shih-wei/E+ by way of Getty Photos

Lam Analysis Company (NASDAQ:LRCX) revealed robust monetary efficiency in This fall 2023 which exhibits vital enchancment in quarterly income. The yearly income development has additionally proven robust enchancment over the previous years. Regardless of the rise in working bills, the robust progress in web revenue signifies the corporate’s potential to revenue from rising prices. This text presents the monetary and technical evaluation of Lam Analysis and offers funding alternatives for long-term buyers. Because the worth is presently buying and selling at overbought ranges, the subsequent dip in worth is taken into account a robust shopping for alternative for long-term buyers.

Firm Overview

Lam Analysis has been the main entity within the semiconductor business and performs a pivotal function in driving the evolution of microelectronics. The corporate has developed essential partnerships with world’s main semiconductor producers over the previous 4 many years, which permits the manufacturing of smaller and environment friendly digital gadgets to fulfill the rising demand for know-how. The corporate is concerned in design, manufacturing and servicing of semiconductor processing tools and continues to evolve in analysis and growth, international provide chain administration, and atmosphere and well being and security initiatives. The core enterprise operations of Lam Analysis are etch methods, deposition methods and cleansing processes associated to semiconductor manufacturing tools. The corporate earnings from the sale of those tools methods to semiconductor producers and likewise earnings from the after gross sales companies together with upkeep, restore, upgrades and sale of spare elements to additional improve the income streams. The corporate has proven robust monetary efficiency over time which highlights dedication to innovation, steady growth and technological developments.

Monetary Efficiency

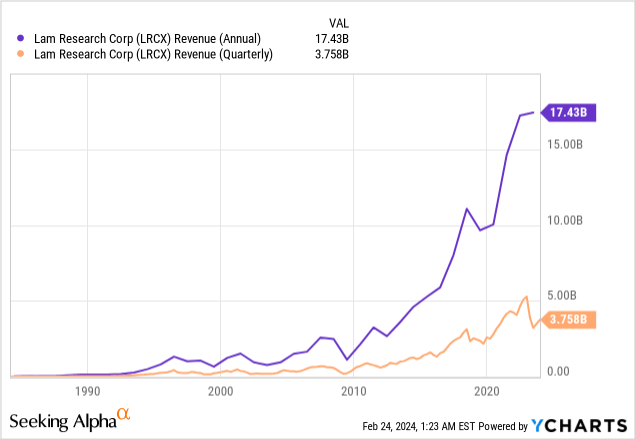

The latest earnings report for Lam Analysis exhibits robust monetary efficiency, which highlights the corporate’s main place within the semiconductor business. The quarterly income for This fall 2023 elevated by 7.9% to $3.758 billion as in comparison with the $3.48 billion in This fall 2022. The income acquired yr over yr drops as in comparison with the same period last year, however the income traits present robust progress from 2010 as proven within the chart under. Furthermore, the yearly income for 2023 was $17.43 billion and exhibits a robust constructive momentum. The continued constructive trajectory in yearly income presents the corporate’s monetary power and market presence over the long run.

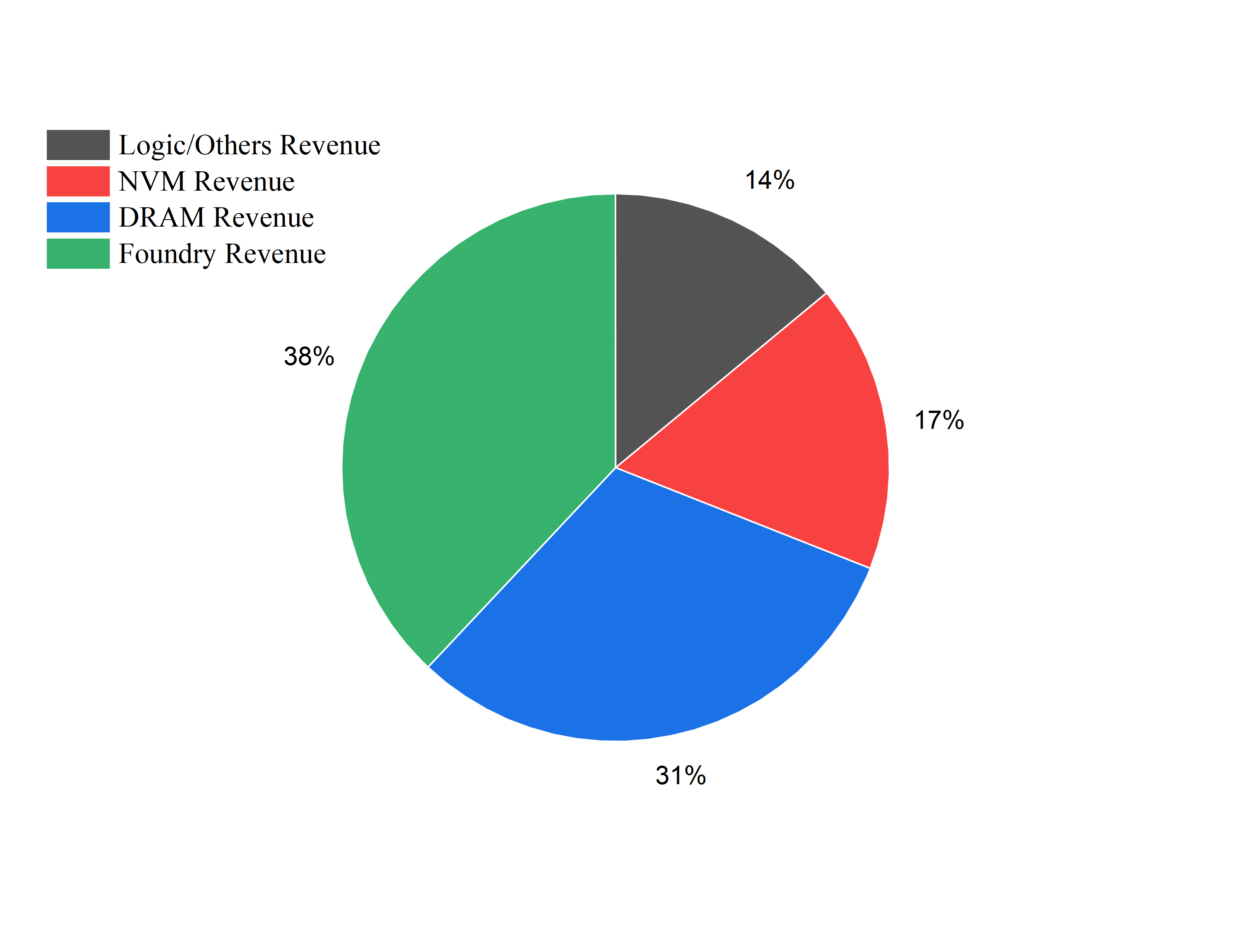

The corporate’s income is distributed between system revenues and buyer support-related revenues. The system income occupies 61.2% of the general income for This fall 2023 with $2.299 billion. The chart under presents the breakdown of system revenue, which exhibits that the corporate is producing the most important portion of revenues from the reminiscence, which consists of non-volatile reminiscence (NVM) and dynamic random entry reminiscence (DRAM) and occupies 48% of revenues for This fall. The memory market size is anticipated to develop considerably, which is able to doubtless contribute positively to the corporate’s monetary efficiency within the coming years.

System Income Segments, chart by Origin Professional (Lam Analysis)

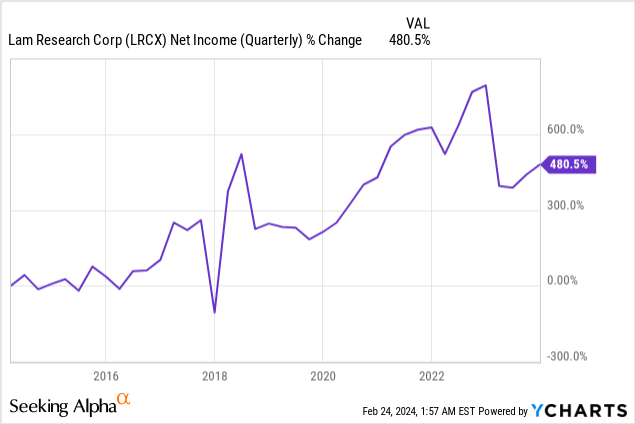

The total operating expenses elevated to $700.24 million in This fall 2023 as in comparison with $631.67 million in Q3 2023. The full value of products offered additionally elevated to $2.001 billion. Regardless of the rise in bills, the web revenue elevated to $954.27 million in This fall 2023 as in comparison with $887.4 in Q3 2023. The chart under exhibits a 480.5% improve in web revenue through the previous decade. The robust progress in web revenue highlights the corporate’s skill to extend profitability by managing bills, even the rising prices.

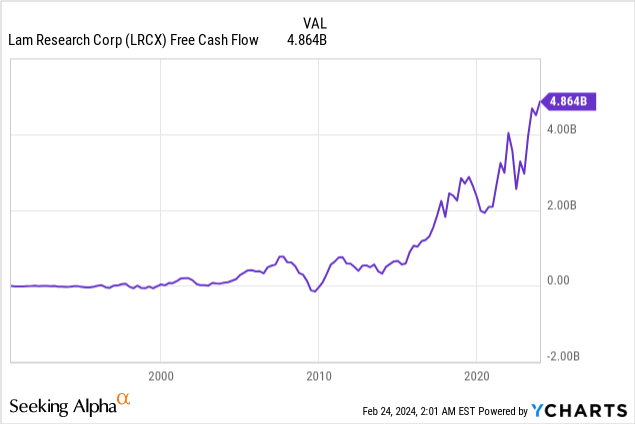

The corporate’s progress can also be noticed within the stability sheet and money move outcomes, because the cash reserve elevated to $5.6 billion in This fall 2023 from $5.2 billion on the finish of the earlier quarter. This progress in money reserve was because of the spectacular money of $1.454 billion generated from the working actions. The full free money move for Lam Analysis for the previous trailing twelve months led to December 2023 is $4.864 billion, as proven within the chart under. The robust free money move signifies wholesome operations and the corporate’s functionality to finance enlargement, pay dividends and cut back debt with out exterior help. This robust liquidity positions the corporate for future investments and progress alternatives.

Strategic Investments and Progress Alternatives

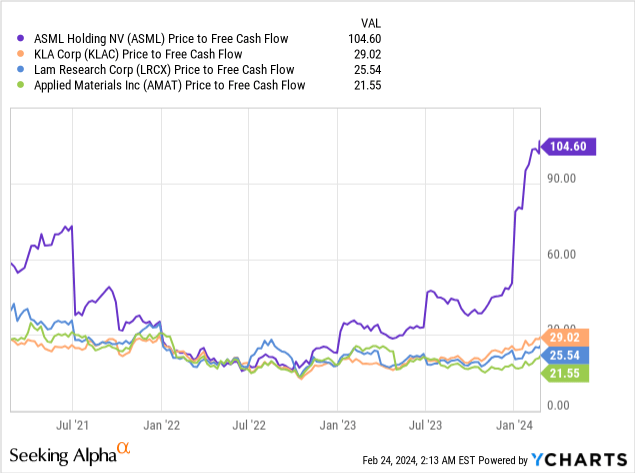

The chart under illustrates the value to free money move ratio for Lam Analysis, ASML Holding N.V. (ASML), Utilized Supplies (AMAT) and KLA Company (KLAC). The ratio for Utilized Supplies and LAM Analysis is lowest, which signifies that these firms are probably undervalued relative to opponents. Lam Analysis has proven robust enchancment in web revenue and free money move, which highlights the operational effectivity. This effectivity won’t be absolutely mirrored within the inventory worth, which makes it seem undervalued relative to its money producing capabilities. Furthermore, the corporate is positioned to capitalize on the surging demand for know-how based mostly on the business’s progress prospects. Due to this fact, the decrease ratio means that the inventory worth is low as in comparison with the quantity of free money move that the corporate is producing, which highlights the potential for additional upside.

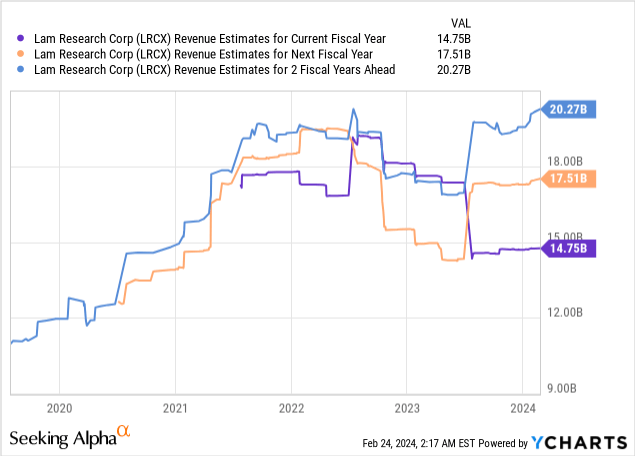

As per the newest earnings report, the President and CEO of LAM Analysis additionally expressed confidence within the monetary efficiency of the corporate when it comes to strategic funding in product differentiation and environment friendly international infrastructure growth. Lam Analysis can also be able to benefiting from the surging demand for AI and HPC within the smartphone, PCs, infrastructure and automotive sectors in 2024. Due to this fact, the corporate expects robust income progress in the long term regardless of the short-term fluctuations. The chart under presents the income estimate for 2024, which is anticipated to be $14.75 billion, which is decrease than the income of $17.43 billion in 2023. Nonetheless, the income for 2025 and 2026 are estimated to be $17.51 billion and $20.27 billion respectively. These robust progress expectations point out that buyers could search for funding within the long-term views.

Furthermore, the $5 billion semiconductor research consortium by President Biden’s administration impacts Lam Analysis and the semiconductor business. This initiative is a part of the Chips & Science Act and indicators robust federal help for the business, which can profit Lam Analysis utilizing the elevated funding in analysis and growth. The deal with home semiconductor business enchancment could result in new alternatives for Lam Analysis by aligning with the federal government’s strategic plans to strengthen the U.S. semiconductor ecosystem.

Total, the newest earnings reviews for Lam Analysis present robust efficiency regardless of the short-term income fluctuations. The robust progress of web revenue and free money move highlights operational effectivity throughout value pressures, which suggests sustainable progress potential. Based mostly on the robust progress expectations of the semiconductor business, the corporate is positioned to capitalize on the robust technological demand.

Lengthy-Time period Technical Image

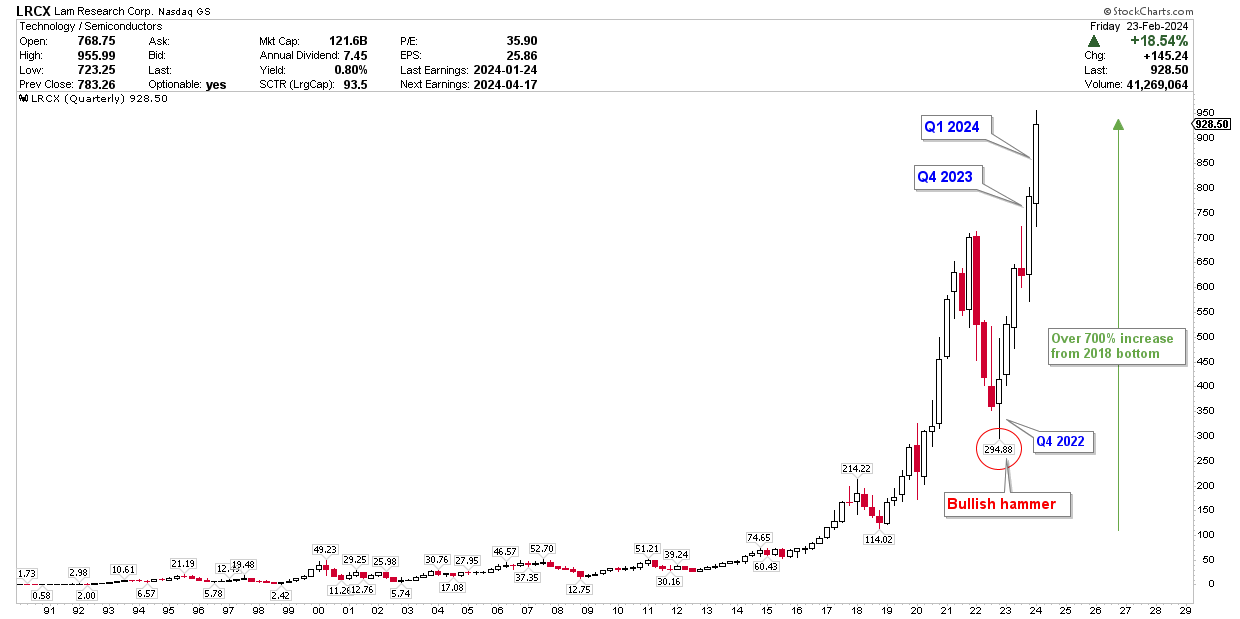

The long-term technical image for Lam Analysis can also be strongly bullish, as seen by the quarterly chart under. The inventory worth has been persistently rising from the 2018 low of $114.02. This robust rally encountered resistance at $712.88 and initiated a robust correction in 2022. This robust worth correction was deep and reversed from the $294.88 key space which is marked by a bullish hammer in This fall 2022 leading to a robust worth surge that broke the earlier document highs. It’s noticed within the chart that the quarterly candles for This fall 2023 and Q1 2024 had been very robust and, which highlights vital worth volatility and signifies a robust worth correction. It’s attention-grabbing to look at that the inventory worth has gained over 700% from the 2018 lows inside a brief interval. This worth acquire signifies robust market demand through the previous years, and subsequently any correction from these areas could also be deeper.

LRCX Quarterly Chart (stockcharts.com)

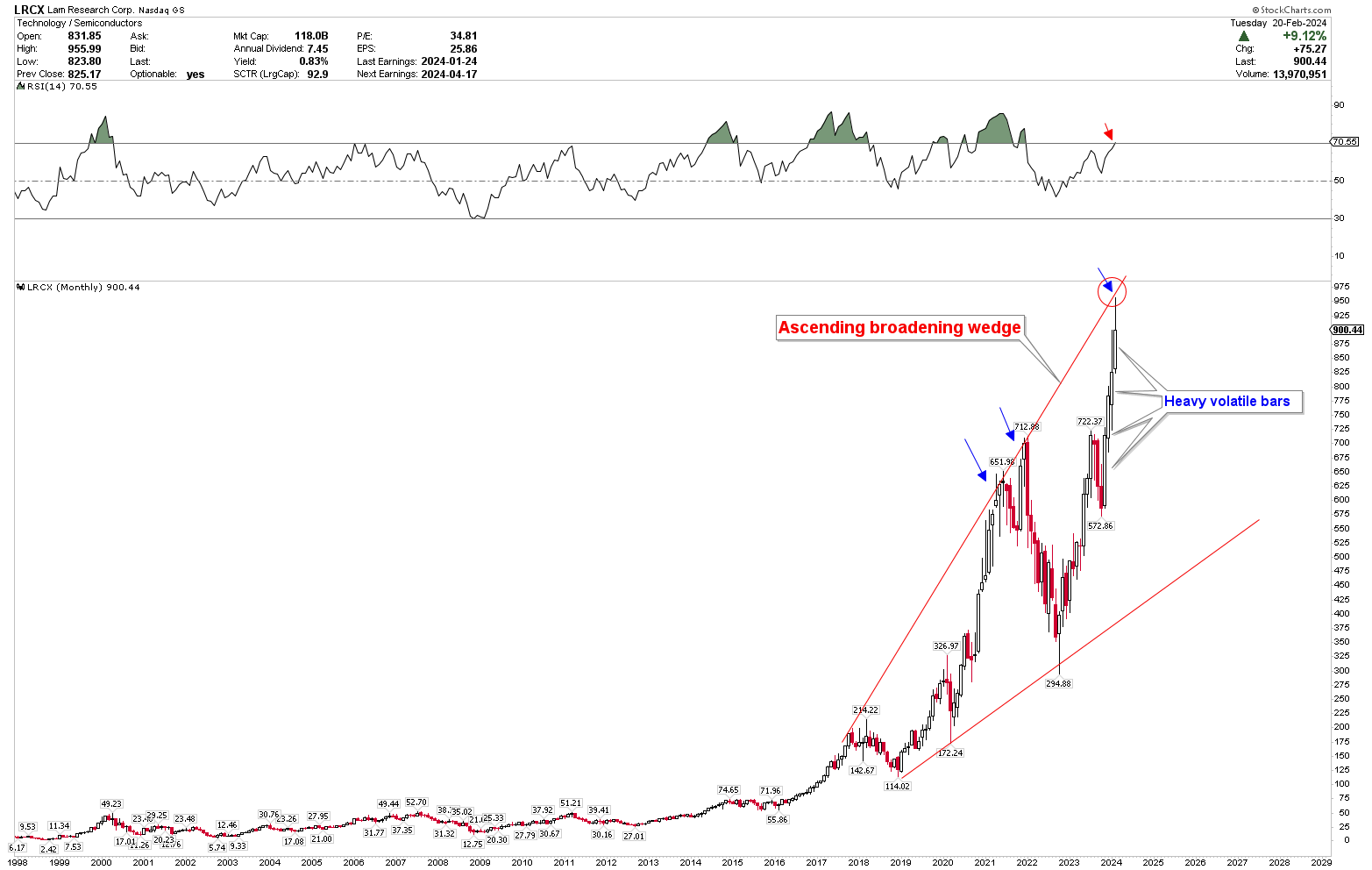

To additional perceive this robust worth improve, the month-to-month chart under exhibits the ascending broadening wedge from the 2018 low of $114.02. The formation of an ascending broadening wedge additional highlights the robust volatility. The robust month-to-month candles for November 2023, December 2023, January 2024 and February 2024 point out that the market could be very near marking a high and able to provoke the robust correction. These month-to-month candles seek advice from the robust risky bars within the month-to-month chart. Furthermore, these risky bars hit the robust resistance of the ascending broadening wedge, which signifies that the market can provoke a robust worth correction. Alternatively, RSI can also be approaching the overbought ranges. The emergence of heavy risky bars and resistance of the ascending broadening wedge signifies that the value could provoke a correction within the chart time period.

LRCX Month-to-month Chart (stockcharts.com)

Key Motion for Buyers

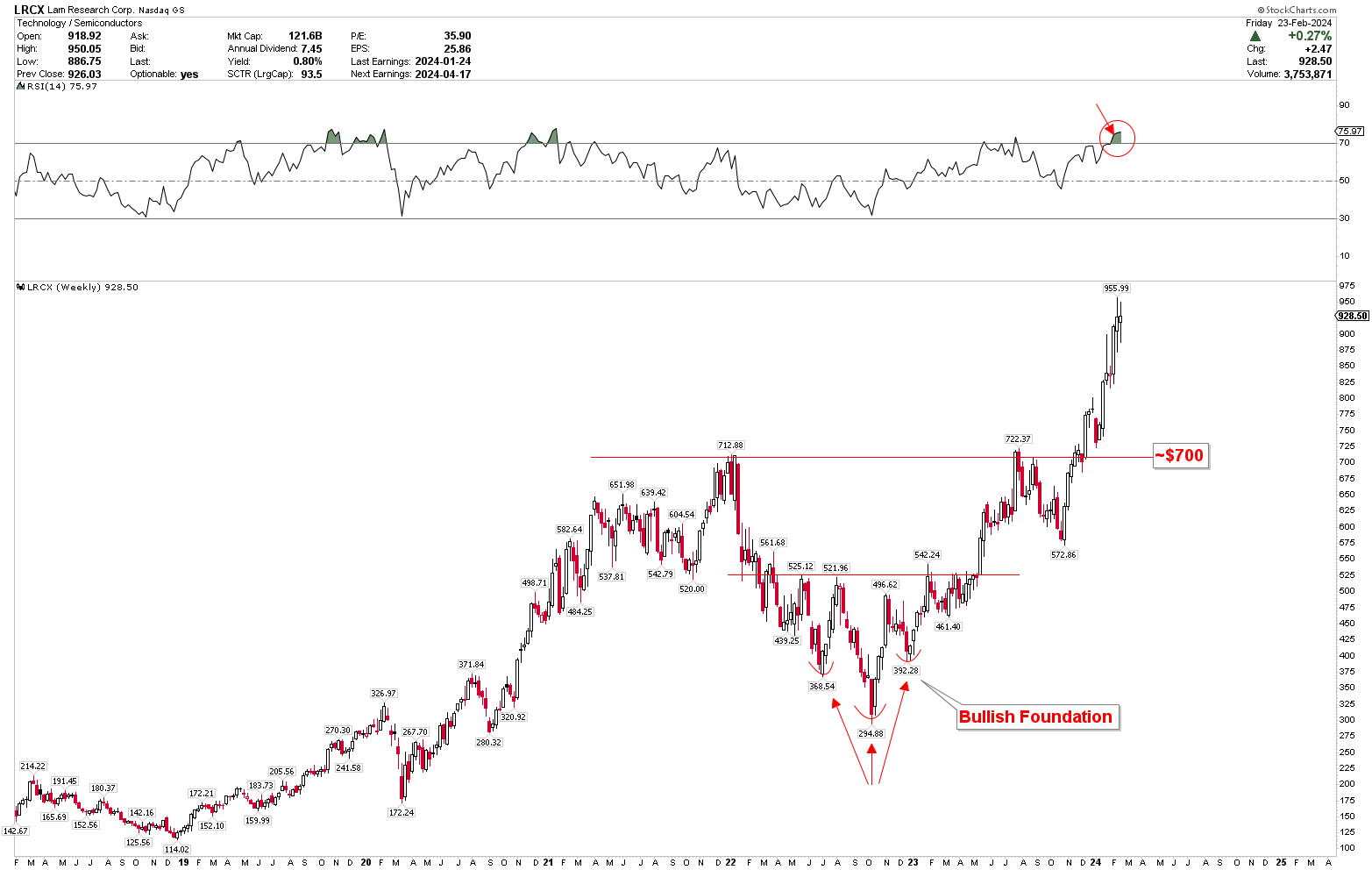

As per the above dialogue, the inventory worth is presently buying and selling at strong resistance and regarded overbought. This overbought situation is additional seen by the weekly chart which exhibits an inverted head and shoulders sample with the top at $294.88 and shoulders at $368.54 and $392.28. These patterns shaped a bullish base and point out that the long-term backside was shaped. Nonetheless, RSI is presently buying and selling on the overbought ranges, which highlights the potential for a worth correction. If the value correction develops from this area, the primary help shall be $700 as proven within the chart under. Buyers can think about shopping for Lam Analysis at this stage as the corporate expects robust monetary progress in coming years.

LRCX Weekly Chart (stockcharts.com)

Dangers

The semiconductor business is cyclical in nature, which ends up in robust worth fluctuations. The cyclical volatility and rising operational bills current the difficult atmosphere for long run secure progress. The robust volatility causes robust worth will increase inside a short while, however the worth can fluctuate in large ranges. Furthermore, the cheaper price to free money move ratio highlights the upside potential, however this additionally presents the market’s present underestimation of the expansion prospects of Lam Analysis. The federal help of the Chips & Science Act presents new alternatives, however the business’s susceptibility to geopolitical rigidity, provide chain disruptions and technological shifts recommend vital dangers. The robust worth volatility is additional confirmed by the ascending broadening wedge, and the value is presently buying and selling on the higher stage of resistance of this wedge and exhibits overbought circumstances. These overbought circumstances may end up in vital worth corrections, and these corrections is likely to be deeper than expectations because of the excessive volatility.

Remaining Ideas

In conclusion, Lam Analysis’s monetary efficiency for This fall 2023 exhibits the potential for secure progress. Regardless of the increment in whole working bills, the corporate exhibits robust progress in web revenue and free money flows, which highlights the operational effectivity. The corporate’s present monetary standing to capitalize on the robust demand for AI and HPC set the stage for long-term income progress regardless of short-term fluctuations. Furthermore, Lam Analysis might additionally profit from the analysis and growth initiatives from the federal help of $5 billion funds.

Alternatively, the technical evaluation signifies robust bullish momentum in the long run, however the worth is presently buying and selling on the overbought ranges which signifies robust potential for worth correction. Because the fundamentals are robust, the subsequent worth correction could also be considered as a robust shopping for alternative for long-term buyers. The robust help for Lam Analysis is round $700 and buyers can think about this stage as a shopping for spot for the funding.