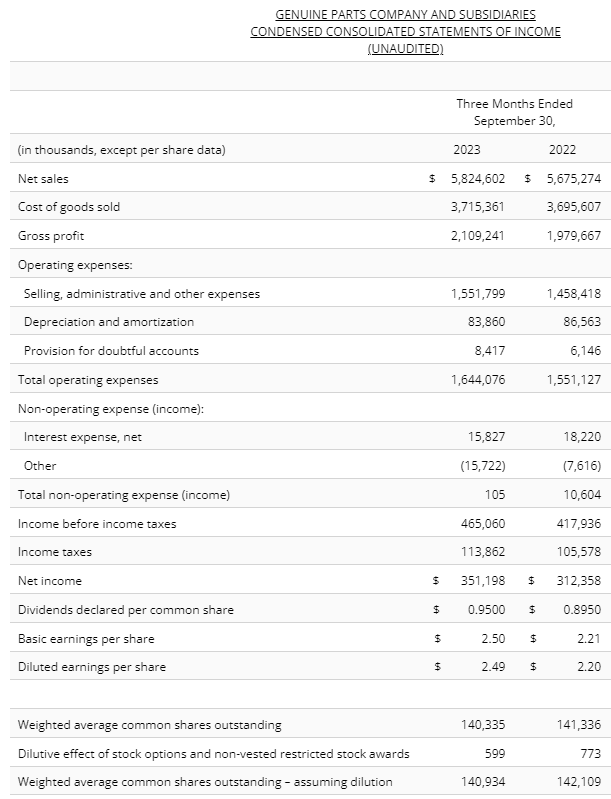

Falling $90 million wanting the analyst consensus for internet gross sales, Real Elements wasn’t capable of pull off a double beat within the third quarter. Even so, the corporate’s $5.8 billion in internet gross sales represented 2.6% progress over the year-ago interval.

Real Elements’ income progress was pushed by a number of elements. First, comparable gross sales grew by 0.5% in the course of the third quarter (0.6% for the automotive phase and 0.3% for the commercial phase). Subsequent, bolt-on acquisitions made inside every phase contributed to 1.7% of internet gross sales progress for the quarter (2.4% in automotive and 0.6% in industrial). Third, favorable overseas foreign money translation within the automotive phase (1.1%) offset unfavorable overseas foreign money translation within the industrial phase (-0.3%). That chipped in 0.5% internet gross sales progress within the quarter. Lastly, a 0.2% adverse impression from different elements within the automotive phase partially countered internet gross sales progress to the tune of 0.1% in the course of the quarter.

Real Elements’ adjusted diluted EPS climbed 11.7% year-over-year to $2.49 for the third quarter. That was $0.07 greater than the analyst consensus. Improved working effectivity helped the corporate’s non-GAAP internet revenue margin to broaden by 40 foundation factors to six% within the quarter. Mixed with the higher internet gross sales base and decrease share rely, that’s how Real Elements’ adjusted diluted EPS progress outpaced internet gross sales progress in the course of the quarter (particulars within the earlier three paragraphs sourced from Genuine Parts’ Q3 2023 Earnings Press Release).

Looking forward to the fourth quarter (earnings are anticipated to be introduced on Feb. 16), analysts anticipate $5.66 billion in internet gross sales. That will suggest 2.5% progress over the $5.52 billion in Q4 2022 internet gross sales. From my view, I’m inclined to agree with the analyst consensus. Real Elements’ modest comparable gross sales progress and bolt-on acquisitions ought to assist the corporate to fulfill these forecasts.

Moreover, the analyst consensus is that Real Elements will put up $2.20 in adjusted diluted EPS. That will equate to a 7.3% progress fee over the year-ago interval. Once more, that is wise for my part. That is as a result of I additionally imagine that internet gross sales progress, margin enlargement, and share repurchases can drive such degree of progress.

The momentum can also be clearly on the corporate’s facet, with 8 out of 10 EPS revisions being upward within the final 90 days. Lastly, the $9.89 in adjusted diluted EPS projected for 2024 can be a wholesome 6.7% progress fee over the $9.27 consensus for 2023 (information within the paragraph based on Searching for Alpha).

Shifting to the steadiness sheet, the corporate’s debt to adjusted EBITDA was 1.6X as of September 30. That is nicely beneath the focused leverage ratio of between 2X and a pair of.5X per CFO Bert Nappier’s opening remarks in the course of the Q3 2023 earnings call. Additionally, the corporate had $2.2 billion in out there liquidity on its steadiness sheet on the finish of the quarter.

Ample Free Money Circulation Can Assist Dividend Development

Within the final 5 years, Real Elements’ quarterly dividend per share has grown by 31.9% cumulatively to the present fee of $0.95 – – a 5.7% compound annual progress fee. I’d count on dividend progress to stay a minimum of as vigorous within the years to return.

That is as a result of, by means of the primary three quarters of 2023, Real Elements posted $732.6 million in free money move. Towards the $393.4 million in dividends paid, that may be a 53.7% free money move payout ratio (information from web page 8 of 31 of Genuine Parts’ Q3 2023 10-Q Filing). That leaves the corporate with adequate capital to pay rising dividends, repurchase shares, and sustain with debt obligations.

Dangers To Contemplate

Real Elements is a high quality enterprise, but it surely nonetheless faces dangers that might harm the funding thesis.

The automotive and industrial components industries are aggressive. If the corporate desires to take care of and construct its market share, it might want to maintain delivering worth to its clients. In any other case, the corporate’s market share and progress prospects may diminish over time.

One other threat to Real Elements is the potential for a cybersecurity breach. Even with its spending devoted to updating its IT programs, there is no such thing as a assure {that a} breach will not ever occur. If such an occasion have been to happen on a large enough scale, it may compromise delicate buyer, worker, and provider knowledge. That might end in a lack of belief within the firm’s manufacturers and litigation that might harm its progress story.

Lastly, Real Elements’ automotive retailer manufacturers are primarily independently-owned shops (6,679 of 9,801 as of the top of 2022). If these franchisees have been to be in battle with the corporate, that might weigh on gross sales since Real Elements sells stock from its company-owned distribution facilities to those franchisees (web page 5 of 93 of Genuine Parts’ 10-K filing).

Abstract: Ready For A Higher Lengthy-Time period Threat/Reward Proposition

FAST Graphs, FactSet FAST Graphs, FactSet

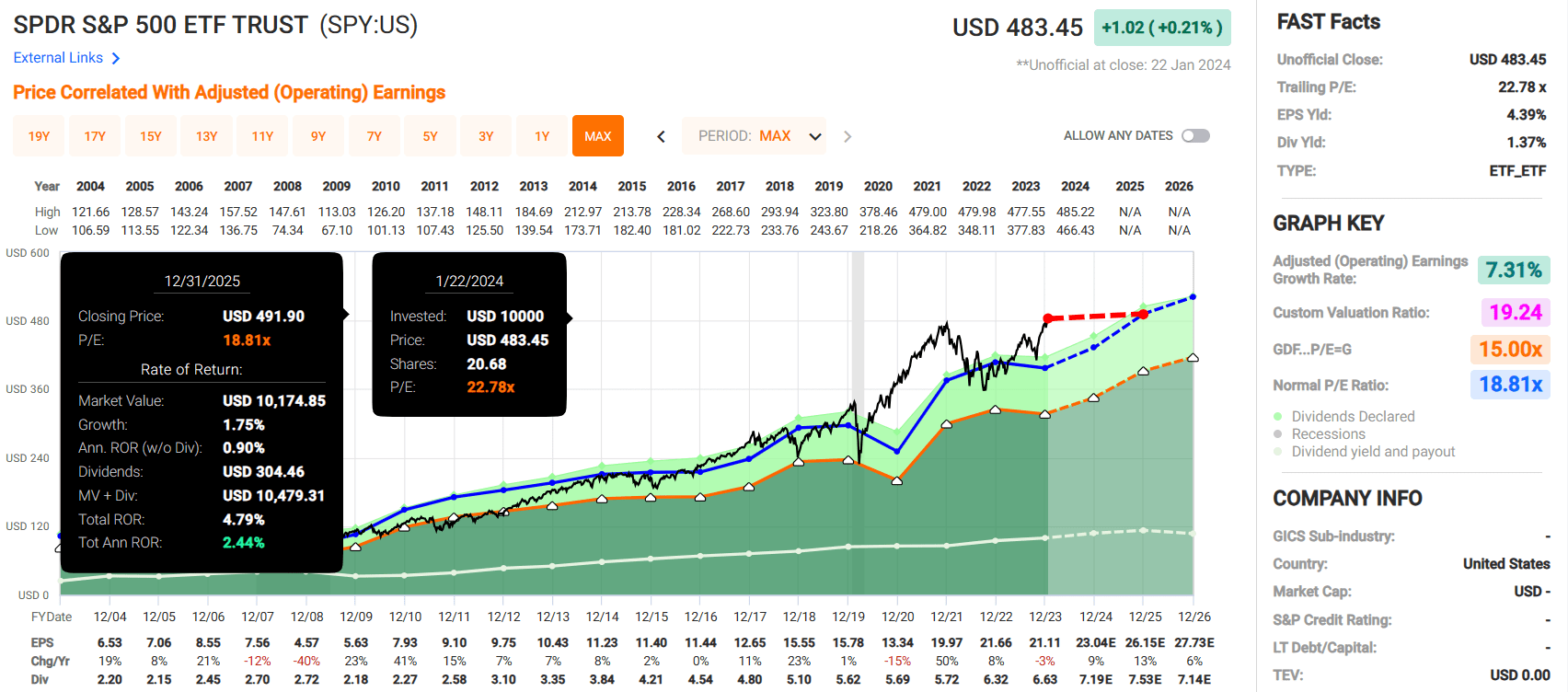

Primarily based solely on its 15.4 blended P/E ratio, Real Elements may have some upside forward within the subsequent couple of years. That is beneath its regular P/E ratio of 18. If it returns to this valuation a number of and grows as anticipated, 41% cumulative whole returns might be generated by means of 2025. That is much better than the 5% cumulative whole returns predicted for the SPDR S&P 500 ETF Belief (SPY) over that point.

Nevertheless, I purchase corporations as a lot for the subsequent 10 years and past. On the present valuation, I am not all for including to my place. It’s because I wish to construct a margin of security to dramatically enhance my odds of incomes 10% annual whole returns. If Real Elements ups its dividend as is predicted subsequent month and there’s a pullback to the low- $130s, I’d take into consideration upping my score to a purchase. For one, the beginning yield can be nearer to three%. Additionally, this valuation would offer a cushion for modest misses of the analyst progress consensus for my part. Collectively, this might make Real Elements a compelling purchase in my view.