designer491

A number of of our members have requested about most well-liked inventory. Does it slot in an revenue manufacturing unit? In that case, the place? It is a good query.

Most well-liked inventory has sure qualities of each fairness and debt. How ought to revenue traders like us, who focus on maximizing revenue progress by way of reinvesting and compounding excessive yields, regard most well-liked inventory? It clearly seems to have some traits that make it a candidate value contemplating. The query then turns into, how does it examine with different options, like senior loans and excessive yield bonds, in addition to high-yielding shares, like utilities, actual property, energy-based MLPs, and so forth.

Listed here are some factors value contemplating:

In contemplating “fixed income” investments, we have to decide what we are literally “betting on” once we make the funding:

- Company loans and high-yield bonds are usually made to non-investment grade companies, the place the first danger is danger of default (i.e. pure credit score danger). There’s little or no rate of interest danger since loans are “floating rate” with charges re-adjusted each month or quarter, and high-yield bonds are comparatively brief time period (5 years or so), so a serious portion of your portfolio is being re-priced yearly at present “updated” rates of interest. Conventional bonds (long run and decrease yields) carry negligible credit score danger, however appreciable rate of interest danger, as a result of if charges transfer increased, you could be caught with a substandard return for years, or face a capital loss in case you want/wish to promote earlier than maturity.

- Credit score danger is comparatively simple to mannequin and handle, particularly within the mortgage market the place nearly all loans are secured by collateral, which ends up in recoveries on defaulted loans usually within the 60%-70% vary. Even unsecured bonds normally recuperate 40%-50%. This implies a headline “default rate” of, say, 5% (a recession stage default fee) would usually lead to losses of solely 2%-3%, consuming into an investor’s yield however not even touching principal.

- Our “bet” in a well-diversified credit score funding is that the tons of of borrowing firms represented within the funds we personal will keep alive and pay their money owed. For taking this danger we’re paid a yield, as we’ll see under, at the moment within the 10%-11% vary for company senior loans and high-yield bonds. As talked about above, defaults within the 5% vary (a lot increased than we have skilled lately) would knock that yield right down to the 7%-8% vary in a given 12 months, however would not invade principal.

- Against this, an fairness investor is betting that an organization (or many firms, in the event that they make investments through a fund) is not going to solely keep alive and pay their money owed (the naked minimal) however may also thrive and develop in order that their earnings and dividends enhance. If all the businesses do is survive however do not thrive and develop, then their collectors might be glad, however their stockholders will probably be very upset.

- It must be apparent that an fairness investor is taking the identical credit score danger as a mortgage, bond or mounted revenue investor that the corporate will fail to outlive and pay its money owed. However in addition to that, it’s taking the extra danger that the corporate will stagnate and ONLY survive, whereas failing to develop and make its inventory value extra.

- Because of this it is crucial that in case you spend money on shares, that your returns must be extra than these of a credit score investor who is barely taking the “existential” danger of defaulting and going bust, however shouldn’t be taking the extra “entrepreneurial” danger of failing to develop its enterprise and earnings.

These points develop into essential once we assess the attractiveness of most well-liked inventory, which resides someplace halfway between debt (i.e. credit score investments) and fairness.

- Like debt, most most well-liked inventory (until it is “convertible preferred,” which is actually a deeply subordinated bond with an fairness possibility connected to it) is mounted in that it has no upside that grows together with the issuer’s efficiency, the best way fairness does.

- However in contrast to most loans and bonds, most most well-liked inventory has no expiration (i.e. maturity) date, so the chance that its dividend yield could develop into out of sync (i.e. too low) in comparison with prevailing rate of interest ranges is way better than a hard and fast time period bond the place the investor is aware of that they’ll at the least get their principal again at par on a identified future date. So if a most well-liked inventory’s worth drops as a result of rates of interest rise, an investor could haven’t any selection however to carry it indefinitely and accumulate a sub-standard yield, or promote out at a loss. Issuers generally “call” most well-liked shares in and pay them off, however they haven’t any incentive to try this if the speed on the popular is low, by present market requirements; provided that the speed is increased. So if an investor is sensible or fortunate sufficient to purchase a most well-liked at an unusually excessive fee, that is the one the issuer will wish to repay as quickly as attainable.

- As well as, when firms do default, most well-liked inventory is on the backside of the legal responsibility stack, and will get paid nothing until and till the senior secured loans and the unsecured bonds above them are repaid in full.

So most well-liked inventory has the worst of all worlds in some methods, in that it has not one of the upside that common fairness does, but it surely additionally has not one of the protections when it comes to collateral or precedence within the legal responsibility pecking order that loans and bonds have. Because of this most most well-liked inventory is issued by pretty well-established funding grade firms, the place the chance of default is lower than that of the standard non-investment grade firms that concern senior loans and excessive yield bonds.

Backside Line:

- When it comes to safety, if the issuer’s credit score ought to go south, and it defaults or goes bust, the popular inventory investor is not any higher off than a stockholder.

- Nevertheless, if the corporate does effectively and grows, the popular inventory investor doesn’t take part within the upside.

- The one benefit the popular stockholder will get is the next money yield than the inventory dividend that standard fairness holders get.

- However, they’re usually much less effectively compensated from a yield standpoint than the debt above them (loans and bonds), and naturally they’ve not one of the protections that these mortgage and bondholders have within the occasion the corporate defaults.

Now let’s take a look at the numbers, to see if the outcomes bear out the speculation.

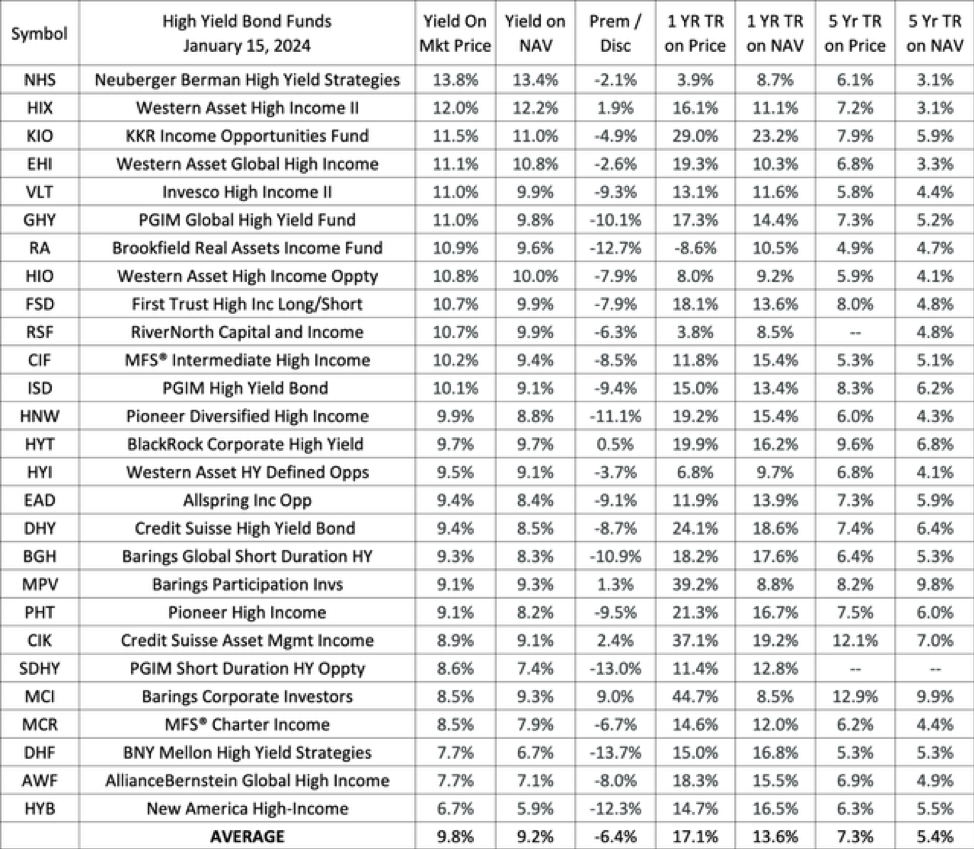

Listed here are the lists of (1) most well-liked inventory funds, (2) high-yield bond funds, and (3) senior mortgage funds coated by CEF Join. I sorted by these three classes, after which parsed the lists to take away funds that have been mislabeled or weren’t “real” members of the class. For instance, there have been funds holding collateralized mortgage obligations ((CLOs)) listed as mortgage funds, and another mortgage and bond funds that held different extra unique investments too, which I eliminated to maintain the lists pretty “generic.” I ranked them by distribution yield, simply as a place to begin for comparisons.

CEFConnect CEFConnect CEFConnect

Here is a abstract of the outcomes:

SB

As you’ll be able to see, the popular inventory funds, whereas they’ve supplied affordable returns, haven’t come near matching the latest returns of our credit score investments, both from a distribution yield standpoint or when it comes to whole return. Because of this I’ve emphasised mortgage and HY bond funds in my private portfolio, in addition to in my “core” mannequin portfolio, each of which goal to focus totally on the “yield” part of their whole return, with capital features, if achieved, being icing on the cake.

If most well-liked inventory funds have a spot in an Revenue Manufacturing facility portfolio, it could be in taxable portfolios, the place the certified revenue they generate (as a result of they pay dividends, not curiosity) will probably be taxed at decrease charges. Then we have now to ask ourselves if we wish to accept the decrease whole returns (as a result of most well-liked stockholders sacrifice the possibility to earn the capital features that “real” fairness funds present us) with a view to get barely increased distribution yields.

I sit up for your feedback and questions, and thank these readers who raised the query and precipitated me to focus extra intensively on this fascinating subject.