General_4530/Second by way of Getty Photos

January’s world PMI information signalled enhancing world financial situations in the beginning of 2024, along with a brightened outlook, with the solar shining particularly brightly upon the monetary providers sector amid a loosening of monetary situations.

Nevertheless, additional enhancements hinge largely on the outlook for world rates of interest and inflation.

Though welcome information has been noticed within the type of falling promoting value inflation in January, indicators of producing prices rising amidst a renewal of provide constraints – particularly in Europe because of the Pink Sea disaster and in sectors akin to building supplies and meals – will must be monitored fastidiously by way of the PMI information within the coming months.

Supply delays return in Europe amid Pink Sea assaults

S&P World’s PMI Remark Tracker information revealed that assaults on ships within the Pink Sea had a notable impression on provide chains in January, affecting supply occasions throughout quite a lot of manufacturing sectors.

The impression was unsurprisingly the toughest hitting in Europe, as diversions to transport traces across the circumference of Africa resulted in as much as two weeks being added to common lead occasions for European producers.

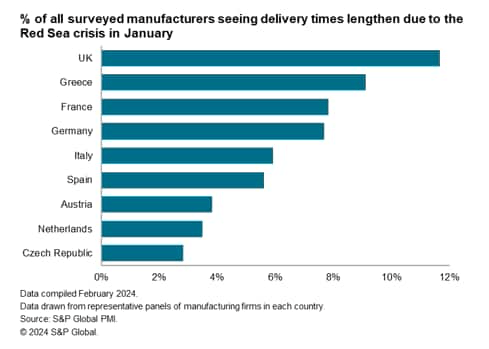

Consequently, provider supply occasions within the UK and eurozone lengthened for the primary time in a 12 months.

Of the European international locations monitored, UK producers had been the worst affected, with 12% of the survey panel seeing lead occasions deteriorate in January. Greek producers additionally generally noticed supply delays (9%), adopted by France and Germany (8%).

Whereas Europe confronted the longest delays, there have been stories of different economies additionally experiencing sea-related disruptions to their provide chains, together with South Korea, Australia and USA.

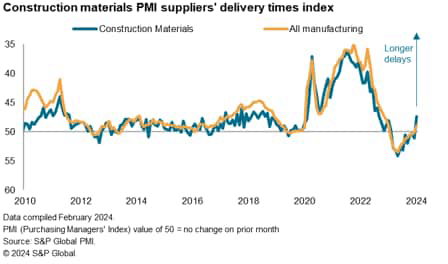

Building supplies and meals sectors face the longest delays

To look at the place provide delays had been most outstanding by sector, we dive into our January World Sector PMI information for additional insights.

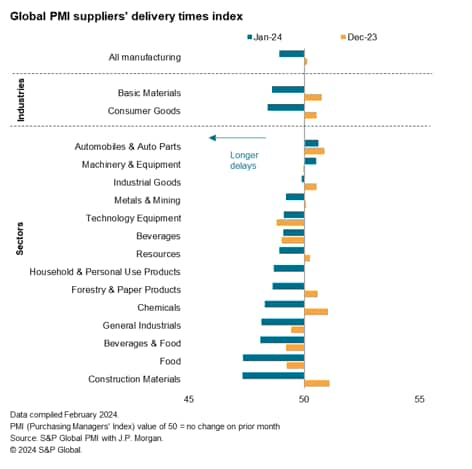

On the broad trade stage, producers of each fundamental supplies and client items witnessed suppliers’ supply occasions lengthening in January after having improved for 12 and 11 successive months respectively.

Detailed sector information additional confirmed that half of the 14 sector and sector teams, for which suppliers’ supply occasions information can be found, skilled a renewed lengthening of lead occasions in January.

Of which, the development supplies sector noticed the sharpest downturn in vendor efficiency. Anecdotal proof revealed that disruptions within the Pink Sea and provide shortages had been the primary drivers for the extension of supply occasions in the beginning of 2024.

The beverage & meals sector group adopted with the second-highest incidence of world delays, with meals producers feeling an particularly sharp worsening of provider efficiency.

Though rising demand partly contributed to the stress on provide chains, geopolitical disruptions and shortages had been once more listed as the important thing causes for delays in shipments of beverage & meals merchandise.

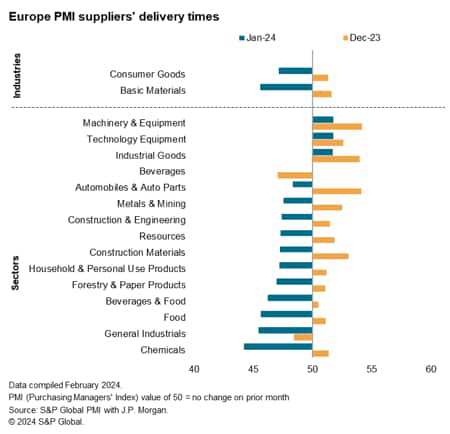

Wanting particularly at Europe, the place the disruptions from the Pink Sea disaster had been most prominently reported by PMI respondents, each industries for which suppliers’ supply occasions are tracked – fundamental supplies and client items – skilled a renewed deterioration in vendor efficiency.

This was likewise the case for two-thirds of the 15 detailed sectors tracked, with the respective suppliers’ supply occasions indices falling under the 50.0 impartial mark to sign a lengthening of lead occasions in January.

Nevertheless, in Europe it was not the development supplies however the chemical compounds sector that noticed essentially the most pronounced worsening of lead occasions at first of 2024, equivalent to latest warnings from corporations and observers of the sector.

Most sectors shrug off Pink Sea impression with optimism constructing

One essential query to ask amid the presence of delays pushed by the disruptions within the Pink Sea is the extent to which this has affected enterprise exercise.

Encouragingly, the general image offered is one among optimism amongst worldwide personal sector companies to date being largely unaffected by the impression from the Pink Sea, together with convincing indicators of goods producers exhibiting no inclination to construct security shares regardless of a renewed lengthening of worldwide manufacturing lead occasions.

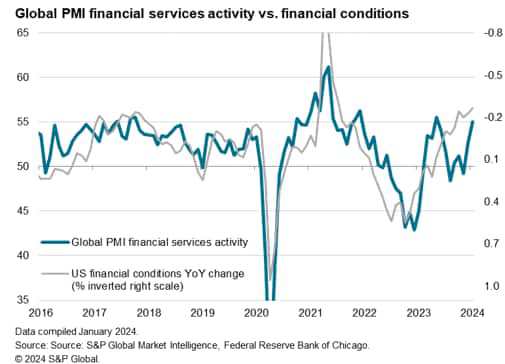

To a big extent, the development in enterprise optimism in the beginning of the 12 months was buoyed by the loosening of monetary situations as personal sector items producers and repair suppliers anticipate world central banks to decrease charges in 2024, which is supportive of demand.

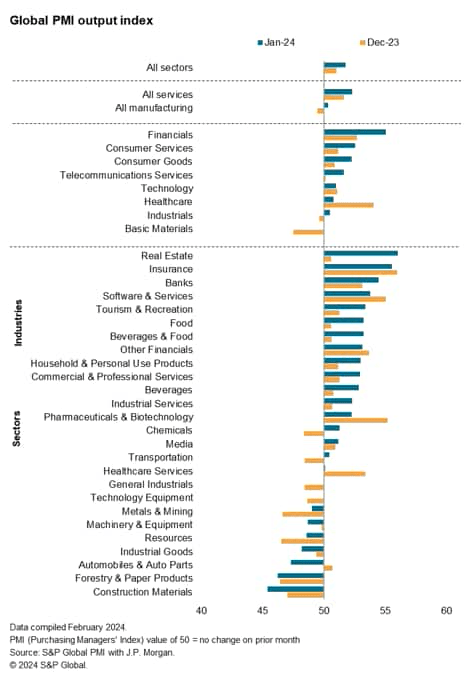

That is particularly evident in monetary providers exercise, with financials having risen to rank first among the many eight trade teams in January on the again of loosening monetary situations, as proven by the Federal Reserve Financial institution of Chicago’s monetary situations index within the chart under.

A majority of the 26 detailed sector and sector teams additionally noticed their respective enterprise exercise (output) index rise in the beginning of the brand new 12 months, although unsurprisingly concentrated amongst providers and services-related sectors.

On the flipside, the commercial items sector group was notably the one sector group to expertise a deepening of the downturn in the beginning of 2024, together with for each building supplies and equipment & gear sectors.

Whereas supply delays performed a component, akin to for building supplies (which confronted the sharpest deterioration in vendor efficiency among the many sectors tracked), broadly softening demand situations inside the industrial items sector group remained the important thing underlying purpose for the downturn in output in response to anecdotal proof.

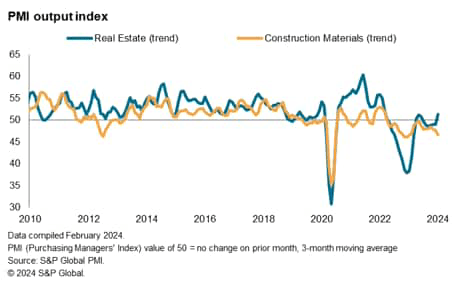

It have to be added that the actual property sector, which has a powerful correlation with the development supplies sector, has seen situations enhance at a extra marked tempo in the beginning of the 12 months, thereby opening up a spot with the latter.

It will likely be of curiosity to check how and when a convergence might happen for the 2.

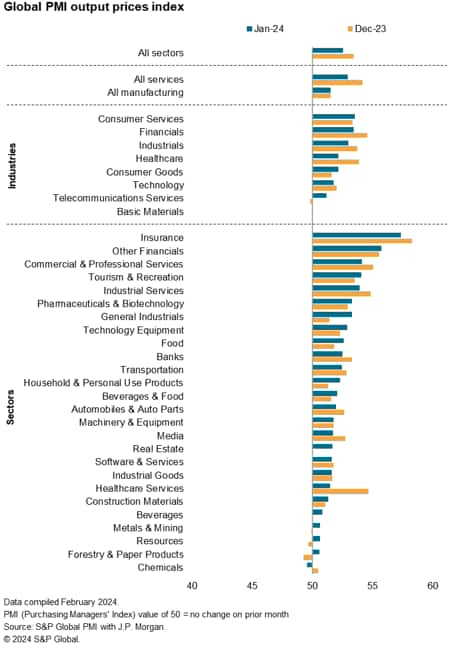

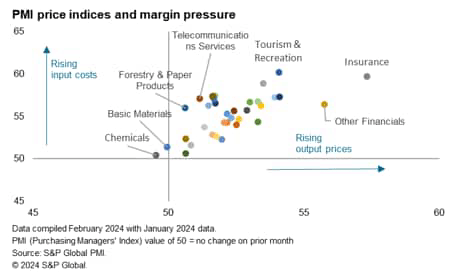

Manufacturing price will increase

One other essential side to analyze is the impression of the latest Pink Sea episode on inflation. As it’s, elevated stories of upper transport prices have surfaced amongst world producers, although on no account to the extent seen throughout the pandemic.

Service sectors remained on the head of the rankings when it comes to price will increase, although varied manufacturing sectors have additionally began to see a renewed enhance in price pressures.

The constructive information is that the sector most affected by the Pink Sea disaster – the development supplies sector – didn’t expertise any price spike because of elevated transport delays.

Nevertheless, given the reliance on sea transport for cumbersome and heavy building supplies, the sector might effectively stay in danger, particularly if demand and output for the sector ought to converge greater with actual property exercise as earlier highlighted.

A faster rise in beverage & meals prices will in the meantime be value monitoring, given the impression this has for headline client inflation. World meals prices rose on the quickest tempo in 4 months, sending output value inflation within the food-producing sector to the very best since September 2023.

Though the speed of promoting value inflation for meals merchandise stay under the worldwide common for all items and providers at current, with the prospect of elevated provide constraints particularly on this sector may present dangers for greater inflation and induce higher warning amongst policymakers for the decreasing of charges.

As it’s, warnings of probably greater meals costs because of Pink Sea disputes have been getting onto media headlines, together with from main meals suppliers.

Lastly, it’s also the sectors which can be seeing extra elevated enter value will increase however which can be unable to cross on the associated fee burdens to purchasers that ought to likewise be on the watchlist.

These sectors are sometimes essentially the most susceptible to weak demand ought to price inflation worsen on the again of geopolitical and different disruptions.

Editor’s Word: The abstract bullets for this text had been chosen by Looking for Alpha editors.