Hispanolistic

Fairness flows have improved in latest weeks. Regardless of money persevering with to pour into cash market funds over the previous year-plus, buyers are seemingly keen to step out onto the danger curve, placing extra liquidity to work into shares and high-grade fixed-income. That bodes effectively for asset administration corporations, however not all of those corporations are created equal.

I reiterate my maintain ranking on Franklin Sources (NYSE:BEN). Whereas the agency has a string of EPS beats, its funding efficiency has been lackluster recently, and the continued shift from energetic to passive is a headwind.

Traders Shopping for Up Shares Just lately

BofA World Analysis

In accordance with Financial institution of America World Analysis, Franklin Sources is a worldwide asset supervisor with over $1.455 trillion in property underneath administration, over 10,000 workers globally, and a presence in six continents. BEN offers funding administration providers to retail, institutional, and high-net-worth purchasers globally with capabilities throughout all asset lessons together with equities, mounted revenue, multi-asset, alternate options, and cash market.

BEN reported a strong set of Q1 outcomes. First-quarter non-GAAP EPS verified at $0.65, topping the consensus estimate by $0.07 whereas income of $1.99 billion was up simply 1% in comparison with the identical quarter final 12 months. Shares have been little modified after the report, however there have been important web outflows through the reporting interval, significantly in its fixed-income enterprise.

Key dangers embody extra weak spot in its energetic fairness methods and delicate numbers from the alts area, as larger investment-grade company bond yields could also be a extra engaging possibility for buyers.

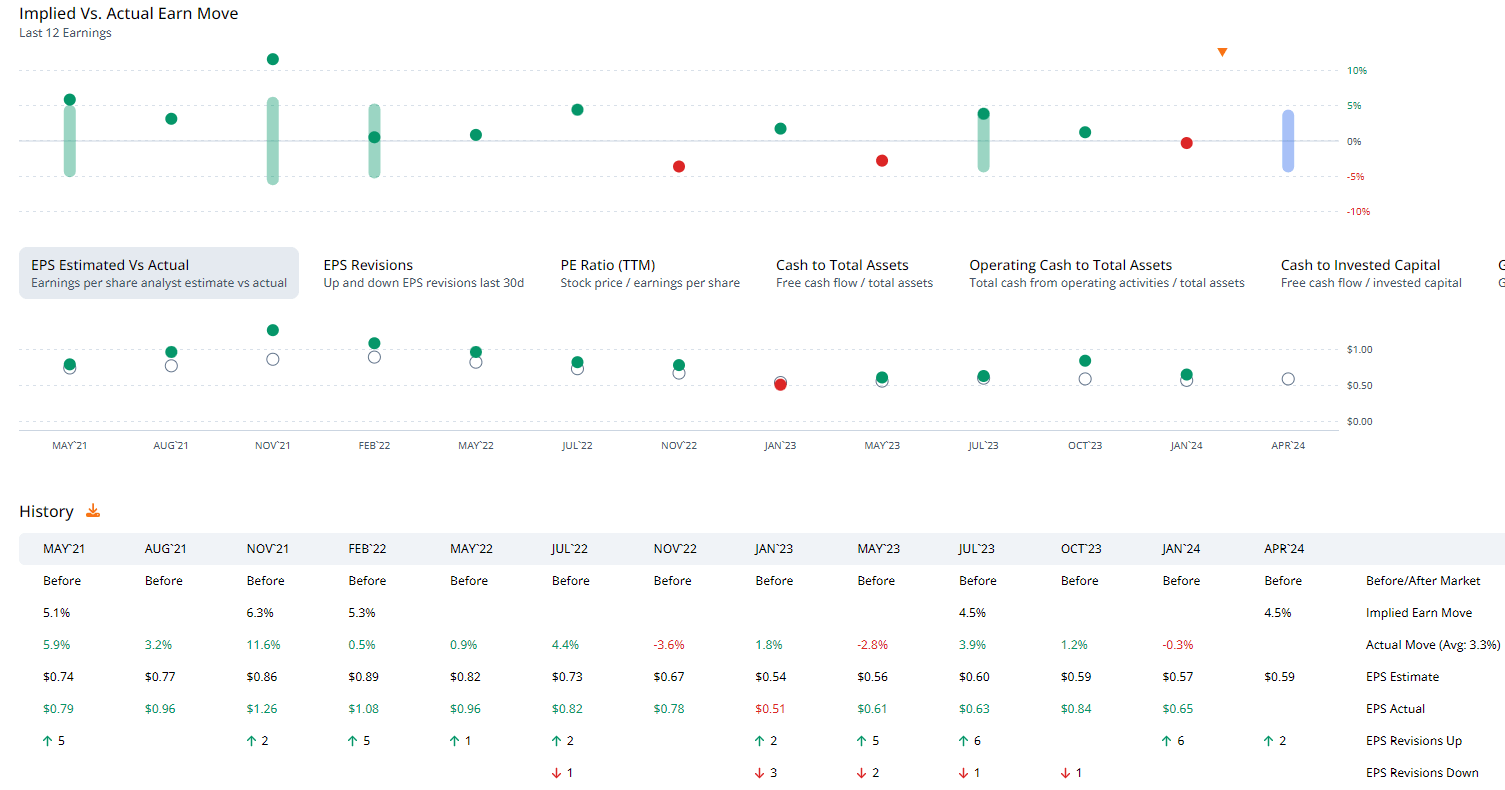

Forward of its Q2 outcomes due out in late April, the choices market has priced in a average 4.5% earnings-related inventory value swing when analyzing the at-the-money straddle expiring soonest after the report, in keeping with knowledge from Choice Analysis & Know-how Providers (ORATS). BEN has crushed bottom-line EPS estimates in every of the previous 4 quarters, per In search of Alpha.

BEN: Sturdy EPS Beat Fee Historical past

ORATS

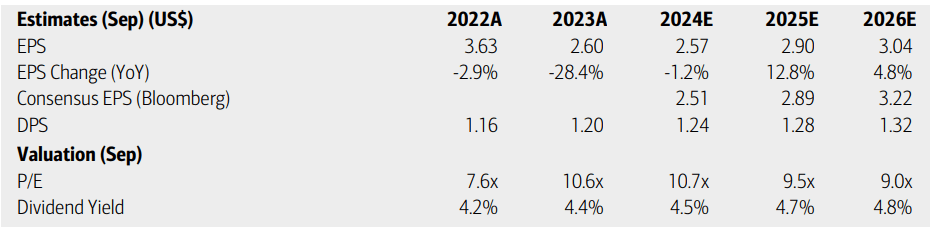

On valuation, analysts at BofA see earnings being about flat this 12 months however per-share revenue progress is predicted in 2025 with steadier progress by 2026. The In search of Alpha consensus outlook is a little more downbeat for 2024, however extra optimistic within the out 12 months. Income is seen rising by 5% this 12 months and subsequent, with simply 1.2% progress by 2026.

Dividends, in the meantime, are forecast to rise at a sluggish tempo over the subsequent handful of quarters. Whereas the valuation is low, the expansion story seems weak as BEN faces secular headwinds within the asset administration enterprise.

Franklin Sources: Earnings, Valuation, Dividend Yield Forecasts

BofA World Analysis

Contemplating that BEN’s long-term ahead non-GAAP price-to-earnings ratio is simply 11.4, and assuming normalized EPS of $2.60, then shares needs to be priced simply shy of $30, leaving some, however little, upside from right now’s value.

With a high yield, above 4.5% as of March 1, 2024, there may be an revenue case to be made, significantly if BEN can certainly generate near $3 of working EPS in 2025. Nonetheless, the onus is on the administration group to fight the headwinds talked about earlier.

BEN: Low-cost on Earnings, Excessive Yield, However Weak Progress

In search of Alpha

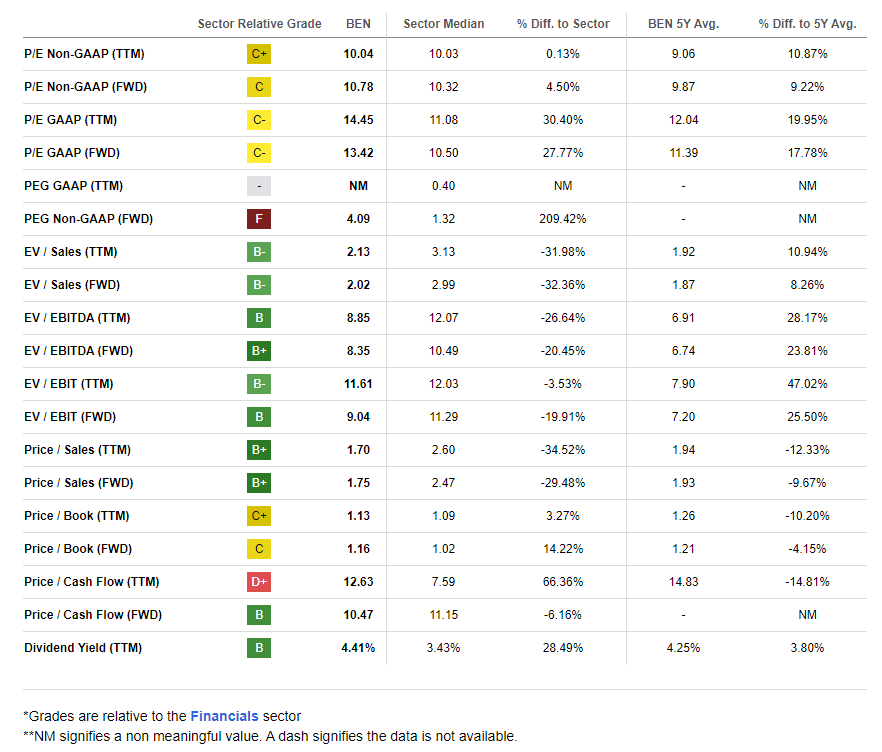

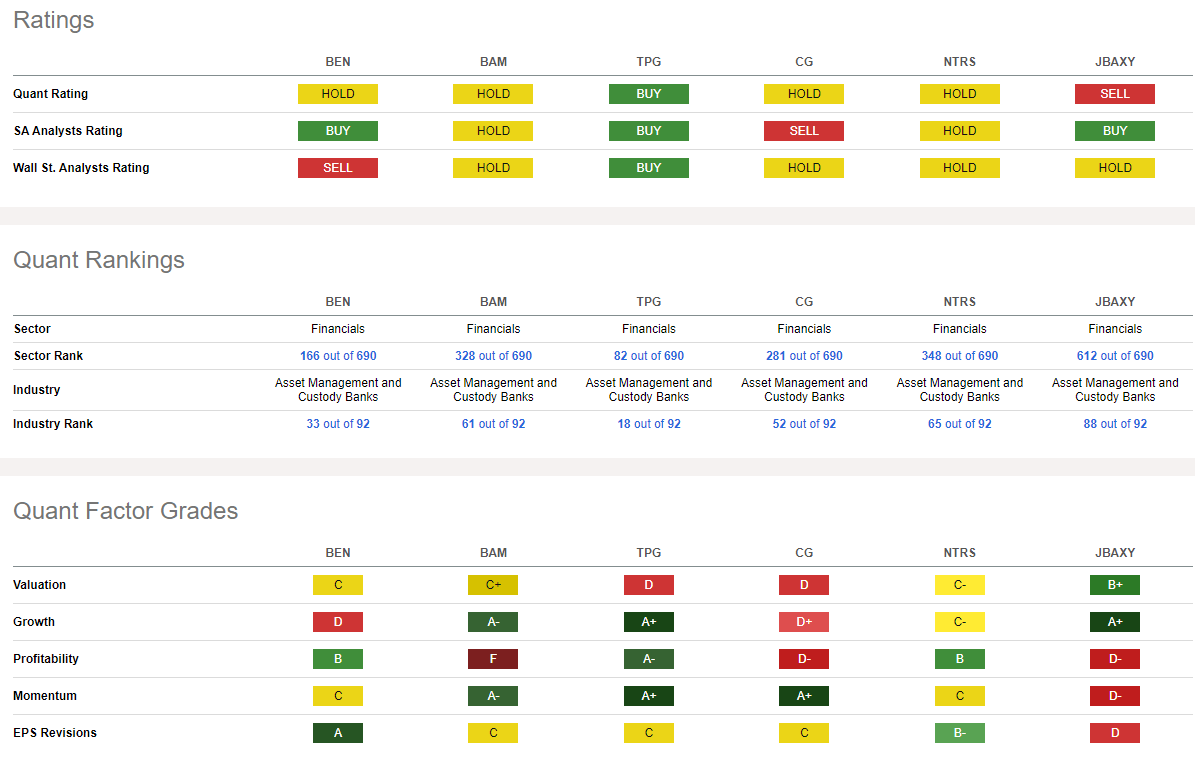

In comparison with its friends, BEN encompasses a lukewarm valuation grade, whereas its progress trajectory is notably weak. Profitability trends are decent, and I believe the yield is protected for now, however share-price momentum is lackluster, I’ll spotlight key value ranges on the chart to watch later within the article. Lastly, EPS revisions are decidedly constructive following the string of bottom-line beats.

Competitor Evaluation

In search of Alpha

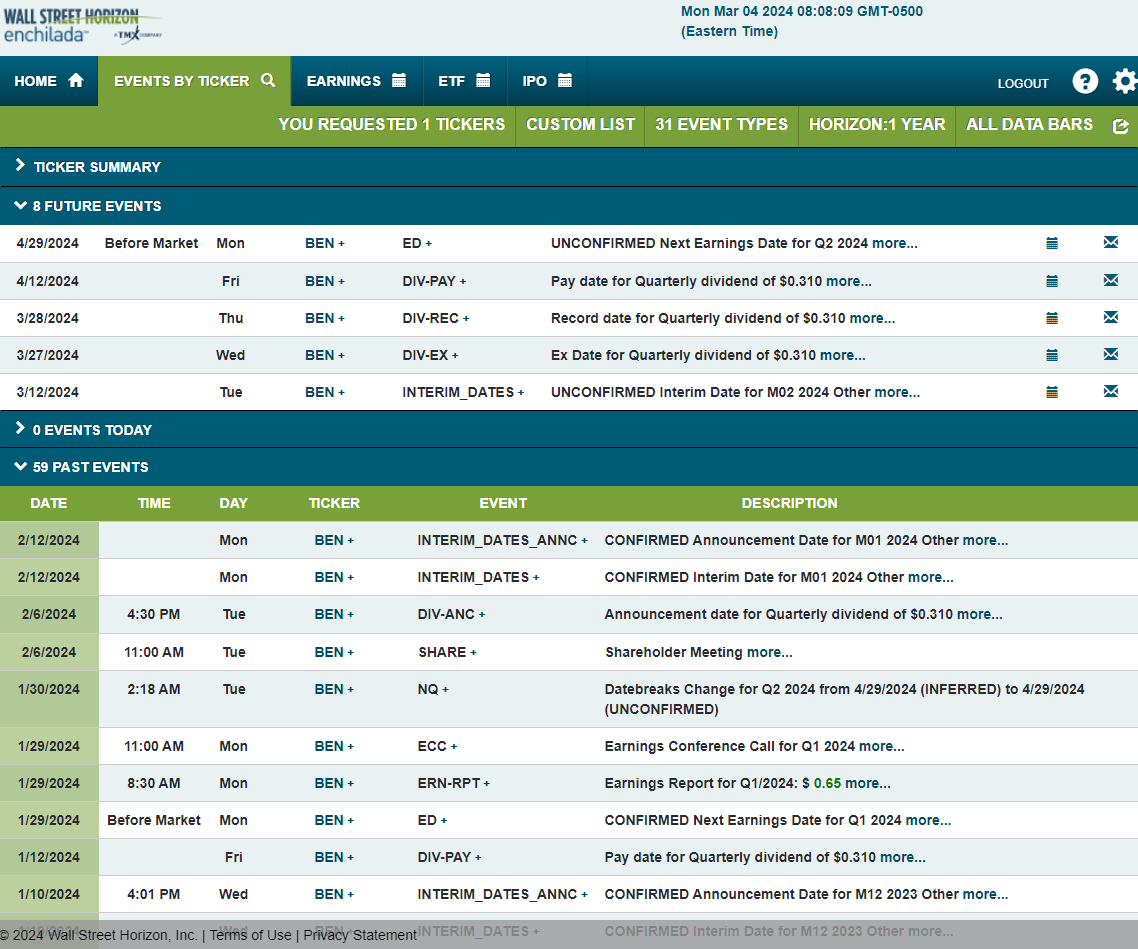

Wanting forward, company occasion knowledge supplied by Wall Avenue Horizon exhibits an unconfirmed Q2 2024 earnings date of Monday, April 29 BMO. Earlier than that, the agency is slated to report interim month-end AUM figures. Recall final month that AUM rose 9.6% in January, reflecting its take care of Putnam.

Company Occasion Danger Calendar

Wall Avenue Horizon

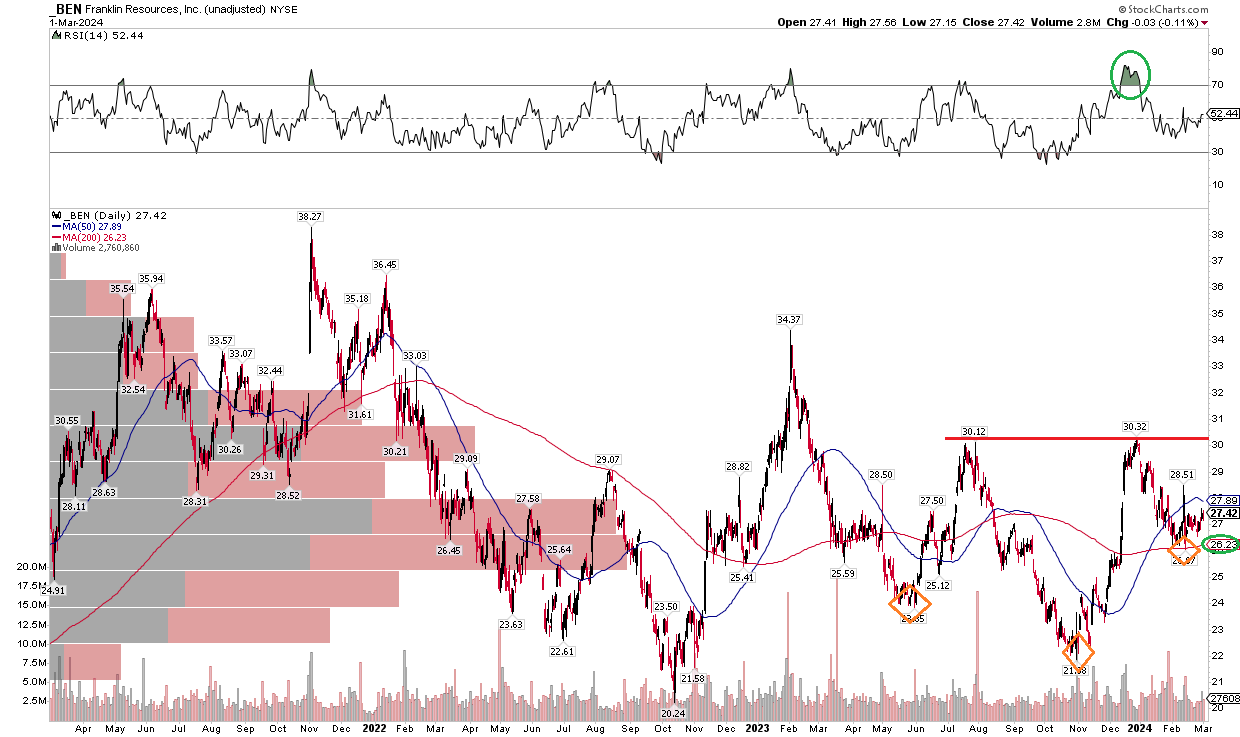

The Technical Take

I used to be impartial on BEN again in Might final 12 months. And whereas shares are larger now, the Financials sector inventory has sharply underperformed the S&P 500. As we speak, I see related impartial traits on the chart. Discover within the graph under that shares have apparent resistance on the $30 mark. As long as the inventory is underneath that spot, it’s laborious to be overly bullish on its momentum. Furthermore, the long-term 200-day transferring common is flat in its slope – this comes because the broad market has rallied sharply within the final 12 months, so there’s a excessive quantity of damaging alpha with BEN.

Additionally, check out the RSI momentum gauge on the prime of the chart – it really printed a powerful larger excessive when shares tried to rally above the excessive from the summer season of final 12 months. The bears re-asserted themselves, although, and BEN retreated to its 200dma. For now, I see help close to $26 with long-term help within the $20 to $22 zone, at which value it will be a strong worth thought.

Total, BEN’s chart is unimpressive, whereas momentum can not appear to maintain itself.

BEN: Stagnant Momentum, Lengthy-Time period Underperformance

Stockcharts.com

The Backside Line

I reiterate my maintain ranking on Franklin Sources. The corporate faces ongoing challenges within the energetic asset administration trade, although latest AUM traits are encouraging. With a low earnings a number of, there’s a worth case to be made contemplating its excessive yield, too, however technical momentum stays weak.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.