JHVEPhoto

Funding Thesis

HP has improved its earnings and free money circulate since our final protection 9 months in the past. After analyzing its progress drivers, we predict the corporate nonetheless has some method to go earlier than choosing up the robust progress momentum it wants. There are additionally slight enchancment in money and leverage of debt, however not sufficient to make sure the strategic spending it’d want for AI PC. We advocate a maintain at this level.

Evaluate

We initially lined HP Inc.(NYSE:HPQ) in July final 12 months in “HP Inc: Cheap For A Motive”. We deemed the inventory’s worth at $30.99 on the time to be low-cost, however we additionally discovered a number of causes that brought on buyers to low cost its worth. Most of all, it is the anemic progress and heavy debt load have stored some buyers on the sideline. Since then, its worth has dropped to as low as $25.67 and is now at $28.29.

Updates

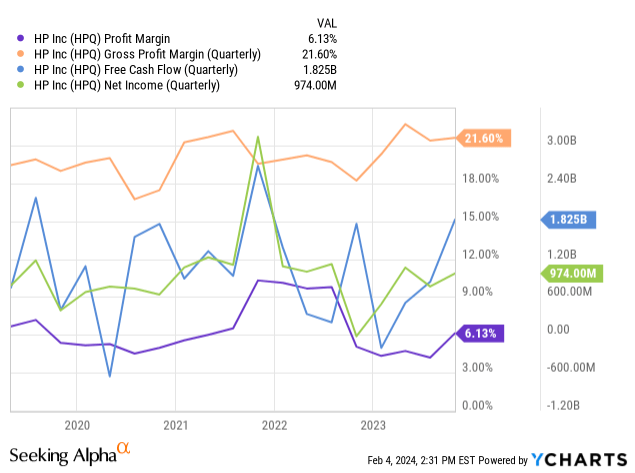

Within the previous article, we primarily expressed two considerations relating to HP’s short-term and medium-term progress. Within the short-term, it had weak free money circulate and internet earnings. Within the medium time period, its money place weaken to historic lows as compared with its heavy debt load that may hamper its long run strategic spending. Within the newest quarters, the corporate has increased earnings, free money circulate together with higher revenue margins.

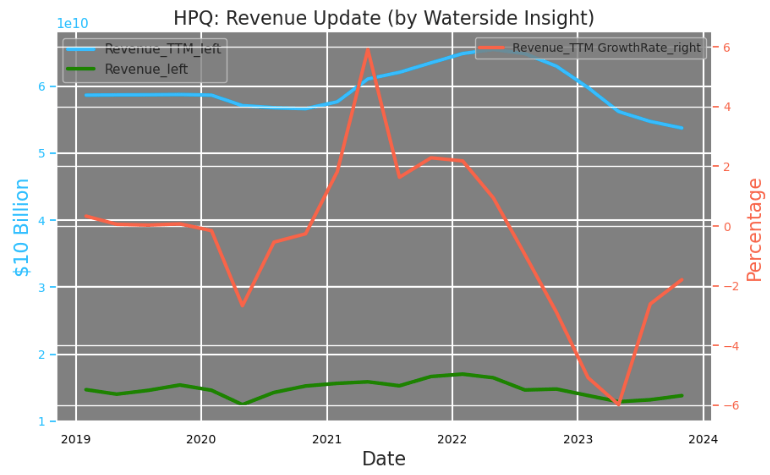

HP’s Q3 income on a QoQ foundation was up by 5.4%, a slight revival from the bottom degree since 2020, however on a TTM foundation, it hasn’t picked up the expansion but because it was nonetheless down 9.3% YoY. To keep away from the quarterly fluctuation, we charted its income progress fee on a TTM foundation, and it reveals since 2019, the typical progress fee has been virtually zero. We’ll evaluate this with the commercial pattern later.

HP: Income Replace (Calculated and Charted by Waterside Perception with knowledge from firm)

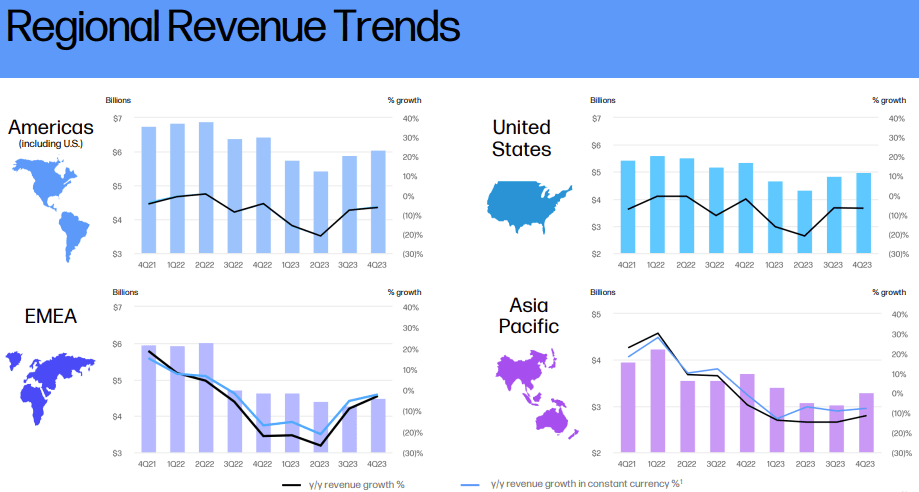

Regionally, the income declining pattern was halted and picked up in Americas and EMEA, whereas staying flatten within the US and Asia Pacific.

HP: Regional Income Tendencies (Firm Q3 Presentation )

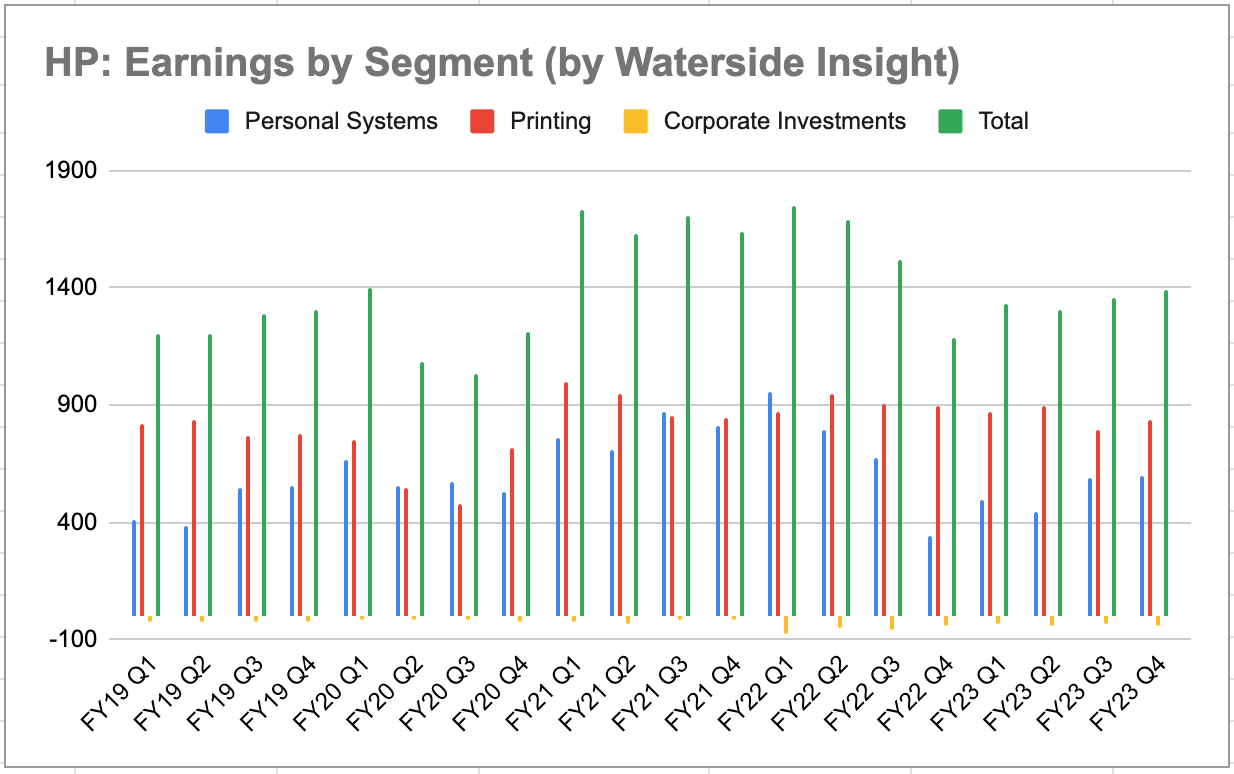

Probably the most attention-grabbing half is the reason of the place QoQ’s income progress comes from. If we have a look at its earnings by section, HP primarily derived it from both Private Programs or Printing. Printing has maintained above $750 million, which was the highest degree earlier than ’20. However Private Programs fell most noticeably in This autumn of FY22 and regularly recovered again to above $500 million, which is about 60% of its peak in 2021 and the typical earlier than ’20 each quarter.

HP: Earnings by Section (Calculated and Charted by Waterside Perception with knowledge from firm)

To zoom into the important thing progress areas within the final reported quarters, we see for the Printing section, Industrial Graphics continued to be robust, which was supported by Labels and Packaging. The hybrid system is pushed by seasonal spending in Shopper peripherals and Poly. Ink and paper subscriptions from shoppers grew YoY for This autumn and FY 23. Nonetheless, the weak spot got here from 3D & Personalization, which had {hardware} and provides declines from demand softness and delayed buying cycles. To drive higher near-term progress, HP supplied to mix its Jet printers with the designing software program Autodesk. Within the Private Programs (“PS”) section, Gaming grew double-digit sequentially for 2 quarters in a row and launched streaming peripherals reminiscent of Cloud III wi-fi gaming headsets. The Workforce Options supplied {hardware} gross sales for each PS and Print segments, and the corporate is attempting to mix PCs, printers, and Poly units all right into a single platform with {hardware} and software program integration. That is aimed extra in direction of firms that want simplicity to enhance productiveness and safety.

Though with a cautious outlook for this 12 months, citing the muted enterprise spending induced by macro challenges, the administration sees two primary drivers for 2024’s progress. One is the pandemic-driven PC buy that enlarged the put in base has handed by 4 years. So these machines will have to be refreshed and upgraded. One other is the Win 11 launch by Microsoft (MSFT) which generally acted as a tailwind driving private techniques buy prior to now. Each of those forces are anticipated to come back into play for FY 24’s topline progress for HP.

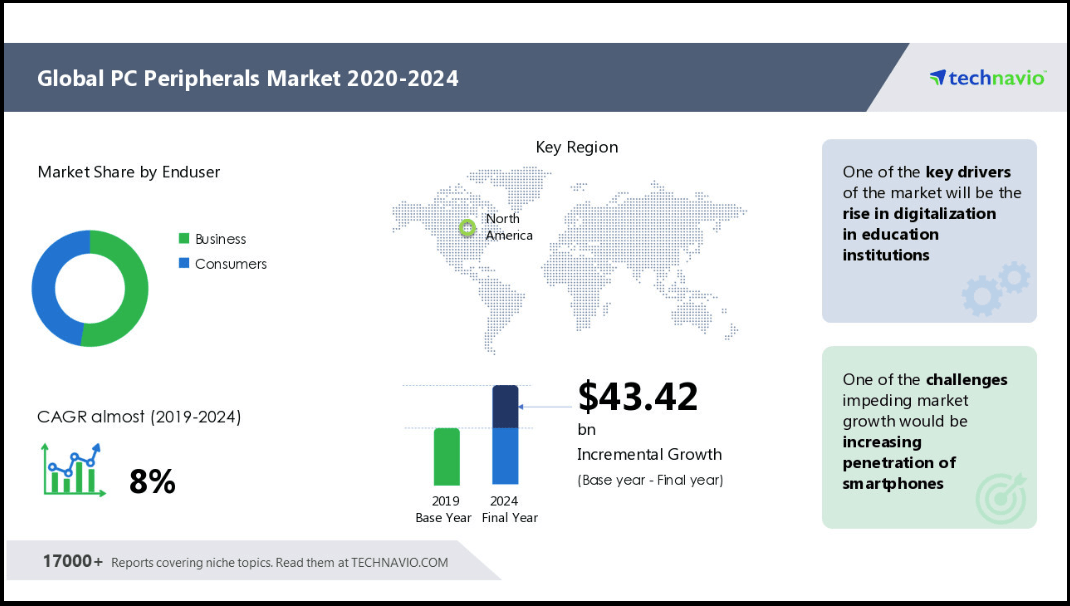

For the long-term progress, HP is seeing 5% to 10% progress in ’25 and ’26 from the Software Service Supplier (“ASP”) and AI PC. The administration is confident that the “computer peripherals” are going to have double-digit progress in income within the subsequent three years. However we’re not completely satisfied as a result of it wants the PS section to enter a lot stronger progress to attain that. In keeping with Technavio, the annual progress for international PC peripherals was 6.7% from 2019 to 2022 and is predicted to be 8% from ’23 to ’24. We simply mentioned the typical income progress prior to now 5 years for HP was about zero. Presently, it’s arduous to see a powerful catalyst for the PS section because the shopper PS continued to be weaker in contrast with the enterprise buyer base, as gaming alone is just not sufficient to drive complete {hardware} gross sales. Except there’s robust demand coming from enterprise prospects who go for the HP system as a complete. In different phrases, the marginal progress depends on the sale of the entire HP system, which brings in PS and Printing all collectively. If the worldwide PC peripherals progress in ’23 to ’24 is 8% as predicted, HP might want to herald further above business progress to be able to understand the double-digit progress. A big revamp for companies as a wave to occur will solely develop into doubtless if there’s a have to improve to AI-assisted techniques.

World PC Peripherals Progress 2019-2024 (Technavio)

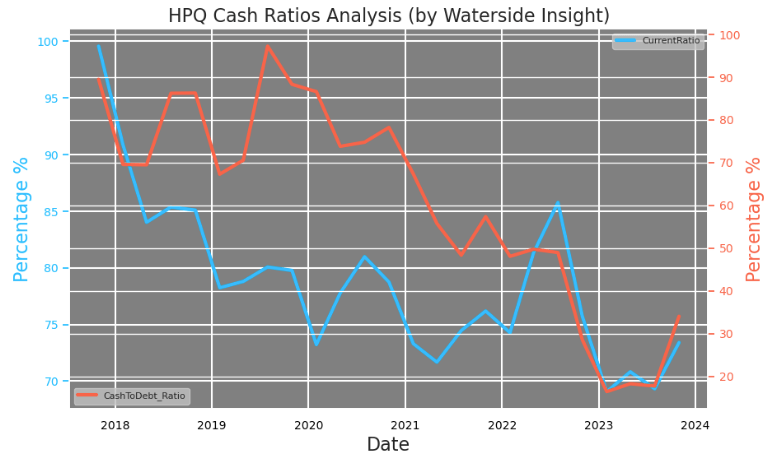

HP has been replenishing its money, with each cash-to-debt ratio and present ratio jumped by about 50% from their lows since early 2023. We mentioned about this beforehand and famous it as a priority that hampering the corporate’s long-term strategic spending capability. This can be a welcoming enchancment, however 0.75x present ratio and 30% cash-to-debt ratio will not translate into a snug place for it to spend on essential initiatives, reminiscent of AI PC.

HP: Money Ratios (Calculated and Charted by Waterside Perception with knowledge from firm)

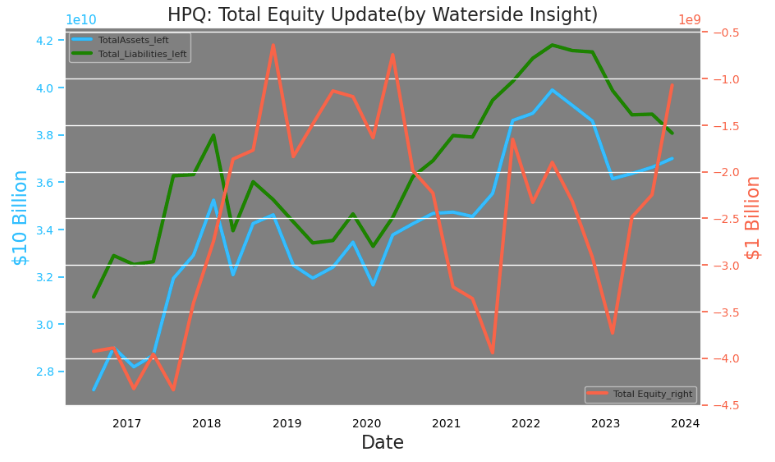

One other concern that buyers common have is the debt load. HP has been lowering debt whereas rising property on each fronts, leading to virtually $3 billion extra of complete fairness. If this pattern continues, it may obtain optimistic complete fairness for the primary time since 2016.

HP: Complete Fairness (Calculated and Charted by Waterside Perception with knowledge from firm)

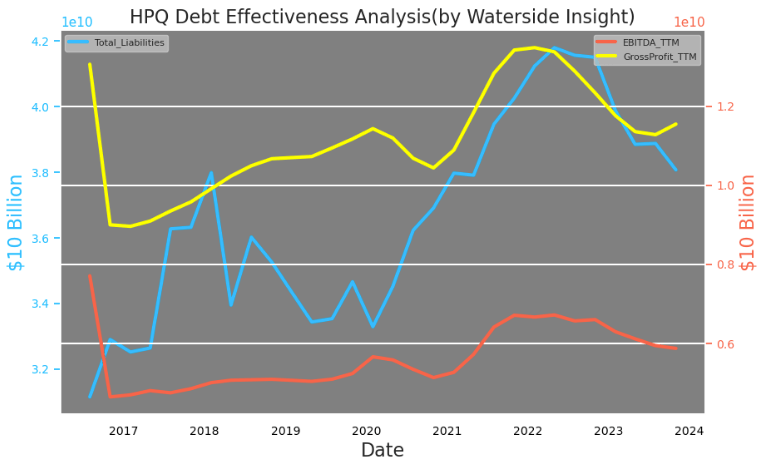

Certainly, since reaching a excessive for its debt load in 2022, HP has been trimming it down for the previous 12 months or so. Its complete liabilities have been down by 10%, however its gross income and EBITDA have additionally been trending decrease. The truth is, the corporate began ramping up borrowing in early 2020 when income have been falling, and higher income adopted. What we need to see is a more healthy natural progress depart from the debt cycle for HP, reminiscent of throughout 2018-19, when it was profitable in deleveraging and rising its earnings on the identical time. Extra natural progress would assist overcome the remaining obstacles in investor confidence within the power of its progress on a extra sustainable path.

HP: Debt Effectiveness (Calculated and Charted by Waterside Perception with knowledge from firm)

Monetary Overview & Valuation

HP: Monetary Overview (Calculated and Charted by Waterside Perception with knowledge from firm)

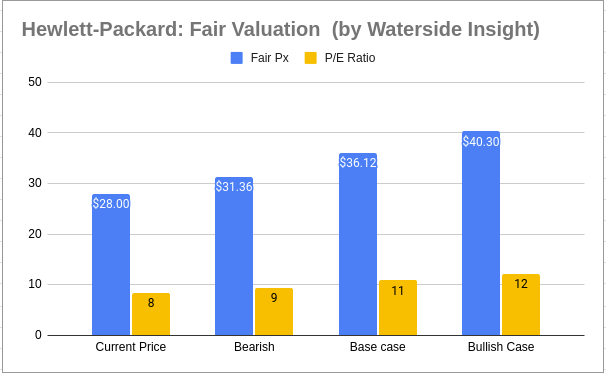

Now we have up to date our fashions on the valuation for HP, principally as a result of YoY decline in money circulate for FY 2023. Though it was pulled up within the final quarter, the entire 12 months’s free money circulate was nonetheless a 19% much less. We assumed a price of fairness of 5.53% and a WACC of 9.31%, reflecting the inflation fee that’s extra underneath management with increased rate of interest persisting. We barely raised the honest worth for all three circumstances assuming HP is on the trajectory for a close to time period restoration, and priced in a mean progress fee of 10% for the subsequent three years beginning in ’24. It appears the market continues to low cost the steerage given by the administration and is pricing the inventory barely under our bearish case.

HP: Truthful Worth (Calculated and Charted by Waterside Perception with knowledge from firm)

Conclusion

HP has pulled in a slight restoration within the final three quarters of FY ’23, and supplied extra bullish steerage for FY ’24 than we anticipated. We’re inspired by the expansion improvement, however nonetheless not seeing a powerful catalyst for a growth in enterprise PC peripherals spending, which the corporate’s progress intimately is determined by. We undertake a wait-and-see mode for now and advocate a maintain.