baona/iStock by way of Getty Photos

By Sam Peters, CFA

Constructing an Adaptive Framework

There is no such thing as a system to get rid of uncertainty relating to the longer term. We imagine the very best method is to simply accept it and embrace probabilistic pondering. That is precisely what our funding course of is designed to do — give us a aggressive benefit by consistently studying and adapting quickly as we observe markets.

This adaptation course of is a cornerstone of how we’re formulating our ideas for 2024. Step one is growing a likelihood framework round doubtlessly key 2024 situations, permitting us to replace our personal possibilities as we observe vital occasions and to falsify misguided forecasts because the yr progresses. A vital second step is to try to unpack what markets have priced in, because it permits us to check our personal possibilities in opposition to the market’s and establish what surprises might transfer markets.

The Worth Fairness staff assigned possibilities to a few broad situations: a recession, a tender touchdown and a no touchdown the place inflation stays sticky above 2% and begins to re-accelerate.

State of affairs #1: Recession

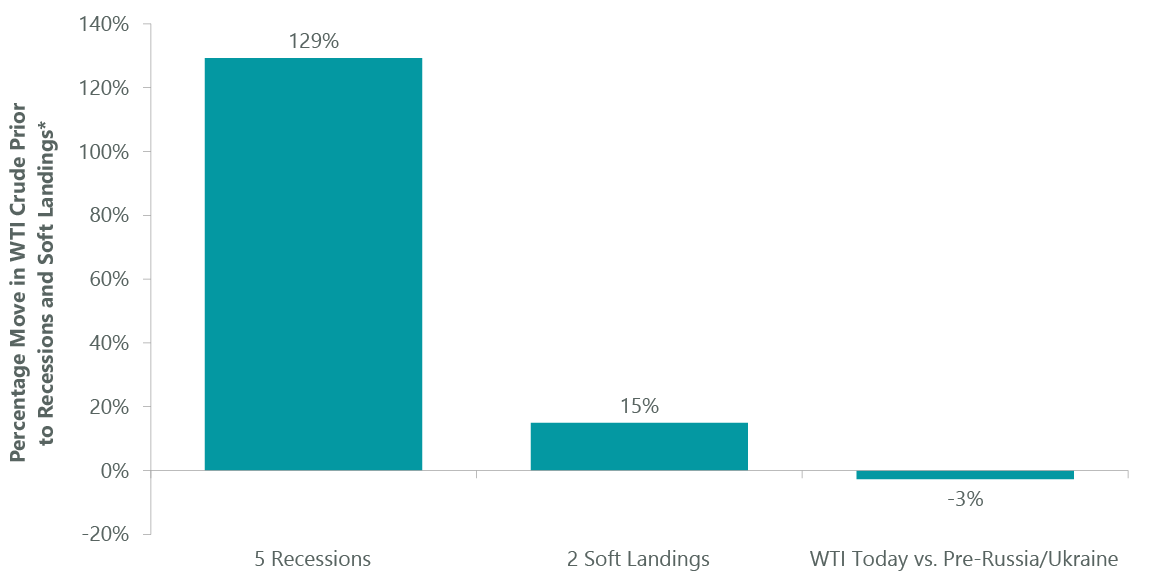

We estimated that the likelihood of a recession in 2024 was roughly 30%, with a spread of 15% to 60%, whereas we estimated that the market was pricing in a recession likelihood of roughly 20%. Some of the troublesome questions we requested ourselves in pondering this situation was had been fashions so improper in confidently calling for a recession in 2023? We expect markets are too targeted on financial coverage and haven’t integrated the huge change that’s underway from fiscal coverage growth, together with infrastructure buildouts and power transition. As well as, we had been improper in underestimating the continued resilience of U.S. shale oil and fuel provide and the Strategic Petroleum Reserve launch. There has by no means been a recession since 1970 with out each larger rates of interest and an oil spike. With oil down 3% because the Ukraine invasion, a vital recession variable is lacking.

Exhibit 1: Oil Costs Present Little Signal of Recession on Horizon

* Value motion in WTI Crude is calculated as the proportion change in worth from one yr previous to the final price hike to the primary job losses since 1970. As of Dec. 11, 2023. Supply: St. Louis Federal Reserve, Raymond James Analysis.

* Value motion in WTI Crude is calculated as the proportion change in worth from one yr previous to the final price hike to the primary job losses since 1970. As of Dec. 11, 2023. Supply: St. Louis Federal Reserve, Raymond James Analysis.

On the difference entrance, our capacity as worth managers to purchase cheaper recession insurance coverage within the fourth quarter and the basic strengths of our portfolio holdings, with resilient free money flows and fortress stability sheets, suggests our portfolio turnover in a recession will not be important. That is significantly true if a recession requires an oil spike, given our bullish views on power. Fairly, the turnover would come when buyers get scared and valuation spreads spike materially. We’re all the time energetic throughout home windows of utmost investor worry when the valuation math will get very straightforward, however the feelings are exhausting – there are nice alternatives to layer in excessive ahead returns from a behavioral overreaction.

State of affairs #2: Mushy Touchdown

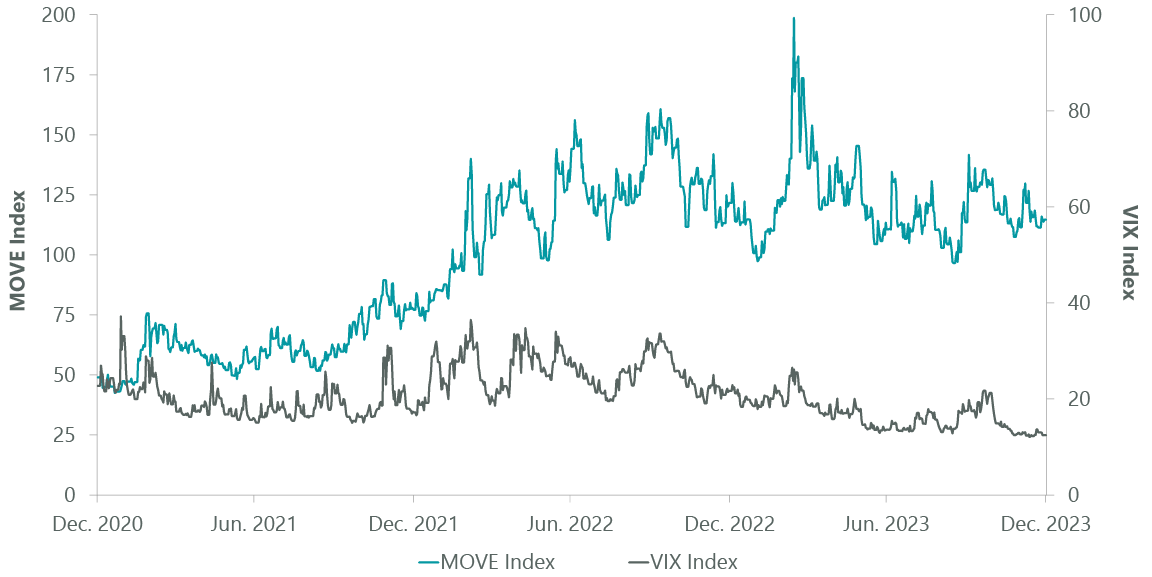

Simply as markets had been assured of a recession in 2023, markets are actually very assured of a tender touchdown. Our staff estimated a 50% likelihood of a tender touchdown, however suppose the market is pricing in a 70% likelihood amid tight credit score and valuations spreads, and really low measures of fairness volatility. Sarcastically, fastened earnings volatility has been properly above fairness volatility measures since early 2021. It’s a little bit of a paradox that historically calmer fastened earnings markets will be a lot much less sure than fairness markets, suggesting the fairness market is overconfident in its capacity to learn an unsure future.

Exhibit 2: Bond Volatility Surpasses Fairness Volatility

As of Dec. 31, 2023. Supply: Bloomberg.

As of Dec. 31, 2023. Supply: Bloomberg.

Adaptation in a tender touchdown situation would additionally possible not require materials portfolio turnover. Fairly, we’d count on the market to proceed to broaden out, because it did in late 2023. With indexes at excessive focus ranges, a continued broadening out would channel extra capital to areas with sturdy fundamentals and engaging valuations, locations the place our energetic valuation funding course of has led us. It could not take a lot, given how one-sided investor positioning is in mega cap U.S. progress shares.

State of affairs #3: No Touchdown

We expect a no touchdown situation is the occasion that may set off main volatility. Our estimate of no touchdown was roughly 20%, which is not less than double what the market has priced. Our bias is that inflation can be cyclical over the subsequent a number of years given large fiscal growth and ongoing deficits, accelerating capital funding required for the power transition and infrastructure buildout, and the shift in geopolitics that dampens structural deflation. As such, we’d count on inflation to bounce above 2% and cycle larger if we keep away from a recession. Sarcastically, the huge decline in rates of interest as markets priced in a tender touchdown late within the fourth quarter would be the key set off for larger inflation later in 2024. We’re coming off probably the most aggressive loosening of monetary circumstances ever, and markets are an enormous causal consider driving financial exercise by way of reflexive suggestions.

Adaptation in a no touchdown situation would require larger portfolio turnover, however a lot lower than for buyers not accounting for this chance. In a latest survey by Financial institution of America, international fund managers had been essentially the most underweight commodities versus bonds since March 2009. This stage of complacency in anchoring on one situation offers us the power to purchase no touchdown insurance coverage on a budget. Once more, we aren’t betting on situations, however reasonably inverting the method and seeing the place embedded expectations in doable futures are promoting properly beneath enterprise worth on the inventory stage. The place we will purchase power and supplies shares at high-single-digit to low-double-digit free money stream yields, with virtually no debt, and engaging dividend and buyback yields, we are going to take it — particularly once we get such a worthwhile inflation possibility.

No matter what situation performs out, our focus stays on discovering shares promoting beneath enterprise worth and the place we have now a extra optimistic view of future fundamentals than what the market has priced. This energetic valuation self-discipline requires that we get the basics proper with little or no assist from valuation a number of growth.

Sam Peters, CFA is a Portfolio Supervisor and co-manages the Worth Fairness Technique and the All Cap Worth Technique, and has over 30 years of funding expertise. Sam earned a BA in economics from the Faculty of William & Mary and an MBA from the College of Chicago. He obtained the CFA designation in 1997.