NurPhoto/NurPhoto through Getty Photographs

Introduction

Nike (NYSE:NKE) is a kind of uncommon corporations that upon listening to their title, virtually everybody (regardless of how a lot investing expertise they’ve) can perceive who they’re, what they do and the way precisely they earn a living. That is due to the formidable model popularity they’ve constructed up over years of working to change into the biggest vendor of sports activities footwear/garments on the earth – and the enterprise of promoting garments is not inherently laborious to grasp.

What is difficult to grasp nevertheless, is the place precisely Nike is headed in the long run and if their present valuation is sensible primarily based on the present monetary place they’re in. It is a firm I’ve seen pop up a couple of instances on X (previously Twitter) saying it is a whole lot within the present worth vary. So after lacing up my monetary evaluation boots, I came upon that Nike’s fundamentals ought to make it a slam dunk in the long run – nevertheless, the sneaky curveball right here is that the valuation may simply not be interesting on the present second relying in your danger tolerance, making Nike a purchase with sure situations.

What’s Nike’s alternative?

In a nutshell, Nike produces and sells athletic associated objects, equivalent to footwear, garments or equipment/gear. They do that by their platform they name “NIKE direct operations” – which is a mix of their retail shops and e-commerce platforms. They use this platform to promote merchandise wholesale or to different distributors.

Due to this fact, their enterprise mannequin has a couple of development vectors they will leverage. Beginning with the obvious – the rising demand for athletic footwear. That is Nike’s bread and butter and makes up roughly 68% of their whole income. On the finish of 2022, the global athletic footwear market was estimated at $133 billion {dollars} and is anticipated to develop at a 4.9% CAGR to succeed in $196 billion by 2030. Whereas this is not the very best development charge on the earth, it is positively sufficient to permit Nike to develop its income at a good charge every year. What we have to see most on this class nevertheless is innovation. Every year the footwear have to be improved upon to ensure that Nike to remain related, which to their credit score they’re doing very properly on. Of their Q3 conference call, they talked about their success with their Ultrafly working shoe, their 3 soccer footwear (the Phantom Boot, the Tempo and the Mercurial) and the expansion of their Jordan model, which is now the quantity 2 model in North America.

The following alternative is with the global athletic clothing market, which makes up 28% of their income. This market has been estimated at $303 billion in 2021 and anticipated to develop at 5.8% CAGR to succeed in $450 billion by 2028.

As soon as once more, this CAGR is not excessive sufficient to warrant an excited celebration, but it surely’s nonetheless robust sufficient to permit Nike to develop its income. What’s extra thrilling nevertheless, is Nike’s deal with the ladies’s facet of their enterprise. Nike has estimated that round $9 billion of their enterprise is because of ladies’s merchandise and that 40% of their members are ladies clients – a determine that’s nonetheless rising and can more than likely overtake the lads in some unspecified time in the future. Why is that this so thrilling? Firstly the women’s athletic footwear market is at the moment rising quicker than the lads’s market – however is definitely predicted to overhaul the lads’s by 2030.

We see an excellent higher scenario with the ladies’s athletic clothes market, which isn’t solely the bigger market at 60% of world income, but it surely’s additionally estimated to develop at a considerably greater CAGR than the lads’s facet – a indisputable fact that Nike might be profiting from. The worldwide ladies’s athletic clothes market is estimated to develop at a 6.4% CAGR from 2023 up till 2028, in comparison with the lads’s which is barely anticipated to develop at a 4.8% CAGR till 2028. Nike additionally acknowledged of their newest convention name that their ladies’s enterprise has grown excessive single digits on common over the previous 3 years. Along with this additionally they acknowledged that their leggings, Zenvy, Go, and Universa, at the moment are above the $100 worth level, which they beforehand had not achieved. It is clear that Nike understands their market extraordinarily properly and is taking steps to develop each the highest and backside line.

Talking of the underside line, I might anticipate this to enhance by an honest margin sooner or later. This is because of their introduced plan to avoid wasting a cumulative $2 billion over the following 3 years, which I’ve determined to separate into incremental $333 million compounding financial savings as a measure of simplicity. My expectations are that Nike’s margins start to enhance throughout the board from 2025 FY onwards.

Their last alternative is with their e-commerce platform. It is clear that the buyer is trending in the direction of on-line procuring, with worldwide e-commerce revenue projected to develop at an 8.95% CAGR till 2028. Nike is at the moment profiting from this development. Working example, Nike Model digital gross sales accounted for about 25% of their whole income for his or her 2023 FY, and grew at a whopping 24% y/y. I might anticipate the digital gross sales for 2024 FY to be weaker because of the aforementioned robust comps usually, nevertheless from 2025 onwards we ought to be seeing wholesome development on this metric because of the increasing market.

One factor I actually like about Nike is their capability to acquire athletic endorsements and partnerships. Simply within the final quarter, Kelvin Kiptum attained the Marathon World Report and LeBron James led his group to the NBA event championship – each sporting Nike merchandise and the well-known Nike tick icon. These are the form of sponsorships which can be priceless and can in fact increase income. On the alternative facet to this nevertheless, is the unhealthy publicity when a well-known athlete decides to publicly half with Nike. A latest instance of this was when Tiger Woods parted ways with Nike only a few weeks in the past. Whereas this parting was amicable, it actually would not have executed Nike any favors – particularly to any hardcore Tiger Woods followers. Total nevertheless, this upside of Nike capitalizing on this chance far outweighs the draw back danger.

What about Nike’s administration group?

Nike has a well-seasoned and dependable administration group. John Donahoe has been the president and CEO of Nike since 2020 and has served on the board of administrators since 2014. The earlier CEO and president Mark Parker nonetheless serves on the board of administrators and serves as the manager chairman. Talking of the board of administrators, there are some very large names equivalent to Tim Cook dinner – who most individuals would acknowledge because the CEO of Apple. Total, the expertise is unquestionably there to steer Nike in the best course.

What about Nike’s monetary place?

Nike’s monetary place is nice. For his or her 2023 FY, they’ve printed about $4.9 billion in FCF and $3.23 of GAAP EPS. I imagine they need to beat each these metrics this 12 months, though by how a lot stays to be seen. I might anticipate the underside line to extend round 10%, give or take a bit, for his or her 2024 FY. I do suppose income development might be significantly weaker, because of the 9.65% high line development final 12 months being an extremely troublesome comp for them – contemplating that is bigger than the CAGR of their market (as proven earlier).

The following quarter may even not be too scorching, contemplating they’ve introduced pre-tax restructuring prices of roughly $400 million to $450 million on account of their plans to streamline their enterprise – a sensible transfer contemplating they will be saving $2 billion in the long run. Nonetheless the quick time period will sadly take successful. Their latest quarter nevertheless was positively good so far as effectivity goes. They reported GAAP EPS of $1.03, a rise of 21% y/y. It was additionally nice to see enlargement of their gross margin by 170bps, exhibiting they imply what they’ve stated about changing into a extra environment friendly enterprise.

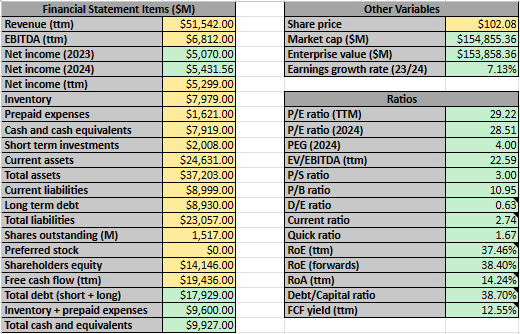

Nike’s stability sheet can be respectable, with roughly $9.9 billion in money and money equivalents and $8.9 billion in long run debt. Relating to the monetary ratios within the beneath screenshot, they’re… fascinating to say the least. Nike is producing some actually good metrics, equivalent to the wonderful RoE, FCF yield, present/fast ratios and D/E yield. Nonetheless there are some metrics which can be really not that nice, such because the very excessive PEG and P/B ratios. It is a blended bag for certain, however total there are no evident purple flags – just a few issues to concentrate on:

Creator’s calculations

their trailing P/E ratio, that is at the moment sitting round truthful worth at 29.2. To place issues in perspective, this sometimes trades between 25 and 35. This might be a horny ratio for the time being contemplating the upcoming price financial savings ought to enhance Nike’s backside line over the following few quarters.

It is a related story with their EV/EBITDA ratio, which is at the moment at 22.6. That is on the decrease finish of the historic vary which Nike tends to commerce at – between 20 and 30, nevertheless the upcoming price financial savings means this might be a bit decrease as soon as the upcoming quarters start to print.

What’s Nike’s intrinsic worth?

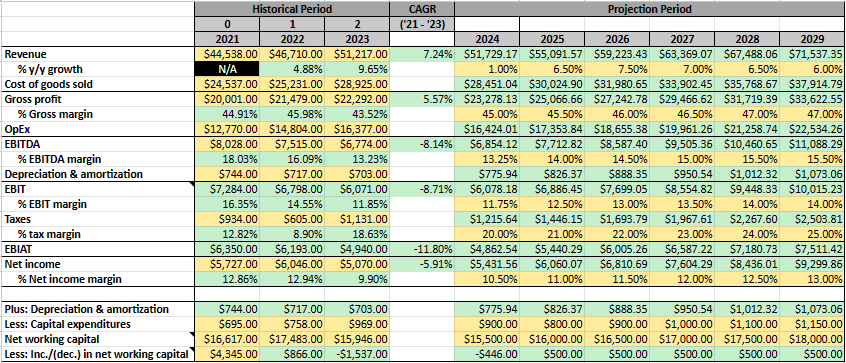

As typical, I’ve determined to undertake 3 totally different approaches to find out the truthful worth per share of Nike’s inventory: A internet revenue evaluation, a EV/EBITDA evaluation and a DCF evaluation. However firstly, please see the beneath monetary projections, which I am going to present a short dialogue on:

Historic financials and projections

Creator’s calculations

As acknowledged earlier, I anticipate income development to be put on for 2024 FY, however then reaccelerate heading into 2025 FY. I imagine it will begin to decelerate in the direction of the top of the last decade to be extra in step with the CAGR of their market. I additionally suppose we must always see continuous margin enlargement as the associated fee financial savings measures begin to take impact over the following few years. Nike has guided for $2 billion in cumulative financial savings, so I’ve determined to interrupt this down into $333 million blocks that accumulate every year – as a matter of simplicity. Both approach nevertheless, Nike has traditionally hit a 13% margin on the underside line, however has bother sustaining this constantly and has by no means had 2 consecutive quarters within the 14% vary. Due to this fact, whereas their effectivity mission may result in historic profitability, I feel it will be a mistake to forecast it with out proof first.

CapEx will more than likely decline/stay stagnant over the following few years as a part of Nike’s plan to cut back prices, however will choose up once more quickly after. I additionally suppose we must always see a gradual improve in internet working capital as Nike will increase their money readily available.

Internet revenue evaluation

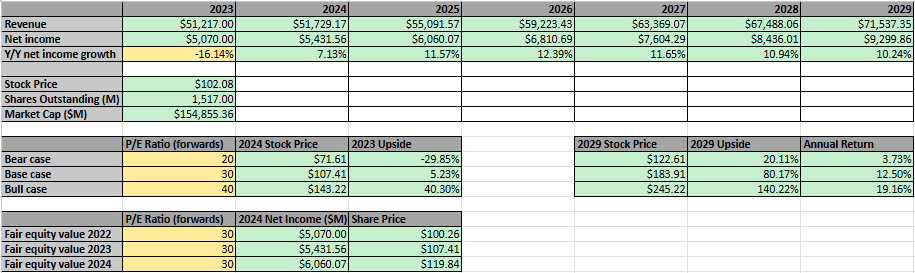

I’ve put collectively the beneath internet revenue evaluation primarily based on the above projections:

Creator’s calculations

Based mostly on the analysis I’ve executed, Nike ought to have a base case ahead P/E ratio of round 30. Though that is throughout the 25 to 35 vary I acknowledged earlier, I imagine that is positively a premium valuation – however there are a pair causes for this. Firstly, Nike will most positively enhance its backside line over the following few years on account of its elevated effectivity and secondly, corporations which have confirmed they will function properly are likely to commerce at a premium.

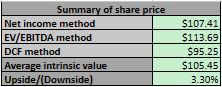

The remainder of their 2024 FY might be a bit rocky as acknowledged earlier, however they will more than likely hit round $5.4 billion or so, which means the truthful worth for this 12 months might be $107.41 – a 5.23% upside from the present worth.

As well as, if my projections are appropriate, a 30 P/E will enable the inventory worth to succeed in $183.91 by 2029 – implying a 80.17% return in 5 years.

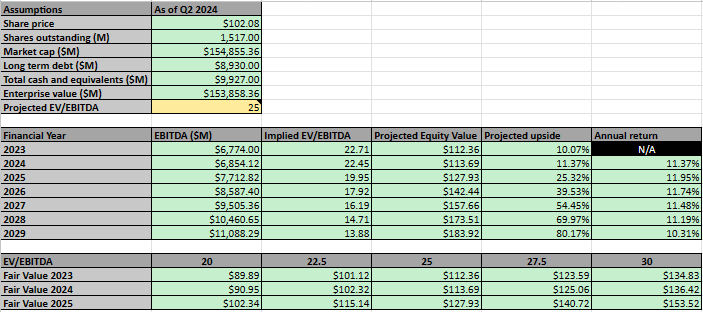

EV/EBITDA evaluation

I’ve put collectively the beneath EV/EBITDA evaluation primarily based on the sooner projections:

Creator’s calculations

I’ve determined that an EV/EBITDA of 25 ought to be truthful for Nike. That is proper in the midst of the 20 to 30 vary I acknowledged earlier. As soon as once more, I imagine that is buying and selling at a premium for a motive – you are buying a strong firm that can proceed to carry out into the long run.

As such, the truthful worth for Nike ought to be round $113.69 per share primarily based on the projected EBITDA for 2024. I’ve additionally performed a mini-sensitivity evaluation for the EV/EBITDA, which I feel can be affordable to make use of should you suppose this ought to be nearer to twenty. Personally I might discover it laborious to justify going nearer to 30 except you are anticipating an enormous ramp up in profitability.

Moreover, assuming my projections are appropriate, there may be an implication the inventory worth will attain $183.92 by 2029, which is almost an identical to the 2029 quantity I’ve forecast in my earlier internet revenue evaluation.

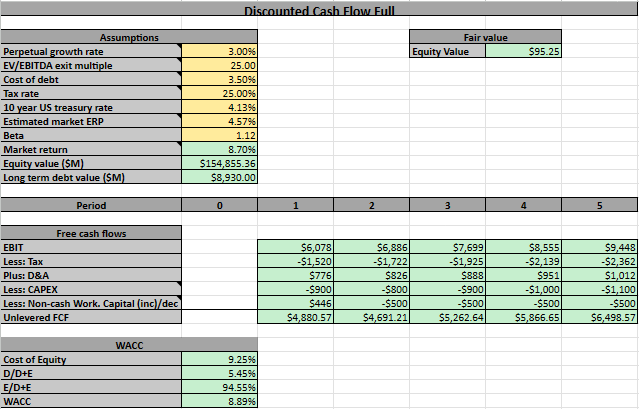

DCF evaluation

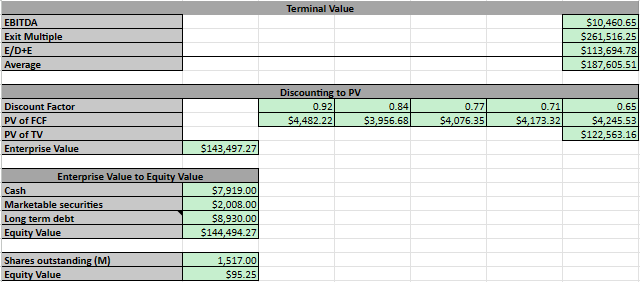

I’ve put collectively the beneath DCF evaluation primarily based on the sooner projections. Please be aware that I’ve calculate the terminal worth utilizing the typical of the EV/EBITDA exit a number of technique and WACC technique:

Creator’s calculations Creator’s calculations

I’ve determined to make use of a 3% perpetual development charge for Nike – which is between the typical inflation charge and GDP development charge of two.9% and three.2%. I additionally imagine a 25 EV/EBITDA exit a number of is suitable, primarily based totally on the identical reasoning I acknowledged in my EV/EBITDA evaluation. I calculated the price of debt from Nike’s newest 10-Okay after which added an approximate 0.5% margin of security, because of the 2 additional quarters. I used an efficient tax charge of 25% as a conservative assumption and selected the ten 12 months US treasury charge as the chance free charge, which was 4.13% on the time of writing.

Nike’s present agreed beta is 1.12 in accordance with varied monetary providers and I used a market return of 8.7%, which is a mix of the chance free charge and market ERP (at the moment round 4.57%)

Utilizing these numbers, I’ve calculated a justifiable share worth of roughly $95.25. I feel that is affordable and does not appear out of the abnormal – albeit it does indicate a draw back from the present worth.

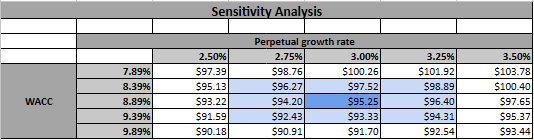

I’ve additionally performed the beneath sensitivity evaluation if you wish to transfer the numbers a bit, nevertheless I am comfortable holding issues as they’re:

Creator’s calculations

Common share worth

As per the beneath screenshot, the typical of those 3 strategies offers us a justifiable share worth of $105.45 – marking a 3.30% upside from the present share worth. This subsequently implies that Nike is barely undervalued and is subsequently a purchase.

Creator’s calculations

What are the dangers?

The obvious danger is Nike’s effectivity prices not working as deliberate. They’ve promised us $2 billion in financial savings over the following 3 years, in the event that they fail to ship on this or worse – do not ship on any effectivity efforts, then the inventory won’t carry out as predicted.

The following fundamental danger is Nike not innovating and shedding floor to competitors. I discover this a bit laborious to imagine as Nike has already confirmed throughout the previous few a long time they do know innovate and keep related.

The opposite most evident danger is because of my evaluation – the three.3% upside has no margin of security. Usually I like shares to have a minimal 10% upside to mitigate towards any unexpected circumstances – something larger than 30% is absolutely once I begin to get . 3.3% then again actually does not depart a lot room for error. If Nike drops the ball on only a few numbers, that upside may simply flip right into a draw back.

Conclusion

This one was difficult to determine a ranking on. I used to be deciding between maintain and purchase, however finally the purchase ranking received the battle. The primary causes for this choice is that Nike has a strong enterprise mannequin and a historical past of being a dependable firm. Additionally they pay a dividend, so should you’re searching for a dividend play that will not see any excessive drops in your capital, then Nike is unquestionably an possibility because of the valuation not being too excessive. All of that is much more true in case you have a long run outlook and are not fearful about quick time period fluctuations.

Nike ought to be value round $105.45, nevertheless you want a margin of security in your shares or simply need some upside potential, I would suggest ready a little bit bit – however provided that you are snug doing so. For instance, I do not personal any Nike, but when we see any significant pullback near the low 90’s, I am going to take into account selecting some shares up. Nonetheless, if we do not see that pullback and Nike’s inventory solely goes up from right here – I am additionally okay with that. In different phrases, should you’re okay with presumably not proudly owning the inventory, then ready for a doable retracement will be the clever choice right here.

The primary danger to Nike’s enterprise mannequin is that they fail to stay revolutionary and lose market share to rivals. As acknowledged within the dangers part, I do suppose that is unlikely. Nike have proven use they are often trusted to function and carry out properly over time. I do not see why the long run can be any totally different proper now.

For those who’re searching for a spot to park your cash and earn some dividends over the approaching years – Nike is an effective place to start out wanting. They have been rising their dividend cost every year since 2004 and I feel it is unlikely they’d need to break this streak and hurt their popularity as a strong dividend payer going ahead. As for me, I will be watching this one intently and seeing if an honest entry level arises for me to “just do it” and begin taking part in ball with Nike.