anilakkus

MFA Monetary, Inc. (NYSE:MFA) is an mREIT that invests in loans and mortgages by using leverage to earn earnings. The corporate has been challenged by the restrictive fee coverage of the Federal Reserve. Final 12 months, I wrote about MFA’s convertible note that was providing a high-yield return. Since then, the company has issued a brand new child bond (NYSE:MFAN) providing an 8.875% coupon maturing in 2029 that, I consider, is the perfect earnings funding between its widespread, most well-liked, and debt securities.

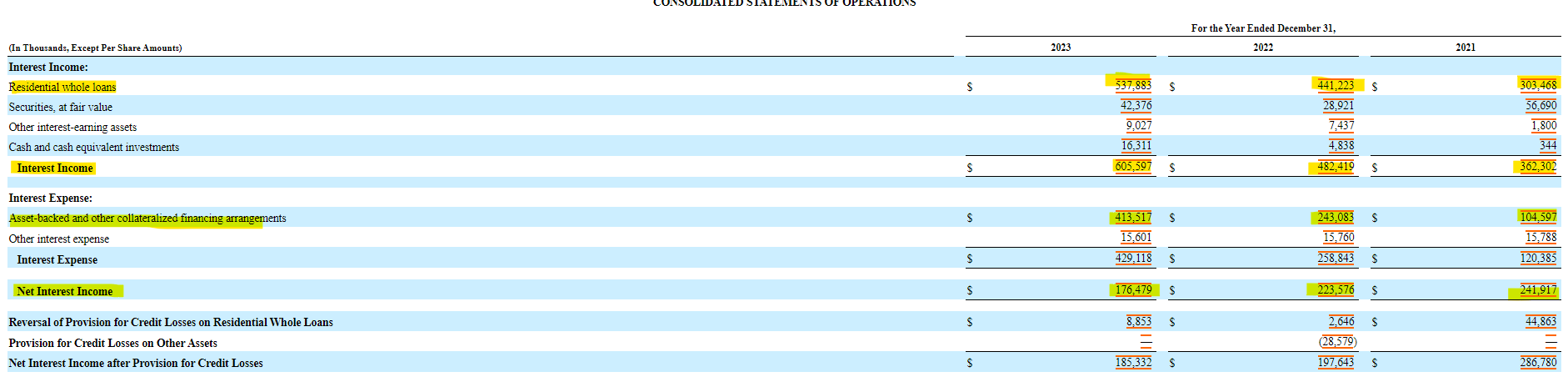

MFA Monetary has seen its profitability erode within the face of upper rates of interest over the past couple of years. Whereas curiosity earnings has risen from $362 million in 2021 to $605 million in 2023, curiosity bills have exploded by 3.5 instances from $120 million to $429 million throughout the identical interval. The top result’s that web curiosity earnings has gone from $242 million to $176 million from 2021 to 2023.

SEC 10-Okay

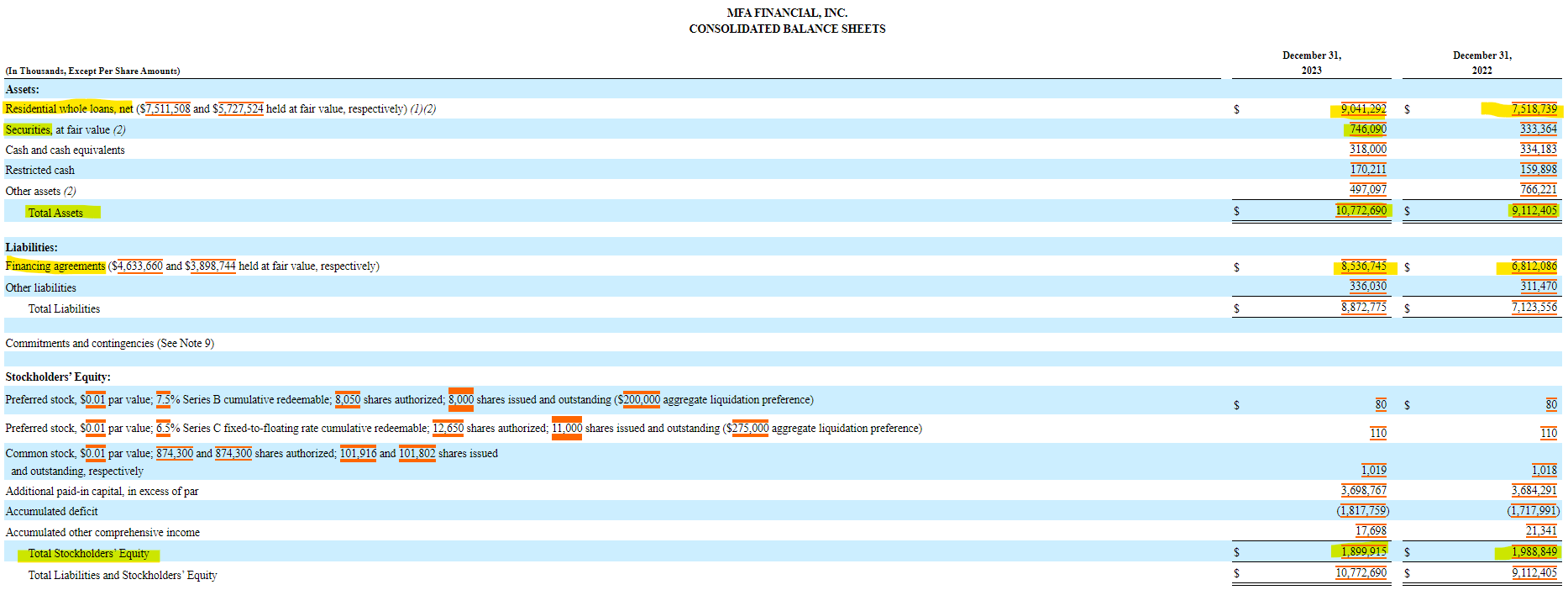

MFA Monetary’s steadiness sheet exhibits a big progress in belongings throughout 2023. The corporate elevated its investments in residential complete loans and securities. The $1.6 billion improve in belongings was primarily led by the rise in loans, which account for greater than 80% of the corporate’s investments. MFA financed its total asset progress in 2023 by way of debt (financing agreements), which elevated by $1.7 billion. The lower within the worth of residential complete loans accounts for the decline in shareholder fairness by $100 million to only below $1.9 billion.

SEC 10-Okay

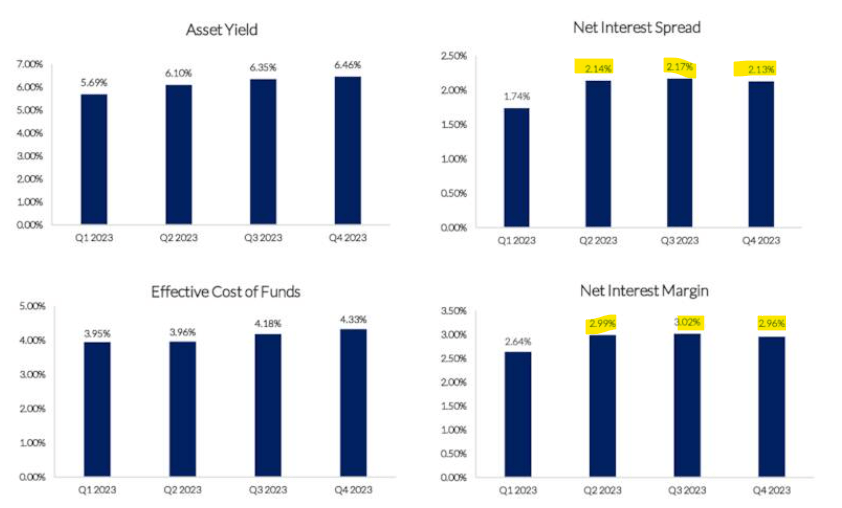

The rise in leverage to spend money on extra belongings throughout a high-interest fee atmosphere appears to be paying off for MFA Monetary. The corporate’s asset yield has gone from 5.69% within the first quarter to six.46% within the fourth quarter. The corporate’s value of funds has grown by lower than that. Successfully, this has led to will increase in each web curiosity unfold and web curiosity margin.

Earnings Presentation

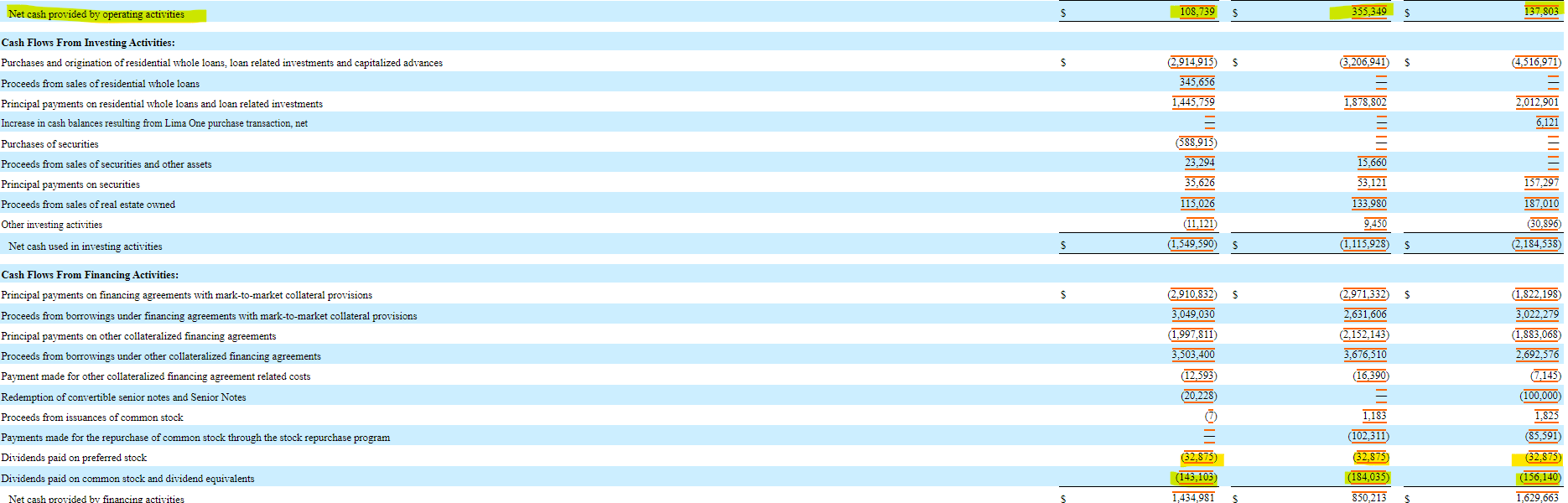

From a money movement standpoint, I often wish to tie in free money movement with the power to fund dividends. Within the case of MFA Monetary, which has no capital expenditure, that process is troublesome. The agency’s investing actions, that are composed of mortgage purchases and originations, are part of the day-to-day operations. It is very important see the dividend obligations for each the popular and customary shares.

SEC 10-Okay

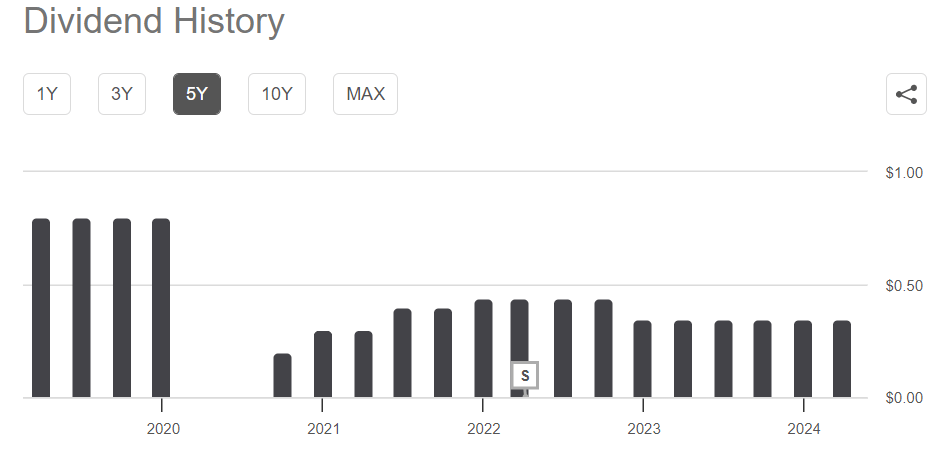

For dividend sustainability, MFA gives distributable earnings to check whether or not or not the corporate is producing the earnings essential to cowl its dividends. Whereas distributable earnings are rising, it was under the dividend threshold three quarters in the past. This tightrope, mixed with MFA’s dividend historical past having a number of cuts over the previous 5 years, makes me uncomfortable with investing within the widespread shares.

Earnings Presentation Looking for Alpha

Rate of interest ranges characterize a key threat to the monetary efficiency of MFA Monetary. The corporate seems to be betting massive that now we have reached the highest of the speed hike cycle. If now we have not, and mortgage charges are to rise, MFA must write down the worth of its belongings, which might push up its leverage ratio. It is also vital to notice that whereas decrease charges will assist MFA Monetary, the drop in curiosity bills could not profit the corporate as shortly as its friends. The 2 highest-interest loans on the legal responsibility facet of the enterprise have charges north of seven% and mature on common between 12 and 21 months out.

SEC 10-Okay

Whereas I’ve nothing in opposition to MFA Monetary’s most well-liked shares (MFA.PR.B) (MFA.PR.C), the Collection B most well-liked share trades at a comparable yield to the newborn bond, and the C Collection trades at a yield of greater than 100 foundation factors decrease. Whereas the C Collection most well-liked share will float at a fee of three months LIBOR (or SOFR) plus 5.345%, that float doesn’t happen till the top of subsequent March. By then, charges might be low sufficient to the place the float fee can be akin to the present child bond fee. The newborn bond gives a pretty coupon of 8.875%, which can give the identical earnings as the popular shares with just a little extra security.

MFA Monetary is making massive bets on rates of interest both stabilizing or declining quickly. The corporate has elevated leverage to spend money on further loans, and part of that capital elevate has been to concern a brand new child bond. Based mostly on the protection degree of every of the securities, I consider the 8.875% coupon child bond is a superb funding for debt and earnings traders alike.