Bloomberg/Bloomberg through Getty Photos

In mid-December, I warned Roku, Inc. (NASDAQ:ROKU) traders that ROKU’s FOMO surge wasn’t sustainable as it surged into well-overvalued zones. In consequence, an extra valuation re-rating would have required the corporate to ship vital outperformance to justify such a transfer. With ROKU down practically 30% from my earlier Promote article because it underperformed the S&P 500 (SPX) (SPY) considerably, I take into account the thesis to have performed out accordingly.

So what occurred that led to ROKU traders deciding to bail out of the inventory post-earnings, however a decent fourth-quarter earnings release by Roku? Furthermore, Roku’s forward guidance also suggests a positive outlook. Traders who paid close attention to Roku’s earnings call would have gleaned administration’s much less sanguine commentary over the expansion momentum of its media and leisure or M&E vertical. Roku’s core M&E section is pivotal to the well being and profitability of its platform enterprise. In consequence, I imagine it is justified that any less-than-perfect commentary to justify ROKU’s costly valuation ought to result in a extra defensive “sell first, ask questions later” posture. Traders sitting on substantial positive factors from ROKU’s November 2023 lows ($55 degree) seemingly took revenue to guard their positive factors.

Accordingly, administration appeared optimistic throughout its convention name, suggesting that Roku has diversified its enterprise mannequin past M&E spending. Nonetheless, the market’s damaging response suggests traders aren’t satisfied until Roku may present extra readability over the slowdown and impression on full-year profitability. Roku has dedicated to balancing development and profitability in 2024, paying extra consideration to its free money stream enchancment. Regardless of that, the dearth of clear development steering on full-year adjusted EBITDA seemingly apprehensive traders.

Accordingly, Roku telegraphed that it has aimed to submit “further improvements in adjusted EBITDA for full-year 2024.” As well as, the corporate highlighted that YoY comps could possibly be tougher, because it anticipates “challenges in the M&E environment for the rest of the year.”

I imagine that seemingly caught analysts and the market unexpectedly, as some analysts peppered administration with questions regarding M&E spend. In consequence, I feel it suggests additional development in adjusted EBITDA for FY24 may show to be far more difficult than anticipated, suggesting 2024 may probably be a flat yr at finest.

However the cautious commentary indicated by administration, Roku’s basic drivers have improved over the previous yr. Administration offered salient updates over key metrics, indicating that Roku has continued to scale remarkably nicely. Accordingly, the corporate delivered an FY23 adjusted EBITDA of $4.3M. Whereas it is nothing spectacular, it underscores the market’s confidence that the worst in its enterprise efficiency has seemingly bottomed out in FY22.

Furthermore, crucial underlying metrics point out that Roku’s market management ought to stay strong. The corporate posted energetic accounts of 80M, up from 70M a yr in the past. As well as, engagement has additionally improved, as Roku streamed 4.1 hours per energetic account day by day in This autumn, up from 3.8 hours within the earlier yr. As well as, the corporate has additionally retained its place because the “#1 TV streaming platform by hours streamed in both the U.S. and Mexico.” Consequently, I assessed that Roku’s platform-agnostic strategy towards ad-supported streaming has demonstrated its worth proposition with customers, bolstering its enchantment. However the more and more aggressive streaming panorama, Roku appears well-poised to learn from the continued shift away from Linear TV as advertisers additional alter their budgets over time.

With the numerous post-earnings battering, ROKU has dropped right into a extra enticing zone, though it is nonetheless priced at a premium. Looking for Alpha Quant assigned ROKU with a “D” valuation grade. Nonetheless, ROKU bulls may argue that its best-in-class “A+” development grade helps justify its development premium. In consequence, I view ROKU with the lens of a development inventory. With that in thoughts, traders involved with its tepid outlook and damaging commentary on M&E spending should stay cautious.

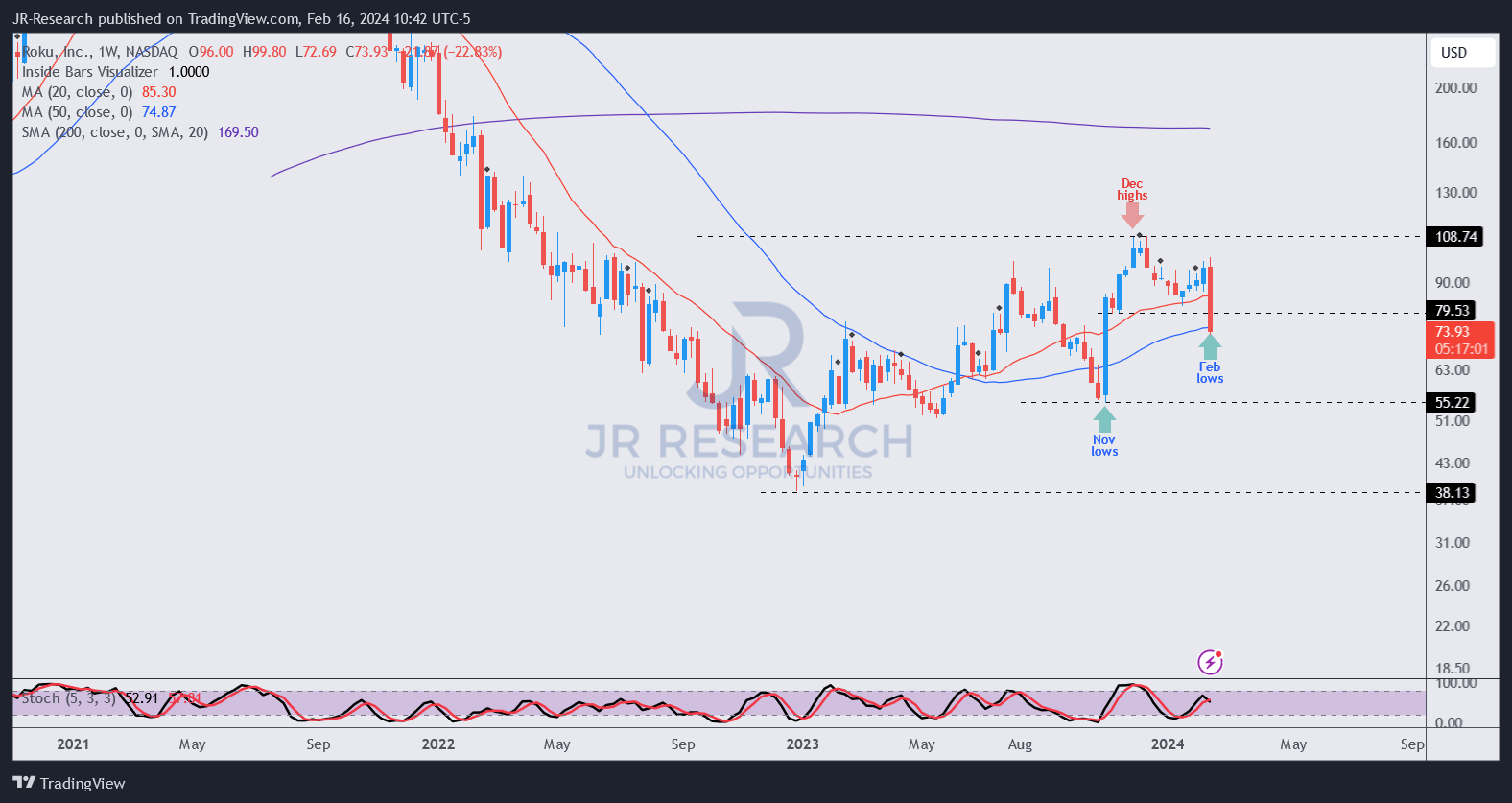

ROKU worth chart (weekly, medium-term) (TradingView)

With the promoting strain ROKU taking out the $80 help zone, the draw back volatility is anticipated because the market shakes out dip-buyers who anticipated that degree to be defended decisively.

Consequently, traders preferring a validated bullish reversal sign ought to look forward to the extent to be retaken by dip-buyers seeking to capitalize on the post-earnings decline.

Nonetheless, I am of the view that ROKU’s steep plunge ought to nonetheless be undergirded by strong shopping for sentiments, because it stays in a medium-term uptrend. In different phrases, bullish shopping for sentiments have already returned to the inventory since its lows in late 2022. In consequence, shopping for vital dips on an uptrend inventory like ROKU is a viable technique.

Due to this fact, I view the chance/reward over ROKU as more and more extra constructive, attributed to the post-earnings battering.

Score: Improve to Purchase.

Necessary observe: Traders are reminded to do their due diligence and never depend on the knowledge offered as monetary recommendation. Please all the time apply impartial considering and observe that the ranking is just not meant to time a particular entry/exit on the level of writing until in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a crucial hole in our view? Noticed one thing vital that we did not? Agree or disagree? Remark under with the intention of serving to everybody in the neighborhood to be taught higher!