MicroStockHub/iStock by way of Getty Photos

Thesis

Cornerstone Strategic Worth Fund, Inc. (NYSE:CLM) is a closed-end administration funding firm, initially included on Might 1, 1987. The automobile is an fairness CEF, aiming to offer buyers with excessive dividends from a portfolio of fairness holdings. Lengthy time period, the fund’s complete return matches the one exhibited by the S&P 500, however CLM is a basic story of a CEF advertising and marketing itself by way of a excessive dividend yield, with the automobile now paying 18%.

On this article we’re going to have a more in-depth have a look at this CEF, its composition and monetary engineering, and derive an opinion on whether or not retail buyers are properly served by coming into this title on the present juncture.

The CEF has intently mirrored the S&P 500 till the ‘AI’ revolution

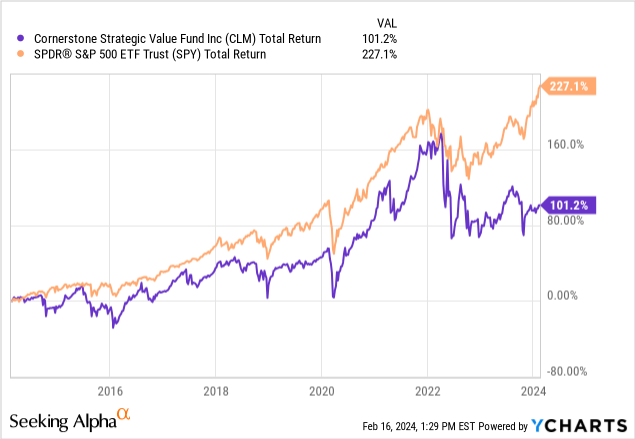

If we take a look on the complete returns posted by the fund over a protracted time frame, we will discover CLM did a reasonably good job of mirroring the S&P 500 complete returns till the beginning of the ‘AI revolution’, and the run-up in costs for names akin to Nvidia (NVDA):

An fairness CEF which pays a really excessive dividend yield must be analyzed from a complete return perspective, as a result of that’s what the CEF construction finally does – remodel threat issue returns (on this case equities) into dividends. As much as the center of 2022, CLM’s complete return intently matched the one exhibited by SPY, however then began lagging.

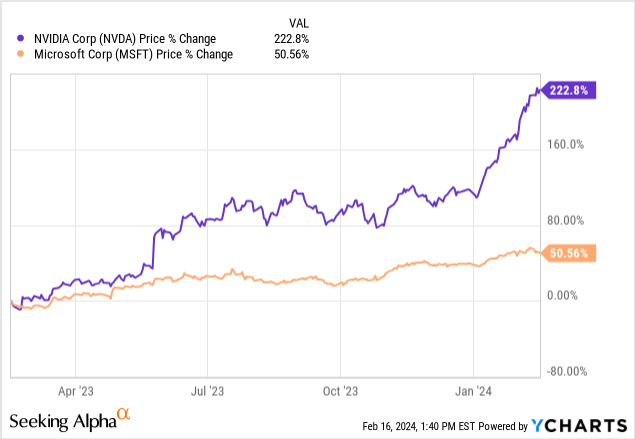

If we have a look at the fund’s composition, we will see it’s underweight sure AI names, specifically NVDA, which represents solely 3% of the CEF, versus 4.35% for the S&P 500. Equally, one other mega-cap tech winner, specifically Microsoft (MSFT) is just 6% of CLM versus 7.2% for the S&P 500. Trying on the efficiency of those two names previously yr, we will start to grasp why these small variations begin to matter:

Prior to now yr, NVDA is up 222%, whereas MSFT is up 50%. If CLM would have been chubby AI names versus the index, it could have outperformed.

The 18% dividend overshoots market returns and is thus not supported

The CEF has a managed distribution plan:

The Fund has maintained its coverage of standard distributions to stockholders which continues to be in style with buyers. These distributions usually are not tied to the Fund’s funding revenue and capital beneficial properties and don’t signify yield or funding return on the Fund’s portfolio. As at all times, the month-to-month distributions are reviewed and authorised by the Board all year long and are topic to vary at their discretion. In any given yr, there is no such thing as a assure that the Fund’s funding returns will exceed the quantity of the distributions. To the extent that the quantity of distributions taken in money exceeds the full web funding returns of the Fund, the belongings of the Fund will decline. If the full web funding returns exceed the amount of money distributions, the belongings of the Fund will enhance.

Supply: Semi-Annual Report

As a retail investor it is advisable perceive {that a} CEF construction can set any dividend it needs to take action. Sure CEFs make the most of excessive dividend yields to draw buyers, even when the underlying asset class can’t present the cash-flows and capital beneficial properties to maintain these distributions.

CLM may be very straight ahead within the assertion that in any given yr, the fund’s belongings may not generate the return essential to cowl the distribution, and thus in these situations the online belongings of the fund will decline.

In impact, if we have a look at the long run returns supplied by the S&P 500, they presently tally as much as 12.5% yearly on a 10-year lookback:

S&P 500 Returns (Morningstar)

This interprets into the underlying fairness portfolio in CLM solely having the ability to generate 12.5% annual dividends, so long as the CEF mirrors the S&P 500 (which it has not). The present 18% yield the fund is paying will not be supported, and primarily based on empirical knowledge, by no means will. Thus, you’re looking at 5.5% (18%-12.5%) as at all times being a return of your individual capital, somewhat than a real dividend yield.

The fund’s Part 19 notices additionally present a really heavy return of capital utilization:

January 2024 Part 19 Discover (Fund)

For the January 2024 cost date, over 50% of the dividend represents return of capital.

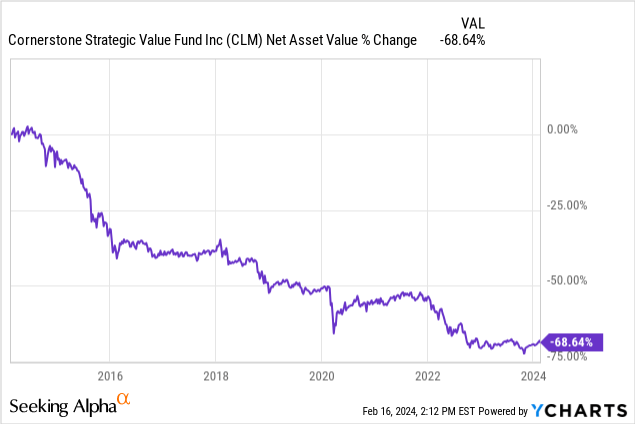

The discrepancy between what the S&P 500 could make yearly (and thus CLM), and what the fund pays out in dividend distributions, can clearly be seen within the fund’s historic NAV efficiency. As per the fund’s personal phrases, after they overdistribute, the online belongings of the fund transfer down:

Prior to now ten years, the fund’s NAV is down -68%, or roughly -6.8% per yr, which equates intently to the determine we calculated above because the distinction between dividend yield and what the S&P 500 generates. Anticipate this state of affairs to persist, because the S&P 500 will be unable to constantly generate 18% annual returns.

Threat components for the fund and the ahead for its worth

There are two essential threat components for this CEF:

- low cost to NAV ranges

- efficiency of the S&P 500 and fund fairness holdings

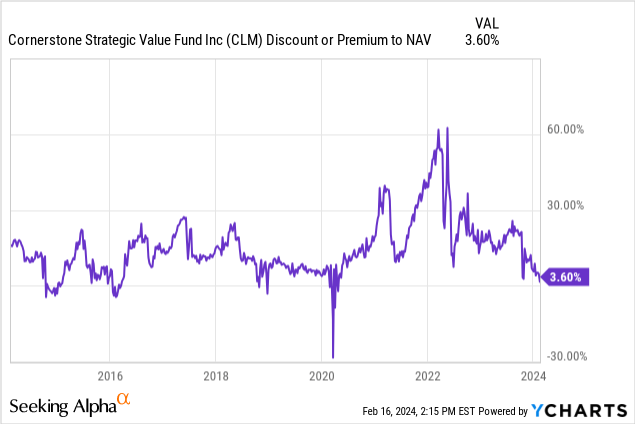

1. The fund has usually instances traditionally traded at very massive premiums to NAV:

Throughout the zero charges surroundings that characterised 2020/2021, the fund moved to an unreal 60% premium to web asset worth. The excellent news is that the low cost to NAV has normalized to a low stage of solely 3.6% premium to NAV. We anticipate the fund to commerce on this vary, absent a big risk-off occasion which might push the CEF into low cost territory.

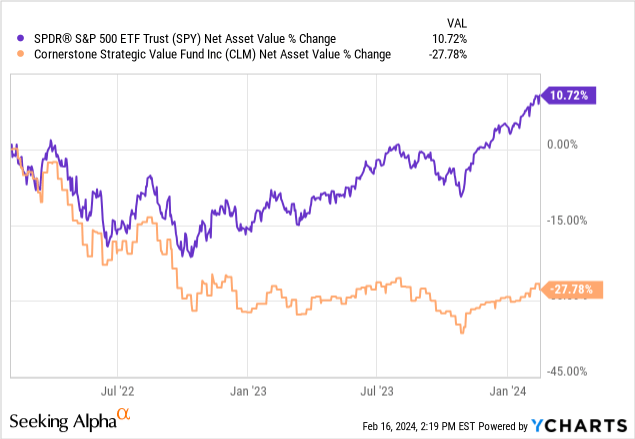

2. CLM will carry out so long as the S&P 500 performs. If the general fairness market sells-off, the CEF may even lose worth:

We will see the shut correlation in CLM’s NAV efficiency with the S&P 500 throughout sell-offs. We’re taking a look at CLM’s NAV right here in an effort to get rid of any actions within the premium to NAV from the equation.

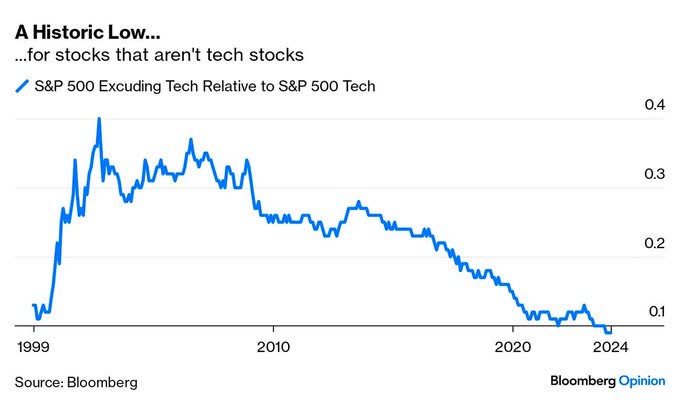

We imagine the general market is overbought right here, pushed by the AI names and tech mega-caps:

S&P 500 Tech vs Non-Tech (Bloomberg)

Whereas AI associated names and tech mega-caps have seen their P/E ranges explode, shares that aren’t tech shares are at a low relative to the S&P 500 Tech names, and in reality have cheap P/E ratios.

Whereas some individuals are arguing for a rotation from tech to different sectors, we really feel the general euphoric really feel shall be cured by a risk-off occasion, somewhat than witness an ideal comfortable touchdown.

CLM will sell-off with the market when that occurs, and it would even transfer to a reduction to web asset worth on the again of such an occasion.

Conclusion

CLM is an fairness CEF which has been available in the market for over 30 years. The automobile usually mirrors the S&P 500 complete returns over lengthy durations of time, however has lagged as of late, being underweight the AI names which have moved the market greater previously yr. This positioning has seen the fund’s premium to NAV collapse to extra palatable ranges, the automobile being now virtually flat to NAV from a premium of virtually +60%.

CLM pays a 18% managed distribution, however may be very straight ahead about the truth that fund belongings will lower if the underlying equities don’t produce these sorts of annual returns. The S&P 500 in actual fact would not, with annualized figures over a decade coming in at 12.5%. The outcome has been an ever reducing NAV for the fund, which buyers ought to anticipate to proceed.

Whereas the premium to NAV threat issue is now inside extra regular parameters, the fund remains to be topic to general fairness market strikes, and we really feel we’ll witness a big risk-off transfer this yr. In our view, CLM’s threat is skewed to the draw back within the subsequent 12 months, pushed by the fund’s fairness threat issue. The fund’s 18% yield is a mirage, and a long run investor ought to anticipate a real yield nearer to 12.5% if the CEF is purchased near market bottoms somewhat than interim tops. We might discover this title interesting -15% decrease from right here, and wish to see the title transfer to a reduction to NAV first on the again of an general market risk-off occasion.