JHVEPhoto/iStock Editorial by way of Getty Photographs

I price Ashtead Group (OTCPK:ASHTF)(OTCPK:ASHTY) as a maintain, as even when the corporate has attention-grabbing drivers forward which may assist it to maintain delivering progress within the subsequent few years, most of these drivers could be priced in. Even after I rated the inventory as maintain, I may use the technique of shopping for a number of shares now and preserve shopping for extra if the inventory goes down. There are attention-grabbing intangibles behind Ashtead’s progress technique within the building and infrastructure sectors which might be value mentioning, though it’s a very intensive-capital enterprise. In the previous couple of years, Ashtead’s bold plans had been mirrored in its double-digit income progress, supported by the profitable Sunbelt 3.0 strategy carried out in April 2021. Ashtead operates beneath the title Sunbelt Leases.

Annual Report 2023

The chart may assist a bullish thesis, however I am unsure if the corporate will develop on the similar charges as these proven within the final decade. Nonetheless, I anticipate respectable progress charges sooner or later whereas seeing how the corporate developed from April 2012 to April 2023, growing considerably its variety of areas, which helps it to bolster its cluster technique that allows a sooner and extra environment friendly supply of apparatus wanted by prospects in lots of areas in North America. However there are extra elements behind this firm that can assist its future progress regardless of its current discount of steering for the total yr 2024 in November 2023.

Later, I’ll evaluate Ashtead with its principal competitor in North America, assessing completely different metrics which may assist us resolve which ones looks like a greater guess for the long run. Lastly, I’ll provide my intrinsic worth, taking completely different assumptions, and given the cycle of the enterprise, I assume a restricted interval of holding till 2026. That is my first article about Ashtead, however I’ve written about one other wonderful German firm within the building sector with a world footprint, Nemetschek, that I feel is value studying. Now, let’s dive into Ashtead.

Context

Outcomes accrued as of October 2023, Q2 2023-24, income progress was 16% YoY whereas working revenue grew at 12% YoY. EPS grew solely 5% in the identical interval which was defined by the upper curiosity bills paid by the corporate because it holds a comparatively giant debt, which is a part of the character of the enterprise and which is one thing I’ll talk about later.

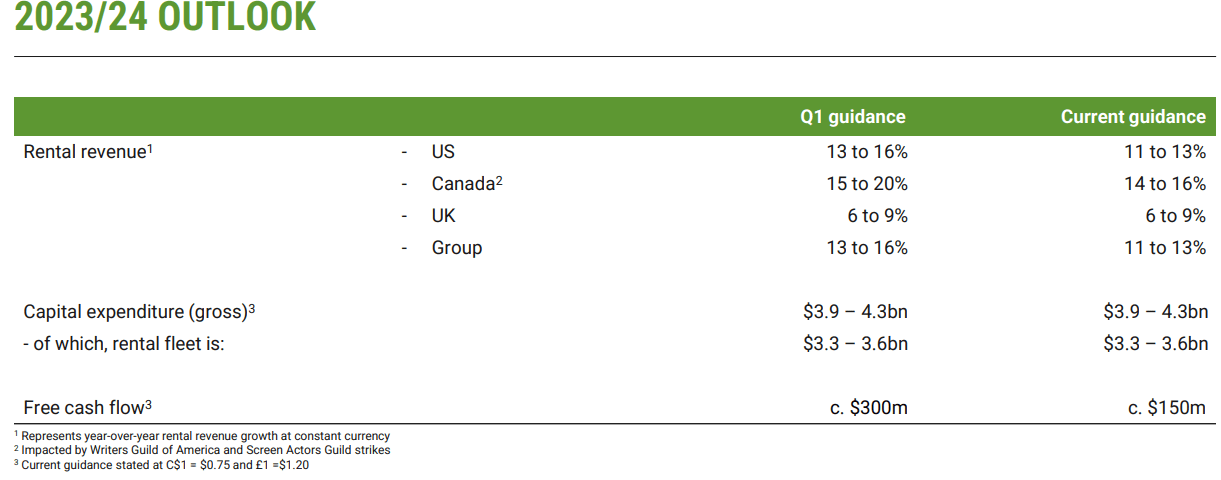

As of October 2023, free money circulation (FCF) was $-373 million in comparison with $139 million one yr later which was pushed by the upper purchases of plant, gear and property on this interval, particularly, a alternative of a good portion of its fleet. Within the Q1 2023 outcomes, the corporate established guidances for every of the nations the place it operates:

Ashtead Presentation

Nonetheless, in November 2023, the corporate diminished that steering because it anticipated that a few of its companies would expertise a income slowdown, resembling decrease emergency response exercise as a consequence of fewer naturally occurring occasions and a deceleration of the movie and TV enterprise pushed by the current actors’ and writers’ strikes.

As a way to perceive extra about these outcomes, it is essential to know extra about Ashtead’s enterprise mannequin to know its nature.

Enterprise mannequin

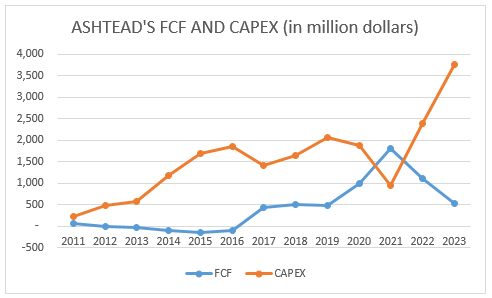

In easy phrases, what Ashtead does could be very easy for the reason that firm purchases an asset, rents it to its prospects by means of its platform, and generates an annual income stream for every year. Ashtead holds that asset for, sometimes, a mean of seven years. Now, the sum of money spent on every of these belongings is comparatively excessive in comparison with the income stream of the primary yr, in order that’s why the FCF has been a bit risky over time.

Writer

Within the chart above, it is proven that within the years 2012-2016, the corporate delivered destructive FCF regardless of its annual income progress in these years of greater than 20%. The excessive necessities of capex could make the FCF destructive some years; as such, Ashtead could be very intensive in CAPEX, so this is a crucial variable that we have to observe up on on this firm. I feel that as the corporate retains increasing its operations, it could be extra environment friendly in its CAPEX administration, lowering the potential for producing destructive FCF. That is associated to the corporate’s technique, which I’ll clarify later.

Q2 2023 outcomes

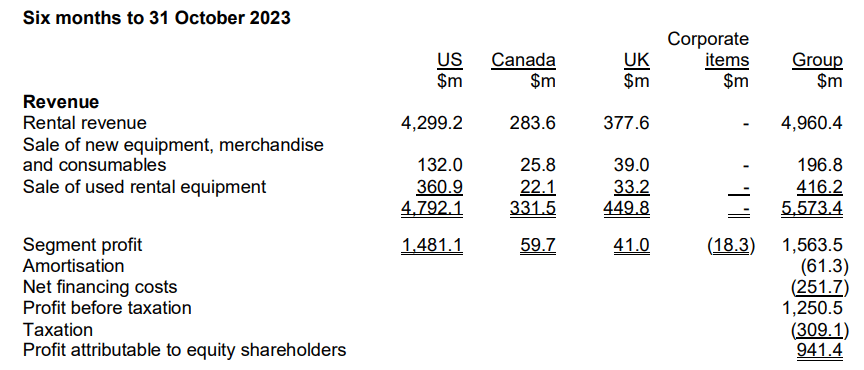

Within the desk above, it may be observed that rental income is a very powerful supply of revenues, representing round 90% of the whole revenues. As I discussed beforehand, Ashtead buys these equipments after which rents them to its prospects; as soon as these equipments should be changed, the corporate sells these used rental equipments to the secondary market, being one other supply of revenues. The sale of consumables and merchandise is one other supply of revenues, but it surely’s not important, with a participation of round 3% of whole revenues.

In the identical desk, I discover that the US is by far Ashtead’s most essential market, representing 85% of whole revenues within the first six months of 2023. Not solely that, the US is essentially the most worthwhile market, with a section revenue of 33% in the identical interval, whereas Canada and the UK generated section earnings of 20% and 10%, respectively.

Ashtead provides its companies in numerous sectors, resembling the development sector, the place the corporate offers assist within the building of airports, highways, and bridges, knowledge facilities, colleges, manufacturing vegetation, inexperienced power, and many others. Within the response sector, Ashtead offers assist in mitigating fires, hurricanes, residential emergencies, different care services, and many others.

Ashtead additionally provides facility upkeep to colleges and universities, buying facilities, workplace complexes, and many others. Lastly, Ashtead is uncovered to leisure and particular occasions, providing assist for nationwide occasions, concert events, movies, TV productions, and many others. The corporate is de facto well-diversified by means of completely different financial sectors, which contributes to its resilience.

As you’ll be able to think about, regardless of being an organization from the UK, the analyst’s focus must be on the US market, which is the supply of many of the firm’s progress and profitability.

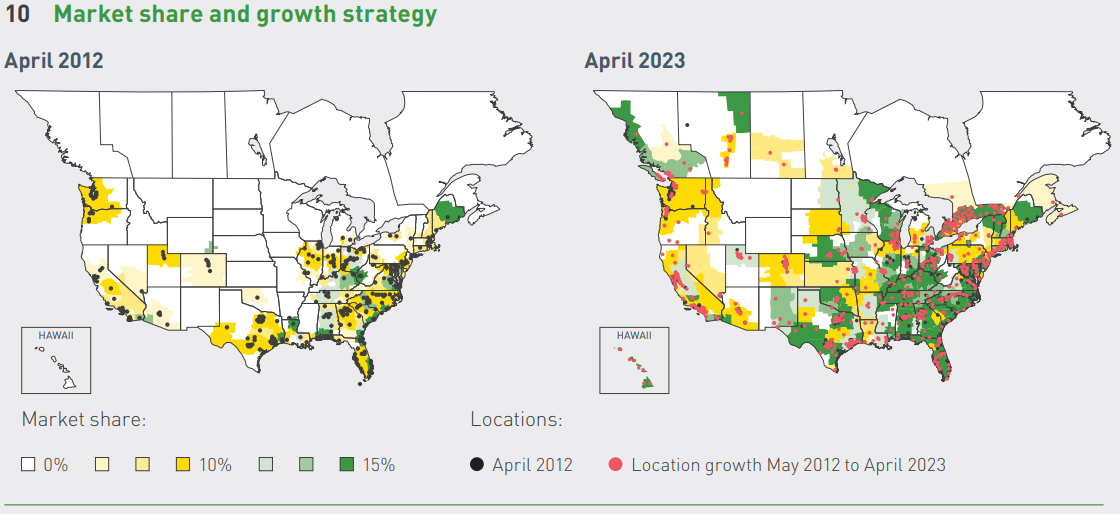

Ashtead presentation Dec 2023

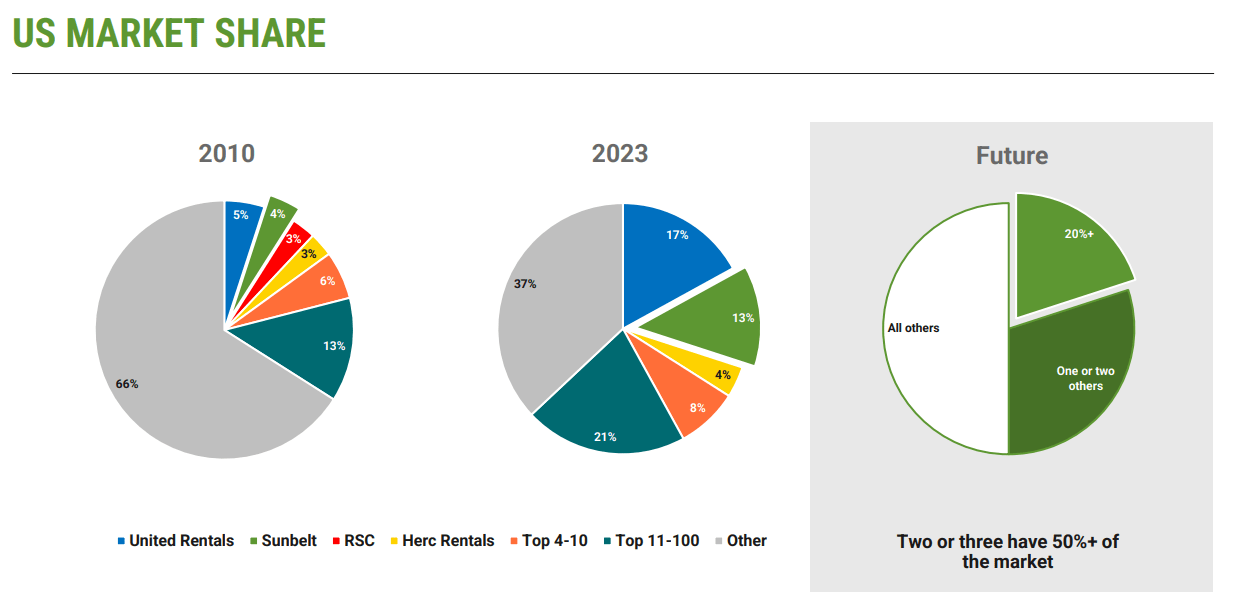

Within the chart above, it’s observed that Ashtead’s market share, beneath Sunbelt’s title, has grown from 4% in 2010 to 13% in 2023, being the second largest after United Leases (URI). Most of this growth of those two massive gamers within the business comes from buying small native unbiased corporations and establishing new shops in numerous areas.

Now, I’ve defined that it is a very capital-intensive business, so the dimensions is essential to dilute the mounted prices to supply extra aggressive costs and a wider vary of companies; as an example, Ashtead buys its rental fleet from one or two suppliers whereas limiting the variety of mannequin forms of every product. Thus, Ashtead will get essential reductions from a number of suppliers for extra standardized fleet purchases. Smaller rivals could be unable to get these reductions, given their smaller demand.

On this sense, the most important gamers have all the benefits in comparison with the smaller gamers, because the latter can’t provide a wider vary of companies at decrease costs. Then again, there may be an underlying technique behind this success of gaining extra market share that makes the corporate assured sufficient to achieve a future market share goal of 22% within the US market: the cluster technique.

Cluster technique and Sunbelt 3.0

The simple option to clarify the cluster technique is to think about completely different geographic markets; in every of those territories, Ashtead units up shops. The variety of shops in every territory may vary from 2 to greater than 15, relying available on the market’s dimension.

For instance, one buyer situated in a sure territory within the US or Canada is demanding a couple of service that includes completely different gear or fleet for a selected goal, so one retailer situated in that territory may ship a selected sort of fleet and one other retailer situated in the identical cluster may ship one other sort of apparatus as a part of the client’s necessities. So the client is served sooner as Ashtead has nearer shops to the client’s areas whereas responding effectively to the client’s necessities.

There are a number of advantages of the cluster strategy that assist Ashtead scale back its prices, resembling sharing spare elements between shops in the identical cluster, which helps decrease the chance of overstocking. All these shops which might be grouped in the identical territory allow frequent use of the belongings for hire, avoiding the idling time of these belongings. Additionally, this technique helps Ashtead cross-sell between building and non-construction companies. Building actions characterize 40% of Ashtead’s whole revenues within the US, whereas non-construction accounts for the remaining 60%. Residential building is only a small portion of all the building section, as this sector is just not a heavy consumer of apparatus.

Ashtead has considerably diminished its dependence within the building space to cut back the cycle related to the sector whereas widening its product providing and buyer base, reinforcing its enterprise mannequin within the non-construction sector, such because the “specialty area,” which represents round 30% of Ashtead’s US enterprise and 65% within the UK enterprise. On this sense, Ashtead is creating specialty areas resembling energy and heating, air flow and air-con (HVAC), local weather management and air high quality, scaffold companies, flooring options, and many others.

Sunbelt 3.0 is the technique that Ashtead began in April 2021 for 3 years, in search of sustainable and worthwhile progress. Earlier than Sunbelt 3.0, Ashtead established a really profitable technique in 2016, named Challenge 2021, reaching a complete income progress of 75% from 2016 to 2021.

Ashtead Presentation Dec 2023

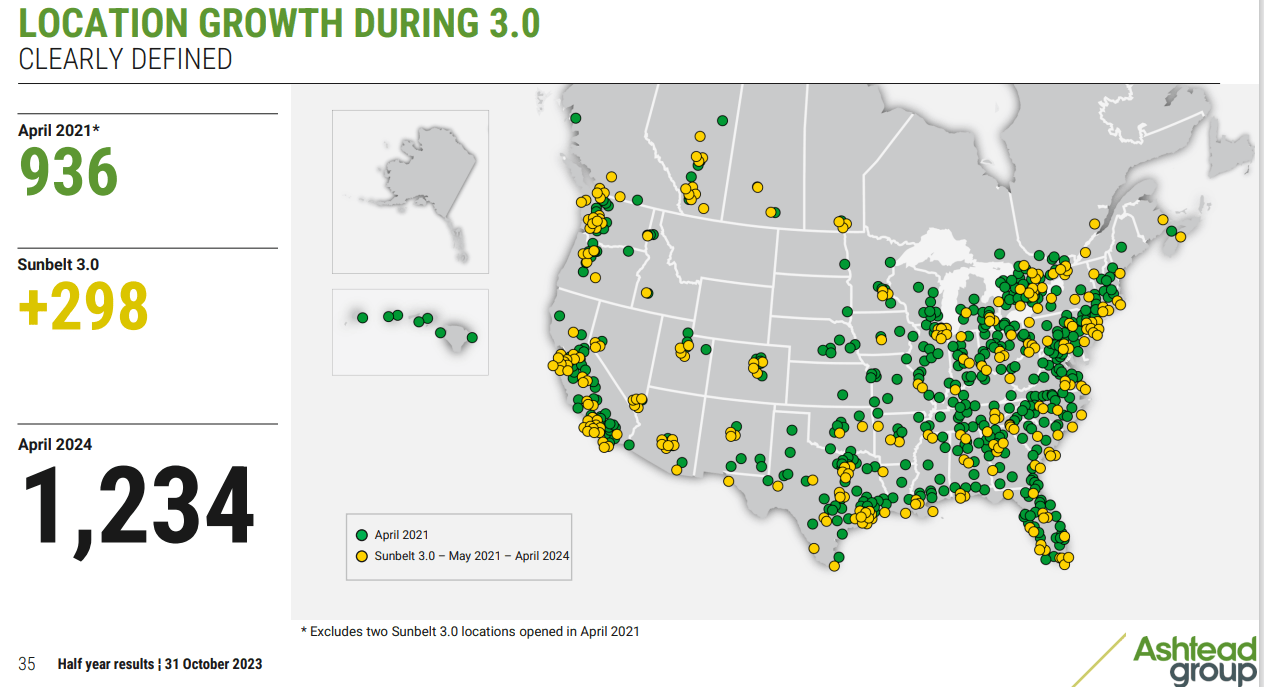

Underneath the technique of Sunbelt 3.0, Ashtead deliberate to open greater than 298 new shops so as to add to its already established 936 shops as of April 2021 with a purpose to have 1,234 shops in April 2024. As of April 2023, the corporate has already added 1,213 new areas in North America, which signifies that, more than likely, the corporate may surpass its aim of 1,234 in April 2024. Within the chart above, it is clear how Ashtead is working to increase its operations to ship long-term progress, profiting from the cluster strategy.

Within the UK, the technique is completely different, taking into consideration its smaller geography, implementing a number of bigger areas mixed with smaller native areas, which isn’t so completely different from the cluster strategy to be tailored to the UK’s buyer base.

Megaprojects: One other supply of long-term progress

Megaprojects have gotten extra essential in the previous couple of years, and, in keeping with Ashtead, these initiatives could possibly be named megaprojects when their worth is greater than $400 million. These sorts of initiatives embody knowledge facilities, healthcare services, airports, liquid pure fuel vegetation, semiconductor services, electrical automobile and battery vegetation, photo voltaic and wind farms, and many others.

Ashtead is profiting from megaprojects, because it has an total market share of roughly 30% in these initiatives. CEO Brendan Horgar mentioned within the final name for Q2 2023:

I feel – effectively, to begin with, these initiatives that had been within the early phases of immediately, we’d anticipate that peak or crest, as I referred to it to final fairly a while. So you are going to see that in FY ’25 and FY ’26 as a result of actually the crest of those initiatives is a few 2-year time-frame in lots of instances. And I feel it is value highlighting to a level simply the state of these 499 initiatives that we talked about.

Simply to place it in perspective, I feel what’s essential is how early we actually imagine we’re on this panorama of megaprojects. So of the 499 that we’d have identified, truly, solely 336 of these are underway. So they’re in begin or assemble as Dodge would calibrate. In fact, we observe each single one in every of these. In order that leaves the stability of 163 which might be in some type of prestart.

This means that Ashtead has essential long-term drivers not solely from its cluster strategy and growth but additionally from these 499 megaprojects, of which 366 are at their early levels and will attain their crest in 2025 and 2026, and the remaining 163 would attain that crest past 2026.

It must be observed that these initiatives require an essential scale, expertise, vast options and merchandise, and an essential monetary capability. I feel that this comparatively new development within the business may contribute to strengthening this means of consolidation and strengthening the place of corporations like Ashtead.

It is value noting that there are three US legal guidelines that favor these sorts of initiatives: i) The Infrastructure Investment and Jobs Act, with $1.2T in investments in numerous infrastructures; ii) The Chips and Science Act, which includes $ 250 billion for these functions; and iii) the Inflation Reduction Act, which is able to present $ 370 billion to assist photo voltaic discipline building, battery factories, wind farms, electrical automobile manufacturing, and many others.

Ashtead in comparison with its principal competitor

United Leases is Ashtead’s principal competitor in North America, and it’s profiting from its place to ship double-digit income progress in the previous couple of years, however I wish to see how its efficiency within the final 5 years has been to check it with Ashtead.

Writer, Annual Reviews

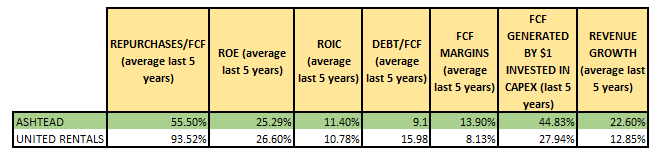

The metrics proven within the desk above embody the final 4Q 2023 outcomes from United Leases that had been just lately launched and boosted the inventory value by greater than 12% in at some point. Taking a look at these metrics, Ashtead has earned higher returns on capital (ROIC) and virtually an identical ROE with that of United Leases, however even after I like extra ROIC than ROE because the latter doesn’t bear in mind how excessive the debt ranges in an organization are, I wanted to make use of different metrics that point out how environment friendly every of those corporations was to get extra FCF by investing $1.

On this sense, I constructed a ratio by including the sum of the CAPEX from the final 5 years within the denominator and the sum of the FCF from the final 5 years within the numerator; the aim is to understand how a lot FCF is earned by $1 invested in CAPEX. On this sense, Ashtead earned 44 cents per $1 spent in CAPEX on common within the final 5 years, whereas United Leases solely earned 28 cents per $1 spent in the identical interval.

Ashtead is exhibiting higher FCF margins mixed with higher income progress on common within the final 5 years and extra environment friendly and worthwhile capital administration than United Leases. One thing that I don’t like is how Ashtead’s administration makes use of the ratio of whole debt to EBITDA to gauge the monetary leverage, which is one thing which may mislead traders since EBITDA is just not metric, notably for a corporation that could be very intensive in capital necessities.

Certainly, I desire to make use of the FCF over the EBITDA to have the ratio Debt/FCF, for the reason that EBITDA doesn’t bear in mind the CAPEX necessities which might be wanted by the corporate to proceed its operations. So, it is anticipated that gamers on this business present excessive debt/FCF, however wanting on the desk above, Ashtead exhibits manner decrease debt ranges than United Rental’s.

Moreover, Ashtead has a ratio of repurchases/FCF (55%) decrease than that of United Leases (93%), which has a correlation with the debt ranges of every firm. This appears unrelated, however a decrease allocation of repurchases or share buybacks permits the corporate to have extra money out there to reinvest in its personal enterprise; if the corporate doesn’t come up with the money for for reinvestments, it wants extra debt, and that is United Rental’s case with greater capital allocation in buybacks and better debt ranges than Ashtead.

In United Rental’s case, I’ve seen that in many of the final 5 years, the corporate was allocating extra money for buybacks than what it was producing in FCF, which doesn’t shock me to see greater debt ranges than Ashtead. Nonetheless, United Leases inventory has appreciated greater than 700% within the final decade, whereas Ashtead inventory has appreciated round 400% in the identical interval; there could possibly be a number of explanations for that distinction.

It is potential that United Leases is a extra well-known inventory amongst institutional traders or that the corporate is the chief within the US with 17% and Canada with 22%, whereas Ashtead has 13% and 9%, respectively. In any case, each corporations will benefit from the consolidation course of within the business, as each are a very powerful gamers.

Nonetheless, wanting on the metrics within the desk above, I like Ashtead extra; due to this fact, my portfolio could be extra uncovered to Ashtead inventory than United Leases inventory, given its greater ROIC, greater FCF generated by $1 of CAPEX, decrease debt ranges, greater progress, and better FCF margins.

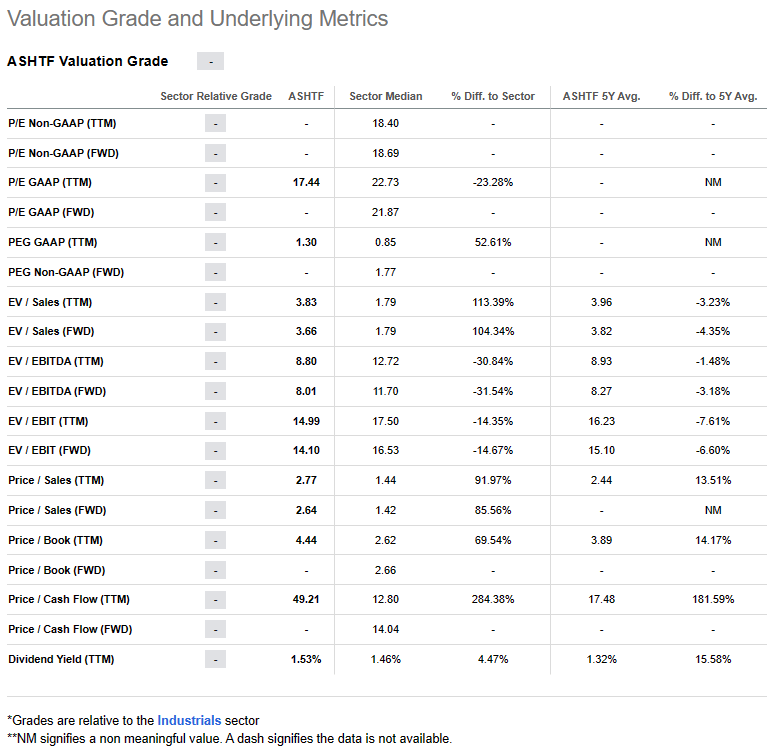

Valuation

The completely different a number of valuations don’t give a transparent image of how enticing Ashtead’s inventory value is now.

SA

I suggest one other methodology to search out the intrinsic worth:

Assumptions

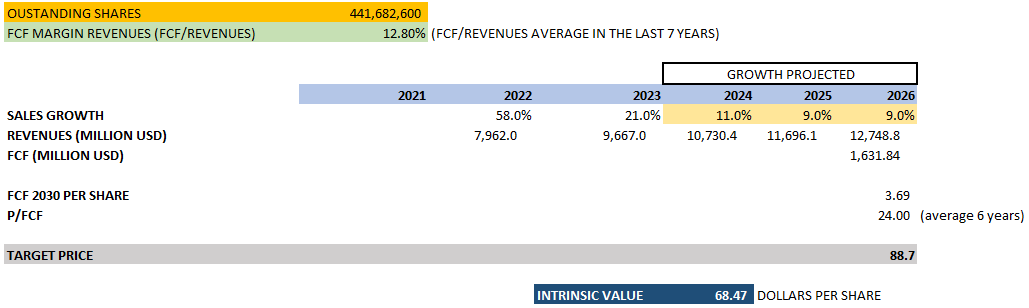

- Excellent shares: 441,682,600 (as of October 2023)

- FCF Margins: 12.8% (common of the final 7 years)

- I assume that Ashtead inventory is held till 2026.

- Income progress for 2024: in keeping with management’s steering

- Income progress for 2025 and 2026: according to consensus

- P/FCF 2030: 24x (common of the final 6 years)

- Discounted price: 9%

Writer

Primarily based on my assumptions, I make a projection of income progress of 11% for 2024, 9% for 2025, and at last 9% for 2026. So, I take the revenues projected for 2026, after which I multiply these revenues by the FCF margins of 12.8% which might be a part of my assumptions. Then, consequently, I get an approximate FCF of $1,631 million for 2026.

Now, I take that FCF of $1,631 million and divide it by the excellent variety of shares of 441,682,600 to get a FCF per share for 2026, getting 3.69. On this sense, I take the FCF per share of three.69 and multiply it by 24, which is Ashtead’s common P/FCF of the final 6 years. Then, I get a goal value of $88.7 per share in 2026, so I calculate the current worth to deliver it again to 2024.

Thus, discovering the intrinsic worth:

Intrinsic worth = 88.7/(1+discounted price)^3

Lastly, I get an approximate intrinsic worth of $68.47 per share, and the present inventory value is $67.68 per share, so there may be not sufficient margin of security to purchase strongly. Nonetheless, as I mentioned firstly of this text, I might purchase on the present inventory value some shares whereas being ready to purchase step by step extra in case the inventory value goes down.

It’s best to bear in mind that my intrinsic worth is conservative and may aid you construct up a margin of security since an intrinsic worth of $68.47 is contemplating comparatively decrease income progress for the following 3 years than the expansion proven by the corporate within the final years. I’ll observe up on the inventory to see how the corporate behaves within the subsequent quarters so as to have the ability to anticipate greater income progress than these of my assumptions, which might increase the intrinsic worth.

One reference was the just lately launched Q4 2023 outcomes of United Leases, whose revenues grew 23% and web revenue grew 15% for the total yr 2023, so the market reacted very positively, boosting the inventory by greater than 12% in at some point. Nonetheless, the steering for 2024 is a income progress of 4%, in order that’s why I should be very conservative within the Ashtead’s intrinsic worth.

Dangers and remaining ideas

The cyclicality of the enterprise may influence the utilization ranges in sure durations of time, with the consequence of poor FCF given the excessive capital necessities. Nonetheless, given my long-term horizon, I just like the enterprise to be held for a number of years, and within the worst situations, I might add extra shares because the enterprise has diversified its progress avenues by means of completely different sectors, as we have seen within the article, which reinforces its resiliency.

One other danger could be the change within the US administration, which may halt a few of the megaprojects which might be a part of Ashtead’s long-term drivers of progress. However, the vast majority of these initiatives require non-public funding in a variety of sectors, resembling semiconductors, LNG, airports, ethane, rail, refineries, knowledge facilities, and many others. So, the diversification of these initiatives and Ashtead’s potential to adapt itself to completely different situations would mitigate that danger.

Lastly, one other danger that we must always concentrate on is the excessive debt related to Ashtead’s business. We have seen that United Rental has the identical downside, although its debt ranges are manner greater than Ashtead’s. Anyway, I don’t like an organization with excessive debt ranges, however I might not be anxious about Ashtead as the corporate has a critical technique to preserve delivering robust long-term progress and nice administration that is ready to benefit from the completely different alternatives to have stage of asset utilization and maintain beneath management the debt ranges.

I like corporations like Ashtead with good administration and a stable long-term technique which have proved their resiliency in COVID-19, delivering double-digit income progress in these years. I put a “hold” as a result of I prefer to be conservative with the worth I pay for a high-quality inventory, and Ashtead surged 6% just lately due to United Rental’s outcomes. Nonetheless, even after I put a maintain score, I might purchase some shares on the present value whereas following up on the inventory to extend my place extra strongly because the inventory value falls from my intrinsic worth of $68 per share.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.