vitpho/iStock through Getty Photographs

This text was coproduced with Wolf Report.

I do not thoughts sounding like a damaged file.

The truth is, I slightly prefer it.

It implies that I am of a excessive conviction within the firms the place my stakes are the very best.

So, when I’m updating right here on Agree Realty Company (NYSE:ADC), an organization I wrote about not that way back, I accomplish that as a result of the brief time period has modified when it comes to valuation, however the long-term outlook actually has not.

Agree is an chubby place (for Wolf and Brad).

Realty Earnings (O) is Brad’s largest stake (~10% publicity).

Each Realty Earnings and Agree Realty characterize very good investments right here at their respective valuations.

I’m of a agency stance right here that anybody not investing right here, and whose funding targets and portfolio methods truly line up with this firm, will remorse not investing right here in 5-10 years.

This was very true when each of those firms dropped throughout fall, and brief time period this has confirmed to be the case, however the current surge upward has been halted, and we have seen some softness within the valuation, which has moved Agree Realty again to a near-5% yield, which makes it of nice curiosity to me.

Agree Realty – Again to close 5% yield

With the case for rates of interest being unsure, some might ask why you ought to be investing in a 5% yield when many bonds and cash market funds present an identical type of return.

This is among the simpler questions for me to deal with.

The yield is just a small a part of ADC’s attraction – the mixture of capital appreciation and yield, coupled with what I argue to be one of the vital qualitative administration groups in triple-net.

Keep in mind, and have a look at the second article that I revealed this week.

I took a victory lap with a few of my higher investments within the final 6-9 months and gave you up to date value targets for them.

Agree Realty does have the potential to go down the identical highway, however I think about it a stretch to the place this actual property funding belief, or REIT, truly reaches a share value the place I’d think about promoting my shares.

I personal the REIT shares for qualitative publicity to interesting triple-net properties, coupled with what I view as a horny value for possession on this setting and contemplating the REIT’s profitability, together with the corporate’s well-covered and engaging 5%+ yield.

I don’t think about it unlikely for my month-to-month positions, which embody ADC, to begin offering me this yr with over $2,000 in money each month – and people are simply the month-to-month positions.

Whereas month-to-month cash is not an argument in and of itself to me – you additionally want to ensure it is sustainable and makes valuational sense – ADC has to me all of the indicators of a qualitative funding.

Its market cap of over $5B, its TSR of 25.9%, and its compounding of 11.3% since IPO, all of these indicators are of a qualitative administration and dealing enterprise mannequin.

What I like about ADC is that the corporate doesn’t skimp on high quality and doesn’t develop at any price.

It is one thing that I imagine the large Realty Earnings might study from.

I imagine that that is one thing ADC does lots higher – however it’s laborious to check the 2 regardless of their sector, as a result of there are funding and enterprise methods that work excellently for firms with sub-$10B market caps however which may work very in another way for a $100B market cap enterprise. It is the size query.

However Agree Realty is an organization that ought to be and deserves to be on the prime of your watchlist.

Its issuing of an elevated 2023E steering which is more likely to see funds from operations, or FFO, rising at 3-4% for the subsequent few years ought to put a lot of the fears and criticism of potential adverse progress to relaxation.

Whereas ADC will not be anticipated to offer outsized, double-digit progress, this was by no means an expectation I had for the corporate.

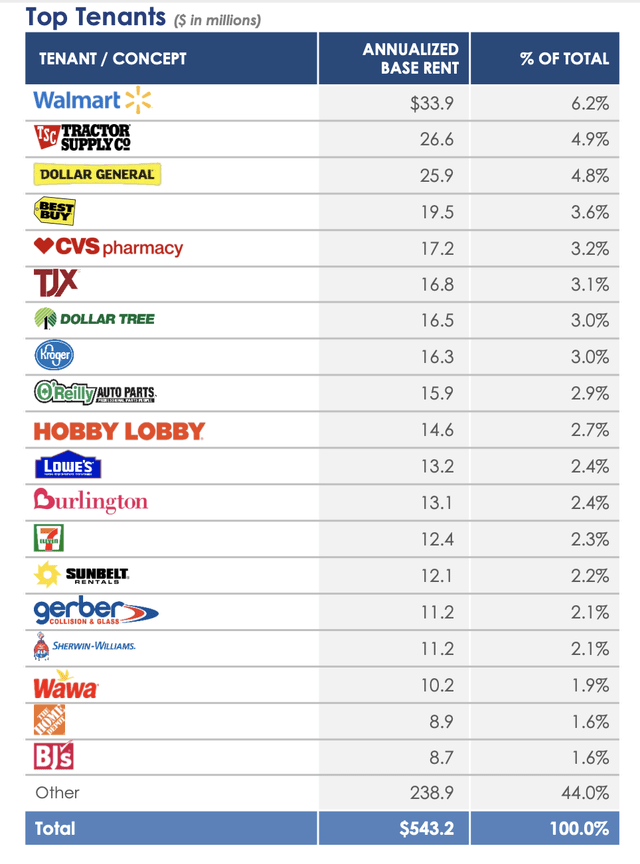

The primary argument right here is tenant high quality.

In contrast to O, we do not have a lot Walgreens (WBA) right here.

The truth is, not solely can we not have Walgreens within the prime 15, I’d say that we have no type of dangerous tenants in that checklist in any respect.

ADC IR

Oh, positive, you’ll be able to argue that CVS (CVS) is a pharmacy as nicely, however I’d argue that current historicals show it extra well-managed than Walgreens in each approach. Additionally, the tenant focus is much decrease right here, with solely Walmart at over 5%.

Virtually 70% investment-graded and even the unrated firms being companies like Aldi, you get an general snapshot of security that is pretty unparalleled on this discipline. The corporate focuses on e-commerce-resistant nationwide and super-regional retailers and corporations, with lower than 2% franchise-focused companies.

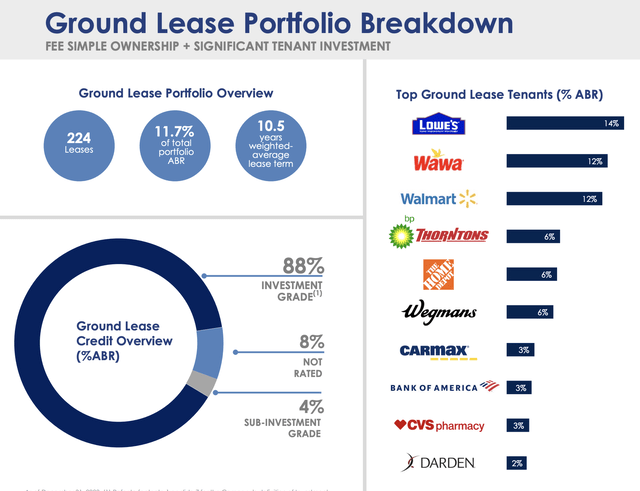

Along with the entire properties it owns, the corporate can also be a really prolific floor lease firm, with a good portion of those kinds of contracts.

ADC IR

How floor leases are structured signifies that tenants have considerably extra curiosity in sustaining the lease given their funding into that parcel, in flip providing the owner, ADC, some further security – and you may see the caliber of firms that maintain the bottom leases.

Even within the circumstances the place these expire, ADC has an outstanding historical past of capturing embedded worth at a 159% price.

There are examples the place the prior lease, to Chase Financial institution, was re-leased at a brand new price improve from beneath $30/sqft to over $46/sqft at a 15-year price with a ten% rental escalator each 5 years – almost doubling the ABR.

ADC is among the best-of-breed firms you discover in Triple-net.

Its disciplined acquisition technique, its portfolio administration, and it is “lean and mean” type of character regardless of a $5B+ market cap, which means it can’t be known as small, makes it straightforward to sing the corporate’s praises. It signifies that I as an analyst should be cautious in order that I don’t come throughout as any type of “fanboy” – I at all times wish to be very conscious of dangers and drawbacks right here.

However the easy truth is that I see only a few downsides with Agree Realty.

Why is that?

1. The corporate has been specializing in investing in omnichannel crucial actual property, recession-resistant properties, and full avoidance of JV’s or PE possession or stakes. Whereas I do spend money on PE, I additionally know the hazards that PE brings. This can be a world I am truly getting deeper into – and I encourage novices, if , to learn the e-book “The Private Equity Toolkit” By Tamara Sakovska, that gives an entry into the considering and “how the sausage is made” for these sectors. However whereas I like this for some sectors and companies, I would like ADC to remain away from this – they usually do.

2. The expansion potential, and by that I imply explosive 10-20% annualized base hire (“ABR”) or FFO progress for this firm is close to non-existent. That doesn’t imply there is no such thing as a potential for gradual and regular progress.

ADC IR

Sluggish and regular progress does imply that the corporate is more likely to see a better diploma of valuation and share value punishment throughout instances when cash, and, subsequently, rates of interest and risk-free charges, are increased/dearer.

This doesn’t hassle me, as a result of I imply to personal ADC for a really very long time, so I do know that in instances of decrease rates of interest, they may return up.

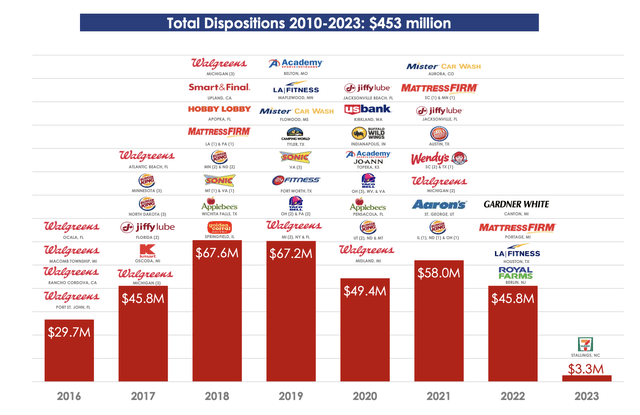

3. The corporate has confirmed, time and time once more, that it’ll proceed to speculate irrespective of the market local weather, so long as the deal is sensible. It’s going to additionally proceed to dump and divest properties. And administration has confirmed apt at recognizing “bad apples,” with one explicit one justifiably highlighted.

ADC IR

Not even Realty Earnings went this energetic.

I additionally wish to repeat once more, as I’ve in earlier articles, that any who argues security wants to know that the corporate has no maturities over $50M till 2028. That is 4 years of basically no maturities.

Debt to EV?

Under 28.5%.

Fastened expenses?

Lined at 5.1x, with web debt under 4.6x.

This is among the most conservative REITs in existence, and it was awarded BBB for it – and rightly so.

Capital markets stay extensive open for Agree, and ADC has confirmed, even throughout frothy durations, that it’ll not enable itself to be tempted to “bad practices,” similar to overleverage. The corporate has been under 4.5x since 2018, throughout your complete COVID-19 and “frothy” interval when different REITs and corporations dialed up their leverage as a consequence of, amongst different issues, FOMO.

How did that work out for a lot of of them?

Joey!

Joey Agree, CEO at Agree, is an everyday commenter on In search of Alpha, and who is aware of, he might drop in and say “hi” within the feedback under.

We actually like Joey’s transparency, one thing that we wish to see with extra CEOs within the REIT sector. Brad has interviewed Joey on many events, and he plans to take action once more after earnings (expected on February thirteenth).

Brad additionally met with Joey a number of weeks in the past at Agree’s new company HQ.

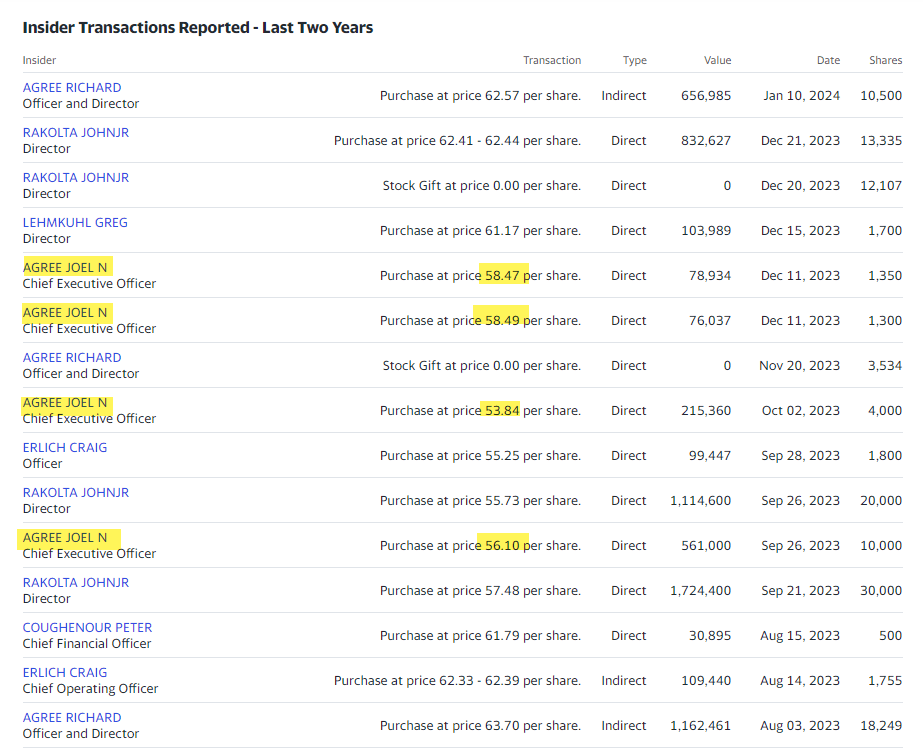

Joey has additionally been an everyday purchaser of Agree shares, one other indication of sturdy shareholder alignment.

Yahoo Finance

Joey owns round 554,000 shares (as of December 10, 2023), which interprets into a worth of slightly below $33 million.

Lastly, Joey and the Agree Realty board opted to start paying monthly dividends in 2021. This can be a big vote of confidence for retail traders, as these month-to-month funds function reminders that the enterprise is producing very secure and constant revenue.

Joey Agree has performed an important job and deserves the credit score for his sturdy alignment of curiosity with the Common Joe and Jane.

Valuation for Agree Realty

One of many core questions of any article or thesis I make is to ask if the valuation for a corporation is sensible to me.

You possibly can argue that ADC is in truth solely price 15x P/FFO with a progress price estimated between 3-4% FFO in an setting like this. That is tremendous, however you’d nonetheless recover from 8% per yr together with dividends.

That may not beat most indices constantly, however you are not shedding cash, and given the month-to-month well-covered dividends based mostly on the type of portfolio we’ve right here, that makes even that bearish situation an revenue investor “dream.”

Why a dream?

As a result of I do not view anybody that guarantees 7-19% yields, month-to-month or in any other case, sustainable over the long run. There’s often some “catch” with that. With ADC, I do not suppose there’s a catch.

However again to valuation.

Should you imagine that, you are additionally ignoring utterly your complete historical past of premiumization of this firm, and also you’re calling this firm price $60/share.

The issue with that’s that this solely is sensible on this very restricted snapshot of the market. Outdoors of this market, and out of doors of this price setting, and contemplating that ADC by no means has missed estimates – solely overwhelmed them or hit them – you need to query such a 15x valuation.

At 16x P/FFO, this firm, even at 3-4% FFO progress, annualized at double digits of 10.2%.

At 18x P/FFO, it annualized at shut to fifteen%.

So what do the historic averages say?

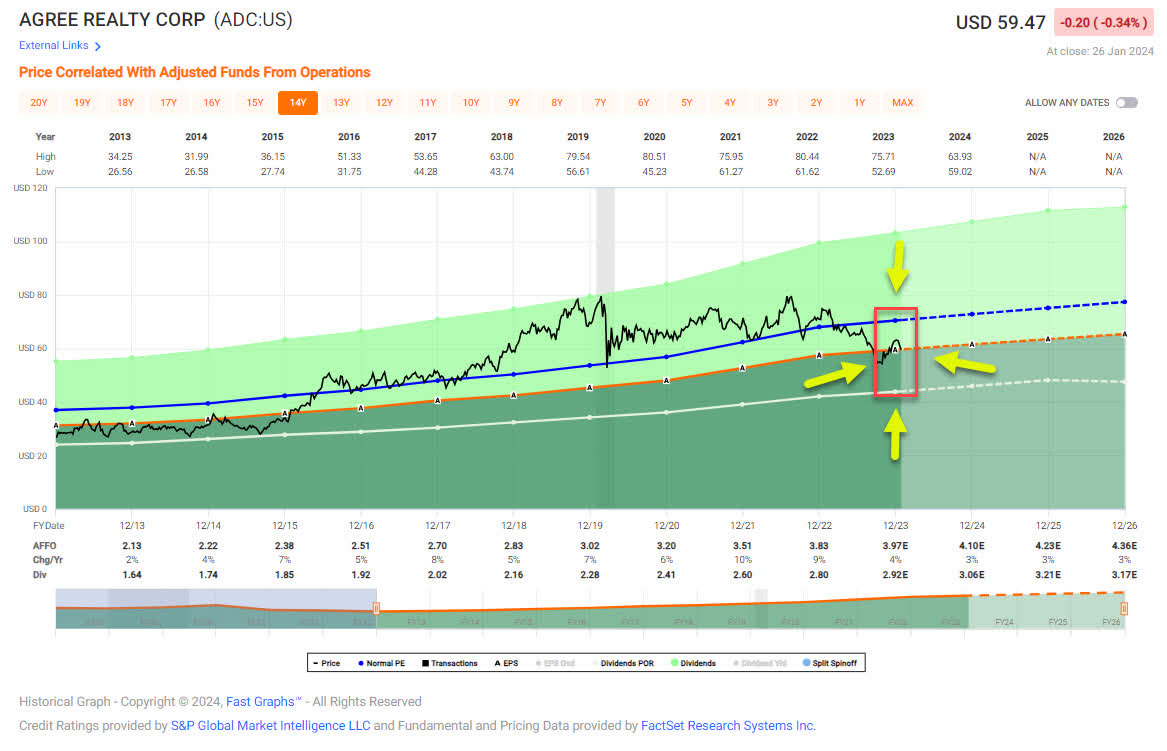

That it is price 17.6x on a 10-year, and 20x on a 5-year common.

FAST Graphs

Granted, we have seen this firm drop-down for intensive durations of time.

Years in truth.

Once more, would it not hassle me if it did?

Not likely – I might nonetheless get my yield, and the decrease publicity means I might justify extra shares.

I imagine the “truth” within the firm’s long run comes someplace between 16-19x P/FFO.

Meaning I think about wherever from 11-19% annualized to be possible even at this valuation, and that doesn’t embody dividend progress, which is presently estimated to succeed in $4.34 by 2026E, which might imply a 2026E funding yield at sub-$60 of 5.3%, which is the place we have been in October – once more, valuation issues.

FAST Graphs

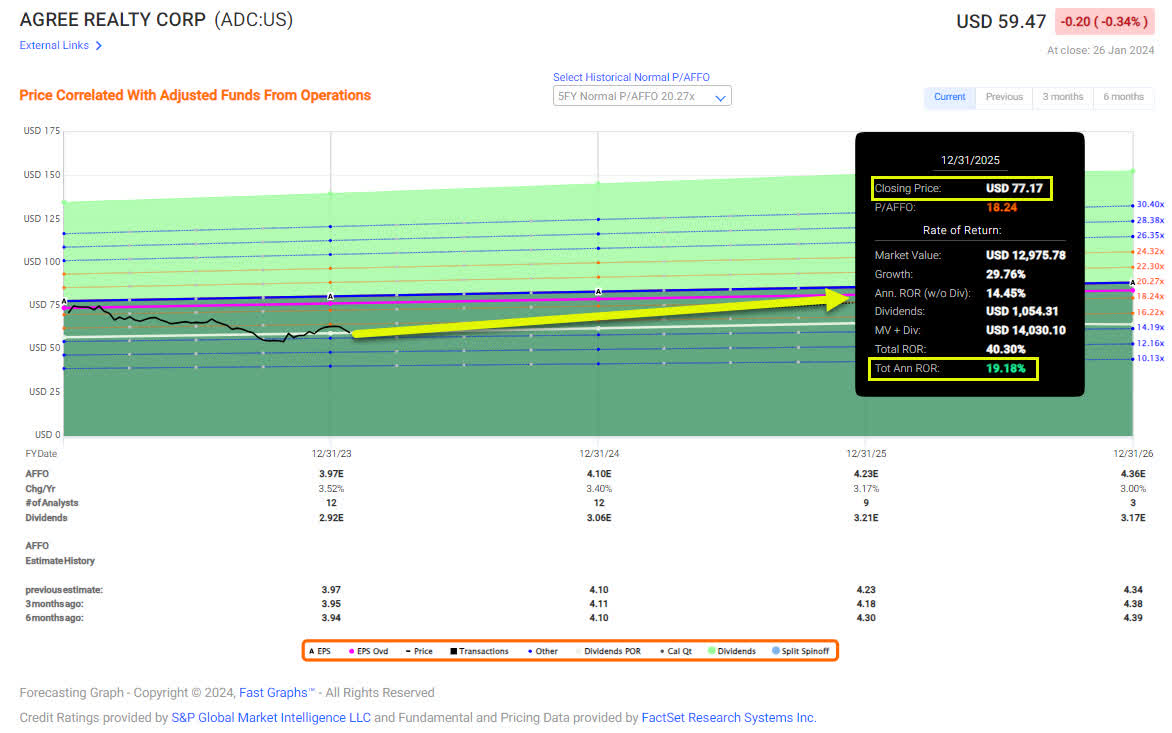

S&P International nonetheless has a value goal vary of $61 on the low aspect to $80/share on the excessive aspect. That is increased than we have seen within the final yr. Out of 14 analysts, 13 are at “BUY” or an identical optimistic score right here, giving us a really excessive diploma of conviction – and I agree with this.

Right here is my up to date thesis for Agree, and why I nonetheless view this as certainly one of my go-to-investments.

Thesis

- Agree Realty is, subsequent to O, one of the vital qualitative investments round in your complete REIT house. Whereas many alternatives do present a better, lifelike upside, there are only a few that provide risk-free-beating dividend yields with the potential for a reversal at such security. ADC is a month-to-month dividend payer with an important future – and I preserve pushing money to work right here.

- ADC makes up a considerable quantity of my conservative funding portfolio – each the non-public and the company one I run. It is also certainly one of my highest “ratings” on the market when it turns into low-cost.

- Agree Realty has a PT of no less than $75/share, giving it an upside of no less than 18% right here, and probably extra.

- Agree Realty is a “BUY,” and I nonetheless think about it to be “cheap” under $60/share.

Keep in mind, I am all about:

1. Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly large – firms at a reduction, permitting them to normalize over time and harvesting capital features and dividends within the meantime.

2. If the corporate goes nicely past normalization and goes into overvaluation, I harvest features and rotate my place into different undervalued shares, repeating #1.

3. If the corporate does not go into overvaluation, however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

4. I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (italicized).

- This firm is general qualitative.

- This firm is essentially protected/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is presently low-cost.

- This firm has a practical upside based mostly on earnings progress or a number of enlargement/reversion.

This firm fulfills each single certainly one of my funding standards barring cheapness – I am at a “BUY.”