Bennett Raglin

Citi Tendencies (NASDAQ:CTRN) is an American retailer specializing in attire and equipment in bodily shops in low-income neighborhoods.

The corporate obtained a windfall when pandemic stimulus cash hit its core demographic strongly, and it grew to become a meme inventory for some time.

After the pandemic, the reverse occurred. The corporate’s low-income demographic is affected by inflation and curbing spending. Regardless of having extra shops, the corporate sells lower than throughout the pandemic.

I like the corporate’s worth proposition and give attention to a selected core buyer (African American low-income moms). The corporate has a robust steadiness sheet to climate an financial downturn. It may doubtlessly recuperate gross sales. The corporate made efforts to manage SG&A, albeit unsuccessfully.

Nonetheless, Citi Tendencies’ present inventory value already reductions a restoration, so the inventory is just not a possibility. I imagine Citi Tendencies is a Maintain and never a Purchase.

Firm Introduction

Citi Tendencies has an easy worth proposition: low costs, a big assortment, and easy shops for African American low to middle-income moms.

Citi Tendencies retailer inside (Wikipedia)

The corporate’s common buyer has a family revenue of lower than $45,000, with 50% of consumers incomes lower than $25,000.

Pre-pandemic investor presentation slides present that 90% of their clients are girls and that 85% of them are African American.

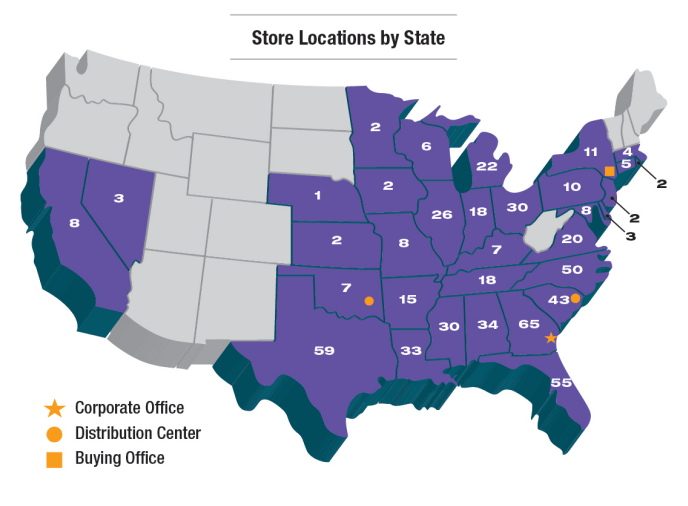

Citi Development shops are situated largely within the Southeastern states, plus close to Chicago, with headquarters in Georgia and distribution facilities in Oklahoma and South Carolina.

Citi Tendencies retailer areas by state (Citi Tendencies FY22 10-Ok)

Males’s merchandise solely make up 18% of gross sales, with the remainder being comprised of Ladies (26%), Youngsters (22%), Equipment (18%), House (9%), and Footwear (7%), in accordance with the corporate’s FY22 10-Ok.

As seen within the picture above or many YouTube procuring vlogs, the corporate’s retailer layouts are easy, with few fixtures. Costs are very aggressive, with most gadgets within the $10 to $25 vary.

Citi Tendencies doesn’t promote (lower than $1 million was spent on this class in FY22), doesn’t have an e-commerce platform, and doesn’t provide reductions.

The corporate has 600 shops and about 4,500 workers.

Pandemic Growth And Bust

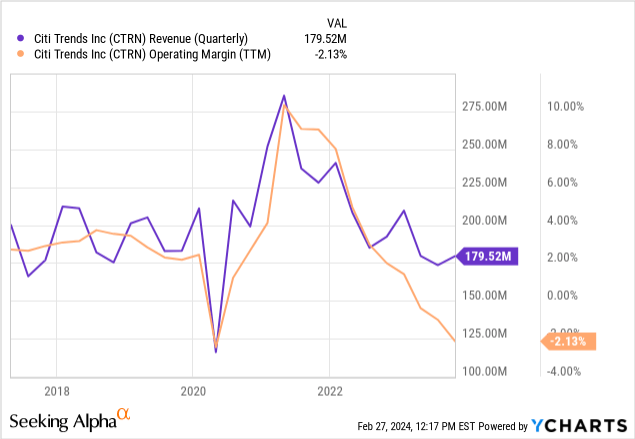

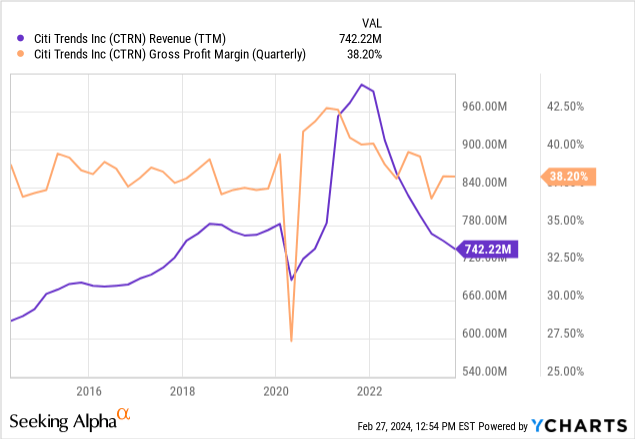

The stimulus cash distributed throughout the pandemic helped the low-income demographic to which Citi Tendencies caters. This led to an explosion in revenues and consequent margin growth, reaching 8% working margins.

Sadly, stimulus cash was not infinite, and finally, inflation began ravaging CERN’s buyer’s revenue. Inflation all the time hits poorer individuals tougher as a result of they don’t have monetary property, usually pay hire, and have much less in-demand jobs with decrease bargaining energy. Inflation was particularly laborious this time in non-discretionary gadgets like fuel and meals.

The ensuing fall in gross margins was anticipated, as attire retail suffers from operational leverage each methods (shops and workers can’t be adjusted on par with demand).

Nonetheless, identical to with just lately coated Tilly’s (TLYS), I’m stunned to the extent that inflation has hit Citi Tendencies’ revenues. The corporate sells lower than earlier than the pandemic regardless of having 7% extra shops. It in all probability signifies that the corporate is having bother attracting clients on high of the macroeconomic headwinds.

Additionally, much like Tilly’s, the corporate’s working margins are a lot decrease than earlier than the pandemic, even with related gross sales.

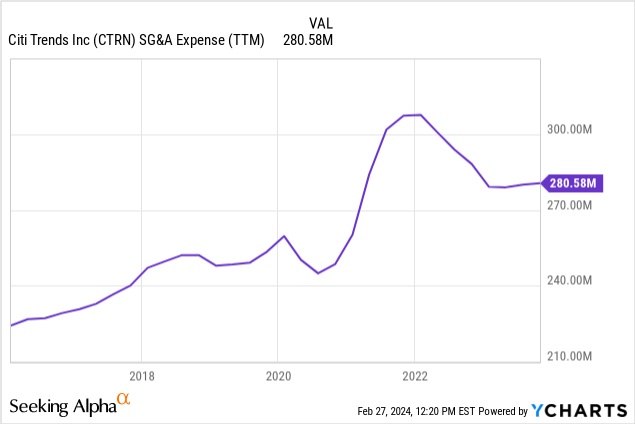

The SG&A Drawback

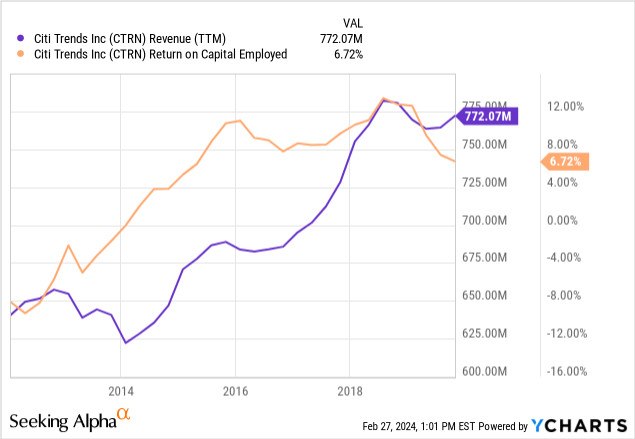

As proven within the above part, the corporate was worthwhile in 2016, 2017, 2018, and 2019, with revenues which can be much like as we speak’s.

Why is it now exhibiting operational losses? The reason being sticky SG&A bills. Regardless of having the identical stage of revenues, Citi Tendencies’ TTM SG&A is $32 million larger than in FY19.

One portion is retailer hire. Citi Tendencies data lease bills in SG&A. These amounted to $71 million in FY22, in contrast with $58 million in FY19. This represents a $13 million improve, $6 million of which comes from the sale and leaseback of its two distribution facilities.

Extra importantly, retailer worker salaries have gone up. In FY19, the corporate had 5,700 workers, in comparison with 4,800 in FY22. That’s an enchancment, contemplating Citi Tendencies has 606 shops as of 3Q23 versus 574 in FY19.

Nonetheless, in accordance with the corporate’s proxy statements for FY22 and FY19, the median worker compensation was $16 thousand in 2019 versus $25 thousand in 2022. Regardless of the lower in headcount, the corporate is now paying virtually $30 million extra in wages than it did in 2019.

This means that administration is working to enhance its effectivity through fewer staff for extra shops, however that the rise in labor prices is greater than offsetting this effort.

Valuation and expectations

Citi Tendencies trades as we speak at a market cap of $255 million and an EV of $190 million (in all probability nearer to $165 million after 4Q23 outcomes as a result of inventories develop into money).

The corporate’s gross margins for 3Q23 are already within the pre-pandemic vary of about 38%. With SG&A of $280 million (very sticky), the corporate must make $740 million to interrupt even. This means that if the corporate can arrest the income fall, it ought to be capable to breakeven operationally in 2024.

Within the pessimistic state of affairs, the corporate would in all probability have to finance losses and shut shops if revenues hold falling. Happily, it has $60 million in money as of 3Q23 and sure as a lot as $85/90 million by 4Q23 (post-Holidays). That is virtually half of the discounted lease liabilities of the corporate.

Alternatively, to generate a ten% earnings yield on the above EV of $160 million, contemplating 30% in revenue taxes and 38% gross margins, the corporate ought to publish revenues of $800 million, or 8% above the present stage.

This does not appear very simple, given the present context. Additional, suppose the corporate’s inventory yields a good return solely beneath the optimistic state of affairs however not the present or a pessimistic one. In that case, it’s in all probability not alternative at these costs.

Additional, it isn’t that Citi Tendencies was a implausible enterprise pre-pandemic, with solely average development charges and common returns on property.

For that cause, I imagine Citi Tendencies’ inventory is just not a possibility as we speak, though I’ll proceed to observe the title.