NurPhoto/NurPhoto through Getty Photos![]()

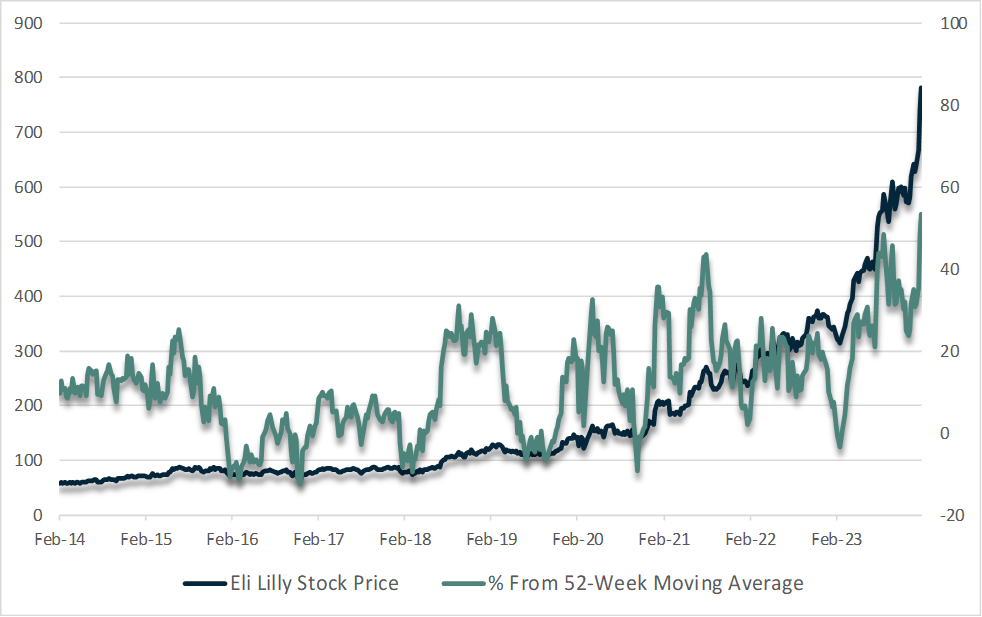

Eli Lilly (NYSE:NYSE:LLY) has seen a parabolic rise that has accelerated in a basic bubble formation. After an entire frenzy in name possibility shopping for and retail curiosity within the inventory, traders are betting closely in favour of additional good points, regardless of it buying and selling at 83x earnings, greater than 4x the pharmaceutical business common. Even below optimistic income development assumptions, LLY now appears considerably overvalued, and a reversal of speculative exercise might trigger a big correction.

Bloomberg

Retail Shopping for And Choices Frenzy Factors To Peak Euphoria

Eli Lilly’s inventory seems to have been the recipient of indiscriminate shopping for by retail traders, choices merchants, and quick sellers. On the retail entrance, the surge in media protection of the weight problems drug market in addition to its newfound standing as a Magnificent 7 inventory, which it achieved when it overtook Tesla in January, have pushed an increase in retail interest within the inventory.

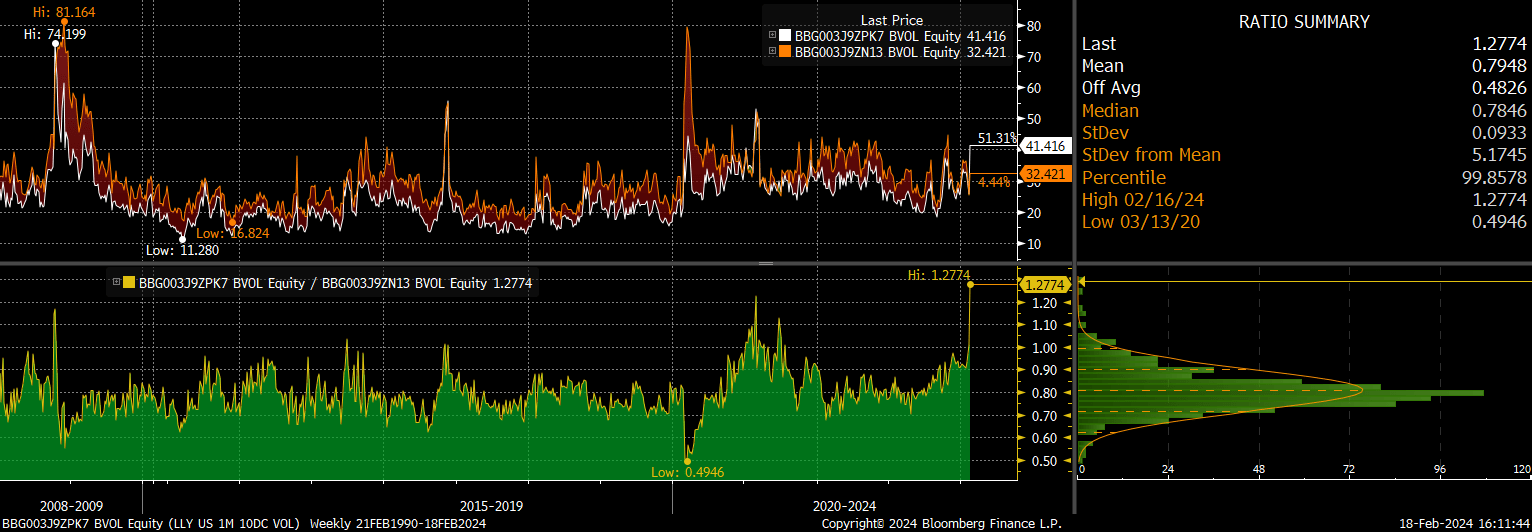

The inventory has additionally been the beneficiary of the proliferation name possibility curiosity as I highlighted here. The leveraged nature of choices signifies that notional shopping for energy can develop into enormous, pushing up costs. The frenzy in name possibility demand is highlighted within the chart beneath, which exhibits the implied volatility ranges for put and name choices over a 1 month horizon. Calls now commerce considerably greater than places which is uncommon certainly and displays excessive greed and a scarcity of worry.

1 Month Implied Volatility. Name/Put Ratio (Bloomberg)

LLY has additionally benefitted from short covering as bearish traders have been pressured to purchase the inventory, typically because of margin calls quite than a basic conviction, and quick curiosity is now at multi yr low as a share of float. As Bob Farrell’s 4th rule to recollect states – parabolic advances normally go additional than you assume, however they don’t right by going sideways. I’d not be shocked to see LLY proceed its advance within the quick time period as talk of a $1trn market cap intensifies. Nonetheless, I’d be very shocked if any additional good points should not given again as the present degree of euphoria burns out. The value-incentive shopping for that has occurred over the previous few months might simply shift to indiscriminate promoting.

Overvalued Even Underneath Optimistic Development Projections

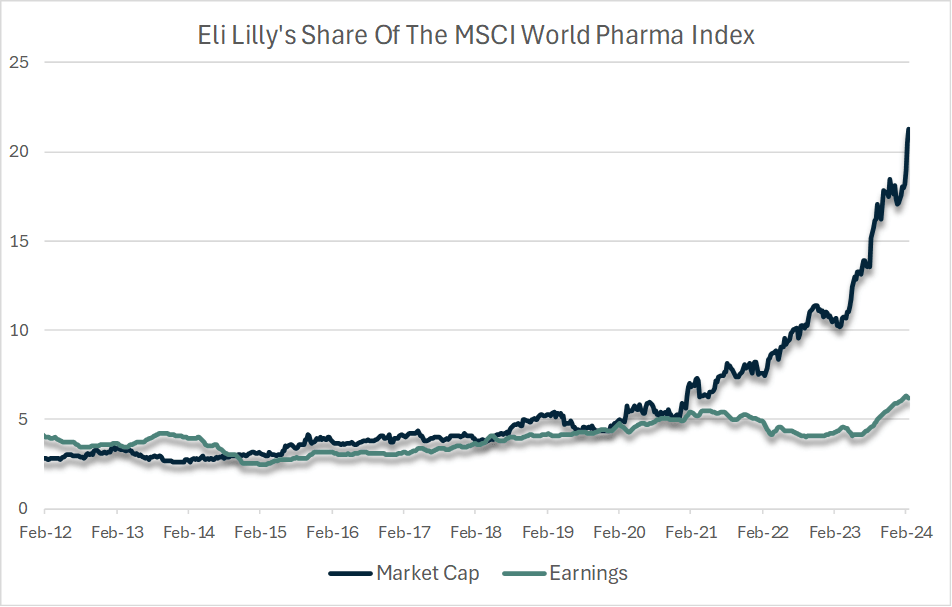

Eli Lilly’s parabolic advance has outstripped the spectacular rise in gross sales and earnings over the previous yr, leading to it buying and selling at a PE ratio of 83x. That is excessive for any inventory, however pharmaceutical shares have tended to commerce at below-market valuations over the previous decade, which means that LLY presently trades at 4.2x the common of the remainder of the sector. As proven beneath, Eli Lilly’s market cap has risen to 21% of your entire MSCI World Pharmaceutical Index, regardless of its earnings representing simply 6%.

Bloomberg

Final week Morgan Stanley upped its worth goal to $950, which might make the corporate value $900bn. It now expects revenues to develop to $96bn by 2030, pushed largely by the weight problems drug market, which Goldman Sachs just lately argued might reach $100bn by then. Nonetheless, even these huge numbers don’t justify LLY’s present worth. If we assume that the corporate can keep its business beating web margins of 25%, revenues of $96bn in 2030 would convey the inventory’s PE ratio right down to 31x assuming its worth stays at its present $742bn.

Whereas this will seem to justify additional good points, two issues are value preserving in thoughts. Firstly, a 31x PE ratio for an organization with $96bn in gross sales can be a really excessive a number of. Development is a slowing operate of market dimension and as firms transfer from mid dimension gamers to market leaders the scope for additional development diminished. There’s a pretty sturdy inverse relationship between gross sales worth and the worth to gross sales ratio among the many largest US firms as traders have a tendency to cost in slower development and decrease web margins for bigger firms.

Secondly, traders have traditionally required a excessive charge of return on development shares and so it appears truthful to say that almost all traders holding LLY immediately are anticipating a minimum of 10% returns, which is the common long-term return on US shares. Which means if the inventory had been to be worth pretty assuming a ten% low cost charge over 7 years it must be valued at simply $462 immediately, 38% beneath present ranges.

To ensure that LLY to be valued according to its business friends it will must develop earnings by 4.2x relative to the MSCI World Pharmaceutical Index, which might justify is share of market cap. Whereas LLY has enormous potential within the weight problems and diabetes markets, it appears extremely unlikely that its earnings will attain 21% of your entire business. Whereas Eli Lilly has various promising merchandise within the pipeline, its new GLP-1 weight reduction drug Zepbound has pushed the majority of the surge in income development expectations. Nonetheless, this optimism surrounding one drug leaves the inventory extremely inclined to competitors on this area. Novo Nordisk (NVO) is its most important competitor however there may be additionally a race to develop an weight problems drug in capsule type. Regardless of latest setback, Pfizer (PFE), backed by web property of virtually 10x that of LLY, is anticipated by some to launch a product by 2026.

Abstract

Eli Lilly’s inventory worth has been pushed up worth insensitive consumers together with retail traders, choices merchants, and quick protecting. Whereas parabolic strikes can go on for longer than anticipated, we’re already seeing file ranges of greed relative to worry in choices market. At over 4 occasions costlier than its business friends, even fast gross sales and earnings development is unlikely to justify present valuations.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.