Michael M. Santiago

Introduction

On December 21, 2023, I wrote about Pfizer Inc. (NYSE:PFE) inventory for the primary time after an extended hiatus since initiating coverage in November 2021. Final time, I wrote about PFE showing oversold and undervalued as a result of seemingly underestimated EPS forecasts for FY 2025 and past. I urged to not panic, however to consider constructing an extended place on the low worth ranges. Sadly, the PFE inventory has since considerably underperformed the broader market:

In search of Alpha, my earlier article on PFE

Nonetheless, a complete quarter has already handed since mid-December. Throughout this time, the corporate managed to current its report for This fall FY2023 and communicate on the TD Cowen 44th Annual Health Care Conference. So what has modified within the relevance of my thesis throughout this time? Let’s discover out collectively.

Pfizer’s This fall FY2023: Financials And Prospects

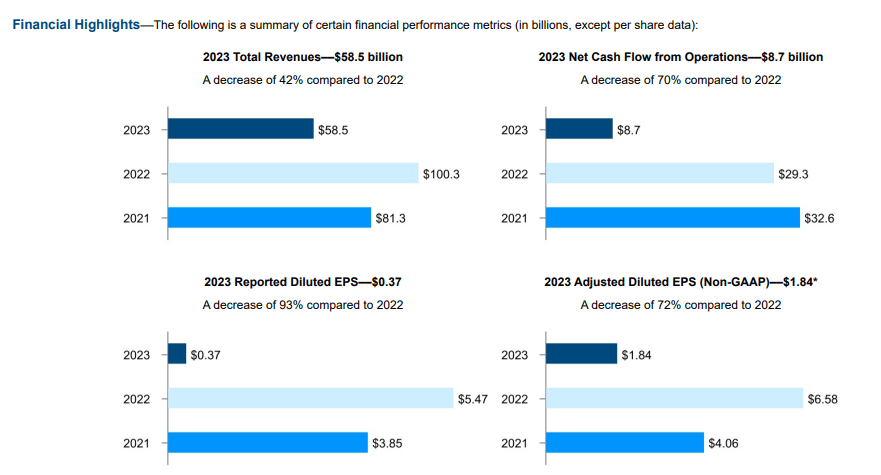

Straight from the press release, we see that Prizer is struggling in its post-COVID period, with consolidated revenues experiencing a major downturn (-41% and -42% YoY for This fall and full year 2023, respectively). Final quarter, the corporate’s reported bottom-line noticed a notable shift from a revenue of just about $5 billion in This fall FY2022 to a lack of round -$3.4 billion in the identical interval of 2023, marking a considerable 93% decline for the complete yr. Equally, reported diluted EPS dropped from $0.87 to a lack of -$0.60 in This fall FY2023. The overall pattern for 2023 might be described as a “rapid fall after a lightning-fast rise”:

PFE’s 10-Ok

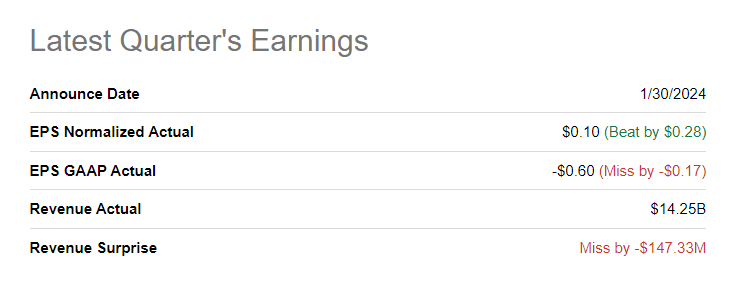

After all, Wall Avenue had initially anticipated a decline, however Pfizer nonetheless dissatisfied, lacking market expectations on a GAAP foundation by lacking on each revenue and gross sales.

In search of Alpha, PFE

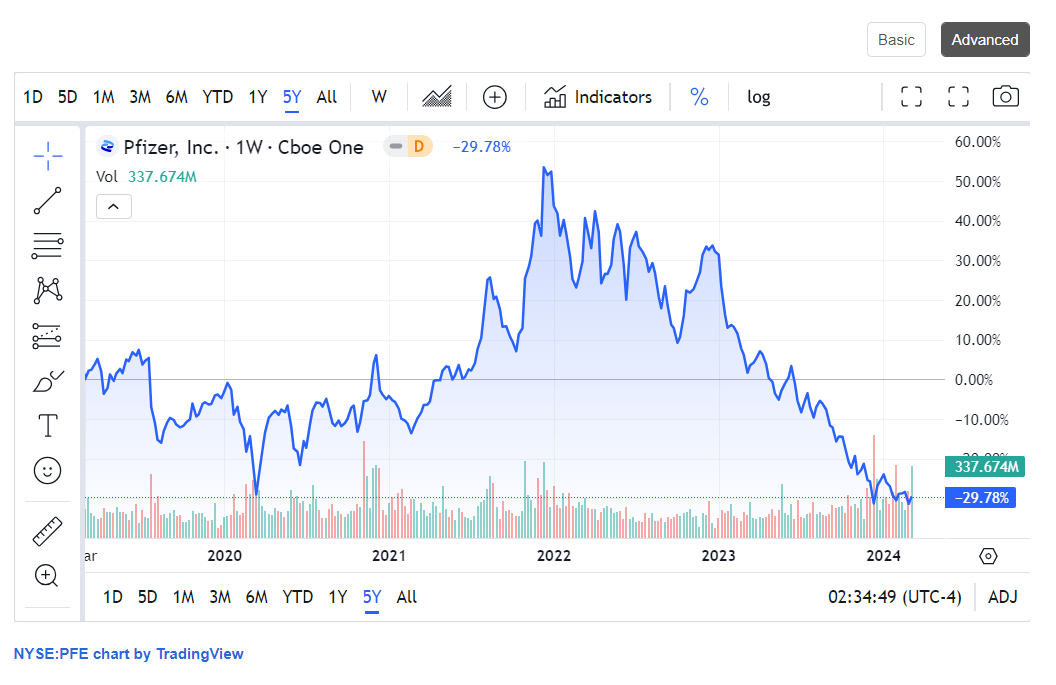

However, PFE beat EPS consensus on a non-GAAP foundation fairly considerably (+$0.10 precise vs. -$0.18 anticipated). However that was not sufficient, and the PFE inventory went to check its 5-year lows after the outcomes:

In search of Alpha, TradingView

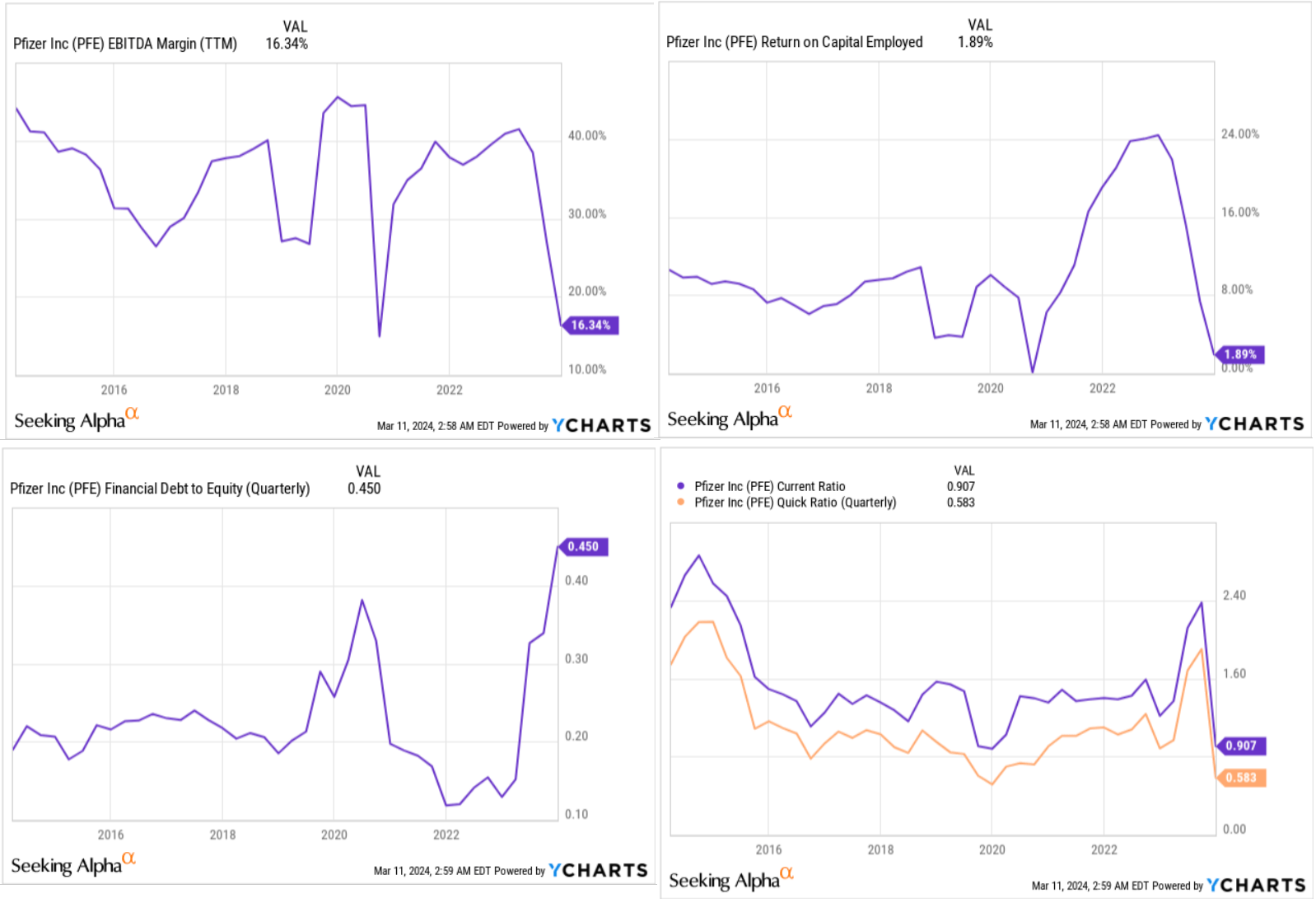

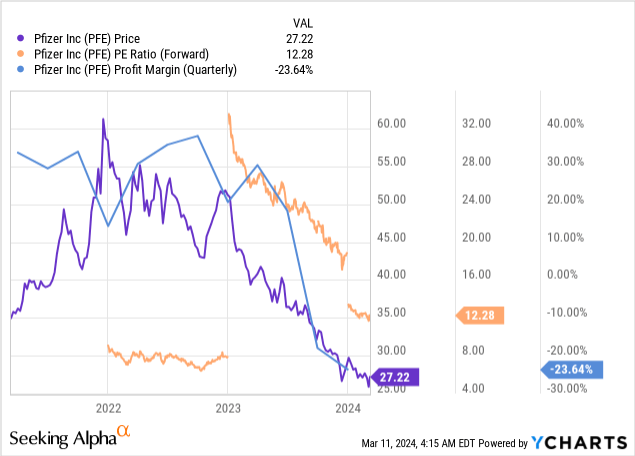

This inventory worth improvement is in no way stunning, because it follows a far-reaching deterioration in a variety of key monetary figures: EBITDA margin is again at a 10-year low, as is ROCE; on the identical time, leverage is rising quickly as a result of acquisitions, and liquidity on the stability sheet relative to liabilities is falling quickly.

YCharts, creator’s notes

In my view, the mere proven fact that PFE’s leverage has not elevated additional and that the corporate has been capable of preserve constructive profitability is one thing of a hit underneath the present situations.

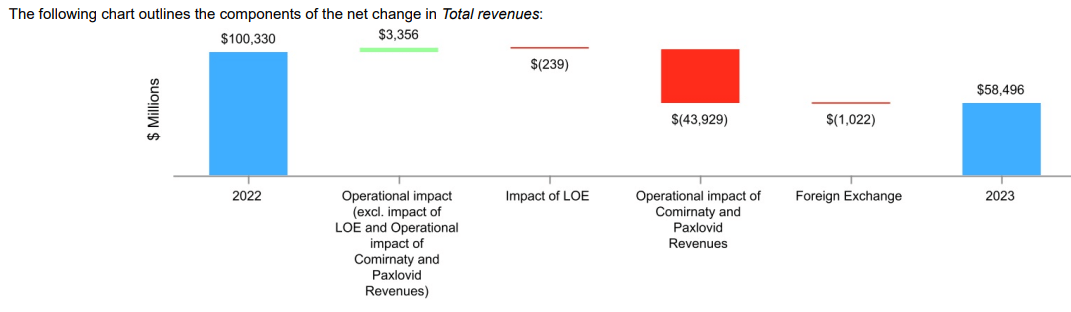

It is clear to all market members monitoring Pfizer’s enterprise what precisely is inflicting such a fast decline in financials. Gross sales of Comirnaty and Paxlovid fell by 70% and 93% (worldwide) respectively in FY2023 in comparison with the earlier yr. That is primarily because of the present insignificance of COVID. Which means PFE under-earned nearly $44 billion in gross sales in 2023 due to these medication. With at the least some working leverage, it ought to in any case have led to the deplorable dynamics of the underside line, as a result of such an adjustment in gross sales often results in a non-linear adjustment in prices.

Nonetheless, if we take these two vital medication out of the equation, it exhibits that PFE’s gross sales would truly improve by round 3.7% year-on-year in FY2023.

PFE’s 10-Ok

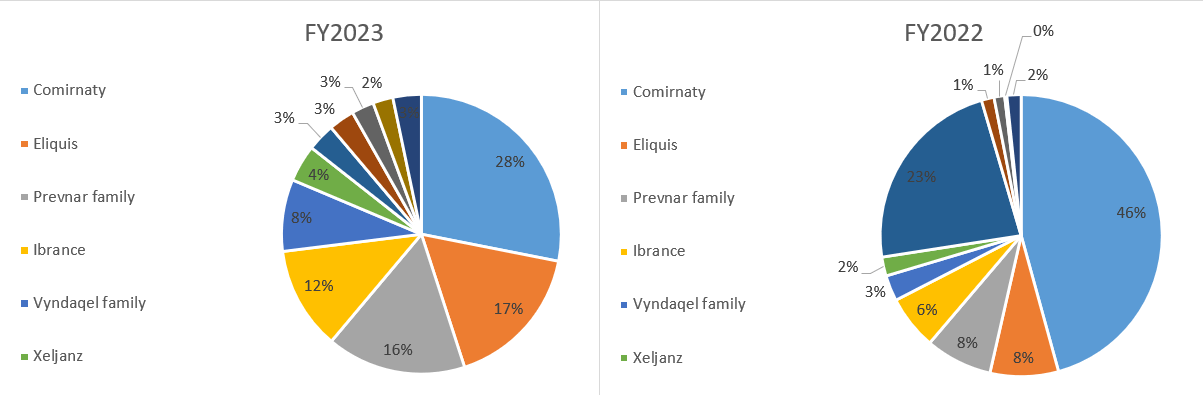

If we take PFE’s foremost sources of income and picture that the corporate has nothing else other than them, we are able to see, due to easy pie charts, that the significance of Comirnaty and Paxlovid is quickly declining. On the time of the final report, none of those medication reached 45%+ of the whole “pie”, as was the case with Comirnaty final yr:

Writer’s work, based mostly on Pfizer’s 10-Ok

If we now think about that the gross sales figures of Comirnaty and Paxlovid decline by the identical relative quantity on the finish of 2024 as in 2023 (-70% and -93% respectively), then the whole influence on gross sales is just -$9.04 billion as an alternative of -$44.24 billion (all different issues being equal).

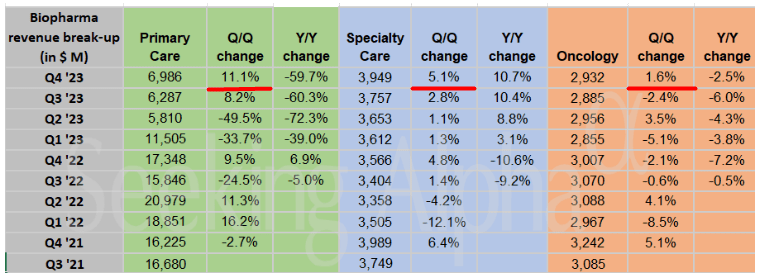

Different merchandise at the moment are coming onto the scene, which have proven way more steady momentum in latest quarters. In This fall FY2023, for the primary time in years, we noticed three sub-segments of the corporate – Specialty Care, Oncology, and Main Care – grow simultaneously QoQ:

In search of Alpha, creator’s notes

In the course of the newest TD Cowen convention, Pfizer’s CFO David Denton underscored the agency’s deal with innovation, notably in oncology following the acquisition of Seagen, and the implementation of a cost-saving program geared toward attaining $4 billion in financial savings by the tip of 2024. In different phrases, this price saving can overshadow the potential results of the above-mentioned drop in gross sales. Nonetheless, we should additionally keep in mind that the quantity of direct prices will proceed to fall along with that $4 billion.

Roughly talking, it may subsequently be assumed that the post-COVID hunch has now been left behind as a result of small price financial savings and the idea that the Comirnaty and Paxlovid phases will proceed on the identical price of decline.

Nonetheless, I additionally see some upsides to that conclusion.

First, Comirnaty and Paxlovid will most certainly not disappear fully from the market in 2024, regardless of the lightning-fast decline. As Seeking Alpha News team reported a number of days in the past, “a U.S. Centers for Disease Control advisory panel has recommended that adults aged 65 years and older get an additional COVID-19 vaccine shot this spring.” That’s, the decline price I assumed above is probably not that extreme. If that’s the case, PFE’s consolidated gross sales will then most certainly be considerably increased.

Second, I am undecided how Pfizer’s first Super Bowl commercial will assist entice new gross sales for the Oncolgy sub-segment, however Padcev (an antibody-drug conjugate Pfizer added with the Seagen acquisition) and the newly launched RSV vaccine Abrysvo ought to present new gross sales development, as Guggenheim analysts recently noted.

As I’ve written earlier than, I’m usually very optimistic about “Pfizer’s oncology future”, and up to date developments such because the FDA approval for the antibody-drug conjugate Besponsa in youngsters affirm my opinion.

As I as soon as wrote about Organon (OGN) in late November 2023, it’s typically darkest earlier than the daybreak. I believe we see a roughly comparable image within the case of Pfizer: A depressed previous, albeit not so long as within the case of OGN, doesn’t permit traders to see the forest for the timber. From an operational perspective, I believe we’ve a robust restoration forward of us. However how a lot is already priced in?

Pfizer Inventory Is Now Even Extra Engaging – Valuation

Assuming that the worst is over for PFE, I discover it considerably puzzling how Wall Avenue analysts reacted after the discharge of This fall FY2023 outcomes – all of them lowered their estimates for Q1 FY2024 (and past):

In search of Alpha, PFE, creator’s notes

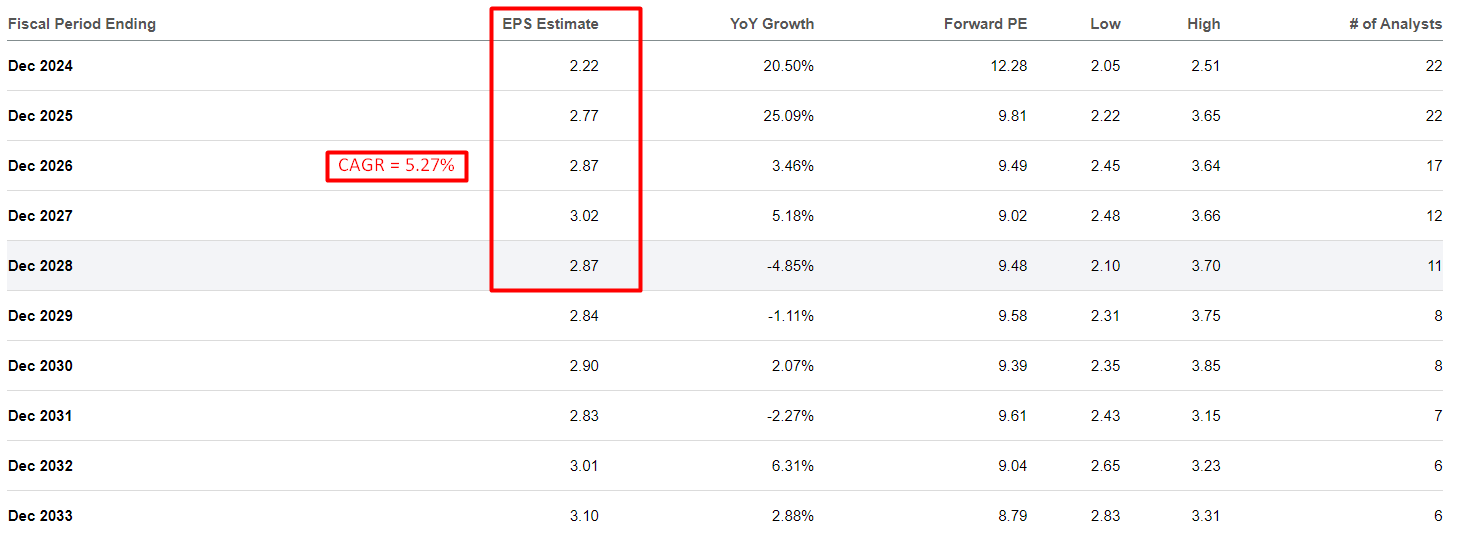

Even in opposition to the backdrop of this negativity, the consensus data exhibits an implied EPS CAGR of round 5.27% for the following 5 years with an exit P/E a number of in FY2028 of solely 9.48x:

In search of Alpha, creator’s notes

Gross sales are anticipated to develop at a CAGR of round 0.67% in the identical interval, which I imagine is just too low a forecast given the present tailwinds from the Oncology. In any case, let’s suppose the consensus is appropriate – what does it inform us? Initially, the discrepancy between earnings per share and gross sales development charges tells us one thing concerning the potential for margin enlargement. The market believes that PFE’s EBITDA margin will begin to get well shortly, however apparently not reaching the COVID peaks. The very fact is, nonetheless, that we do not want the previous peaks for the inventory to additionally develop.

As historical past and monetary idea present, an organization’s valuation premium is often defined by both its development potential or persistently high-profit margins. In different phrases, the revenue margin performs a giant function in terms of forecasting the potential worth/earnings ratio in 3-5 years.

If even depressed earnings estimates predict a rise in EPS over gross sales after a spate of detrimental revisions, then the chance of margin enlargement may be very excessive certainly. We have to see at the least some enchancment on this entrance and the inventory worth ought to observe this enchancment, as the present assumption of 9x for FY2028 P/E most likely turns into too low underneath this situation.

It doesn’t matter what conspiracy theorists write, Pfizer is definitely one of many world’s main pharmaceutical firms. Even after a disgusting share worth efficiency in latest quarters, PFE has a market capitalization of ~$153 billion and almost $12.7 billion in money on its balance sheet. Sure, debt has elevated considerably lately, inflicting valuation points, however the debt-to-equity ratio continues to be beneath 1, which is often advantageous for such a big firm, in my opinion.

I believe PFE’s worth/earnings ratio must be round 20x in 4–5 years, which is barely beneath at the moment’s median norms for the healthcare sector. If we assume a conservative consensus EPS of $2.87 (SA information), this leads to a worth goal of $54.7 by the tip of 2028 (100%+ from the most recent shut worth).

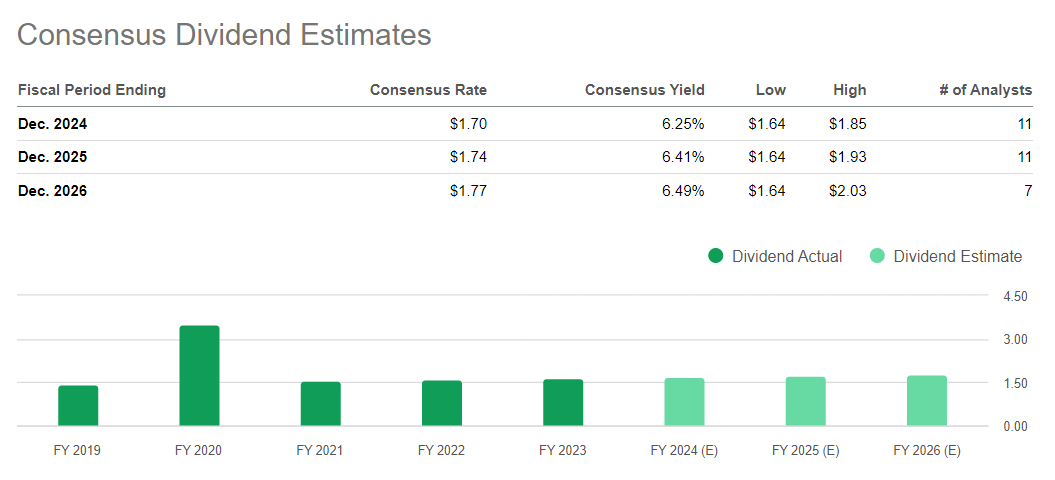

Agree – that is good development potential contemplating PFE pays a 6.25% dividend. Additionally, this yield goes to remain above 6% for the following 3 years, which is illogical if we assume the Fed cuts charges quickly (i.e. the yield ought to fall because of the rise within the inventory).

In search of Alpha, PFE

The place I Can Be Unsuitable?

Initially, I ought to observe that my thesis runs the danger of overestimating the corporate’s operational restoration. I imply, I assumed that Pfizer’s restoration from the COVID hunch is imminent and that the worst is over. Nonetheless, healthcare spending and shopper conduct are unpredictable. The continuation of the Comirnaty and Paxlovid hunch could proceed to influence Pfizer’s monetary efficiency past my present expectations.

Moreover, my bullish thesis relies on optimistic assumptions concerning the development potential of Pfizer’s product portfolio outdoors of COVID-19, notably in oncology. Whereas there are certainly development alternatives in these areas, there are additionally dangers associated to competitors, regulatory challenges, and the tempo of innovation that would influence gross sales and EPS estimates.

It is usually vital to notice that market sentiment – which I anticipate to enhance – and investor conduct might be unpredictable and never at all times consistent with fundamentals. Due to this fact, my assumptions a few a number of enlargement by 2028 are maybe too optimistic.

The Verdict

Regardless of the dangers, I am nonetheless inclined to imagine that Pfizer inventory has grow to be much more engaging now that the market has risen lately with out it.

Sure, maybe pundits have questions on PFE from a technical evaluation perspective, however I take a look at the 3-5-year medium-term outlook and clearly see development factors within the non-COVID companies. The Wall Streetanalysts’ present forecasts additionally level to this, however in my view, their estimates are considerably underestimated. I calculate the expansion potential at 100%+ in 4-5 years – and this does not even embody the dividend yield of 6%+ {that a} potential investor can safe at at the moment’s costs.

I’ve subsequently determined to improve PFE inventory to “Strong Buy” at the moment.

Thanks for studying!