Galeanu Mihai/iStock through Getty Photos

Zscaler (NASDAQ:ZS) has been one of many strongest tech shares as of late. It isn’t laborious to see why: the cybersecurity firm has posted top-notch basic outcomes over the previous 12 months despite a powerful macro atmosphere, producing best-in-class progress charges and displaying increasing working margins. Whereas the inventory is now not filth low cost because it was one 12 months in the past, the corporate has arguably earned a premium valuation. ZS maintains a web money stability sheet and seems on the verge of inflecting on GAAP profitability. That stated, the present inventory value doesn’t seem like providing sufficient potential reward for the present danger profile, even when we assume sturdy high and backside line progress charges over the following decade. I’m downgrading the inventory to a impartial “hold” ranking.

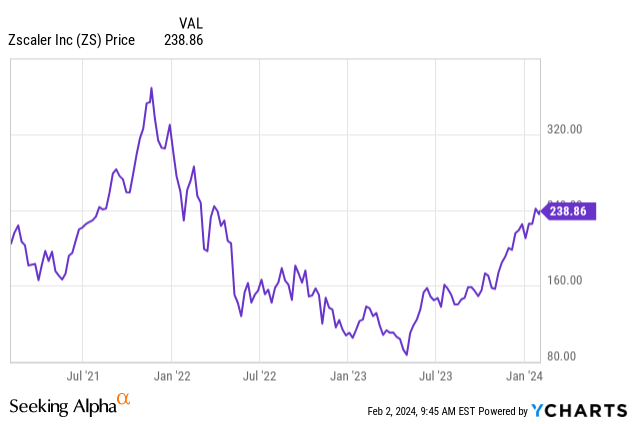

ZS Inventory Worth

It’s humorous how rapidly sentiment can change. It was simply lower than a 12 months in the past when the market seemingly had all however given up on ZS, considering that progress charges can be heading decrease. ZS has confirmed the doubters fallacious, and those that caught by the inventory have been rewarded handsomely.

I last covered ZS in November the place I reiterated my purchase ranking on account of generative AI being a possible tailwind for cybersecurity shares. The inventory is up considerably since then however could have run a little bit too far and a little bit too quick.

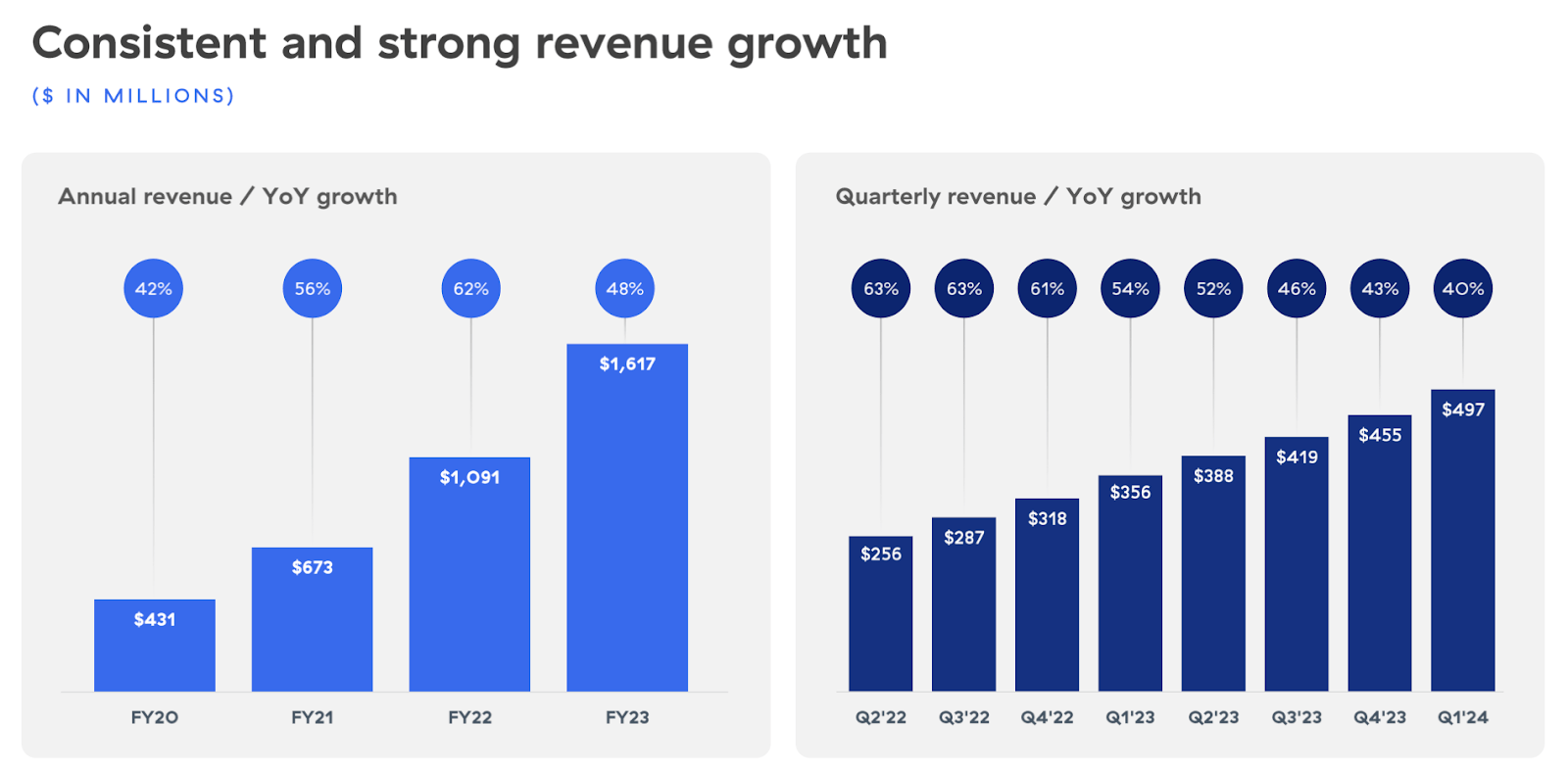

ZS Inventory Key Metrics

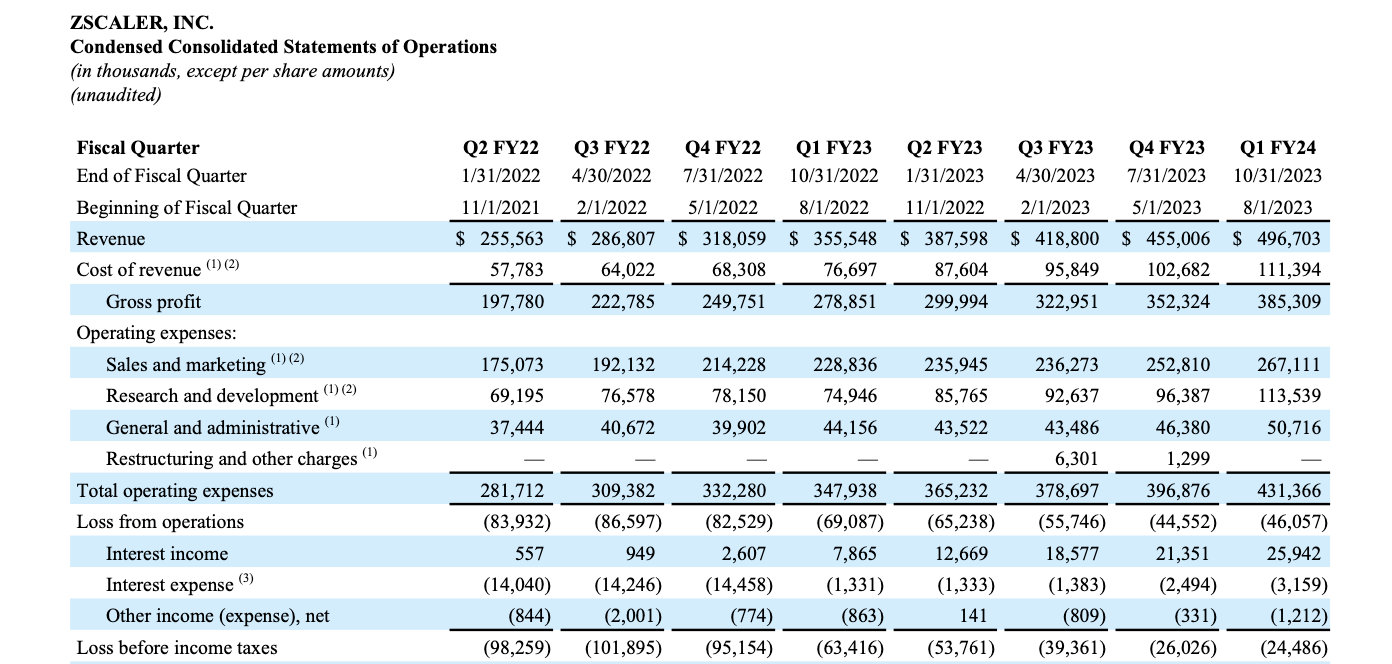

In its most up-to-date quarter, ZS generated 40% YoY income progress to $497 million, smashing steering of $474 million.

FY24 Q1 Presentation

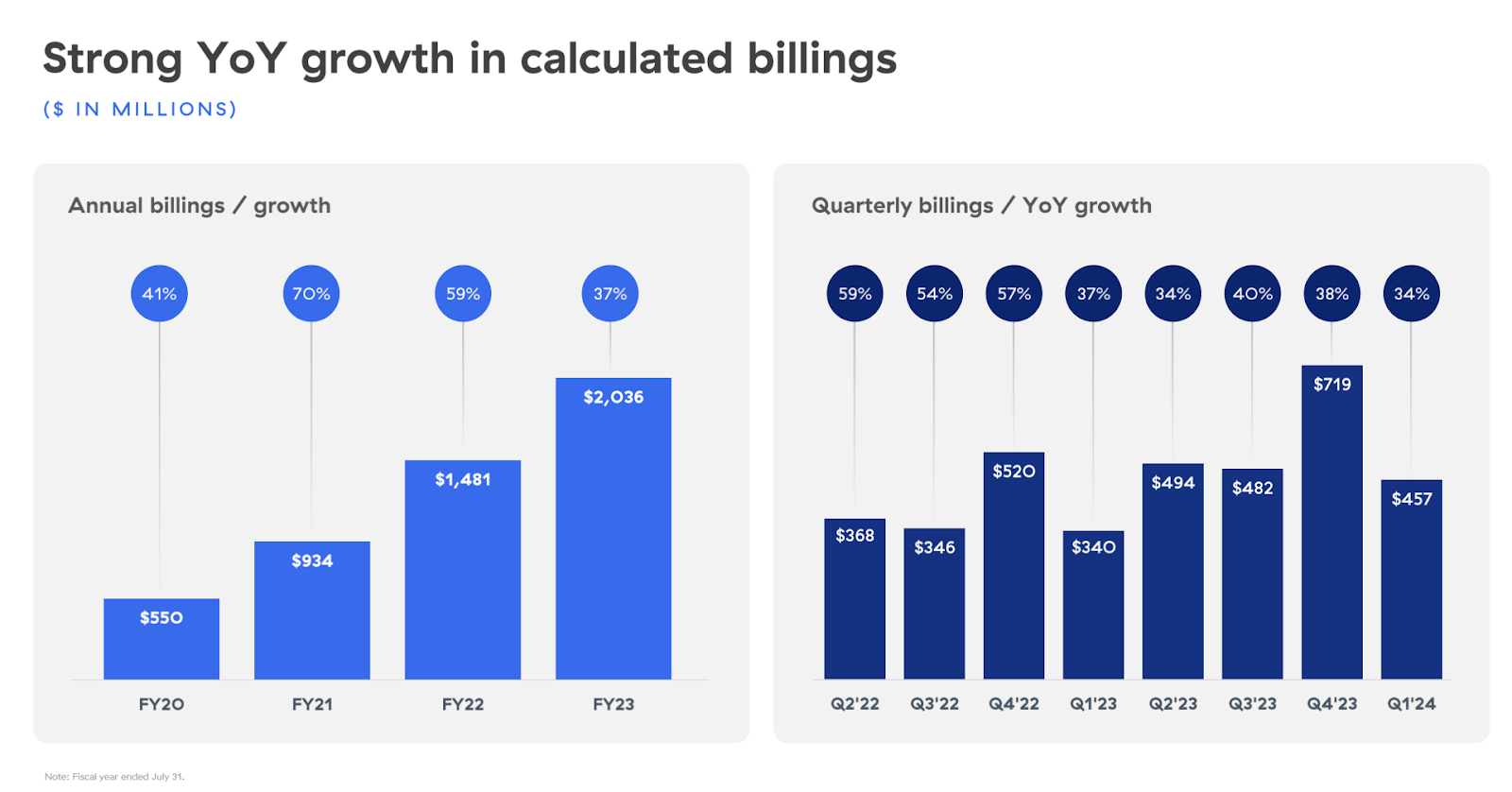

The corporate paired that sturdy income progress with 34% YoY billings progress.

FY24 Q1 Presentation

On the convention name, administration famous that the present remaining efficiency obligations (‘cRPOs’) grew 3.5% QoQ and 32.7% YoY. Between the sturdy billings and cRPOs progress, I count on ZS to maintain speedy top-line progress over the approaching 12 months.

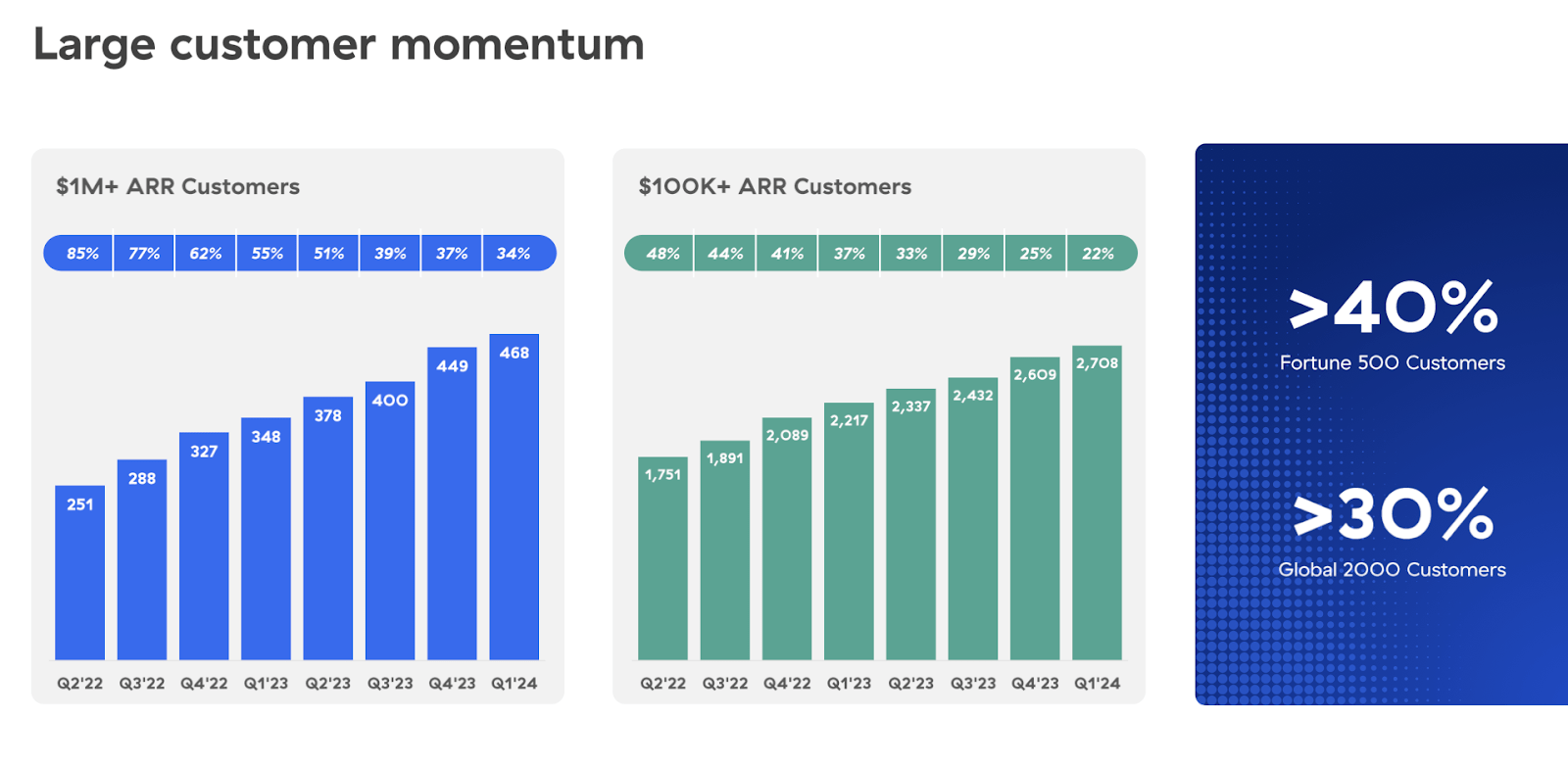

ZS has benefitted from its huge product portfolio, because the 120% dollar-based web retention fee was a key driver of the aggressive top-line progress. ZS has by some means additionally delivered on aggressive buyer progress, a powerful achievement given the elevated scrutiny on IT bills.

FY24 Q1 Presentation

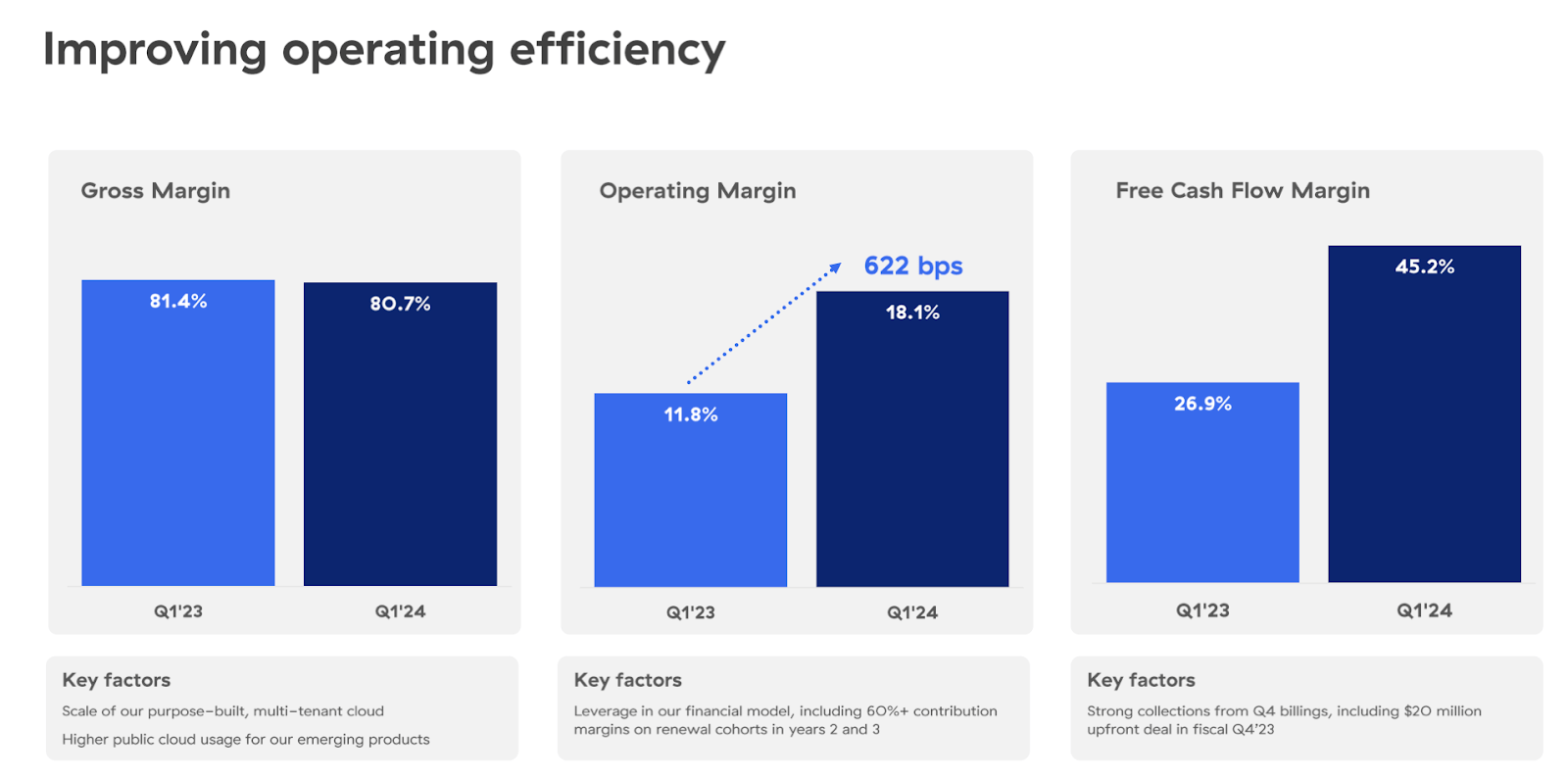

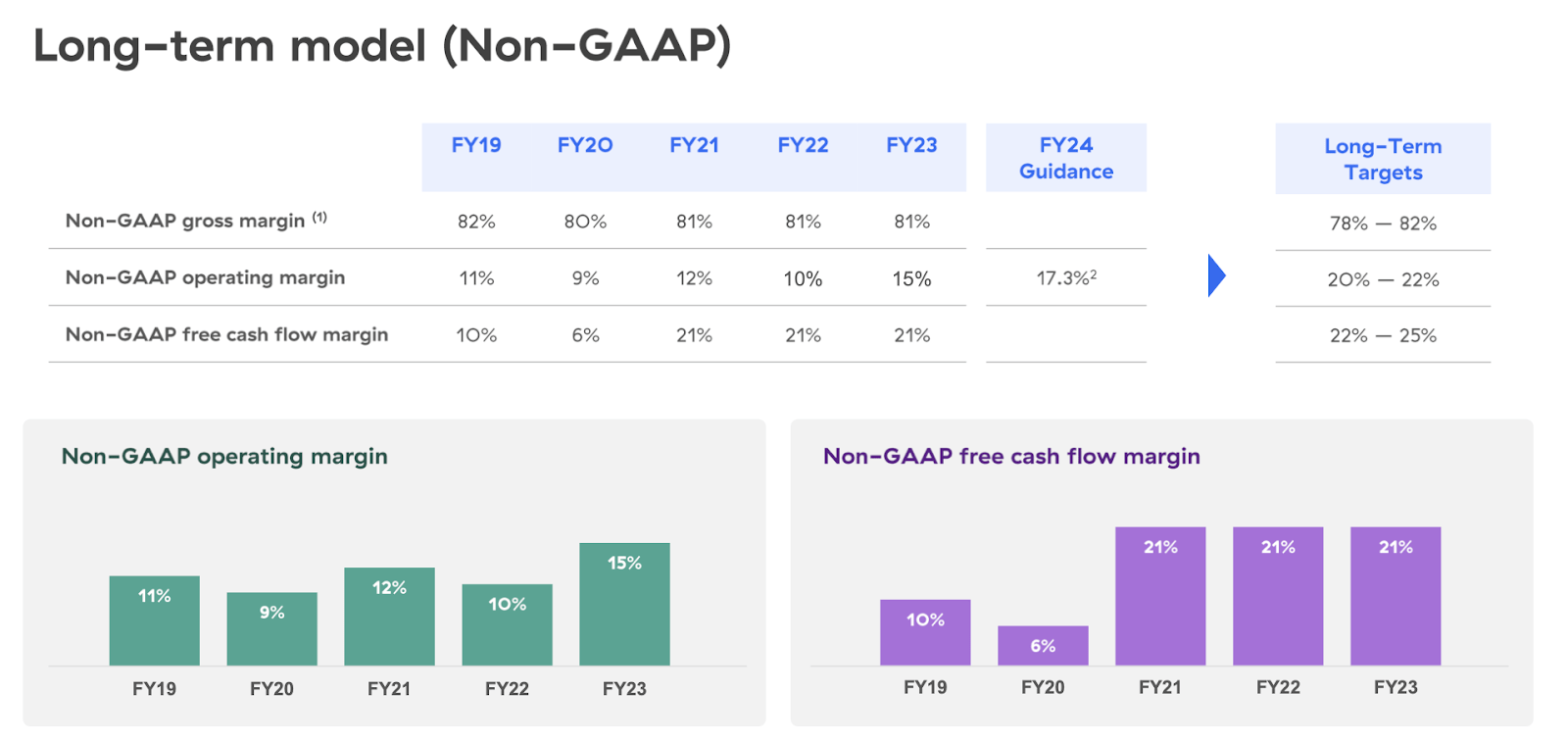

ZS additionally delivered stable profitability positive aspects, with non-GAAP working margins rising 622 bps to 18.1% and non-GAAP EPS coming in at $0.67, smashing steering for $0.49.

FY24 Q1 Presentation

It’s value noting that ZS is now very near attaining GAAP profitability. The upper rate of interest atmosphere has helped result in a surge in curiosity revenue, however even excluding curiosity revenue, ZS would want to generate solely a 31% incremental working margin to attain GAAP profitability (assuming 30% ahead progress). In reality, sooner or later I count on ZS to start producing incremental working margins in extra of 75% or greater as working leverage takes maintain. It is a firm that might present GAAP income each time it chooses to.

FY24 Q1 Supplemental

ZS ended the quarter with $2.3 billion of money versus $1.1 billion of convertible notes. These convertible notes carry a 0.125% rate of interest, which helps to elucidate the excessive web curiosity revenue. These notes mature subsequent 12 months.

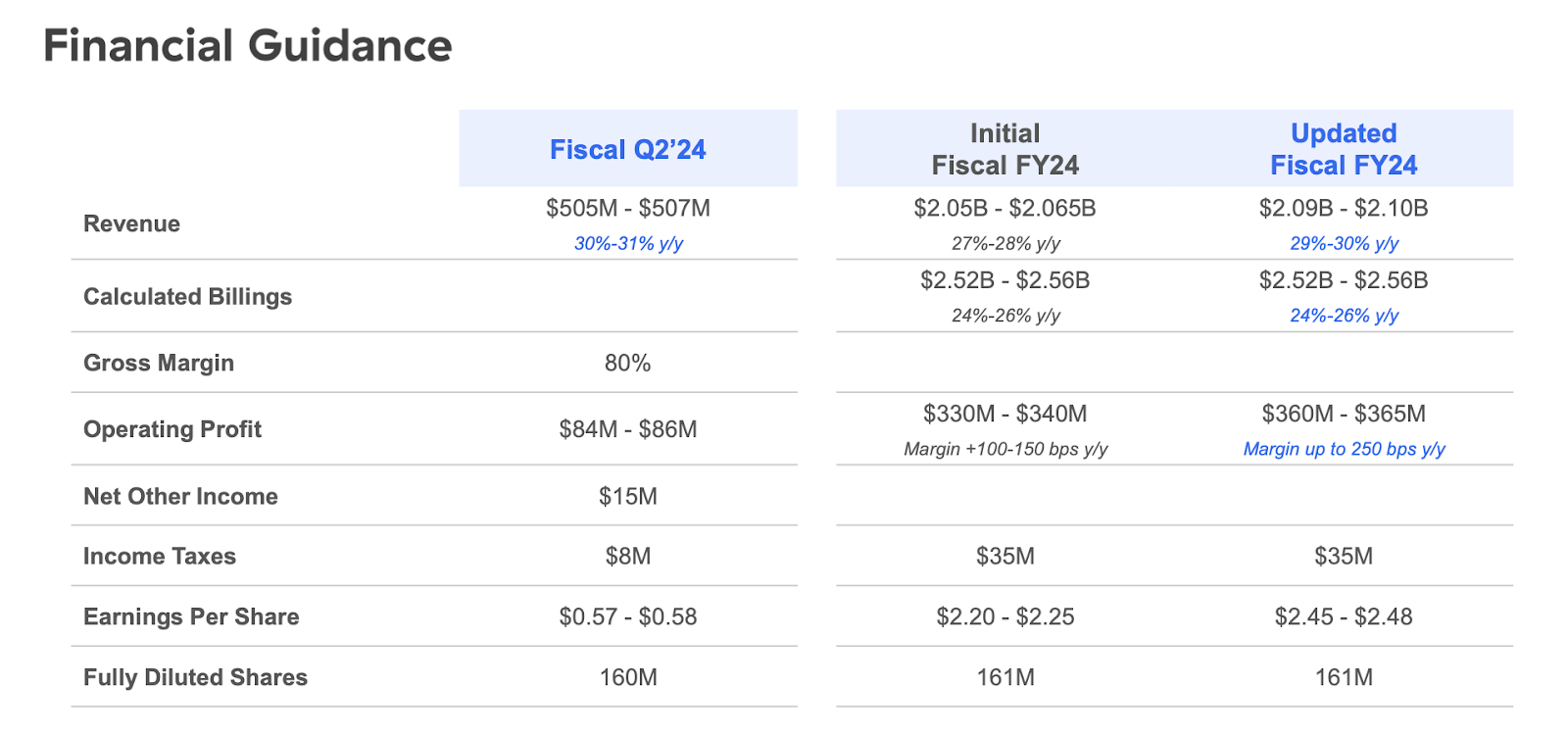

Wanting forward, administration has guided for the second quarter to see as much as 31% YoY income progress. Consensus estimates have the corporate coming in on the center of income steering at round $506 million and on the excessive finish of earnings steering at $0.58 in non-GAAP EPS. Administration raised full-year steering to see as much as 30% YoY income progress and 26% YoY billings progress.

FY24 Q1 Presentation

On the conference call, administration famous that the macro atmosphere remained difficult although “customer sentiment seems to be stabilizing.” Given commentary from Microsoft’s (MSFT) current earnings name that cloud optimization headwinds have eased dramatically, it’s attainable that ZS could profit from an bettering macro atmosphere shifting ahead. The powerful macro atmosphere had impacted ZS’ enterprise by way of slowing headcount progress at its prospects (even when ZS nonetheless generated sturdy outcomes). As typical, Wall Avenue has invested forward of the elemental information as this optimism is being priced into the inventory.

Is ZS Inventory A Purchase, Promote, or Maintain?

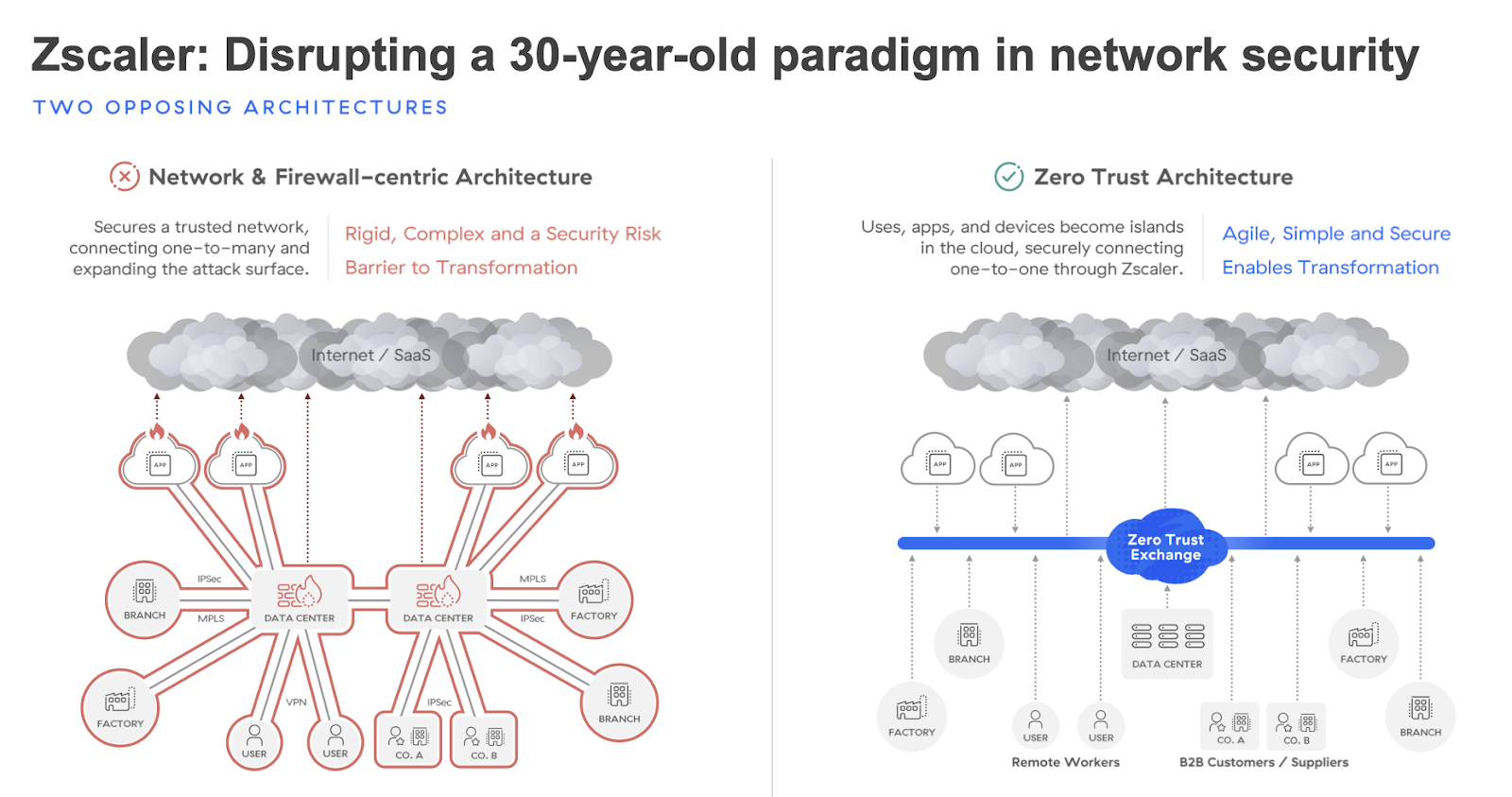

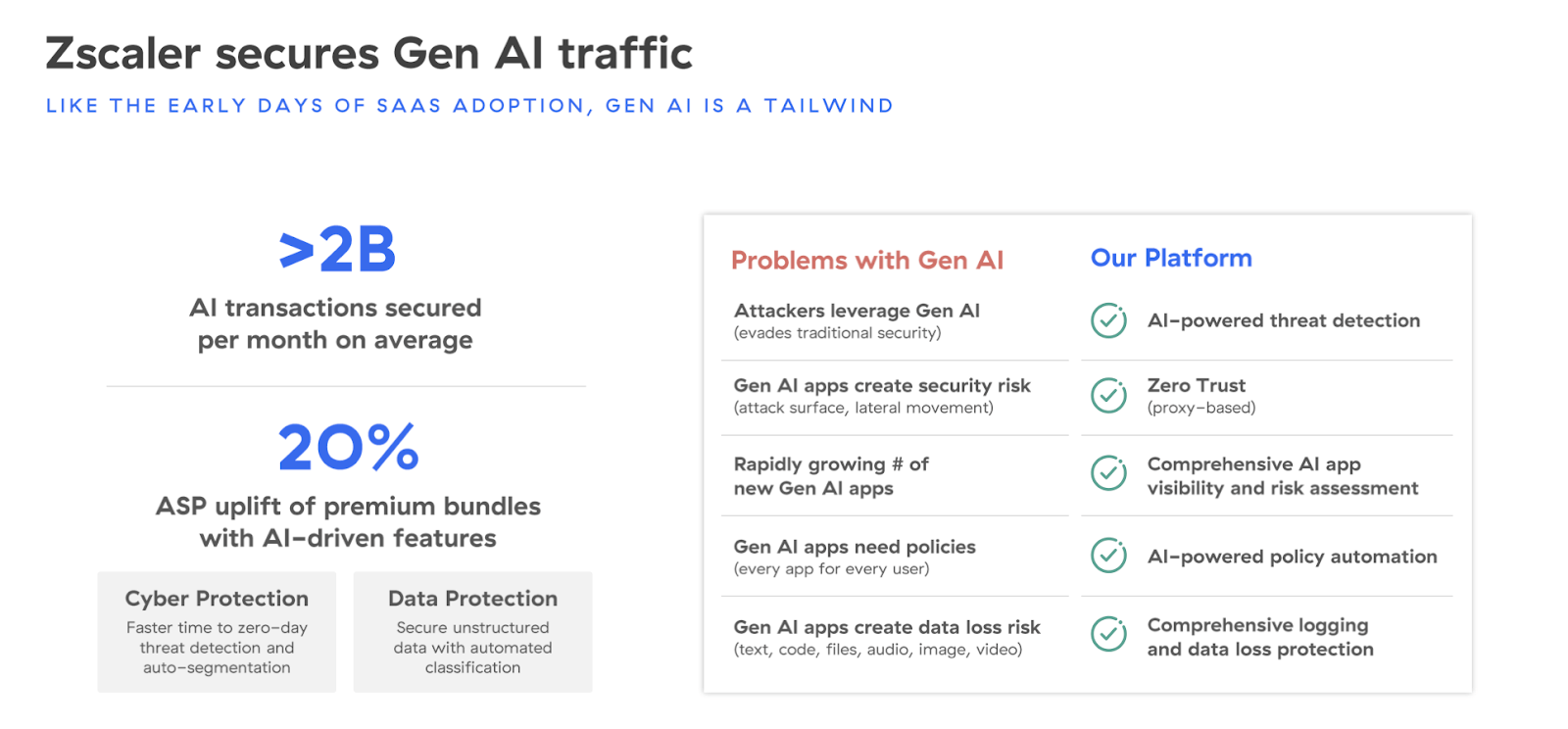

ZS is a cybersecurity inventory that’s disrupting the normal firewall safety mannequin. ZS’ zero belief structure protects knowledge and apps on the person degree, resulting in sturdy safety in a cloud-driven world.

FY24 Q1 Presentation

Generative AI could profit society, however it might additionally improve the prevalence and class of cyberattacks. That ought to speed up demand for new-generation cybersecurity firms like ZS.

FY24 Q1 Presentation

As of current costs, ZS was now not buying and selling “dirt-cheap” because it did for a lot of 2023. The inventory lately traded arms at round 17x gross sales.

Searching for Alpha

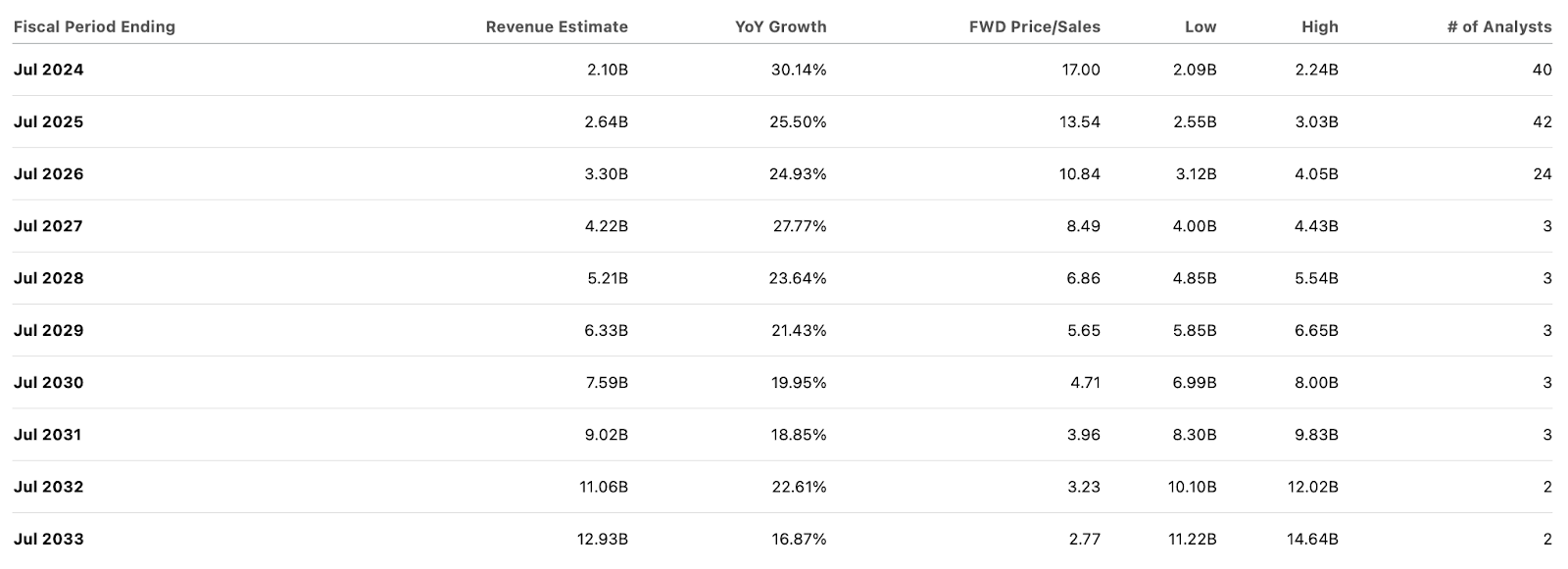

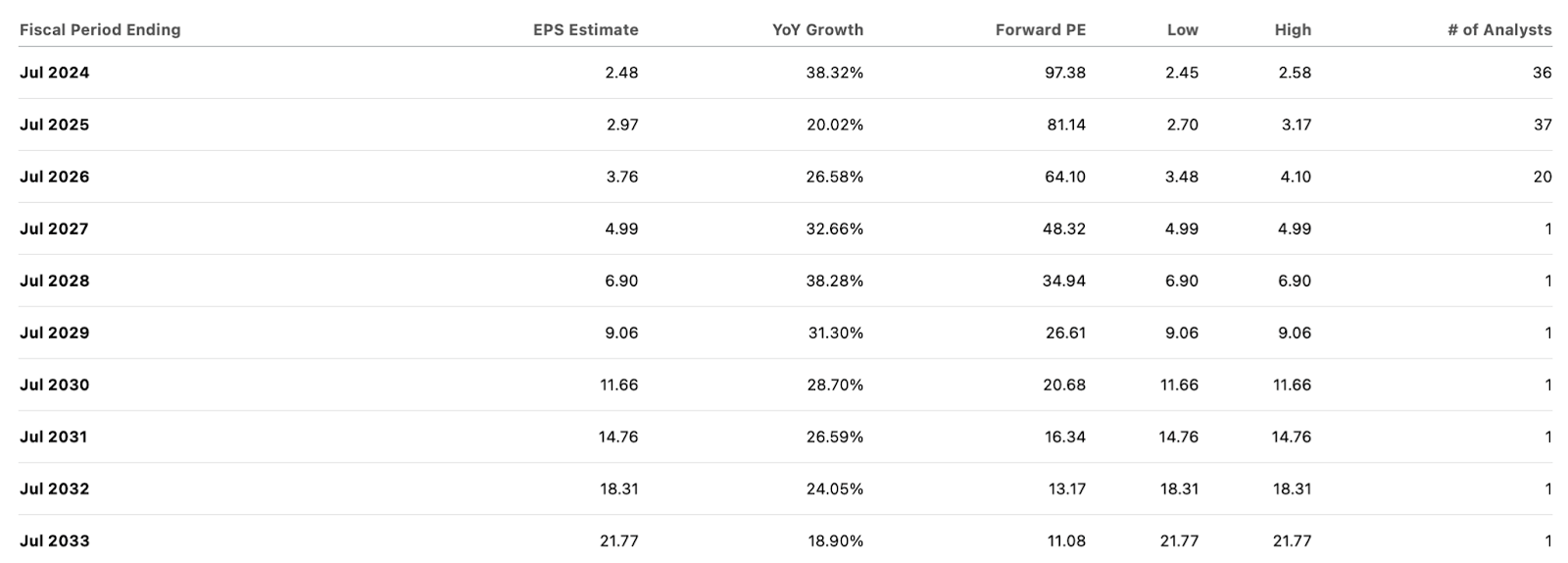

Consensus estimates name for ZS to point out sturdy working leverage over the approaching decade.

Searching for Alpha

Administration has given long-term steering for round 22% in non-GAAP working margins, although consensus estimates name for 25% non-GAAP web margins by 2033.

FY24 Q1 Presentation

I’m of the view that ZS can get to 25% to 30% GAAP web margins over the long run given the excessive 80+% gross margins. I can see ZS buying and selling at round 30x earnings by 2033, equating to a valuation of seven.5x to 9x gross sales. That suggests 11.7% to 14% compounded annual return potential over the following 9 years. That might seemingly beat the broader market, and consensus estimates don’t look too aggressive. Nonetheless, given the dearth of GAAP profitability, I’m of the view that these potential returns are usually not excessive sufficient to justify shopping for the inventory over the broader market index. I would like a potential return potential of 14% to 18% for a reputation of this sort of danger profile. If the corporate can execute on producing sustainable GAAP profitability and start rewarding shareholders with share repurchases, then I’d be extra inclined to decrease my hurdle necessities.

Whereas ZS continues to fireplace on all cylinders, I’m downgrading the inventory to a impartial ranking and promoting out of my place, as the present valuation just isn’t constructive to dependable market-beating returns.

![The Most Complicated Emojis within the World [Infographic]](https://whizbuddy.com/wp-content/uploads/2024/04/bG9jYWw6Ly8vZGl2ZWltYWdlL2NvbmZ1c2luZ19lbW9qaXMyLnBuZw.webp.webp)