LeoPatrizi/E+ by way of Getty Pictures

New York Group Bancorp (NYSE:NYCB) had a devastating week. The corporate’s share value was pushed down greater than 50%, additional than it dropped throughout the regional banking scare of March 2023. The set off was an announcement that the firm was chopping its dividend and shoring up its monetary place after losses on business loans.

That is regardless of the corporate buying Signature Financial institution final yr, one of many prizes of the downturn, and going above a $100 billion in property threshold.

2023 Efficiency

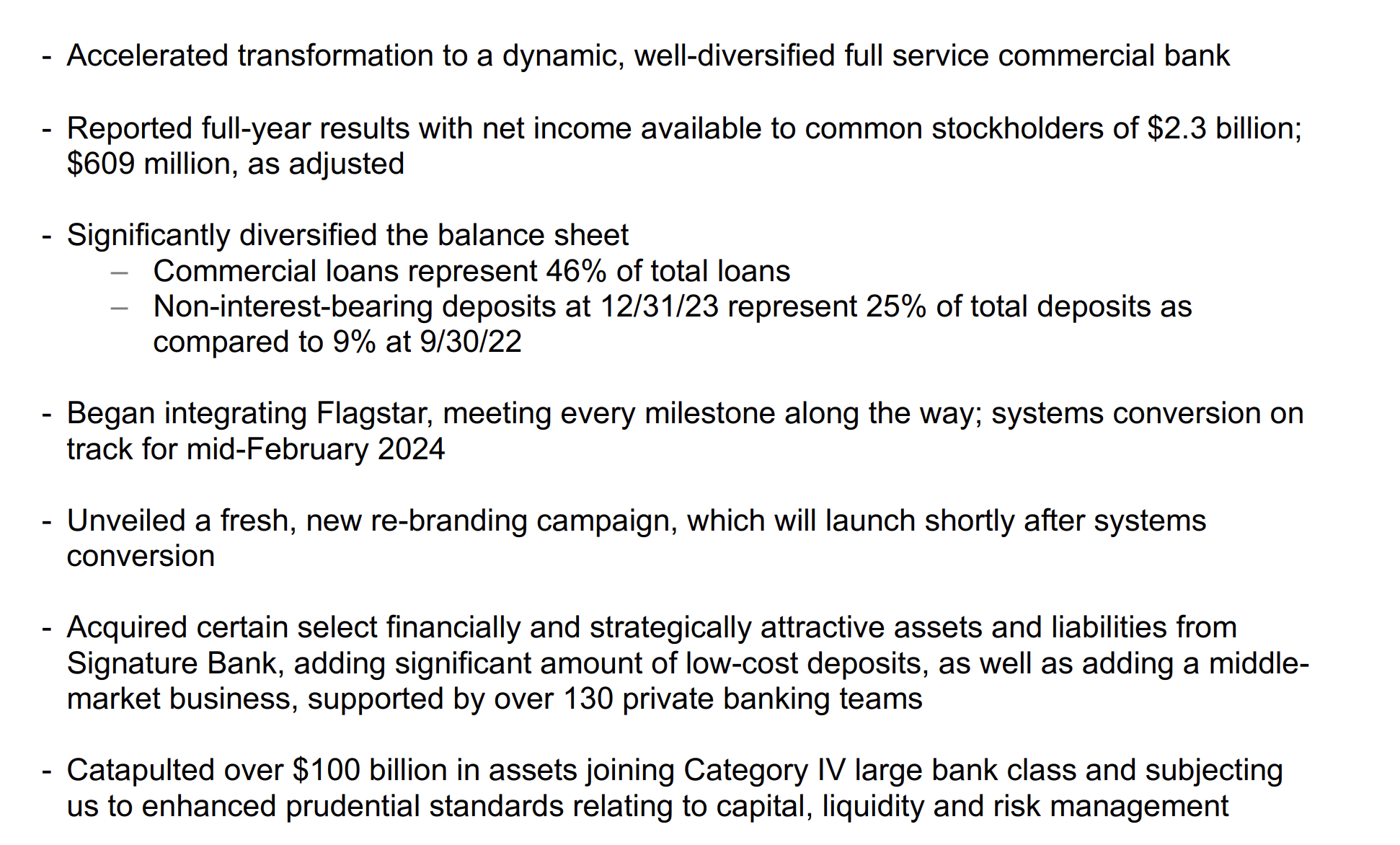

The corporate had a transformative 2023 that has finally put it in its present predicament.

New York Group Financial institution Investor Presentation

The corporate acquired each Flagstar Financial institution, an acquisition that closed at year-end 2022, a $2.6 billion acquisition, after which acquired Signature Financial institution property from the FDIC when it went bankrupt throughout the early 2023 banking rout. The corporate had sturdy internet revenue for the yr versus a weak market cap, after the corporate’s current weak point.

The corporate has diversified its steadiness sheet, with 46% of its complete loans as business loans. Non-interest-bearing deposits nonetheless symbolize 25% of deposits. The corporate has handed $100 billion of property, a threshold that led to its current predicament, as the corporate has needed to put aside money to regulate.

NYCB Place Enhancements

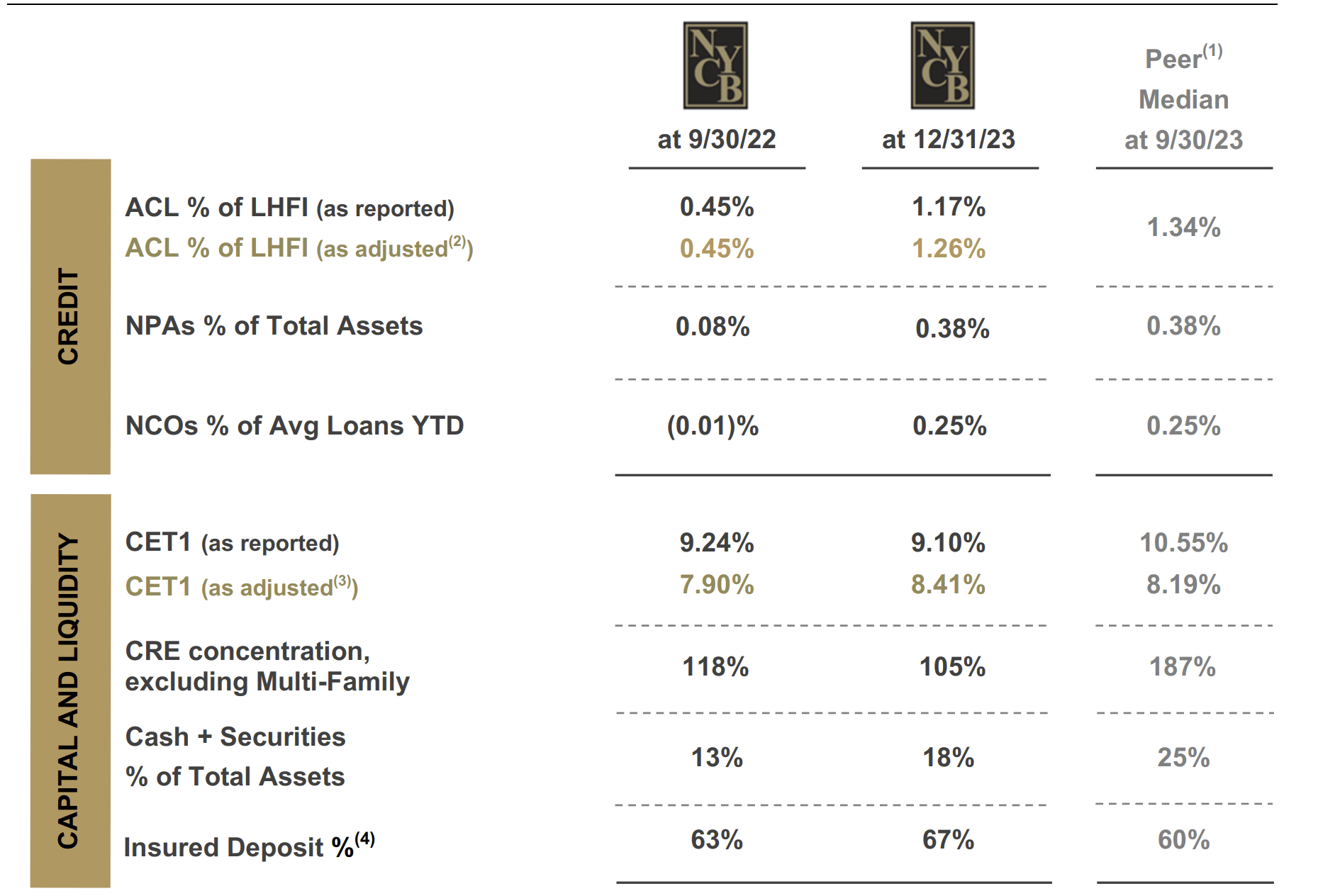

The corporate has labored to enhance its place, regardless of having some problematic loans.

New York Group Financial institution Investor Presentation

The corporate’s ACL (allowance for credit score losses) has roughly tripled. That is a lot nearer to the peer median and permits the corporate to guard itself within the occasion of one other downturn. The corporate’s NPA and NCO did enhance, however once more they’re in step with the corporate’s peer median group at an inexpensive stage.

It was anticipated that the corporate’s prices would transfer in step with its peer group, so sooner or later, the corporate must chunk the bullet. The corporate’s CET1 ratio stays low. Nonetheless, insured deposits, money + securities, and business actual property focus have all improved dramatically.

We would wish to see the corporate hold bettering this, however it’s made huge strides for a serious yr.

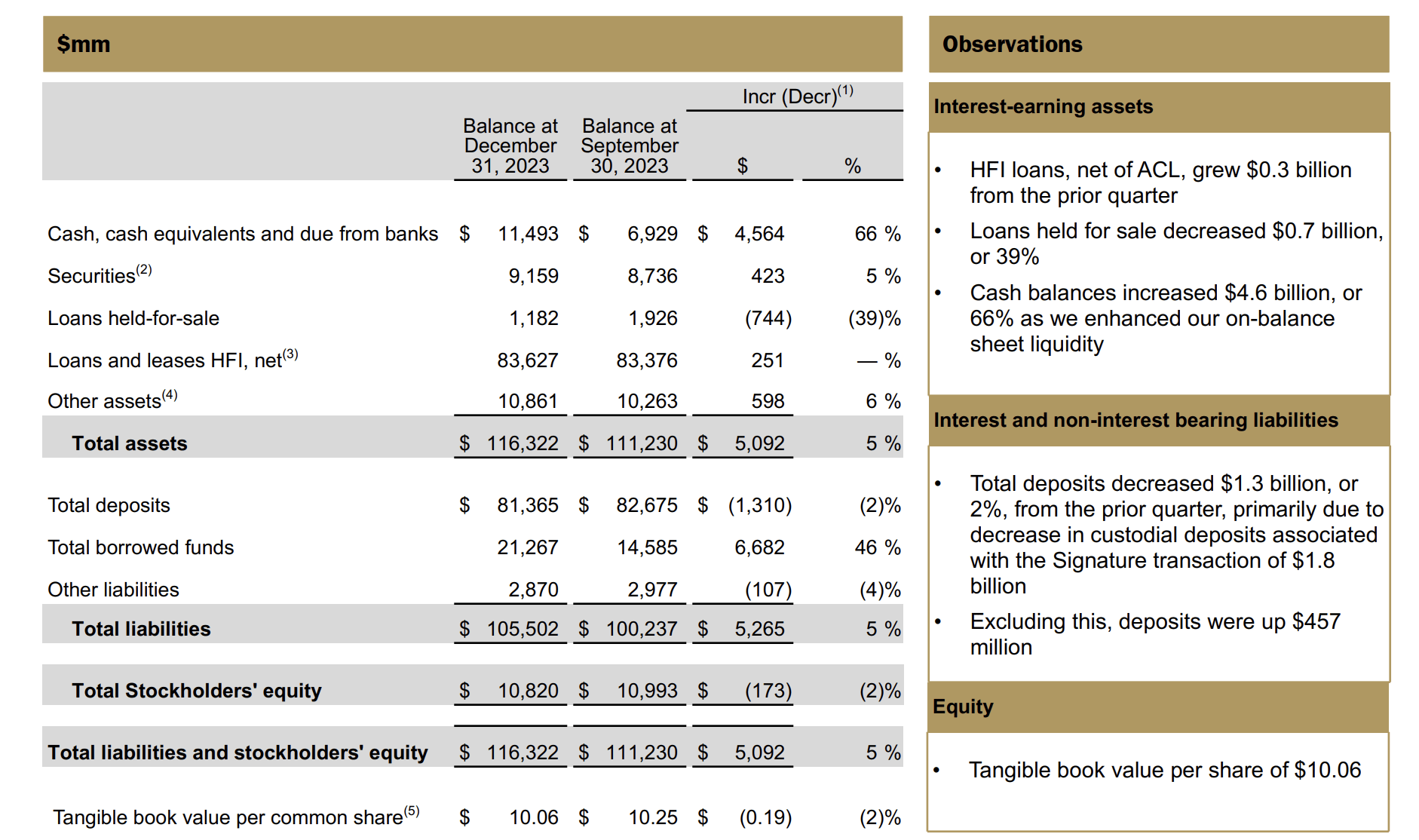

NYCB Monetary Highlights

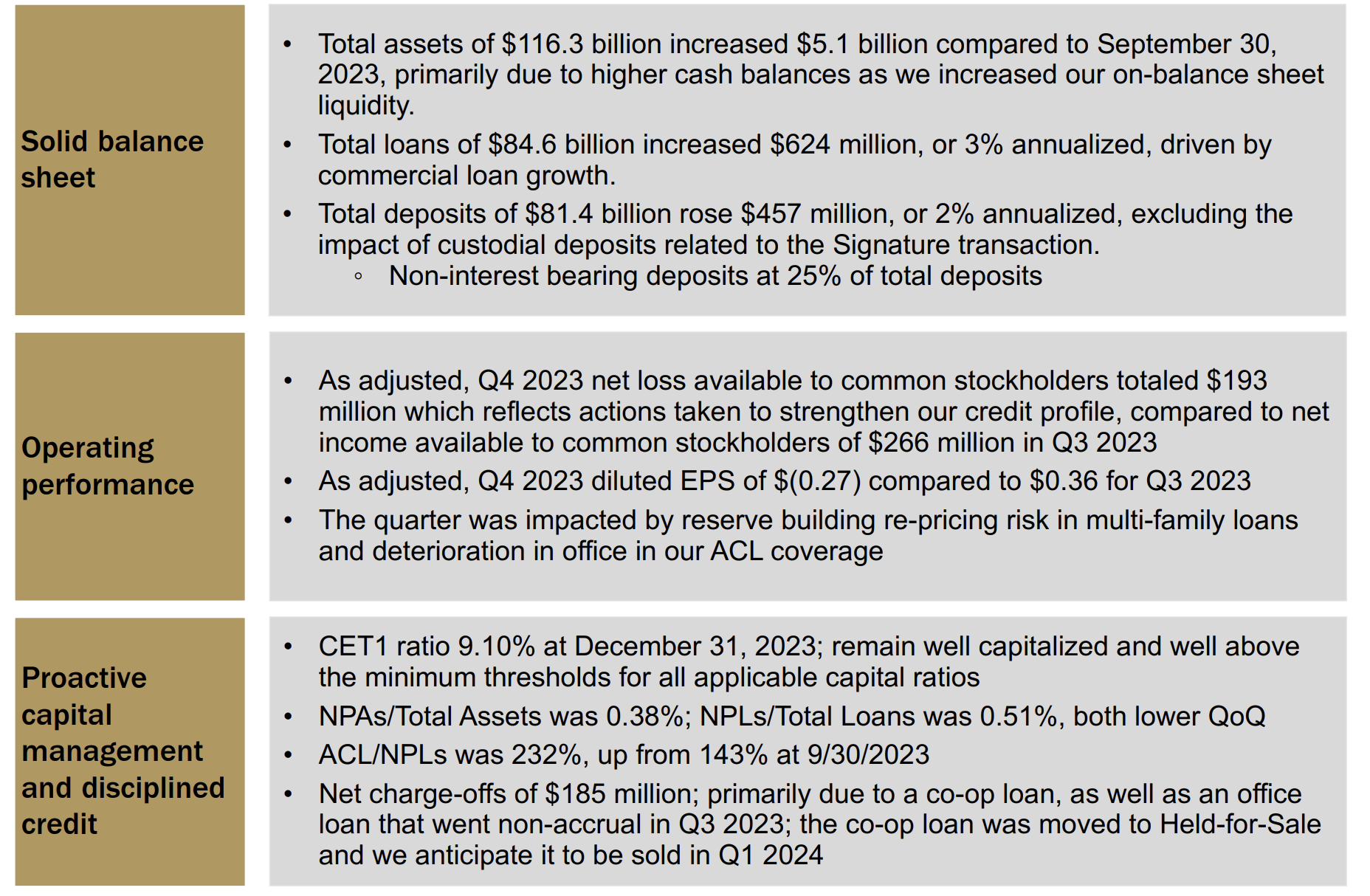

Financially, the corporate stays extremely properly positioned versus its market capitalization.

New York Group Financial institution Investor Presentation

The corporate’s property are $116.3 billion, transferring it over that $100 billion threshold, an extremely sturdy stage. The corporate’s property elevated $5.1 billion QoQ as the corporate labored to carry out its liquidity. The corporate’s complete loans are only a hair underneath $85 billion, and complete deposits are $81.4 billion, not counting Signature deposits. 25% non-interest deposits are useful.

The corporate’s internet loss dropped to $193 million within the quarter, an enormous decline as the corporate accounted for a deteriorating business mortgage profile. Hopefully, it is a one-time main adjustment for the corporate, because it continues to regulate for 2 dangerous loans that went non accrual. We count on these $185 million of charge-offs to be momentary.

NYCB Monetary Efficiency

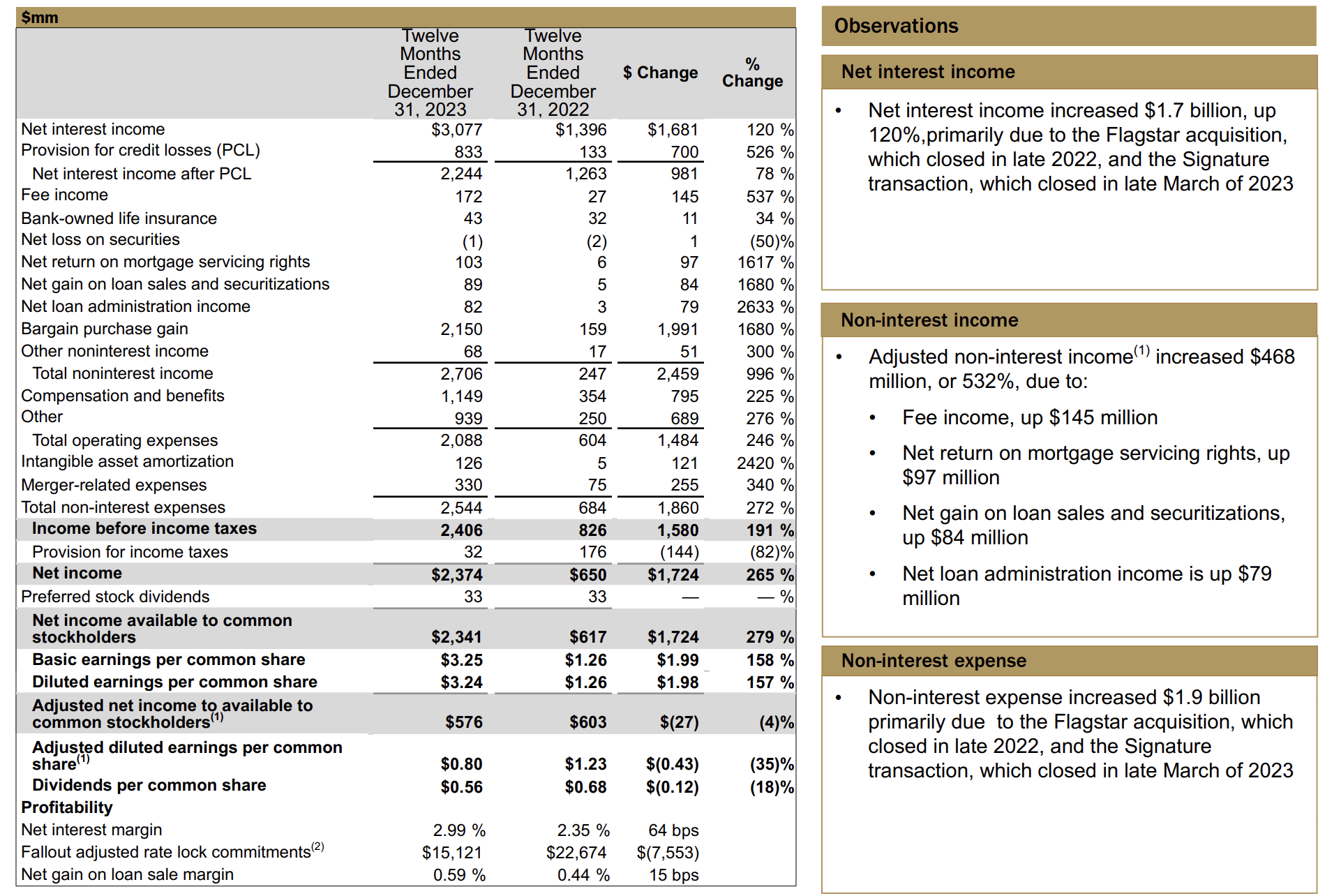

The corporate’s detailed monetary efficiency is seen beneath.

New York Group Financial institution Investor Presentation

What’s most vital to a financial institution is two-fold. The primary is internet curiosity margin. A financial institution’s income and income are based mostly on taking in deposits and loaning these deposits out at the next charge. The corporate had $2.37 billion in internet revenue, a unbelievable revenue charge versus the corporate’s market capitalization. The corporate’s profitability of virtually 3% stays extremely sturdy.

The corporate had some non-interest bills, however these had been one-time issues on account of closing acquisitions.

New York Group Financial institution Investor Presentation

The following vital a part of a financial institution is what’s the money loaned out to. Should you mortgage out and lose all the cash, not paying buyer deposits again causes banks to go bankrupt. The corporate has greater than $10 billion in stockholder fairness, which means that its ebook worth is ~2x. That is an extremely sturdy ebook worth and reveals how a lot the corporate’s share value has dropped.

This is the place the corporate’s potential weak point is. These business loans of $185 million. The corporate’s business actual property and ADC mortgage complete is $13.4 billion. Greater than 40% of it’s in NY. Loads is homebuilder and retail, however workplace nonetheless makes up 25% of the portfolio. Greater than 50% of that workplace portfolio is in Manhattan ($1.8 billion).

The corporate does have one profit that the mortgage roll-off per yr is minor, which decreases the prospect that substantial non-performing rolls arrive unexpectedly. Solely $200-300 million in loans are contracted per yr from now till 2030. That could possibly be a rollover that is dealt with with minimal bankruptcies on account of increased rates of interest.

Liquidity Disaster

In contrast to Silicon Valley Financial institution, which had 94% of its assets as uninsured, New York Group Financial institution has dramatically decrease uninsured property. That is backed by virtually $19 billion in reciprocal deposit capacity. First Republic Financial institution had virtually 70% of its property as uninsured, and Signature Financial institution had roughly 90% in uninsured deposits.

New York Group Financial institution has had $850k in insider acquisitions. The corporate can financially afford it, and we perceive the business portfolio danger. The one query is whether or not there is a run on the financial institution, which we see as not possible given the sturdy insured deposits, ideally insured prospects haven’t any cause to withdraw money.

To this point, the corporate appears to persevering, however we want extra particulars from the corporate.

Thesis Threat

The biggest danger to our thesis is the chapter of the corporate. It is a huge deal. Even when the corporate can financially deal with the downturn, the danger of a run on the financial institution can’t be overstated. That run might push your funding to $0. Nonetheless, we see that probability as low, given the corporate’s profitability and excessive insured deposits.

Conclusion

New York Group Financial institution had extremely weak earnings because it turned one of many preliminary victims of issues over business loans. You want numerous revenue to make up for some main losses in banking, given low-interest charges. Nonetheless, regardless of that, the corporate remains to be very worthwhile general, and it is taken benefit of some main acquisitions.

We count on there to not be a run on the financial institution given the excessive % of insured deposits. Assuming that is the case, the corporate’s income can stay excessive, driving substantial long-term shareholder returns and a restoration within the firm’s valuation. Tell us your ideas within the feedback beneath.