miniseries

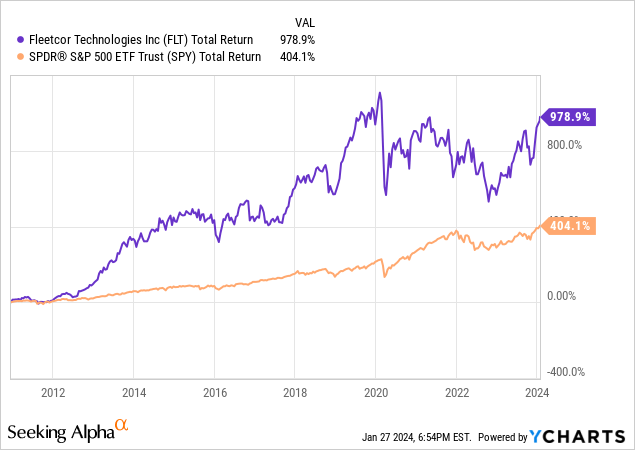

FLEETCOR Applied sciences (NYSE:FLT) has delivered sturdy outcomes for shareholders since turning into a public firm in December 2010. Since its IPO, FLT has delivered a complete return of 979%. Comparably, the S&P 500 has delivered a complete return of 404% throughout the identical time interval.

FLT’s sturdy efficiency for shareholders has been pushed by sturdy efficiency in its underlying enterprise as EPS has grown at an almost 15% CAGR over the previous 10 years.

Regardless of having a market cap better than $20 billion, FLT is roofed by comparatively few analysts on Looking for Alpha and has not been coated since October 2023. The three most up-to-date Looking for Alpha articles on the inventory have all been Maintain rankings. There are 4 the explanation why I’m extra bullish on the inventory and am initiating protection with a purchase ranking:

1. Excessive diversified and high-quality enterprise mannequin

2. Potential beneficiary of elevated EV adoption

3. Aggressive share repurchase program

4. Extremely enticing valuation vs the broader market

5. Enticing valuation relative to historic norms & cheap valuation vs friends

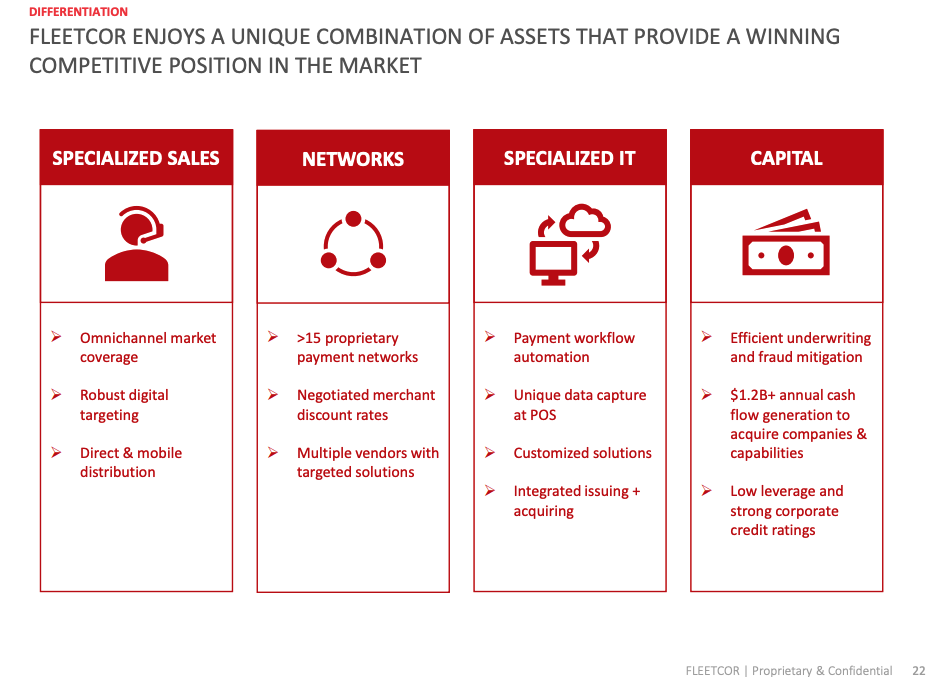

1. Extremely diversified and high-quality enterprise mannequin

FLT is a number one international enterprise fee firm that focuses on serving to corporations higher handle and monitor expense-related buying. The Firm’s present segments embrace Fleet (~38% of income), Company Funds (~27% of revenues), Brazil (~14% of revenues), Lodging (~15% of revenues), and Others (~7% of revenues.)

The Fleet section, which incorporates the corporate’s gas options enterprise excluding Brazil, generates income via program charges comparable to transaction charges, card charges, community charges, expenses, and interchange.

The Company funds section consists of the corporate’s company funds enterprise exterior of gas and lodging. The Lodging section supplies resort fee companies and generates income based mostly on the distinction between the quantity charged to a buyer and the quantity paid to a resort for a given transaction and commissions paid by accommodations. The Brazil section consists of all the firm’s operations in Brazil whereas the Different section consists of the Reward and Payroll card companies.

The corporate generates ~58% of whole income within the U.S., 14% in Brazil, 12% within the U.Ok., and 17% in different nations.

FLT is clearly diversified when it comes to each its product providing and its geographical publicity. I view this as a key constructive as the corporate shouldn’t be overexposed to potential challenges in any given a part of its enterprise or geographic area that will come up.

Along with being extremely diversified enterprise, FLT is a really high-quality enterprise. Whereas the corporate faces competitors in all of its core companies, FLT has constructed up aggressive benefits because of community results and specialization. FLT enjoys a really sturdy buyer retention fee of 91.2% which exhibits the stickiness of the corporate’s enterprise mannequin.

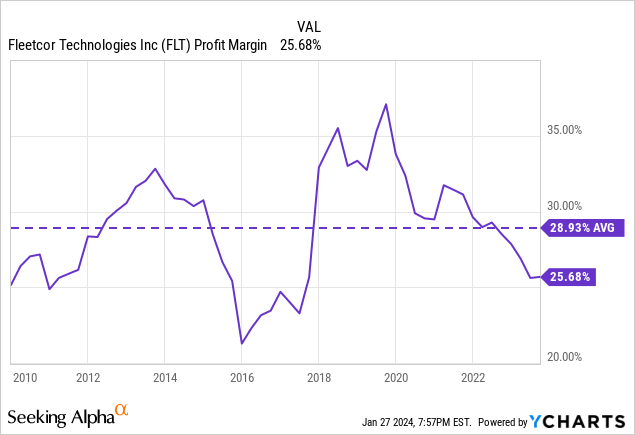

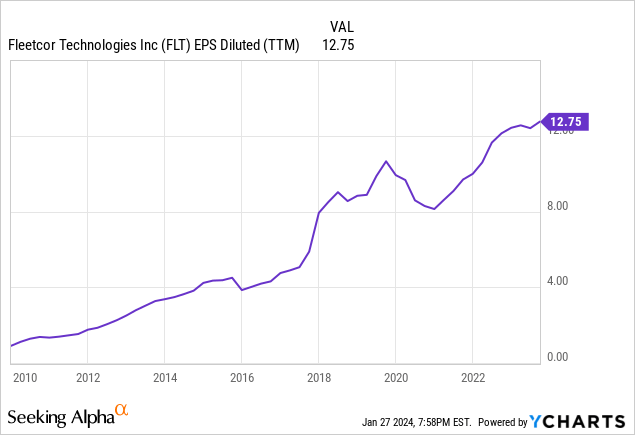

Additional proof for the comparatively sturdy aggressive benefit that the corporate enjoys may be seen within the excessive and secure revenue margins and regular EPS development. Traditionally, FLT has achieved a mean revenue margin of ~29% and has grown EPS at an almost 15% CAGR over the previous decade.

FLT Investor Presentation

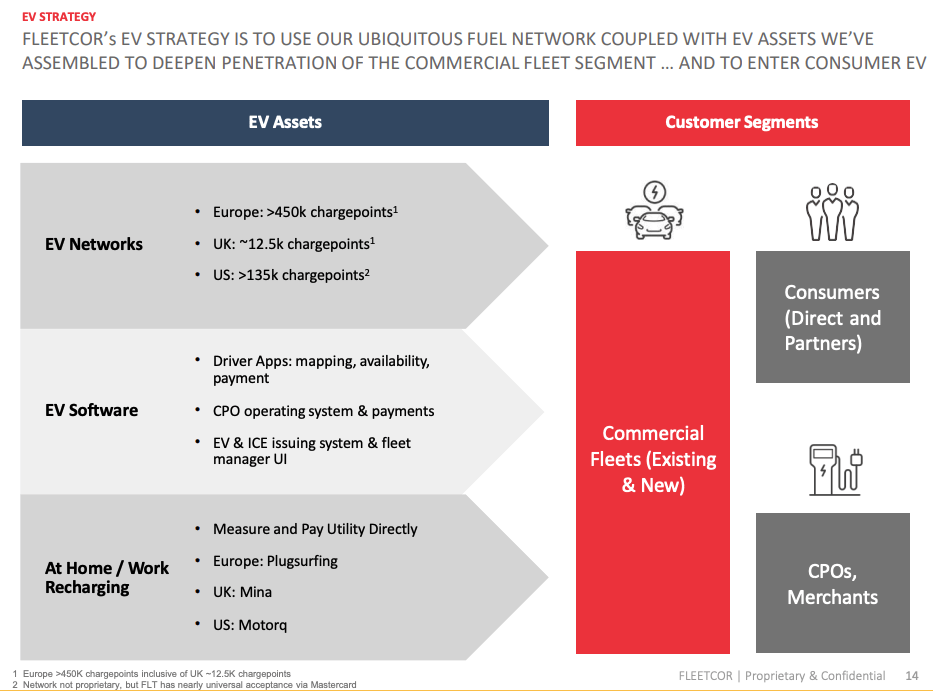

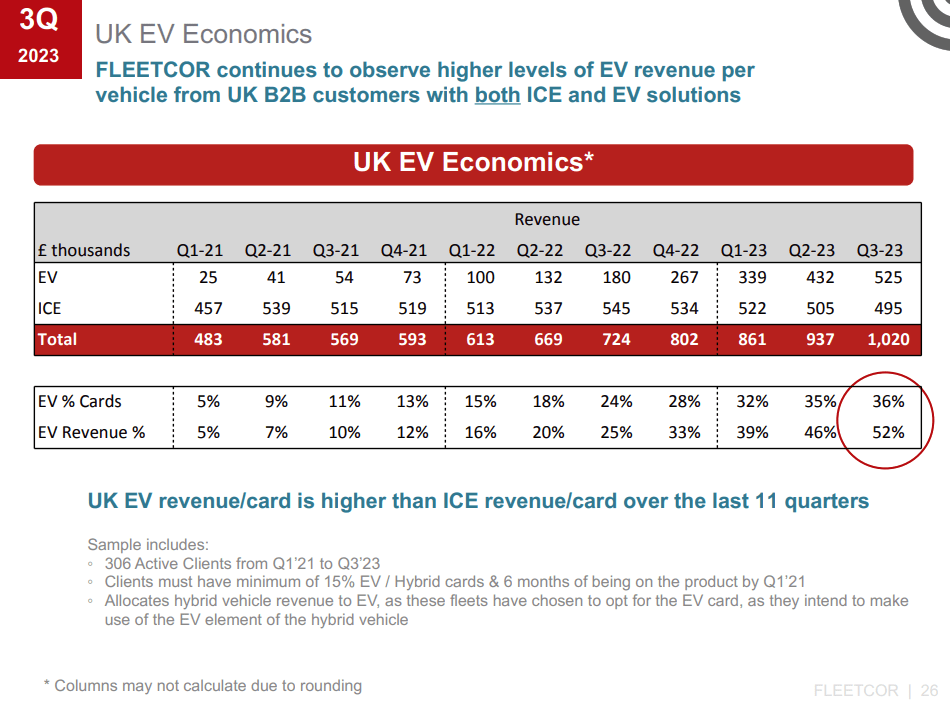

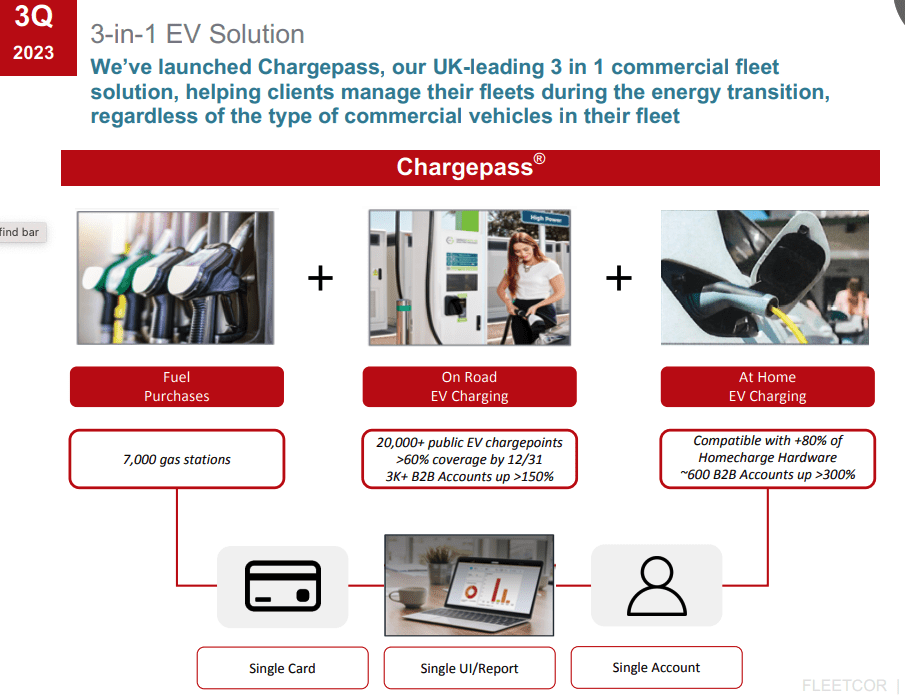

2. Potential beneficiary of elevated EV adoption

Given FLT’s vital gas enterprise, one pure investor concern is {that a} transition in direction of EVs could end in diminished income as the price for charging is considerably lower than gasoline. Nevertheless, the corporate has constructed out a really sturdy EV providing which incorporates ~600k in community chargepoints and complex EV software program and measurement programs.

The corporate is furthest together with its EV product rollout within the UK the place it has launched Chargepass, a 3 in 1 business fleet resolution. To date, the outcomes have been spectacular with EV-driven income now accounting for greater than ICE-driven income. EV playing cards presently account for 36% of whole playing cards within the U.Ok. however have contributed 52% of whole income. This implies that EV playing cards end in extra income for FLT than conventional ICE playing cards. The implication of that is that as EV adoption expands globally, FLT is poised to learn.

FLT Investor Presentation FLT Q3 Investor Presentation FLT Q3 Investor Presentation

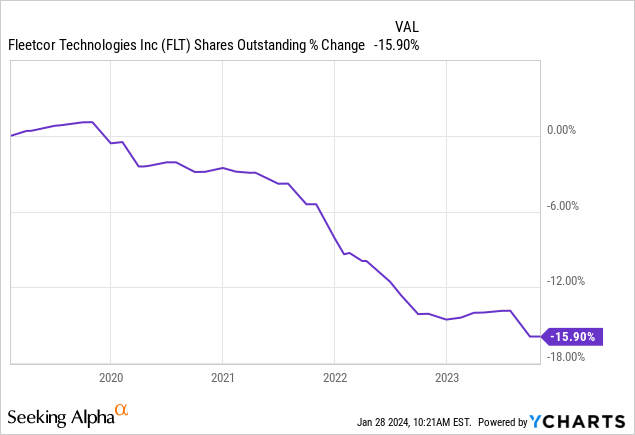

3. Aggressive share repurchase program

Over the previous 5 years, FLT has been an aggressive repurchaser of its personal shares. As proven by the chart beneath, the corporate has diminished its share rely by almost 16% over that point interval.

Throughout Q3 2023, FLT repurchased $530 million of inventory together with a $450 million accelerated share repurchase settlement which was completed at a value of $270.04 per share. As of the tip of the quarter, the corporate had $700 million remaining beneath the present authorization. At present costs, this represents ~3.3% of the corporate’s whole market capitalization.

I view the buyback favorably because it means that administration views repurchasing its personal shares as extra enticing than returning capital to shareholders by way of dividends. Furthermore, when fundamentals and valuation are sturdy, as I consider the case is with FLT, I desire to see corporations repurchasing shares versus paying out dividends. Share repurchases permit buyers to compound their funding on a tax deferred foundation and provides buyers higher management concerning the timing of realizing positive factors for tax functions.

I count on the corporate to proceed with large-scale repurchases within the months forward, which must be supportive of the inventory.

4. Extremely enticing valuation vs the broader market

FLT trades at 15x consensus FY 2024 EPS and 13x consensus FY 2025 EPS. Comparably, the S&P 500 presently trades at 22x consensus FY 2024 earnings.

Along with buying and selling at a decrease valuation than the broader market, FLT has higher development prospects. FLT is presently anticipated to develop FY 2024 EPS by 14% and FY 2025 EPS by 16%. Nevertheless, I view these estimates as pretty conservative given the truth that the corporate has guided to fifteen%-20% annual EPS development over the medium time period. Comparably, the S&P 500 is predicted to develop FY 2024 earnings by ~12% and traditionally has grown earnings at a high-single digit fee. Thus, based mostly on FY 2024 development figures FLT trades at a ahead PEG of 1.07 whereas the S&P 500 trades at a ahead PEG of 1.83.

Given the truth that FLT is a high-quality enterprise with above-market development prospects, I consider it ought to commerce at the least in keeping with the broader market. A ahead P/E ratio of 22x would suggest a good worth of $426 per share for FLT, which represents a ~45% premium from present costs.

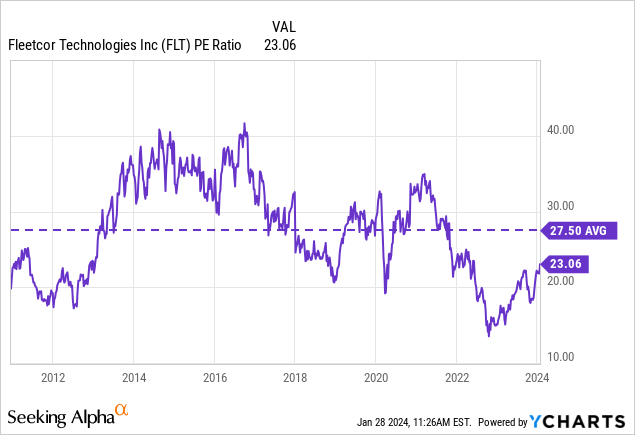

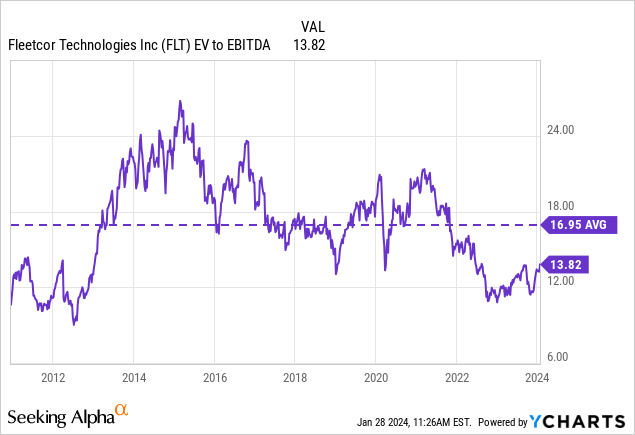

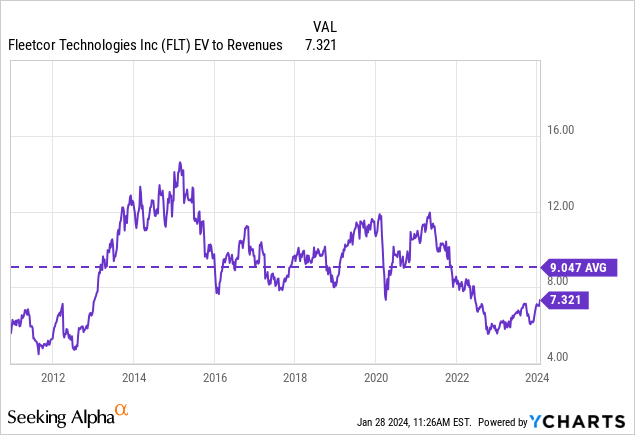

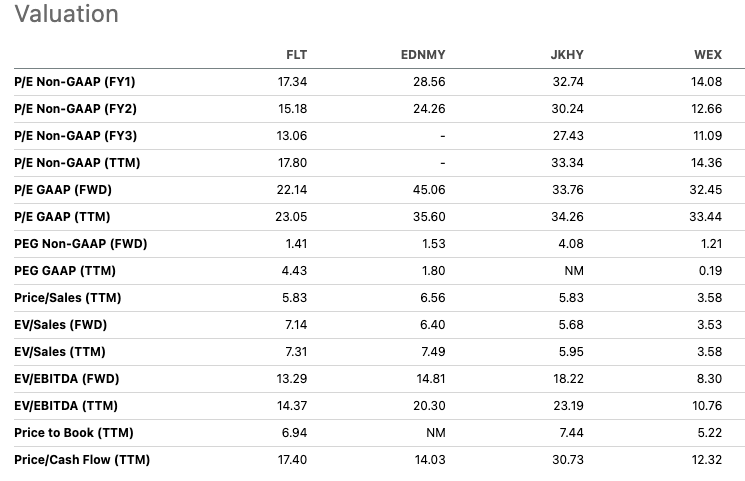

5. Enticing valuation relative to historic norms & cheap valuation vs friends

FLT is presently buying and selling at a considerable low cost to its common historic norm valuation. Traditionally, FLT has traded at a mean trailing P/E ratio of 27.5x vs 23x presently. FLT can be buying and selling at a reduction relative to its common historic EV/EBITDA and EV/Income valuations.

I don’t view the low cost as being warranted as FLT has future development prospects that are in keeping with historic development prospects.

FLT is buying and selling at an affordable valuation vs friends within the funds enterprise. WEX Inc. (WEX) is arguably the corporate’s closest peer and trades at a modest low cost to FLT however is rising extra slowly, has much less scale, and is a lower-margin enterprise. JKHY trades at a better valuation than FLT however is uncovered to a unique a part of the funds worth chain as it’s extra targeted on fee software program options for small and midsize banks.

Looking for Alpha

This autumn 2023 Earnings Preview

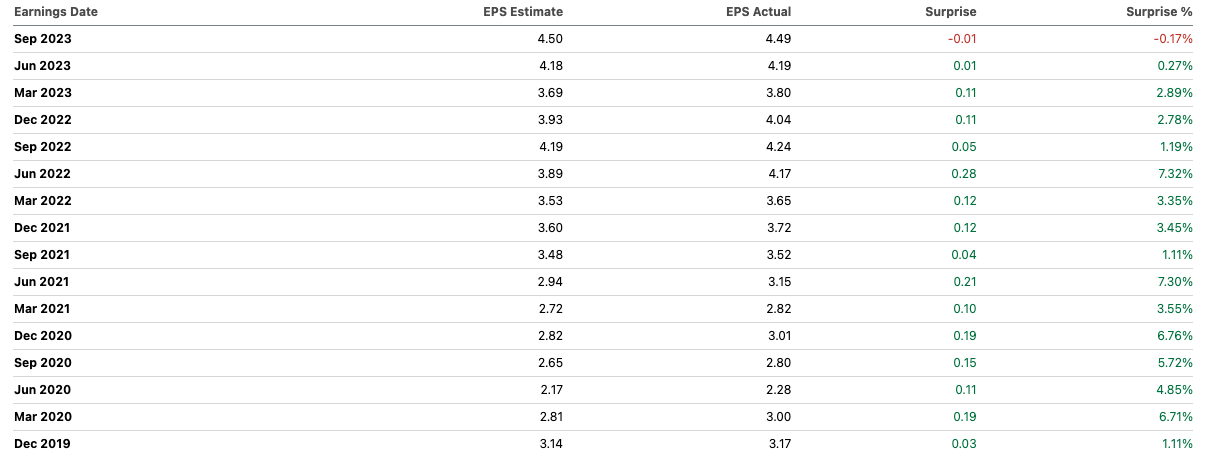

FLT is scheduled to report This autumn 2023 earnings on February 7, 2024, after the market closes. Consensus estimates name for the corporate to report normalized EPS of $4.48 per share which represents a ~10.9% on a year-over-year foundation. Income is predicted to return in at $970 million which represents a ~9.8% enhance on a year-over-year foundation. Over the previous 3 months, 6 analysts have raised their EPS estimates for the quarter whereas 8 analysts have lowered their EPS estimates for the quarter. This implies there may be some uncertainty concerning the course of issues heading into the report.

Traditionally, FLT has virtually all the time exceeded consensus estimates. For that reason, I might not be stunned to see the corporate report better-than-expected earnings and the inventory transfer larger. I might view any pullback associated to slight earnings miss as a shopping for alternative.

Looking for Alpha

Dangers To Take into account

One threat to contemplate is that FLT is uncovered to broader financial situations. If the financial system have been to expertise a slowdown, then company spending would decline. Underneath these circumstances, FLT would discover it tough to fulfill present earnings expectations. I don’t presently count on a near-term financial slowdown however it’s a threat I proceed to watch.

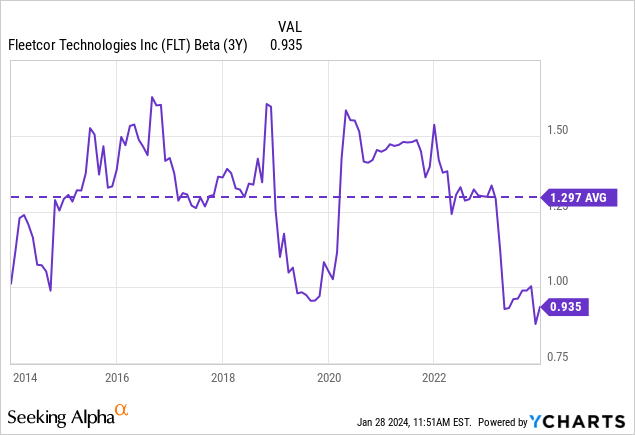

One other key threat to contemplate is rising rates of interest. Whereas the corporate’s leverage ratio of two.66 represents an enchancment from 2.8x on the finish of 2022, it stays reasonably excessive for a reasonably cyclical enterprise. A big enhance in rates of interest from right here would result in additional will increase in curiosity expense which might end in decrease EPS development than is presently anticipated.

The consequences of a reasonably cyclical enterprise and a average quantity of leverage may be seen in the truth that FLT has exhibited a historic common 3-year trailing beta of 1.3x. Thus, buyers contemplating an extended place in FLT must be conscious that the inventory tends to be extra risky than the broader market.

Conclusion

FLT is a high-quality enterprise with a historical past of delivering sturdy outcomes for shareholders. The corporate advantages from community results and has a really excessive diploma of buyer retention. Regardless of working in a reasonably aggressive enterprise, FLT has been capable of constantly ship excessive revenue margins.

Latest success of the corporate’s EV-based enterprise within the U.Ok. means that the shift in direction of EVs could profit the corporate over the long run when it comes to elevated income alternatives.

FLT trades at a considerable low cost to the broader market regardless of having superior development prospects. I don’t view this low cost as warranted and consider FLT ought to commerce at a a number of which is at the least in keeping with the broader market. Primarily based on this view, I consider an affordable estimate of truthful worth for FLT is $426 per share.

Along with buying and selling at a extremely enticing valuation vs the broader market, I additionally view FLT’s present valuation as enticing relative to the corporate’s personal historic valuation vary.

For these causes, I’m initiating FLT with a robust purchase ranking. I might think about downgrading the inventory if the valuation turns into much less enticing or the corporate fails to ship EPS development in line or higher than present expectations.