visualspace/iStock through Getty Pictures

Pricey readers/followers,

Sampo (OTCPK:SAXPF) (OTCPK:SAXPY) has been an funding I’ve put capital into a number of occasions over the previous 10 years, and all the time exited with a good or acceptable RoR given the circumstances. For the previous 1-2 years for the reason that firm made huge modifications in its construction, particularly changing into much less of a multi-line finance conglomerate that owns 20%+ of the Financial institution Nordea (OTCQX:NRDBY), to a pure-play insurance coverage holding firm, I have been considerably much less enthused in regards to the firm.

This isn’t associated to any materials weak spot within the firm’s fundamentals, however relatively what the market has put by way of pricing for this enterprise. After I final wrote about it, the corporate had dropped 15% in lower than 4 months. I didn’t change my “HOLD” ranking, and certainly this was the proper selection. As a result of since then, the corporate, regardless of transferring up, has underperformed the broader S&P500 by a cloth quantity of round 7% since then.

Now, my earlier thesis on Sampo was clear. Sampo has a powerful mixed ratio and secure efficiency within the Nordic market, making it a pretty funding possibility on the proper worth. My PT was €35/share at the moment, on this case, October of 2023, in an article you can find here.

Let’s replace and see what this firm can do for you going ahead.

Sampo – there are such a lot of nice insurance coverage companies obtainable at cheaper costs

Once more, the argument in opposition to Sampo is just not one primarily based on poor fundamentals. As a substitute, we’re speaking about pricing. Some analysts would argue that Sampo’s very good mixed ratio by far justifies its excessive valuation – and better – and that the corporate can, actually, be purchased with a conservative upside right here.

My response to this is able to be, when you’ve got thought-about future development prospects and at what danger the corporate is rising going ahead. As of as we speak, the corporate’s native share worth is over €41/share. I take into account this to be a cloth distinction from any type of conservative valuation. The corporate yields lower than 4% in a market the place 4% is principally the risk-free deposit price.

Stability is definitely price one thing. And really, extra analysts than I’ve anticipated have gone to name this firm “undervalued” within the final 2 months. That is one of many causes I am writing this text – to defend my stance on the enterprise.

First off, as of this text, I’m growing my worth goal on Sampo.

Why am I doing this?

As a result of the corporate is exhibiting very favorable pricing developments, managing to extend pricing forward of inflation in all classes and geographies. I actually don’t solely have my personal insurance coverage by way of one of many fully-owned firms by Sampo, however I even have my company insurance coverage – all of it – by way of the corporate. I am very conversant in how they function, and I like what they do.

The corporate has additionally, lastly, gotten to some extent the place a secure distribution is feasible along with a brand new buyback program. As to what actual stage of distribution I’m growing my goal, we’ll get again to that within the close to time period future within the valuation section for Sampo.

For now – know this.

Sampo is without doubt one of the largest private line insurers in Scandinavia. Its major focus is just not on development, however on enhancing its underwriting high quality. Which means that as an insurer, it is paying much less in acquisition prices. As a result of the corporate has digitized a lot of its operations throughout its varied owned firms within the insurance coverage house, this will increase effectivity.

In brief, Sampo is doing just about all the pieces proper and appears to be enhancing much more on this on a ahead foundation.

Additionally, most of the firm’s property, which I’ve spoken about as riskier previously, are property that the corporate both has divested or is actively within the strategy of divesting. A great instance right here is the Mandatum operations, that are being divested.

What would such capital, for these divestments, be spent on?

I consider the corporate, aside from share buybacks, will deal with enhancing its operations even additional. I consider a non-trivial share of the proceeds will probably be put into its underperforming operations, which have resulted in margin compression on a company-wide foundation. Topdanmark is the one which involves thoughts right here. Sampo already has an in-house course of for enhancing underwriting, and it is possible the corporate is already doing this with its Danish subsidiary and can proceed to do that extra on a ahead foundation.

The introduction of Hastings is just not one thing I essentially take into account a optimistic, although I perceive Sampo’s urge to develop. Executed accurately, it may very well be a value-add for Sampo who in some methods is excellent at issues like auto and restore, however maybe lacks a bit in fraud detection/KYC, the place I consider UK-based/European-based companies are higher.

A phrase or two on outcomes. The corporate did handle some fairly wonderful efficiency throughout a tough macro, which little question can be the explanation why the corporate has seen valuation enchancment. Premium development of 12% is nothing to sneeze at in 4Q, and the UK was an enormous a part of that. Claims inflation was additionally exhibiting stabilizing developments.

On the flip aspect, and as a result of firm’s exposures, Nordic climate claims have been growing with adversarial climate results. This is without doubt one of the causes I am pretty cautious about European P&C, which Sampo is partially uncovered to. Most of the climate developments we have seen in US insurance coverage will not be but one thing we have seen in Europe – once more, but.

Sampo IR (Sampo IR)

Funding revenue was naturally optimistic with optimistic rate of interest enhancements within the risk-free price, and Sampo stays very conservatively leveraged.

The important thing ratios for the corporate improved much more. I’ve mentioned it earlier than, and I’ll say it once more. Sampo is a combined-ratio margin chief. Discover me an insurance coverage firm this dimension and sort that manages these kinds of developments.

Sampo IR (Sampo IR)

The corporate’s fastened revenue yields at the moment are up above 4.1%, which is spectacular for this type of insurance coverage store, particularly with 89% of those investments IG-rated for the brand new 2023 flows.

In occasions of bother, most additionally have a tendency to stay to “things they know”, and never check out new insurance coverage gamers. I’m personally an excellent instance of this, however the identical is true of the remainder of the market, expressed by way of elevated retention regardless of elevated charges and worth hikes.

Underwriting earnings remained stellar, and total, I don’t see any type of main indication of fear within the firm’s P&Ls.

Sampo IR (Sampo IR)

So what dangers precisely do I see?

Let’s have a look.

Sampo – Dangers and Upside for the corporate

Going straight into the dangers I see for the corporate, I say as flows. Whereas Sampo is giant, it’s not a market chief in any sector or nation. The businesses that dominate the market will not be publically listed in Scandinavia, and whereas this in itself is just not an inconceivable scenario in any means, it does open the corporate as much as competitors in a means that many bigger insurers that I put money into don’t expertise. I’d, as an example, count on the corporate to expertise extra competitors when and if they begin elevating costs additional.

Whereas I can go on and on in regards to the firm’s very good mixed ratio and an underwriting firm, most Swedish and Scandinavian firms do, actually, share this attribute. Sampo is, actually, not the very best in underwriting in its core markets.

Additionally, whereas the Hastings enterprise including to Sampo is a optimistic, it under no circumstances improved the corporate’s aggressive state. That is as a result of even Hastings faces bigger competitors in its house markets, which must be thought-about. All of this to me interprets to decrease development than we would count on going ahead.

Apart from this…even with the brand new payout, it is greater than many higher friends, and the corporate’s valuation, which we’ll have a look at, is at fairly excessive ranges after we have a look at historic ranges, each on a e-book and pure P/E perspective.

I’d characterize Sampo as a higher-risk insurance coverage funding due precisely to this pricing and valuation, not the corporate fundamentals, that are very stable.

Sampo’s Valuation

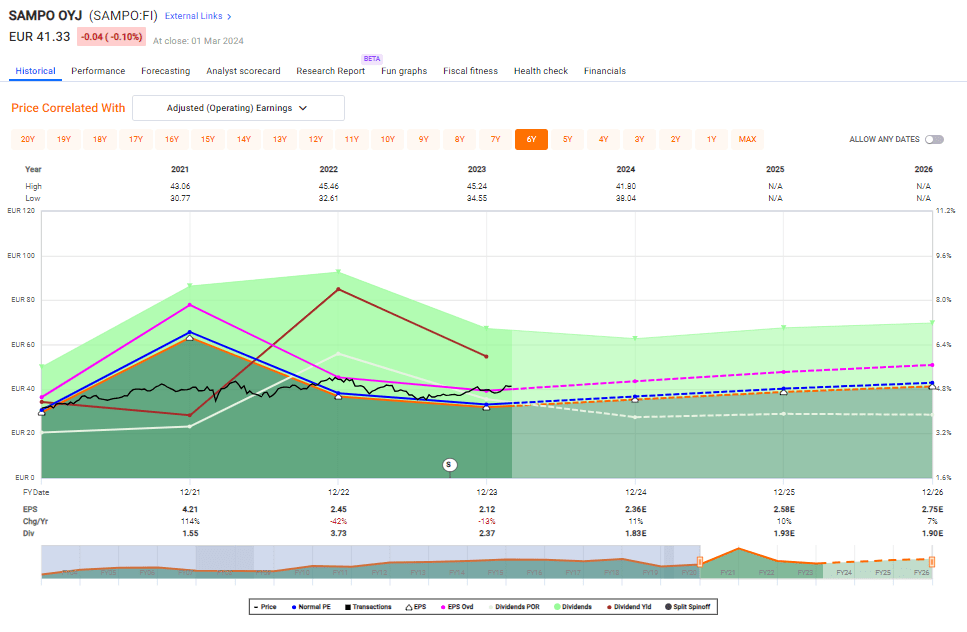

So, as I mentioned originally of this text, I am bumping my Sampo goal. On this case, that focus on is being bumped to €38/share to account for what I take into account a significant enhance within the firm’s truthful e-book worth and prospects. Different buyers have elevated it to over €43/share (Supply: Morningstar) however I’d not go that far.

I additionally wish to clearly present you that the corporate is actually at a comparatively overvalued state at this explicit time – at the least compared to any related historic ranges.

Sampo Upside (F.A.S.T graphs)

Historic ranges are definitely not gospel in any means – however they do include some relevance to me as a result of I partly do mannequin my future estimates on how the corporate has carried out on a normalized historic foundation.

Enable me to place it like this. If the corporate, which is about to develop round 7-9% within the subsequent few years on an annual foundation manages 15x P/E, which is excessive for an insurer, we get an annualized RoR of lower than 5%. As a way to get 15% per yr or above, you’d must forecast Sampo at a stage of on the very least 21-22x P/E.

Are you aware what different insurance coverage firms I take into account to be price 21-22 occasions earnings?

The easy reply – is none. And never Sampo both.

The 20-year normalized common involves lower than 15x, round 13.5x. Even the 10x common doesn’t attain 15x. It is solely in the previous couple of years that the corporate has managed to broach that 15x, and once more, that 5-year normalized is round 16x which might indicate annualized about 7%, and that is with dividends.

Are you seeing my downside with this?

I could also be harping fairly a bit on normalized P/E ratios right here, however the e-book ratios present the same imbalance to the historic numbers.

The principle query for you have to be if you happen to consider that Sampo’s divestment of Nordea has been a danger discount and a value-add by way of what the corporate has executed since then.

I don’t consider that to be the case. I actually consider they need to have caught with their Nordea stake, particularly given the newest few years of efficiency. I personal a big Nordea stake in each my personal and my company portfolio, and that has actually executed higher than Sampo.

Due to that, that is my thesis for Sampo.

Thesis

- Sampo is without doubt one of the higher insurance coverage firms in all of Europe. Along with Allianz, Munich Re, and AXA, I take into account them the 4 prime investments in multi-line and reinsurance. At any time when certainly one of them is reasonable, that could be a time to “BUY” the corporate for me.

- Sampo, at this explicit time, is just not an affordable firm per se. Buying and selling at 16x P/E, each on a European and Worldwide comparability, it is an costly insurance coverage firm for what it provides, regardless of its very good administration and A-rated credit score security in addition to very low leverage and over €20B price of market cap.

- I’d at present view Sampo as a “HOLD” right here. As soon as the corporate hits under €38/share, I’d take into account it a “BUY” once more. It is a elevating of my PT, however nonetheless nowhere close to the present worth of €41.3.

Bear in mind, I am all about :1. Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly huge – firms at a reduction, permitting them to normalize over time and harvesting capital features and dividends within the meantime.

2. If the corporate goes effectively past normalization and goes into overvaluation, I harvest features and rotate my place into different undervalued shares, repeating #1.

3. If the corporate would not go into overvaluation, however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

4. I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (italicized).

- This firm is total qualitative.

- This firm is essentially secure/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is at present low cost.

- This firm has a sensible upside primarily based on earnings development or a number of enlargement/reversion.

As a result of it’s neither low cost nor has a stable upside potential, I view this as not being an fascinating or legitimate funding at the moment primarily based on my objectives. I give the corporate a “HOLD”.

This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.