champpixs

Introduction

US packaging merchandise maker Berry International Group (NYSE:BERY) is the second largest place in my inventory portfolio in the mean time and February 7 was an eventful day for traders. In addition to releasing its Q1 FY24 financial results, the corporate revealed that the spin-off and merger of nearly all of its Well being, Hygiene and Specialties phase in a transaction that values this enterprise at $2.6 billion. Below the deal, Berry International will obtain $1 billion in money and its world nonwovens and movies operations will likely be merged with engineered supplies producer Glatfelter (NYSE:GLT). In my opinion, this deal is a win-win for each firms and I’m stunned the market appears upset contemplating the market capitalization of Berry International slumped by 13.02% on February 7 and eight. Let’s evaluation.

Background and particulars in regards to the deal

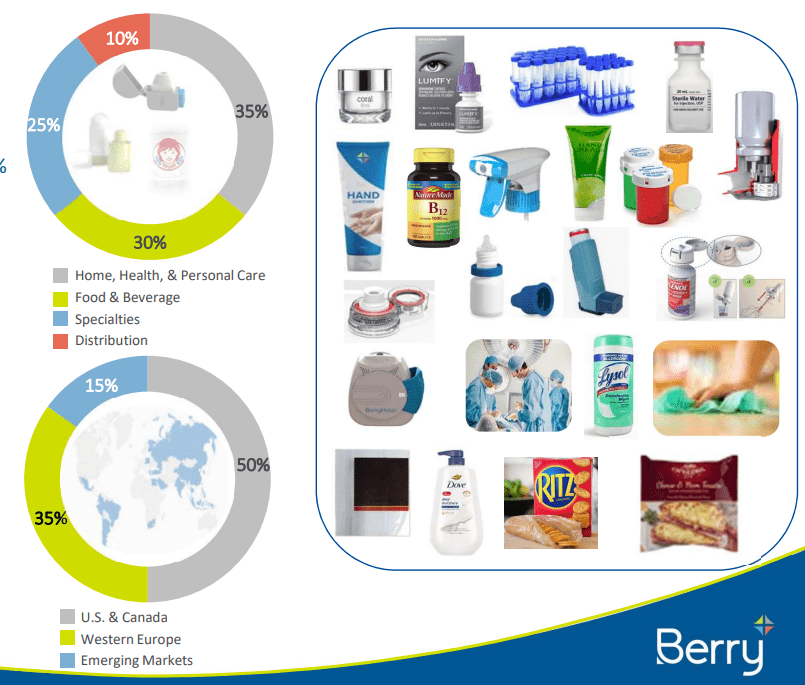

Berry International was established in 1967 and is an Evansville-based packaging firm targeted on North America and Western Europe. Greater than 70% of its gross sales are concentrated in shopper packaging options for meals, beverage, private care, and healthcare merchandise. Berry International produces over 100,000 varieties of objects and a number of the manufacturers with its packaging that I’ve at house embrace Pampers, and Listerine. The group has over 250 places throughout some 40 international locations and employs greater than 40,000 folks. The Well being, Hygiene and Specialties phase is concerned within the manufacturing of plastic materials that are utilized in diapers, wipes, well being care safety, and building supplies amongst others.

Berry International

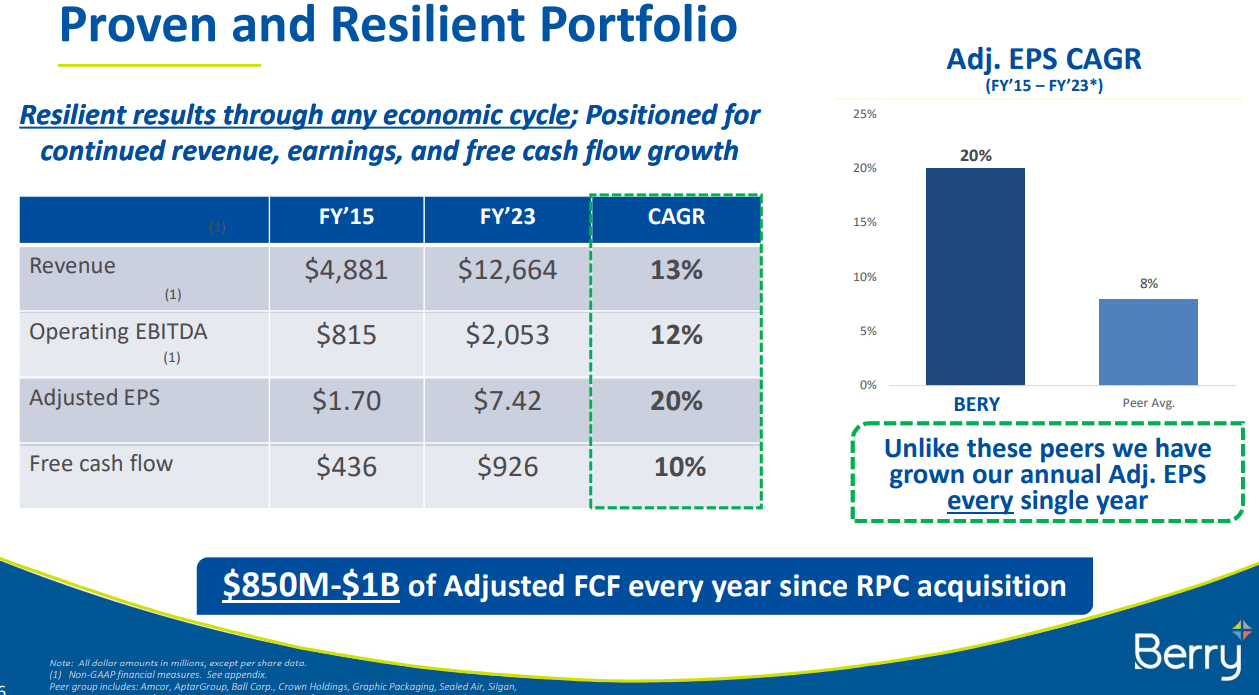

General, the worldwide packaging area is extremely fragmented, and Berry International has been rising its enterprise primarily by acquisitions over the previous decade. Its greatest buy was plastic packaging provider RPC Group for $6.5bn in 2019. Berry paid about $4.3 billion in money and assumed about $2.2 billion in debt. But, synergies and economies of scale allowed it to considerably enhance FCF as properly EPS and the group has been rising a lot sooner in comparison with its friends over the previous a number of years.

Berry International

But, it’s value noting that demand for Berry International’s merchandise acquired a lift through the COVID-19 pandemic, notably its Well being, Hygiene and Specialties phase. In FY20 and FY21, Berry targeted on decreasing its debt load however its share value was stagnant throughout that interval which led to an activist investor named Ancora suggesting in November 2021 a shift within the capital allocation technique – share buybacks, actual property asset gross sales, or a sale of the entire firm. Ancora argued that Berry International may very well be value $100 per share if bought. In November 2022, Berry International entered right into a mutual cooperation agreement with Ancora and one other activist investor and most of its $800-$900 million annual free money movement has been going into share repurchases since then.

Berry International

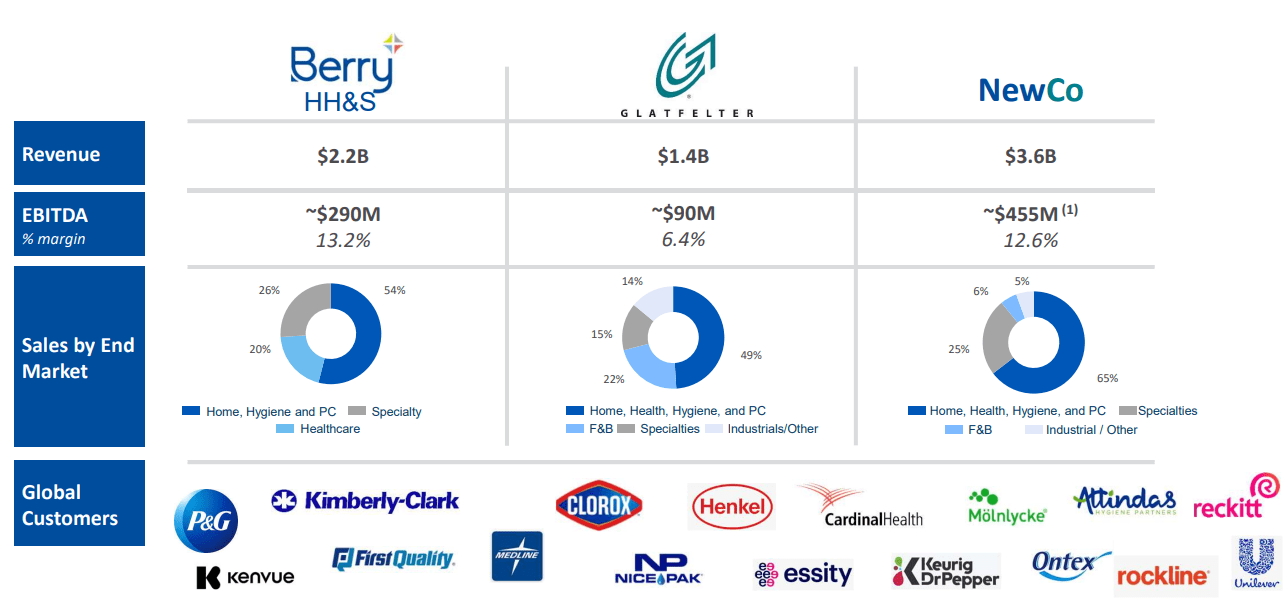

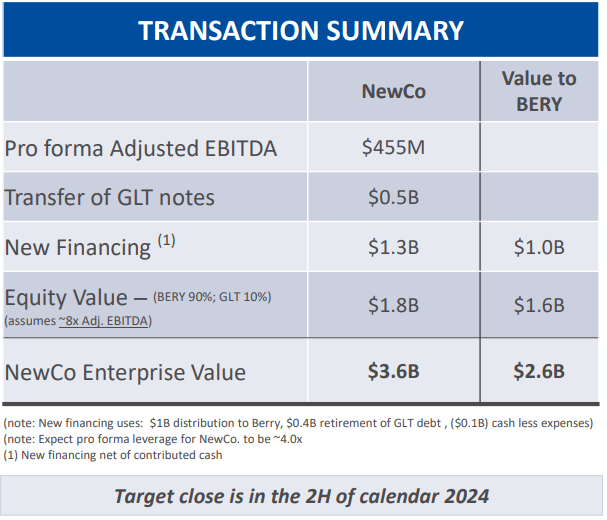

The sale of the Well being, Hygiene and Specialties phase is in step with this new route of the corporate and media studies that the operation was within the works began popping out in August 2023. Again then, analysts estimated that the worth tag for the enterprise may very well be as a lot as $2 billion. On September 8, Berry International confirmed that it was evaluating strategic alternatives for the enterprise which may embrace a sale, a strategic partnership, a three way partnership or a spin-off amongst others. That is how we obtained to the settlement with Glatfelter that was introduced on February 7. Below the deal, Berry International will spin off nearly all of its Well being, Hygiene and Specialties enterprise, merge it with Glatfelter and get 90% of the brand new firm, refinance the latter’s money owed, and obtain a web money distribution of about $1 billion at closing. This transaction will create a significant specialty supplies agency with TTM gross sales of round $3.6 billion and adjusted EBITDA of $455 million (this determine consists of price synergies of $50 million and mixed professional forma changes of $25 million by 12 months three). The but unnamed firm could have 45 places, over 1,000 clients, and a few 8,650 workers.

Berry International

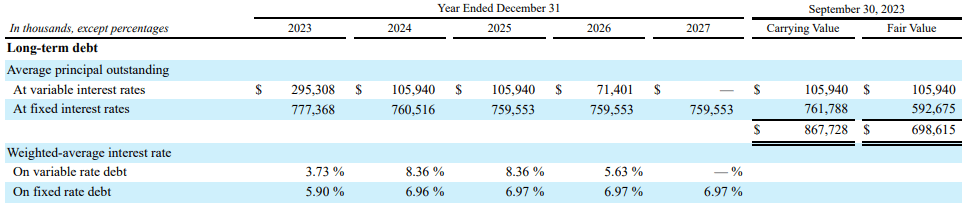

In my opinion, the deal is a godsend for Glatfelter as the corporate has been struggling financially for the reason that begin of the Ukraine conflict as defined intimately by The Insiders Discussion board on SA here. Mainly, the corporate had key clients for its high-margin wallcover merchandise in each Russia and Ukraine and excessive power prices in Europe didn’t assist both. Earlier than the cope with Berry International was introduced, Glatfelter was struggling to restructure its enterprise and return to the black which was made much more difficult by the excessive price of its debt. As of September 2023, the weighted-average rate of interest paid was 8.36% (page 47 of the Q3 2023 monetary report) and the market capitalization of Glatfelter was lower than $60 million earlier than the transaction with Berry International was introduced.

Glatfelter Glatfelter

Below the terms of the cope with Berry International, about $400 million of Glatfelter’s debt will likely be retired and solely the 4.75% senior notes due 2029 will stay. As well as, the brand new firm has obtained dedicated financing from two banks. In spite of everything is claimed and executed, the brand new agency could have a leverage of about 4x. This quantity isn’t far off Berry International’s personal leverage stage of three.7x and the transaction is anticipated to be leverage impartial for it. At 8x EV/EBITDA, the brand new firm would have an fairness worth of about $1.8 billion and be 90% owned by the shareholders of Berry International.

Berry International

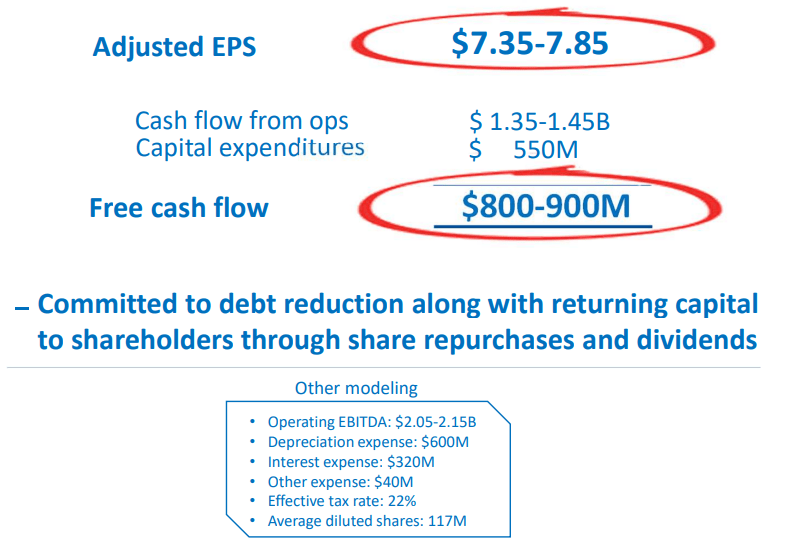

The advantages for Berry International from the deal are that it could give attention to its Client Packaging, and Flexibles segments that are much less cyclical and require much less sustaining CAPEX. As well as, the worth for shareholders was estimated $2.6 billion, which is round $600 million greater than what analysts have been anticipating. Then why did the share value droop? Properly, I believe there are two predominant causes. First, 8x EV/EBITDA is likely to be too optimistic for a packaging enterprise that’s experiencing falling demand in addition to headwinds in Europe. Glatfelter has a market capitalization of $100 million as of the time of writing, which means that the market is valuing the brand new firm at simply $1 billion. This could drop the worth for Berry International’s shareholders to $1.9 billion. The determine isn’t too far off from the $2 billion estimates by analysts August, however the latter have been anticipating a part of the sum for use for share buybacks again then. With Berry International sticking with its plan to scale back leverage to three.5x by the top of FY24, because of this the $1 billion in money that it’s going to get will most likely be used for debt compensation, limiting share buybacks. The second cause for the share value droop appears to be the delicate Q1 FY24 monetary outcomes of Berry International. The corporate booked non-GAAP EPS of $1.22, missing by $0.09. Income, in flip, went down by 6.9% 12 months on 12 months and missed by $90 million. On a optimistic be aware, Berry International saved its steerage for FY24 unchanged because it expects the second a part of its fiscal 12 months to be stronger. It nonetheless expects to e book EPS of $7.35-7.85 and free money movement of $800-900 million.

Berry International

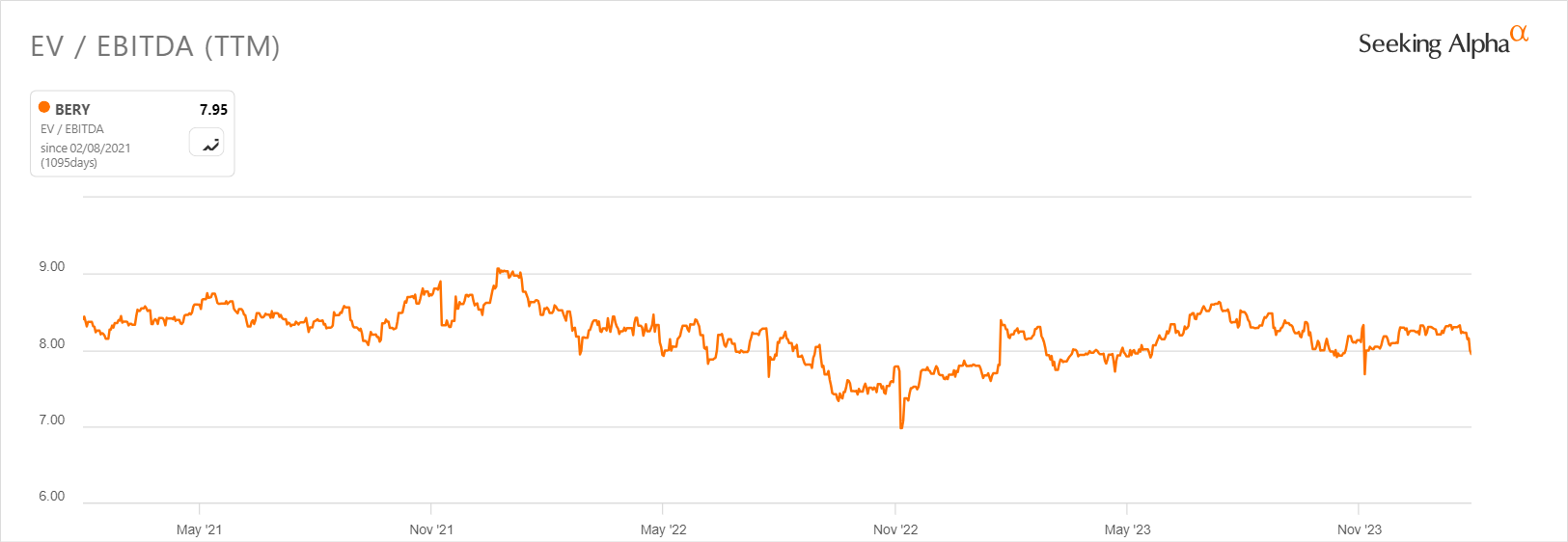

General, I believe that Berry International is getting an excellent value for its Well being, Hygiene and Specialties enterprise for shareholders even when Glatfelter continues buying and selling at round $2.20 per share. Whereas the Q1 FY24 outcomes have been considerably underwhelming, the steerage for the fiscal 12 months nonetheless appears to be like sturdy and the share value ought to obtain assist from buybacks within the coming months as share repurchases for the quarter have been simply $7 million. The corporate thus has $435 million remaining underneath its share buyback plan. historic information, Berry International has hardly ever been valued under 8x EV/EBITDA over the previous three years. In view of this, I’m optimistic that the valuation of the corporate will enhance to round 8.5x EV/EBITDA over the approaching months.

Searching for Alpha

Wanting on the draw back dangers, I believe the main one is that Berry International may very well be overoptimistic about its monetary efficiency over the second half of FY24. The packaging trade is susceptible to recessions and Europe has been fighting progress over the previous two years. Whereas unlikely, it’s additionally attainable that the cope with Glatfelter may fall by if the latter receives a greater provide for its enterprise over the subsequent few months. The transaction wants a inexperienced mild from Glatfelter’s shareholders.

Investor takeaway

I believe that Berry International is getting an excellent value for its Well being, Hygiene and Specialties enterprise and its inventory is beginning to look oversold. Whereas a few of fall available in the market capitalization may very well be attributed to the weak Q1 FY24 monetary outcomes, I doubt that it’s a significant half contemplating the steerage for the fiscal 12 months was saved unchanged. In my opinion, the valuation of the corporate is probably going to enhance to round 8.5x EV/EBITDA over the approaching months.