matejmo

By Caglasu Altunkopru, Head of Macro Technique – Multi-Asset Options | Aditya Monappa, CFA| World Head – Multi-Asset Enterprise Improvement

After pandemic-era extremes, development and inflation ought to method historic averages in 2024. Right here’s how multi-asset buyers can reply.

The turmoil of the post-pandemic interval ought to proceed to subside this 12 months, leaving a “less exceptional” panorama for buyers to navigate. Inflation is cooling throughout most main economies, which is especially welcome information. Within the US, December’s Client Worth Index rose 3.3% 12 months over 12 months, effectively off its peak of 8.9% in June of 2022, however nonetheless above the Fed’s 2% goal. Central banks are beginning to sign willingness to chop charges, ought to this development maintain.

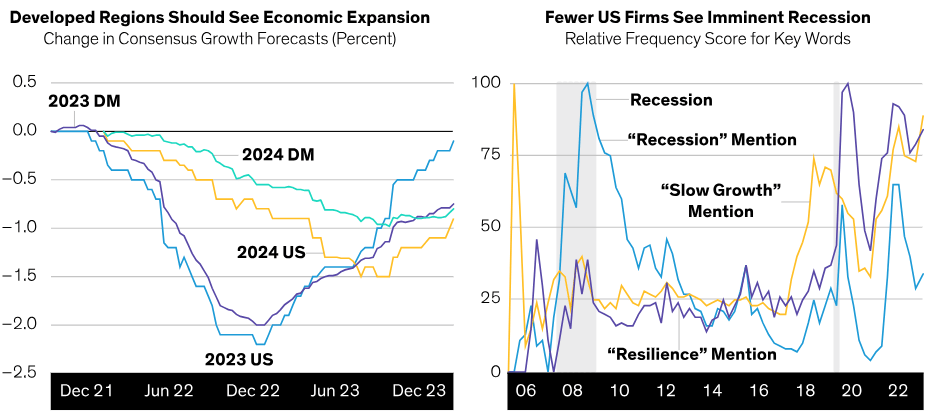

Recession Discuss Pivots to Gradual-Progress Expectations

The fears of an financial contraction that dominated 2023 have pale. Right this moment, the consensus is for gradual however constructive development for developed markets (Show 1, left). Firms are more and more optimistic too; fewer earnings calls point out “recession,” whereas references to “slow growth” and “resilience” have elevated (Show 1, proper).

Progress Expectations Bettering

Historic evaluation doesn’t assure future outcomes.

DM: developed markets. Durations of US recession are highlighted grey in the precise show.

Left show as of November 30, 2023; proper show as of November 5, 2023

Supply: AlphaSense, Bloomberg and AllianceBernstein (AB)

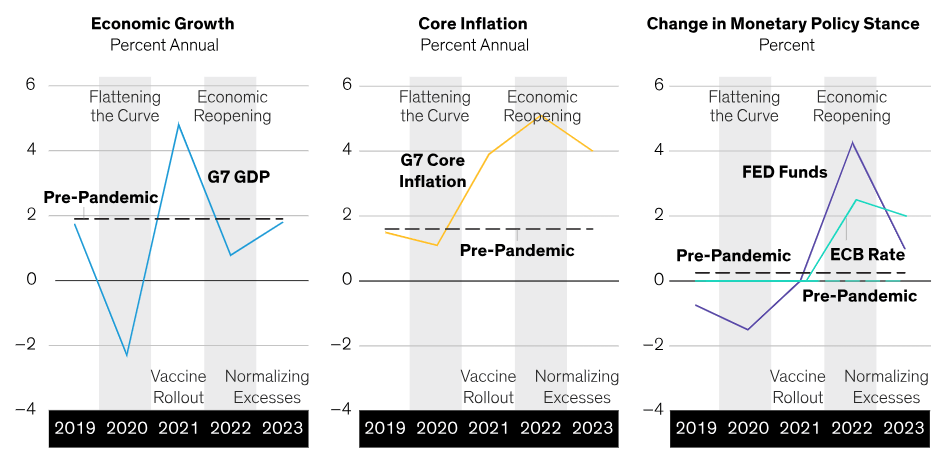

Over the previous few years, the worldwide financial system has endured a collection of extremes in financial development, inflation and coverage response. The collapse in world development in 2020 was adopted by a pointy restoration in 2021 as economies began to reopen, and large coverage help began to circulate via (Show 2, left). This was adopted in 2022 by an historic uptick in inflation (Show 2, heart) that led to aggressive financial tightening in developed economies, the place excessive charge adjustments started to shift nearer to regular between 2022 and 2023 (Show 2, proper).

Progress and Inflation Normalizing After Pandemic-Period Extremes

Historic evaluation doesn’t assure future outcomes.

Pre-pandemic averages proven are for information factors between 2015 and 2019; 2023 figures proven mirror estimates.

As of November 30, 2023

Supply: Bloomberg, Worldwide Financial Fund and AB

We noticed the beginnings of a gradual return to regular in 2023. Client spending energy improved as inflation pale, providers sectors recovered, extra jobs have been stuffed, extra inventories fell, and commodity and housing costs cooled. We anticipate extra progress towards this “new normal” in 2024, with development and inflation monitoring towards to pre-pandemic tendencies.

Spending Up Amongst Shoppers, Down for Companies

To date, resilience in family consumption has been largely a US phenomenon. US shoppers benefited from stronger wealth results and low publicity to rising charges and have been prepared to cut back financial savings charges to maintain spending. In distinction, EU and UK shoppers elevated their saving charges to anticipate rising curiosity cost obligations. Due to this fact, with inflation and charges now falling, we predict spending urge for food will enhance outdoors US.

We anticipate labor markets to remain resilient in 2024, however with job creation slowing to extra sustainable ranges. This could proceed to prop up shopper spending as effectively.

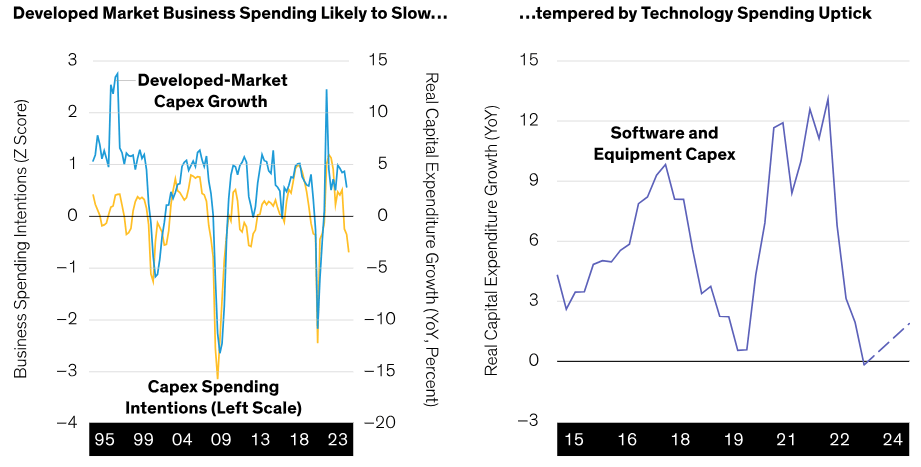

Enterprise funding is slowing throughout developed markets after an prolonged sturdy interval early within the post-pandemic restoration. Spending intentions have plunged (Show 3, left), whereas bottom-up estimates now recommend low single-digit development. Whereas spending on tools and constructions is more likely to gradual, gradual restoration in US tech funding—software program and tools, particularly—ought to assist restrict the draw back (Show 3, proper).

Enterprise Spending Could Soften Aside from Tech

Historic evaluation doesn’t assure future outcomes.

Forecast for software program and tools capital expenditure is a median primarily based on J.P. Morgan, Morgan Stanley, UBS and Wolfe Analysis analysis estimates for 2024.

As of December 7, 2023

Supply: Goldman Sachs, Haver Analytics, J.P. Morgan, Morgan Stanley, UBS, Wolfe Analysis and AB

Fiscal and Financial Coverage More likely to Normalize

The mixture of closer-to-normal financial development and easing inflation shall be key to coverage normalization in 2024. Aggressive fiscal spending has bolstered the US economy, however the impression on development is fading. The Worldwide Financial Fund tasks modestly contractionary fiscal coverage throughout most main economies this 12 months.

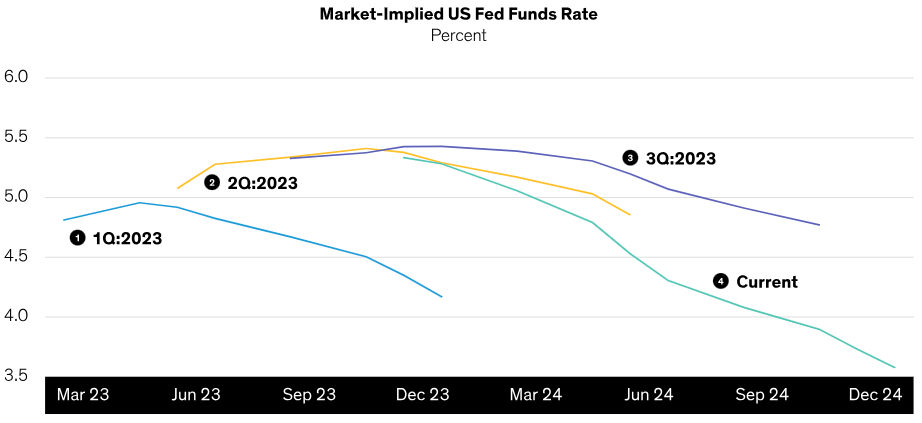

The period of exceptionally restrictive financial coverage ought to begin fading, too. Fee hikes have seemingly peaked, with cuts anticipated in 2024. This could cut back mortgage charges and assist residential funding. US markets anticipate simpler coverage than the Fed’s projections present (Show 4), an assumption which may be examined if development stays resilient.

Fee Expectations Proceed to Head Decrease

Previous efficiency doesn’t assure future outcomes.

Implied coverage charge calculated utilizing US fed funds futures.

As of December 13, 2023

Supply: Bloomberg and AB

What “Normalization” Means for Multi-Asset Buyers

We anticipate financial normalization to translate right into a return-to-growth mode for company earnings. Whereas financial development has been constructive, over the previous 12 months company earnings have been challenged by stock changes, commodity worth volatility and a scarcity of working leverage for service firms. These headwinds have now pale, which we predict supplies a good surroundings for equities and different threat property. In truth, stocks have outpaced other assets when rate cuts happen outside of recessions—which appears more and more seemingly.

Search for development and high quality in shares. Shares rallied in 2023, led by a number of tech names; we see this momentum lasting into 2024, given the improved financial image. We see EU shares benefiting from enhancing development prospects, whereas a gradual restoration in tech funding and AI prospects may proceed to help US equities. We stay cautious on rising markets, given China’s muted development outlook.

Fastened earnings provides extra potential. Bonds rallied in late 2023 and yields at the moment are effectively under October highs. Whereas markets have priced in a number of charge cuts in 2024, we consider bonds can present good diversification if development disappoints. Given our comparatively benign financial outlook, we predict it’s smart to remain near impartial in allocations to period, or interest-rate threat. We do assume US and UK sovereign bonds are comparatively enticing, given the actual fact there’s extra room for coverage normalization.

Diversifying asset lessons stay essential constructing blocks. Within the present local weather, we predict a impartial commodities publicity is the very best course. Costs have been declining towards pre-pandemic ranges due to subdued items demand and muted China stimulus, although ongoing geopolitical dangers may maintain some upside in sure situations.

The pandemic period introduced distinctive volatility to financial development, inflation and asset returns. We anticipate this panorama to shift nearer to historic “norms,” which may make it extra amenable to multi-asset buyers. As all the time, it’s essential to remain versatile and selective to navigate the transition.

The views expressed herein don’t represent analysis, funding recommendation or commerce suggestions and don’t essentially symbolize the views of all AB portfolio-management groups. Views are topic to revision over time.

Editor’s Be aware: The abstract bullets for this text have been chosen by Searching for Alpha editors.